How do you like that confidence?! It’s true though – I am (thrilled to be on the) So Money podcast again! 🤑 And I was…

Money | Minimalism | Mohawks

How do you like that confidence?! It’s true though – I am (thrilled to be on the) So Money podcast again! 🤑 And I was…

The one thing I miss the most from being away from the blog lately is hearing everyone’s stories and how they’ve figured out not only…

What up, what up! Happy New Year! Lol… It’s me J$ – remember that guy?? Mohawk rockin’, FIRE wielding, personal finance nerd who went rogue…

They say that just looking at and touching money makes you happier, so here are a bunch of moneys for you to look at… Be…

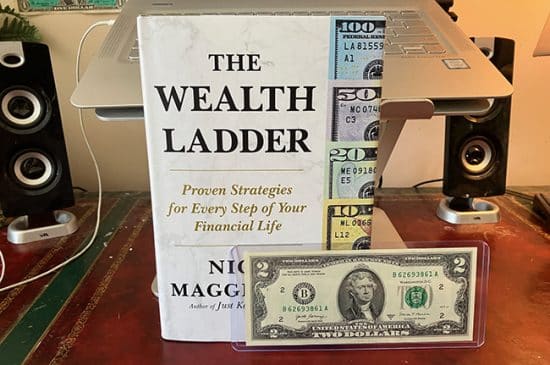

What’s up y’all! My boy Nick’s new book just hit the shelves this morning! “The Wealth Ladder: Proven Strategies for Every Step of Your Financial…

Good morning, friends! Got another great book to give away today! But first – wanted to thank you real quick for all the love and…

Hi all! So I’ve been working on a new project lately, and it’s officially live :) It has nothing to do with personal finance (*gasp*),…

[Good morning, friends! Got a fantastic guest post for you today that’s got me reconsidering all kinds of habits over here! It comes from Amanda…

Morning! So right as I went to hit “publish” on this post, I got hit with a 2nd great credit card tip so you’re gonna…