INSIDE: Are you wondering, “should I buy one stock or multiple?” Or maybe putting all of your eggs in your basket sounds crazy. Here’s why I did it and how it went.

Today’s post may surprise you, scare you, or even enlighten you (maybe all three?), but I’m sharing it with you anyways because that’s what us financial bloggers do. We dish it out exactly how it plays out in our lives, and then we leave it open for every jackal with an internet connection to either praise us or kindly debate what big idiots we are.

And I love every moment of it :)

Should I Buy One Stock or Multiple? Here’s What I Did

[This is the opposite of what financial planners are allowed to do btw – which is why I’ll never be one. Sharing general investment advice online with you may be fine, but I’m not interested in generalities here – I want to show you specifics so you can get a real life example of how people manage their money, and then make your own decisions from there. It’s what makes blogging so great – real life stories from real life people doing real life things! Just don’t sue me*, okay? ;)]

The Background

If you recall, last month I decided to get off my ass once and for all and start paying attention to my investments again. There’s tons of stuff in this life that I’m good at (saving, hustling, getting the money TO invest somewhere), but the one area I’ve failed over and over again in is coming up with a robust investing strategy. Though I was never shy at getting creative.

Here were the last two strategies I used in maxing out my RothIRA:

- The “Copy what Warren Buffett is doing” Strategy

- The “Invest in the companies you love (and use)” Strategy

It’s literally been years (2? 3?) since I last paid real attention to all my investments (other than pouring in the money), so I finally pulled the trigger and made the switch from USAA to Vanguard, effectively ending my “all accounts under one roof” mantra I had lived all these years. That tells you how much I believe in this new strategy though. Or, more specifically, Vanguard.

I won’t go into all the details again as to why I want to make sweet passionate love with them chose them (you can read all about it here), but in a nutshell:

- I wanted to simplify

- I wanted to be lazier

- I wanted extremely low fees

- I wanted a place I could trust and love as much as I do USAA

- And at the end of the day I didn’t want to think about it any more

These are the three main posts that eventually led to this “a-ha” moment:

- Portfolio ideas to build and keep your wealth @ jlcollinsnh

- How to make Money in the Stock Market @ Mr. Money Mustache

- Thriftygal’s Money Strategy @ Thriftygal

Prior to this move I had a total of 5 separate investment accounts – A SEP IRA, a Roth IRA, and three Traditional IRAs (remember my crazy IRA Test??) – and I was finally done dicking around once and for all… I needed a plan that was much more aligned with my new found vision here, which was basically:

Find a smarter, lazier, way to grow my money

Meaning, set up a plan that EMBRACES laziness, but one that makes sense and fully allows you to “set it and forget it” while making a decent amount of money too. Keyword being, *decent*. I’m not out to become a billionaire over night (though that would be nice!) but I do want to make a fair amount over time and I’m totally fine being patient and waiting for it. The whole 80% type deal. I’ll gladly take 80% of a total 100% amount of money for minimal effort vs 90-100% and killing myself to get it. Which of course is never guaranteed since we all know you can’t time the market anyways (you do know you can’t time the market, right?).

Should I Buy One Stock or Multiple? I Chose the Lazy Way

So after all my reading and thinking, I came to the conclusion that it’s all about INDEX funds for me. No more fancy stock picking, no more weird strategies of picking out my favorite companies, just plain ol’ “you make money when the overall stock market makes money, and you’ll lose money when the overall market loses money.” (Which is when you pick up even MORE shares, btw!). And if you believe in the markets all around, as I do, then why not cast a wider net around it?

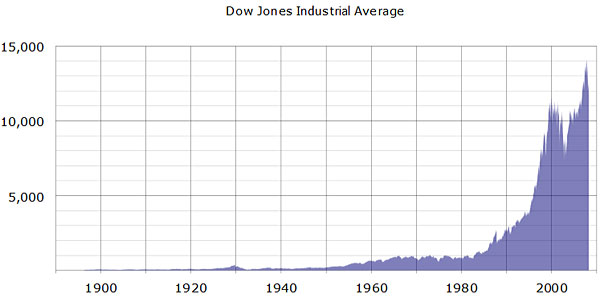

Here’s a graph on how the Dow has performed over the past 100 years, even though it needs to be updated (we’re now hovering around the 17,000 mark):

(Hat tip to Thriftygal / Wikipedia)

If you think it’ll continue going up in the long term, then you might like Indexing :) It certainly has its fair share of supporters not only from the personal finance blogger world, but also Vanguard itself (d’uh – they INVENTED index funds!) and even the main man himself, Mr. Warren Buffett. Who recently turned heads when he shared that he wants his own estate to go almost entirely to index funds once he’s outta here. And he’s the smartest investor of all time!

I called up my stock broker friend to get his advice on this too, and he just laughed at me. I asked if he hated Vanguard, and he said no. He hated how boring it was! I told him luckily I wasn’t in it to have fun (even though “fun” is in index FUNds – zing!), I was in it to win it ;) And according to everything I’ve read, statistically the odds are in your favor going this route than others long term anyways. Even my stock friend gets it wrong and he spends 60 hours a week researching this stuff!

But I digress…

Here is what I used to be invested in:

To put things in perspective, here are all the stocks I used to own as of a month ago. $350,000+ invested, and I couldn’t tell you what half these funds consisted of, nor their expense ratios (partly because I never paid attention, and partly because it’s confusing as hell):

- USEMX — USAA Emerging Markets Fund

- USAAX — USAA Growth Fund

- USHYX — USAA High Income Fund

- USAIX — USAA Income Fund

- USISX — USAA Income Stock Fund

- USIBX — USAA Intermediate-Term Bond Fund

- USIFX — USAA International Fund

- USAGX — USAA Precious Metals and Minerals Fund

- USRRX — USAA Real Return Fund

- USSPX — USAA S&P 500 Index Fund Member Shares

- USSBX — USAA Short-Term Bond Fund

- USCAX — USAA Small Cap Stock Fund

- IIBWX — Voya Intermediate Bond Fund Class W

- UCAGX — USAA Cornerstone Aggressive Fund

- USCRX — USAA Cornerstone Moderately Aggressive Fund

- USSPX — USAA S&P 500 Index Fund Member Shares

- URFFX — USAA Target Retirement 2050 Fund

- USAWX — USAA World Growth Fund

- ABEYX — American Beacon International Equity Fund Class Y

- DDVIX — Delaware Value® Fund Institutional Class

- SGOIX — First Eagle Overseas Fund Class I

- HLMIX — Harding Loevner International Equity Portfolio Institutional Class

- HNVIX — Heartland Value Plus Fund Class Institutional

- HWSIX — Hotchkis and Wiley Small Cap Value Fund Class I

- EMBIX — Lazard Emerging Markets Equity Blend Portfolio Institutional Shares

- LISIX — Lazard International Strategic Equity Portfolio Institutional Shares

- LKSMX — LKCM Small-Mid Cap Equity Fund Institutional Class

- MFEIX — MFS® Growth Fund Class I

- PTTRX — PIMCO Total Return Fund Institutional Class

- SEMNX — Schroder Emerging Market Equity Fund Class Investor

- TGEIX — TCW Emerging Markets Income Fund Class Institutional

- AMZN — Amazon.com INC

- PNRA — Panera Bread Company Class A

- SBUX — Starbucks Corp

- TGT — Target Corp

- TJX — TJX Companies INC New

- ALLE — Allegion Public LTD

- AXP — American Express Company

- T — AT&T INC

- CSCO — Cisco Systems INC

- KO — Coca-Cola Company

- COP — ConocoPhillips

- ETN — Eaton Corp PLC

- GE — General Electric Company

- IR — Ingersoll Rand PLC

- WFC — Wells Fargo & Co NEW

- XLP — Sector Consumer Staples Select Sector SPDR ETF

47 total stocks/funds. Ridiculous.

And here’s what I’m Invested in now:

- VTSAX — Vanguard Total Stock Market Index Fund Admiral Shares

Yup! My answer to “should I buy one stock or multiple?” is now, one.

Just one kick-ass fund :) And I know exactly what’s in it (3,671 stocks), and exactly what the expense ratio is (0.05%, lower than 95% of similar funds out there). And the beauty is it holds all my favorite stocks too, like the Amazons and Targets, and even more so Warren Buffett’s Berkshire Hathaway! UPDATE: It also has a dividend of 1.84% – forgot to mention that earlier (hat tip to “Whiskey”).

Here’s more about the fund according to Vanguard:

Created in 1992, Vanguard Total Stock Market Index Fund is designed to provide investors with exposure to the entire U.S. equity market, including small-, mid-, and large-cap growth and value stocks. The fund’s key attributes are its low costs, broad diversification, and the potential for tax efficiency. Investors looking for a low-cost way to gain broad exposure to the U.S. stock market who are willing to accept the volatility that comes with stock market investing may wish to consider this fund as either a core equity holding or your only domestic stock fund.

(Vanguard has an “Investor shares” version of the fund too, fyi, for those who can’t invest $10,000 or more into the fund (VTSMX). The expense ratio is a tad bit higher @ 0.17% (still drastically better than 87% of the competition) but the stocks you hold here are exactly the same)

Now it may look dumb/scary to “have all your eggs in one basket” here – which was my first concern – but the reality is it isn’t just one stock. It’s one stock ticker, but over 3,600 stocks (ie companies). When you invest in index funds you invest in itty bitty fractions of hundreds/thousands of companies. If any one of them die out at any time, it doesn’t kill your money.

See! Answering “one to “should I buy one stock or multiple” isn’t really as scary as it sounds.

But on the flip side, it doesn’t grow your money as fast either like, say, if one of them takes off like Apple. It’s an average person’s game, with better than average results over time (and by “average” I mean compared to most of those day traders and probably your friends).

There are, however, downsides to this VTSAX strategy, specifically you’re not invested in bonds or international markets at all. But at this stage and age of my life I’m okay taking on more risk (ie no bonds), and most, if not all, stocks in VTSAX does business around the world anyways. So from my understanding you still do have exposure to the foreign markets, just not directly like, say, by investing in funds that hold actual foreign companies.

This is one area I’d like to learn a lot more about, though, so if any of you care to chime in with thoughts I’d love to hear them! I’m definitely learning as we go here.

VTSAX vs. VASGX

The other fund I was considering, if you’re interested, was VASGX (Vanguard LifeStrategy Growth Fund). This is the fund Mike Piper from Oblivious Investor has every one of his retirement pennies in (see, I’m not the only crazy one!), and which is still aggressive’ish, but less so than VTSAX. I debated hard going this route instead -which would still be just ONE fund, only diversified more, but ultimately chose the more aggressive route – at least for now.

(And btw “aggressive” in index funds is much different than “aggresive” in stock picking :) With one you’re invested in hundreds or thousands of companies and the other you’re invested in a single company. So “risk” here is different)

Here’s the quick bio on this fund:

The LifeStrategy Funds are a series of broadly diversified, low-cost funds with an all-index, fixed allocation approach that may provide a complete portfolio in a single fund. The four funds, each with a different allocation, target various risk-based objectives. The Growth Fund seeks to provide capital appreciation and some current income. The fund holds 80% of its assets in stocks, a portion of which is allocated to international stocks, and 20% in bonds, a portion of which is allocated to international bonds. In addition to stock market risk, the fund is also subject to currency risk and country risks. Investors with a long-term time horizon who are looking for growth of principal over time and who can accept stock market volatility may wish to consider this fund.

And here is what VASGX holds:

- 56.1% — (VTSMX) Vanguard Total Stock Market Index Fund Investor Shares

- 24.0% — (VGTSX) Vanguard Total International Stock Index Fund Investor Shares

- 16.0% — (VTBIX) Vanguard Total Bond Market II Index Fund Investor Shares

- 3.9% — (VTIBX) Vanguard Total International Bond Index Fund

So as you can see, almost half of the fund covers international exposure along with bonds, and only 56% of the fund I’m currently invested in (again, I’m in the “Admiral Shares” version of VTSMX since I have more than $10,000 invested taking advantage of the lower fees). And this VTSMX has a low expense ratio too of only 0.17%.

When I asked my good blogging friend Jim Collins what he thought between the two, whom I trust heavily since he’s been retired for over 20 years and only invests in index funds & Vanguard himself (he’s in a few vs one due to his age and phase in life), he told me this:

VTSAX is the total US stock market index: 100% US stocks. Holding VTSAX is very aggressive. Recommending it as a sole holding, as I do, is very much an outlier concept. In fact I am aware of no other financial writer who does. So Mr. Piper definitely has the majority opinion on his side.

Holding VASGX is also very aggressive at 80/20, but less so than VTSAX… also with it being a fund of funds, the ER is a bit higher. You are paying for that multiple fund diversification.

It is certainly not a dumb choice. As you know, personally my preference is VTSAX. But I am Very aggressive in my investing and have proven my ability to stay the course during crashes. That’s absolutely critical, with either of these actually.

Looking 20+ years out, VTSAX will very likely make you richer, unless we go the way of Japan. But the race will be close and your savings rate will be the more powerful element in the mix than your fund choice.

I then asked what he would do if he were me and he responded with:

Yep, if it were my money I’d do VTSAX. In fact I do, 75% and the other 25% in bonds. Then I just rebalance occasionally to keep the percents where I want them, Easy peasey and cheaper ERs than with a TRF.

If I were still working and adding new money it would be 100% VTSAX. The new money has the same kind of smoothing effect as the bonds do for me now.

It was at that point I pulled the trigger :) I don’t have a problem with risk(ier) – I’m young and have plenty of time to ride the waves! Plus you can always tweak it later as life changes.

Final thoughts about should I buy one stock or multiple

So, in a nutshell I used to be invested in over 45 stocks/funds across 5 different retirement funds, and now I’m only invested into ONE fund across 2 accounts: my SEP Ira and my ROTH Ira.

(Did you know you can merge Traditional Iras with SEP Iras btw? According to Investopedia, “The only difference is that the SEP IRA is allowed to receive employer contributions. Therefore, you can combine the SEP IRA into the Traditional IRA without any ramifications. When doing so, move the assets as a (nonreportable) trustee-to-trustee transfer.” I had no idea!)

And now, instead of all my investments under USAA’s roof where my other 10+ accounts are sitting, it’s all under the roof of Vanguard. And with a much better peace of mind too. It sucked to research everything and figure out what’s best for our family at this stage of the game (again, this stuff doesn’t interest me one bit!), but it had to be done and now we can go back to doing what we do best – MAKING money vs investing it ;) Or rather, finding the best place to invest it. Now we’ve got a solid foundation!

I know this post was pretty damn long, and I probably forgot a few things along the way, but I DO hope it helps :) Even if just a little. Remember that there is never a one-strategy-fits-all here with investing (just like with managing your money), but there are templates that get you close. And I hope this gives you another idea to either love on or hate on depending on your own style .

Let me know what you think in the comments below! Was this a smart move? Would you have done something differently? Are you doing something similar now? Please share any and all thoughts with us (even your OWN portfolio mix!) so we can all learn more… Most people get more out of the comments here than they do my posts anyways (hah!) so if not for me, do it for them ;)

Here’s to financial freedom!

———-

* Seriously, I’m not a licensed profession. Please take all this as informational purposes only and do your own research before investing in anything. I love you and want to keep blogging transparently but I can’t if it becomes a problem :)

PS: Btw, for anyone who’s making the switch to Vanguard, make sure to ask them the best way to xfer your funds from your old account to theirs – specifically with “cashing out” of your old funds and into new Vanguard ones… There’s ways you can save the selling fees that they can help you with – the one question saved me at least $400 when doing all the trades at the end. And fyi you can also just move your same funds to theirs too and then pick the new funds later. Just ask them what’s best as they’re customer service is killer :)

PPS: I have no affiliate with Vanguard at all and certainly not getting paid to say kind words – I’m just their newest fanboy!

[Funny cat canoe by Elvis Weathercock]

Get blog posts automatically emailed to you!

I haven’t invested in any of the stocks that you listed, but I have tried to invest in a farm land before. It was a pretty good investment, but after 2 years the owner claimed his loan farm land to me.

Farm land? How does that work?

Nice. I too have considered Vanguard and will probably make a jump once the employment situation changes. Their 401k stinks but its free $ so…

I dont remember if you said you use Personal Capital but if so, have you run the tool before and after to see what you will be saving in fees?

It also looks to return dividends which is freeeeeking sweet. Looks to average .15 per share so @ 3500 your getting $555 per year. Extra cash, yessss! Do you plan to reinvest?

Keep us updated on its progress. It keeps us minions motivated.

Yeah, that’s the prob with 401(k) – outside of our control :( But you’re right – can’t pass on the free money! I’d take that over great funds any time – your investments compound like crazy!

RE: Personal Capital – I have poked in there before, but still need to go back and really check it out. People have been raving about it (especially investor people since it focuses on investments) so thx for the reminder :)

RE: Re-investing – Hell yeah man! All day, every day! Can never touch that money – gotta keep re-investing and pouring in more over time to speed up the compounding :) And fortunately it’s all automatic these days so you don’t have to lift a finger!

Ooof! Just realized that its not 555 per year, its more like over 2300 per year. Thats uber sweet!

Hmmmm…Gonna be the “devil’s advocate” because…well…I worry. I have an investment with Vanguard’s competitor TIAA-CREF….and the returns the last couple of years have been no less than remarkable. BUT when you start looking into the many funds and how they are invested into other funds inhouse it’s like a “house of cards”. Secondly in a time when it costs me $125 just for repairman to show up at rental property, the folks at Vanguard are going to manage the investment for .05%? Sooo to manage a $300,000 account they recieve $150…per year… for their work….How do they keep the lights on? I reviewed my Tiaa-Cref accounts and saw that these guys were “killing me” at .45%. Sooo that same $300,000 account would pay $1350 in management fees per year. A lot of money BUT last year these funds returned 36 and 38% respectively …so maybe the fee was worth it. I worry about the “herd mentality” BUT what I worry most about is energy prices. Make no mistake higher energy pricing is a “direct tax” on business and life in our Country.

I don’t know squat about energy prices, but here’s a good quote from Kiplinger on why Vanguard rates are so low – it’s pretty unique:

“From the day John Bogle started the firm in 1975, after being fired by Wellington Management, Vanguard was a different kind of fund company. Instead of being owned by a money-management firm (or a bank or an insurance company), it was set up essentially as a co-op, to be owned by the shareholders of its funds. Unlike other fund companies, Vanguard makes no profit. It sells all of its funds without loads, or commissions, and the company insists on ultra-low fees because that’s what the owners want and because lower costs lead to better results. The alignment of Vanguard’s interests with those of its customers is the foundation of the trust the firm engenders among its clients.”

Sorry J. ….I’m a worrier and Bernie Madoff is fresh in my mind. I think John Bogle is a wonderful gentleman…however Vanguard has “overhead” like everyone else and they need to pay a decent wage to keep competent help. Not a fan of Kiplinger any longer they have truly lost their way and when they say Vanguard is “unique”….I put that in the same category as …”it’s different this time”. I can appreciatte you “simplifying things” but take a moment and take a look at TIAA-CREF. IMHO these guys are “really unique”….like “thinking out of the box”…to the point that TIAA-CREF is now one of the largest owners/producers of almonds in California. For the record almonds in this neck of the woods are almost $9 a pound….

The control 190.1 Billion in assets so at .04% the make roughly 7.6 Billion per year. I think they can hire a lot of repairmen 29246 Full Time ($125 repairmen per year)

Vanguard has over $2 trillion AUM (assets under management). Their revenue is quoted as $2.3 billion which puts them at an average fee load of .115%.

Not sure what there is to be skeptical about. They are making almost $200k per employee for funds that aren’t actively managed. They don’t pay their employees the most, either (I have multiple friends who work there). Frugality pumps through their veins – employees share hotel rooms, don’t take accela or business class when taking amtrak, etc.

Vanguard is unique in that they are the low cost leader of the investing world.

I am happy to find out that we share the same investing strategy! haha. It’s a great one. I will say that maybe in the future I’d like to be more involved in evaluating companies and picking stocks. But right now, since I can’t commit to that kind of time, I go with the index funds and that is just fine with me.

Exactly. In a perfect world we’d all have time to spend learning all kinds of things! But sadly we have to prioritize and at this point I’m perfectly fine setting it up and then letting it ride while I go and live my life :)

When I saw the list of what you did hold, my jaw dropped! That was A LOT of investments. When I worked for a financial planner, I typically dealt with new clients so I would have to organize all of their holding onto a spreadsheet. Some people hundreds of funds. This one guy had 7 printed Excel pages worth of holdings. I just shook my head.

Personally, I’ve never heard of this one fund being someone’s entire portfolio. I have heard of (and even recommend) just 3 fund portfolios). While you are completely diversified here in the US, the lack of international exposure could be an issue. Yes, many of the companies in this fund do have international sales, but the question is what percent of the companies and what percent of their sales. Personally, I wouldn’t want to do that research to figure it out. My guess is that is rather low. I would want some more exposure to international markets. But that said, things are different now. We live in a global economy. Back when people were recommending portfolios, economies were more insulated.

In the end, I say just run with what you have and see what happens. As with what Jim Collins said, your greatest risk is that we turn into Japan. But I think everyone will feel that if it were to happen.

Yeah, I might eventually go the 3-fund portfolio route, especially after seeing everyone else’s comments below talk about it too, haha. It very well could be smarter, but for now I’ll lay low and enjoy not worrying about it for a while :)

Investing scares the crap out of me. Most of our investments are tied up in 401Ks but we inherited some individual stocks a couple years ago. The returns have been fantastic, but part of me really would like to move some of that money into index funds. Too much of our stocks revolve around the banking industry, which is terrifying. We somehow need to emotionally detach ourselves from these stocks, but since they were inherited it’s hard not to mentally link them to the person who passed on.

Emotions are everything with investing! And not always for the good, as you’re finding :( Definitely might be worth talking with someone, or reading some of those links I posted above to get an unbiased opinion on things. It’s always much easier for an outside person to share advice since their emotions are out of it (unless they’re getting paid to sell you something, haha…).

Absolutely love it. J$, welcome to the good life!

I was partially prompted by our chat on your podcast :) Next time I’m on you’ll have to ask me how it’s going so I can redeem myself!

Wow, 47 different holdings! The crazy thing is I used to speak to people that had at least double that. I always wondered how on earth they managed that many and the fact is they probably didn’t manage it very well as who can keep up with 100+ holdings…unless you’re Buffett of course. ;)

I was at the Berkshire annual meeting in May and they were asking him about his statement on Index Funds and it was just crazy. They thought he was trying to say something about his company and he finally said something along the lines of “Listen, being with the market is much better in the long run and will do quite well for my heirs”. Point being, if he thinks it’s good enough for his family then I think it’s good for many. With all that being said, I’m at about a 70/30 mix between several index funds and the rest is largely some solid dividend paying stocks.

Re: Personal Capital – I just started using it several months ago and it’s a great tool to use.

It’s all about working smarter. Sounds like you streamlined your investing process in a way that works for you. Bravo! It’s nice to feel organized and in control. Gives you a lot of peace of mind that’s for sure : )

Same story here, but in went with a Vangaurd a Target Date Retirement Fund. Even less work for me to do! Automatic rebalancing!

There you go! Slightly higher expense fees, but worth it for 100% laziness! :)

Holy Cow you were investing in 42 different things?… there’s diversification and then there’s that! hahaha

I have Vanguard for my Roth and couldn’t be happier. The fees are very low and I love the fact that I don’t have to worry about what I’m investing. I’m just as lazy as you and stayed with an index fund.

My Roth IRA is composed as follows: VTSAX (60%) and VTIAX (40%). I maxed out the account at the beginning of 2014 and have barely looked at it…except when I receive the quarterly dividends. Lazy, indeed.

Hey man,

I also LOVE VASGX, and we have all of our retirement funds in the fund (or model the fund in the case of my 401k). One thing though – it isn’t a retirement fund like Mr. Collins mentioned, and currently as structured will not add more bonds as time goes on. VASGX is a fixed 80/20 stock/bond fund, not a TRF (Target Retirement Fund). If you’re looking for a TRF with a current 80/20 stock/bond allocation, that would be either VTTHX (currently 84/16 stock/bond), or VTHRX (currently 76/24 stock bond).

Hi Big Guy…

You are absolutely right!

VASGX is what Vanguard calls a Life Strategy fund. Very similar to a TRF with the exception that, as you point out, the allocation remains fixed.

Thanks!

No problem – glad I could help :)

Updated the post so it’s more accurate – thx guys :)

With my Roth IRA, I have been lazy since the beginning in 2007. It’s always been in a Vanguard target date mutual fund – invested high in lots of stocks now and adjusts as you get older to shift more into bonds.

Your last Vanguard post actually inspired me to open up a Vanguard account. I have a chunk of my money in the Admiral shares too just so I don’t have to think about it. I’m also (still) planning to rollover my old 401(k) there to do the same strategy too.

I still play around with some money in other investing strategies but over time that pot of money has gotten larger and the volatility stresses me out more because of that. So taking some money out of my hands and putting it somewhere I don’t have to think about it eases my mind.

Oh, great! Welcome aboard – we’ll be newbie members together :) Now hurry up and get that old 401(k) moved over! I literally just called them and they did it all for me over the phone – it’s pretty easy…

Very nicely expressed post, J$…

Thanks for the kind mentions. Although you did promise not to use that picture of me in the canoe…

Let me also add, I use VTSAX not only because investing in index funds is easier, which it surely is, but because it is more effective. If better results were to be had holding a more complex mix, that’s what I’d do.

I laughed when I saw that huge list of holds you used to have. Yet, while I never had quite that many, I wasted the 80s and 90s doing much the same.

May I add another to your list of three influential posts?

http://www.gocurrycracker.com/reminiscing-about-the-glory-days-of-2008/

GCC is one of my favorite travel bloggers and he does a fine job of writing financial post when he so choses.

Big thanks to you for giving me the final push to take action :) And, really, the first few pushes too as it usually takes me a while of hearing the same thing over and over again – and in different ways – for it to finally sink in! I guess that marketing saying that we need to see stuff 7 times holds some truth. Only the application here is much MUCH better for your ultimate worth ;)

Going now to add that link to my bookmarks to check out later – thx.

Thank you Jim, you are too kind. I’m blushing all shades of red over here

The picture of Jim in the canoe was my 3rd favorite part of this post

We managed to get over the “diversity through too many different funds” phase at some point, and I think are better off for it. We are getting closer to 100% VTI / VTSAX and I don’t think it aggressive at all, primarily because of 3 things

– come nuclear war, the next black plague, or Armageddon, we will never sell

– our withdrawal rate is low enough to allow us to never sell (the closer you get to living exclusively off the VTSAX effective payout, the better off you are)

– did I mention we will never sell?

With those 3 very important things in mind, going 100% stock is a great move. I approve ;)

Short Term, all in one basket thinking is not prudent. I believe now is the time to store some cash to take advantage of opportunities. 100% in Equity doesn’t allow for this. At the most aggressive, i only recommend an Equity Portion of 70%, but at the obvous bottom of a market cycle like 2009, an 80% Equity position is fine, provided your time horizon is more than 12 years. Good luck, a market correction is coming at some point.

I’m more aggressive as well when it comes to investing, retirement investing is a little different as I prefer a good mix of boring. My investments are spread out over 4/5 index funds. I agree with Mr. Collins it might be just a big aggressive, but I don’t think it’s the craziest thing I have ever heard of(45 different funds sounds crazier to me).

The general concept of a index fund over a single company stocks works for me. I see Target was one of your single stocks, I wonder how they preformed since the identify theft / credit card issues during last Holiday season? I’d take the slow and steady path in the index fund over single stock path any day.

That’s a good question? I bet you can find out with a quick online search or two… I won’t do it though in case it tanked, haha… I have happy thoughts with Target after all these years of investing in them!

47 line items!?!?!?!?!?! You had more than clients of mine who have 3x the investments, but I am glad that you have finally seen the light. 90% of investment returns come from asset allocation and only 10% on the type of asset you have. So it really doesn’t matter much how you get stock, bond and other exposure, just that you have some mix of it. I like life strategy funds like the one you mention because in essence you are telling the portfolio manager what your goals are and they manage and rebalance you all the way there. Your strategy isn’t lazy, it’s KISS – keep it simple stupid which is the best way to manage money over the long haul.

I’ll be KISSing my money come 20-30 years, that’s for sure!

I’d like to add an important point to this…

The strategy is great and I’ve been following the same one since 2004 (I got the lowdown from fool.com and went 100% into VFIAX). It only works if you can stomach the crashes. Those risk profile tests could be beneficial. Imagine that tomorrow, the stock market crashes 10%. Then 8% the next day. Oh no, what is the bottom going to be? What do you do? If your answer is “sweet, I’m dollar cost averaging like a boss and getting some cheap shares,” then this is the strategy for you. If your answer is, “Shitballs, I’m going to sue J. Money while I move these to bond funds,” then you shouldn’t do this strategy. I believe this strategy works, but that people don’t. For the record…I can stomach the crashes like a boss.

Nice!! VFIAX, eh? Didn’t come across that one in my readings but seems to be similar – I love it. And great point indeed. I typically freak out just a little, but never to the point that I’d ever hit cash out since I’m in it for the long haul and always plan on picking up more to your point of dollar cost averaging. So I’m like 75% boss in those situations, which is fine by me :) You need the risks to get the rewards!

0.05%??? Holy macaroni, that’s cheap!

Here’s the deal: I think this is a fantastic strategy. From the standpoint of reducing the amount of time spent worrying and researching investments, it’s a tremendous savings. Think about it: Now you can spend your time doing something else while your money is at work! The one cautionary point is that you may be too diversified in the stock market with a fund like this… It offers little risk protection through bond funds. Otherwise, I like your thinking here. Might just have to follow it!

Let me know if you do! Def. not thinking about investing for quite a while, haha… I had my fill trying to figure out all this over the past cple months :) Only thing I’ll be thinking about is pouring MORE into it now!

Did you look into VMVAX as it has an expense ration of .09 and has outpaced VTASX for the last three years. I have most of my money in it.

I don’t know if it’s entirely fair to compare the returns of VMVAX against VTSAX. VMVAX had its inception only 3 years ago, and one of those years (2013) was a HUGE bull market. So that will account for a lot of the weight of the returns for VMVAX. VTSAX has been around much longer, so its returns have had more time to average out.

No, hadn’t checked out VMVAX but will, thanks :)

And thanks for chiming in Josh! I suck at keeping things in perspective totally when comparing funds – I rarely look at how long they’ve been around for! Probably need to change that.

You’re welcome!

I’m no pro myself, but I do read A LOT of personal finance material (obviously including budgetsaresexy.com). It’s always said that past results do not predict future returns, but I feel with huge index funds like this (that hold positions in hundreds or even thousands of companies) this is actually somewhat true (over the long run, which is all we care about right now anyways). So in these instances, it’s good to look at 3,5 and 10 year returns (if applicable) as well as returns since inception (and of course, inception date).

Excellent! John C. Bogle would be proud. His “Little Book of Common Sense Investing” makes it very difficult to argue against this strategy. Here are a few quotes:

p. 83 – Only three out of the 355 equity funds that started the race in 1970—8/10 of 1%—have survived and mounted a record of sustained excellence.

p. 87 – “Even fans of actively managed funds often concede that most other investors would be better off in index funds.” – Jonathan Clements

p. 135 – It may not be as exciting, but owning the classic stock market index fund is the ultimate strategy. It holds the mathematical certainly that marks it as the gold standard in investing, for try as they might, the alchemists of active management cannot turn their own lead, copper, or iron into gold. Just avoid complexity, rely on simplicity, take costs out of the equation and trust the arithmetic.

Bet you’re feeling even better…Congrats for making a great choice.

Oh yeahhhhh, sure am! Thanks for the confidence boost :)

We’ve been at Vanguard for years and love the “invest in it and forget about it” philosophy. We have the 500 Index fund and the Total International Stock Market fund. I think you made a good choice getting out of those 47 different investments. Seems like there may have been a good deal of overlap there in some of those funds…and a lot to keep track of.

Awesome. I actually have VTSAX written on a post-it note by my computer from comparing/researching my funds a while back (I have a few different funds. Not 47, but a few, haha). I’m pretty new at the whole investing thing, so it’s good to read that I’m on the right page.

Sweet! You sure are :) At least if you like index funds and keeping things simple, haha… Let me know what you end up doing later :)

I do index investing at Vanguard as well. My only problem with using just the VTSMX fund is that it is highly weighted on Large Cap US stocks, so I would try to add in a small cap index fund (VSMAX), a mid cap index fund (VIMAX), and an international fund (VFWAX). I just recently added the REIT index fund (VGSIX) to my portfolio as well. 5 funds total, a bit more complex than 1 index fund, but no where near as hectic as 47! All still index funds, but giving a broader overall exposure.

Probably a safer bet for sure… Doesn’t it get annoying to split up the money though every time you put some in? or do you do it at the end of the year or something? Probably not the biggest deal in the world, but enough to get me to pause – as sad as that is :) We’ll have to see how many I get into down the road though, or if I’ll stick w/ just the one. Either way, I’m totally convinced index funds are the way to go for me, which is the biggest battle.

We basically just have one fund in each account. My wife has a 401K at work that we use the Total stock market fund in. We each have an IRA and a Roth IRA, and we have an HSA. Each account and fund there in gets an automatic investment every week, so no work splitting them up required. All I have to do is make sure the bank account has some money. I suppose this could get troublesome if/when we decide to do some re-balancing, right now we are in the early stages of acquisition so re-balancing isn’t a big concern right now.

Ahh gotcha, yeah that def. makes things easier – good call.

Couldn’t you just buy VTSAX ($10,000) instead of buying VSMAX ($10,000) and VIMAX ($10,000)? VTSAX contains large, mid, and small cap I believe, so wouldn’t it be wiser to just buy VTSAX instead of investing in the separate mid and small cap investments? I thought VTSAX was already broad by itself, but maybe you buying the others increases your diversity, thus increasing your returns over time.

Welcome to Vanguard! I love having my accounts there! It’s always good to simplify unless you’re into the world of stocks. I’m not so I use Vanguard:P I still have my retirement accounts in a good place and I just check it every now and then.

Are we twinsies? I just moved my entire Roth over to VTSAX last week. wtf?!

My 401k only index option is VINIX, but it’s MUCH lower cost (and performs better overall) than all the other crap in there.

Here’s to “losing” half our money in the next crash! ;-)

HAH! Would you look at that :) And we have BUDGETS in our blog names too – BAM x TWO!

Woot! Great minds…

Awwww yeaaaah!! Vanguard fanboydom commence. Glad you finally pulled the trigger.

I do think a little international and real estate index exposure would be wise, but VTSAX is a good strategy.

Hey, any company that mails you a mug and coffee after a Twitter convo is a-okay in my books ;) Just strengthened my decision even more! (Yes, I can be bought pretty easily)

Wow, that was quite a cluster of funds you used to own. I like the fact that you are simplifying your fund line-up and making things less complex. But I think you could diversify just a bit further by adding the VG Total Int’l Stock Fund. Yes, US companies are much more global than they’ve ever been, but int’l mkts have different industries, growth prospects, dividend yields, etc. They also don’t always perform in line with one another so you could take advantage by rebalancing periodically between the two funds to increase performance.

Either way, the biggest drivers of your success with be your willingness to stick with the fund(s) you choose and your ability to invest when stocks inevitably fall — so you need cash flow coming in for new contributions with no bonds to rebalance.

Sounds like an interesting experiment. Good luck…

Thanks man :) Appreciate the thoughts regarding international stuff too – I could def. use some more schooling in that area.

Nice J

I’m also a big fan of vanguard and try to follow the 3 fund portfolio which consist of the total stock market, total international, and total bond index funds. That’s my core portfolio although I do hold some individual stock also, and I am investing a little bit in P2P lending. I might consider adding REIT index funds in the future with vanguard for more diversification. Not sure if you have heard of the boglehead forum board but it is dedicated to jack bogle and follow his philosophy, you can find a lot of information there http://www.bogleheads.org/forum/index.php.

Thanks man. Heard of it but still haven’t spend any time there yet – I have a feeling I’ll be sucked in and smiling the whole ride :)

You can’t beat that 0.05% expense ratio. This is very similar to what “The Smartest 401k Book You’ll Ever Read” recommends: Basically all your investments can go in one of three mutual funds with Vanguard: Index stocks, index bonds, and index foreign stocks. It’s simple, and because you’re simply indexing you know you’ll do better than at least half of the active investors out there.

I do love me some vangaurd. I have a taxable account over there and a roll over IRA over there. The taxable is 85/15 stock fund/bond fund and the IRA is in a 5 ETF lazy portfolio. Those are my Ronco (Set it and forget it… remember that guy?) investing accounts. I also have a ROTH IRA where I get pretty risky and pick some individual stocks, because well, I love doing the analysis of them.

Did you look at VMRAX when making your decision?

Nah, didn’t come across that one – are you invested in it? Looks to have multiple managers handling stuff?

I have three funds, all at Vanguard, and they have all served me well thus far- The Total Stock Market Index Fund, The International Total Stock Market Index Fund, and the LifeCycle Fund . Sometimes lazy is better ;)

I am 100% invested in the same Vanguard index fund as you. I am an aggressive investor who is willing to accept a higher rate of risk but I don’t have the desire to be micromanaging my investments. Good call J. Money.

Nice!!! Love hearing that!

Holy cow! 47 different funds?!? And you were paying fees on all of them. I’m not at Vanguard at the moment because everything I have is at Fidelity – which is doing pretty well on competing with Vanguard for low expense ratios (for their Spartan funds). But we’re about 55% total US, 20% international (ex-US), and 17% bonds – all in low cost index funds. We’re a bit older, and Dad’s not that aggressive, so we want the bonds in our portfolio.

The sad thing is I couldn’t tell you WHAT fees I was paying, and for what funds… In fact I never really cared about fees until I started reading about financial independence by the early retiree crowed. I figured as long as I was making money it’s all good! But apparently you can make even more when watching the fees :)

I’ve heard great things about Fidelity too – my parents use them and always seem pretty happy. Glad their fees are competitive!

I love it! We only own four things, but they’re all indexes. The biggest pain is rebalancing, but I’m such a nerd that I get pleasure out of doing it.

Pretty bold J to be all in on 1 fund. I have been with vanguard for 10+ years now, I have a total stock fund as well, a REit Fund, and a long term bond fund. Pretty boring, but I have been happy with the results so far.

Go bold or go home, right? ;)

You inspired me!

I finally got off my butt (sexy though it is) and organised an index fund.

Mine is with Vanguard Australia — so very similar, only slightly “down under” so to speak – haha.

Thanks!

There we go!! Congrats on taking action! :)

you are probably not diversified enough even if you are holding VTI which is the US. if we revert to the mean, USA might have ran its course. Perhaps one of VT, which is the vanguard total world stock market ETF might make sense

Thanks to you J. Money! after reading this blog( three times!) I opened my first Roth last night, you know, its been years in the making but you actually gave me the extra push I needed. I followed your advice although my pocket can only afford to open an index driven with 3k. Finally this is it!. I will commit to maxing it out and next year open one for my hubby and will find a way to max both. You are very inspirational!

Rock on!! Love to hear that, Izzie – you’re gonna amass the $$$ in no time :) Thanks so much for letting me know this morning – totally made my day.

Do you invest your retirement for both your wife and you in Vanguard? I’m trying to decide if I should do my husband’s in Vanguard and mine in Fidelity. Thoughts

Don’t know much about Fidelity other than I hear great things about them as well, but no – right now only *my* investments are in Vanguard, though of course it’s still “ours” :) I do want to move my wife’s money over to them too though, just have to have “the talk” with her as she likes having everything in one place and hates talking about money… So we’ll see what happens with that – hah!

I like Vanguard and I also like keeping all of my finances under the USAA umbrella. You are probably aware, but you can invest in VTSAX (and most other Vanguard funds) through the USAA ‘Mutual Fund Marketplace’ and still keep things under one roof. I am probably a bit too obsessive about the under one roof concept, but it helps to keep my mind calm…

Yup! I did know that, but the sucky part is they charge something crazy like $40 a transaction to buy/sell? At least that’s what I paid when I first invested in a Vanguard fund the other year… I really REALLY didn’t want to move my stuff out of USAA, but deep down I knew it was the better route long term so decided to finally suck it up. If there were no fees involved at USAA like with Vanguard for investing in them I probably would have stayed!

Excellent article.

Taylor

Jeni, both Vanguard and Fidelity are good companies — I’ve used both for decades. But there’s no question that Vanguard is the low-cost leader, and costs do matter…a lot! When I retired I transferred all of my Fidelity 401k funds into my Vanguard IRA’s (traditional and Roth). Between BH and myself we have 5 Vanguard accounts: joint taxable, my IRA, my Roth, her IRA, her Roth. It’s easier keeping track of things when everything’s in one place.

As retirees, we can’t be so aggressive with our investments. For the record we’ve got 47% stocks (80% domestic VTSAX and 20% int’l VTIAX), 47% bonds (90% intermediate VBILX and 10% Hi-yield Corporate VWEAX), plus 6% in cash equivalents — enough to carry us for two years, so we won’t feel forced to sell at the bottom. Is that a perfect allocation? Probably not, but it’s one we can live with (and that we don’t lose sleep over).

“It’s one we can live with (and that we don’t lose sleep over).” – That’s exactly the mindset we have too, and many others… The unemotional people won’t agree, but most everyone is affected by them ;)

Another Vanguard fan here. Smart move.

One thought on the 100% VTSAX move: studies have shown that a small (10%-20%) allocation to bonds doesn’t have a huge impact on long term portfolio returns (vs. being 100% VTSAX). I like them being there (even if you’re an aggressive investor) to slightly lower the risk, but also (more importantly) to be a source of funds within the account to rebalance into VTSAX when the periodic correction in the market arrives. All it would require of you is to rebalance periodically (annually, semi-annually…..whatever works for you). It would only take a few minutes to complete with only 2 funds.

You’re probably right, but at this stage of the game just feels too conservative for me… like having cash in a money market or savings account :) I’m okay with the risk of losing more as long as it has the chance to earn more as well. I’m sure I’ll change my tune as the years go by though…

I think your 1-fund portfolio is better than what it replaced, by why not add an international fund? Home-country bias could be dangerous. Ask a Japanese investor circa 1990. Or a Russian investor in 1913. International diversification is almost a free lunch. The fees for Vanguard’s Total International Index Fund (VTIAX) are just a little more than your fund. Your total returns might not change much, but your portfolio volatility should reduce slightly and you’ll be partially protected from worse case scenarios should the US economy falter in a way we don’t expect (sorry to write this on Independence Day — how unpatriotic of me). FYI, I’m at 65/35 US/International, up from 70/30, and I’ll probably move gradually more toward equal-weighted.

Hah! Even better you’re writing on Independence day :) I’d def go the international route sooner than I would the bonds route as others have mentioned. Just want to go with the flow with the one main fund for a while and see how that feels… I’m def. keeping my options open down the line for sure.

Too much home bias. No international stocks, no emerging markets. I really don’t understand why given the opportunity to diversify internationally you would choose to put everything in the US. Even the Lifestrategy Growth has too much of a US bias for my liking.

You can read some of the comments I’ve responded to above for more info (or the article again, for that matter ;)) but really it comes down to it just “feeling right” right now. And a $hit ton better than the previous set up too… I never say forever with any choices though, so I’m sure it’ll be tweaked as time goes on.

Vanguard is great!

Did you consider a bit more diversification across asset classes, as recommended by (e.g.) Personal Capital, Wealthfront, or Betterment? We took a look at all three of those (they don’t agree on the details, more so on the concept) and decided to mimic the Wealthfront portfolio of Vanguard ETF’s. Mainly because we already had IRA and employer retirement accounts at Vanguard, and Wealthfront uses Vanguard’s funds for almost all asset classes.

So today’s portfolio is:

Fund Alloc ER

LQD 10% 0.15% (the only non-Vanguard fund but a similarly low ER)

VEA 18% 0.09%

VIG 15% 0.10%

VNQ 14% 0.10%

VTI 22% 0.05%

VWO 15% 0.15%

VWOB 7% 0.35%

TOTAL 100% 0.12%

According to Personal Capital (fantastic FREE analysis tool) this gives us the following:

Stocks 70%

Bonds 15%

Alternatives 15% (mostly real estate)

Cutting it another way

International Stocks/Bonds 42%

US Stocks/Bonds 43%

US Real Estate 15%

You could have Wealthfront do the investing and rebalancing for you but why pay them 25bp for that — it could really cut into your long run earnings, and besides, isn’t one of the big objectives to get fees to rock bottom?

We will have to periodically do some selling/buying to keep our target allocations where we want them. Maybe twice a year? I need to do more research on this point but it seems that more frequent rebalancing is better (assuming no transaction fees). In any case this portfolio is spread among asset classes and domestic/foreign with low fees an not too much care and feeding. We are definitely buy and hold investors.

I should add that we are in our 50’s so the allocation is influenced by our proximity to retirement.

That very well could be smarter, but it already gives me a headache looking at it :) I think there are a lot of different ways to reach the finish line, so as long as this looks good to you it’s all that matters my friend. You’re much more in tune with this stuff than I!

Why do we think that there is money to be made by tracking the index in the first place? Why do we think that the index is going to go up?

‘Cuz it’s always gone up over time? And most people suck at stock picking? (At least I do :)). I wouldn’t advise investing in the market if you don’t believe it’ll eventually pay off.

J. Money’s answer is solid.

Here is another way of saying the same thing, from my own experience:

Many years ago I realized that every quarter when I got my 401(k) statement — this being in the days of paper statements and before online visibility — anyway, every time I got my statement I looked at the return on the various mutual funds in my account, and then I looked at the S&P 500 index to see whether they had done better or worse. Then one day I noticed the S&P 500 Index Fund and realized if I just put all my money in that it would never do worse and I could stop worrying about it. That was the moment I committed to being a long term buy-and-hold investor from then (age mid 20’s) until retirement.

Now it is 30+ years later and all those 401(k) contributions with employer match have compounded to about $500,000. A nice nest egg to retire on. Of course there was that little bump about five years ago when it was down under $300,000 but thank goodness the market came back. There is no guarantee that the index (market) will go up but over the long haul that’s the way to bet.

Way to go man! It’ll keep growing as time goes on too!

J. Money,

One question: why VTSAX over VTI (Vanguard Total Stock Market ETF)? I see the expense ratios (0.05%) are the same for both, but realize some recommend ETFs if we’re talking a long-term investment game (YNAB’s 9-day email Investment Course comes to mind for the ETF discussion). Maybe it’s splitting hairs?

The real answer is because all my blog friends talk, and rave, about VTSAX and I didn’t see VTI come up much, or at all :) So once I started looking into it and agreed with the overall principle (and chatted with some people) I just pulled the trigger knowing it’s 1,000 x better than what I was doing. VTI very well could be even sexier, I just don’t know much about it other than what you just said and doing a quick google search :)

Thanks for the review! Are you familiar with Betterment at all? Not knowledgeable with investing/Roth IRA’s in the least but really want to get started. Vanguard seems a bit more complicated.

I’ve heard their name pop up a number of times – and know some people that love ’em – but haven’t researched personally myself. Here’s a review my friend John did on them if it helps:

http://www.frugalrules.com/betterment-review-investing-option/

Interestingly enough, I see they have vanguard funds to choose from ;)

I am presently invested in TIAA-CREF with my employer (401k) and in Ameriprise with my old 401k, Roth, and SEP IRA. I can’t do anything about my current 401k, but decided to move all the Ameriprise stuff over to Vanguard because of fees. Right now I am slated to go into one of their target retirement funds. Do you think that is the best or should I put it all in VTSAX? Also, do you think I should move everything over to TIAA-CREF so everything is in one place?

Hey Andrew :)

Honestly I’m not the best person to ask on what’s best cuz I can barely figure it out on my own for my specific situation, haha… I will say that in general I haven’t heard anyone complaining about Vanguard though and they DO have low fees. So I’d def. check them out. Also check out the Bogelheads forum (http://www.bogleheads.org/) and drop your question (you can just copy and paste!) into Jim’s Q&A page in the comments and I’m sure he’ll answer it for you real well:

http://jlcollinsnh.com/ask-jlcollinsnh/

He’s a pro at this stuff while I’m just a tadpole :)

My husband and I have been with Vanguard since we started investing which was at the beginning of this year. But we have gone from VTSMX to VTSAX in a short time. We’ve added more money when the stocks were down and been pretty happy with the results. No panicking for us I tell you! Feeling confident with Vanguard and moving towards FI.

Good! Best time to buy is when everyone’s panicking and pulling out – well done :)

I recently made a similar decision! I have a 401k through work, with my employer contributing 9.04% along with my 5% contribution. (Nice employee benefit, right!?) In addition to that, I recently started my own Roth IRA. After some trial and error, I decided to go with only VTI in my IRA. I thought about switching to VTSMX once my account reached $3,000, but I decided to stick w/VTI until I get to $10,000. The ETF fees for VTI are only .05%. Once I reach $10k in the account, I’ll switch to Admiral Shares.

FYI, VTI is the ETF version of VTSMX/VTSAX.

There you go! Love it.

Also – yes. A 9.04% matching of FREE money is incredible, way to take advantage of it!! (And why the .04%? haha..)

Just found your blog, and as I mentioned on Twitter, I’m so glad I did! Found it a month too late though, as I just rolled-over a Vanguard 403B from my old job into a new traditional IRA brokerage account with USAA with the goal of simplifying things under one umbrella. I like the idea of index funds better than USAA’s Cornerstone Aggressive fund and the bonds it holds, which is what their guy was suggesting. I’m 35, don’t have much to invest ($13,500 in the new IRA, just parked there until I figure out what to do with it), but a long time before I will need to rely on it.

My question is, according to USAA’s website, a brokerage account with them provides the “USAA Fund Marketplace” which “gives you the access to thousands of mutual funds from USAA, Vanguard, Janus, T. Rowe Price and dozens of other firms.” Would there be a huge difference between buying the VSTAX through USAA’s Marketplace and directly with Vanguard? I could call USAA and ask, but I have a feeling they might be biased!

Haha… I totally understand the “under one roof” thing – I had 19+ acct with USAA at one point! There’s definitely something to be said for that :)

As for investing in Vanguard funds w/ USAA – yup! Def. do able, but if I recall you have to pay like $40 or something crazy big each time you made a transaction (I could be wrong, but I believe that’s what i paid a few years ago when I wanted a Vanguard fun and I just made sure to move a big chunk at once and then leave it alone (it was for my Roth IRA I believe)).

I’d still call them up and confirm though. Perhaps all the Vanguard converts are leaving USAA now due to this post and they’re waving fees for everyone – hah!

I’m pretty thrilled, I just moved all my money from USAA *back* to Vanguard! After spending 6 months trying to decide what to do and having the 13K sit in a money market acct, I decided that $45 fee with USAA was silly, and duh, I should just go back to Vanguard and take advantage of no fees and crazy low expense ratios. It was so easy to transfer it back completely online with Vanguard’s transfer tool and it only took a week! I think tomorrow I’ll pull the trigger and buy the VTSAX, since I know you can’t time the market and there’s no point waiting for a down market day when it drops a dime or so in price (although I’m tempted).

So glad I found your blog! I love the ‘one and done’ ‘set it and forget it’ approach. I think I might add the Total International Index at some point, and then a bond fund down the road. (I’m 36, I’m fine with just stocks for now).

Rock on! Glad it was so easy and smooth for you to move over too – that’s awesome. It’s already been a year since I made this switch and I can’t tell you how nice it is to not have to think about it anymore. I never have to worry or over think future investments – I always know now where it’s all going :)

I love Vanguard and opened my first Roth IRA account here under VFORX (Target Retirement Fund 2040). I also transferred my previous employers 401k to Vanguard IRA under VTTHX (Target Retirement Fund 2035). I also read quite a bit of jlcollinsnh and have approx. $30K in VTSAX. I currently have $100K in cash and wondering if it would be wise to dump all of it VTSAX? Or would I be the only fool to invest this much money in VTSAX? Would one of the Target Retirement funds be a better alternative?

Well, if you’re a fool I’d be an even bigger one considering I have $400,000+ in VTSAX only :)

I think people will say it’s better to be more diversified with 2-3 indexes with bonds and world exposure, but I’m no expert (obviously). I’m personally happy with my all-in-one fund right now, but who knows – maybe I’ll add another as time goes on if it makes sense to.

My husband is 48 with no retirement (I’m 36). Would you suggest Vanguard Index Funds or Vanguard Target Retirement Fund 2035 for him? Thank you in advance!

Hey Jeni – SO GOOD you guys are looking into investing now!!! Super super important to do if you want to be able to retire one day.

I’m not qualified enough to advise one way or the other, I just know index funds make the most sense for me so I run with it. I’d Google around, or better yet – just Call up Vanguard and ask them what they think! They have licensed professionals there to answer exactly those types of questions :) And they’ll need to ask you/your husband questions in order to best advise too.

Here’s their #: 1-877-662-7447

And honestly, investing in *anything* right now is better than $0.00 – so don’t get too bogged down trying to find the perfect answer and not take action :)

Thanks so much for the quick reply! I will definitely call them up! Thank you :) I had no idea you can just call them up and seek advice. Again, thank you!

I have a question about all-in-one funds as my husband and I are transitioning into retirement. Our financial advisor is suggesting we consolidate our IRA’s and regular investment account into one of these. I do like the overall simplicity, as we don’t know much about the stock market and they seem safe with a decent return. If we go this route, we’d like to do as you did and find an index all-in-one, although weighted more heavily in bonds for more protection at this age. Do any exist? Where would I find this info? I’ve been looking online and my head is spinning!

Deepest thanks,

Jacqueline

Update: my advisor has stated that he’s not recommending all-in-one funds for our retirement account, but “managed solutions portfolios” like Vanguard’s “Strategic Solutions.” They are index funds, but look like they focus on ETF’s? Do you have a sense about these?

Hey Jacqueline :)

Great questions indeed… I’d hit up JL Collins when you get a chance and read through his stock series – you’ll learn a lot there: http://jlcollinsnh.com/stock-series/

But yes, Vanguard and similar companies offer all types of variations of indexes and ETFS and I personally believe you’d be fine however you proceed. Whether they’re weighted one way or another (and you can always just call them up and ask! they’d be able to tell you 1-2-3 and get you squared away). Though FYI I’m no expert in investing :)

I think consolidating all your brokerage accounts everywhere will make things MUCH easier and simpler to manage going forward as well. I have almost all of my stuff in one place (one for investments and one for banking) and I can’t tell you how much easier my life is.

The important part here is to *take action* and pick the route that you find makes the most sense and then adjust as time goes on.. Sometimes there’s just too many options to choose and you don’t want to throw in the towel :)

Good luck!

I too like Vanguard and use them almost strictly for my investments and Roth IRA. I have a money market account for my emergency fund, Roth IRA for me and the wife and the Vanguard LifeStrategy Growth Fund. Love the low costs and the simple approach to investing. I set up everything on auto pilot- easy!

Glad to see I’m not the only one who believes index investing is cool.

Great article J Money!

Hell yeah dude! It took me a handful of years to finally catch on, but I’m glad I’m now here and officially a Vanguard lover :) So easy once it’s all set up!

Hi, there! Thank you for such a great blog post about VTSAX. I opened my Vanguard account this afternoon and will soon buying this stock. But I had a question I was hoping you could clarify something first. There’s an investment income calculator (https://personal.vanguard.com/us/funds/tools/incomecalculator) on the Vanguard site, but the estimated annual income it shows for the VTSAX doesn’t align with the chart showing the hypothetical growth of $10,000 for this fund (https://personal.vanguard.com/us/funds/snapshot?FundId=0585&FundIntExt=INT).

Am I doing the math incorrectly, or is the income calculator not the same thing as the growth chart? In the calculator, I enter 1.85% for the yield and an investment of $10,000, and it tells me my yearly income will be ~185. After 10 years, that’s $1,850, but the chart is showing a hypothetical growth of ~$12,827. What does that mean? Hoping you can make this clear for me. Thanks!

Oh man, I have nooooo idea sorry. I suck with calculation stuff :( Maybe one of them is including dividends over the 10 years and one is not? I know I get a lot of sexy dividends myself w/ VTSAX :)

I’m a UK investor and had a much more complicated portfolio than yours a few months ago before I discovered bogleheads and taylor larimore’s wonderful advice (and also Jcollins stock series).

I sold everything I owned and am now pretty much 100% in VWRL (Vanguard all world). It is so much easier for me as I don’t want to have to consider which investment to top up. Just stick it all in whenever I get lumps of cash now.

In the UK in our taxable accounts we get approx 11k per year capital gains allowance tax free so I may also use vanguard lifestrategy to switch to and from for tax gain harvesting

Rock on! A simpler life is so much better, isn’t it?? I love not thinking about it anymore :)

PS I found this article as I googled 1 fund portfolio to check I wasn’t the only one!

Rock on! You’re def. not alone!

Gday J.Money from Sydney Australia I have sold everything and now hold a simple two fund Vanguard Portfolio VAS.AX (Australian Shares) and VGS.AX (All World Shares ex Australia) 50% invested each way How simple is that ? Why complicate things hey :)

PS Great blog

You know I’m down with that! :)

Is there a reason you didn’t consider VTWSX ? It’s a bit more expensive but by being 100% VTSAX, you are missing out on some quality foreign companies like Nestle, Shell, Toyota, Samsung, etc.

No reason really, just didn’t come across it while initially poking around :)

J. Money,

You still 100% in VTSAX? I have $50,000 at Vanguard in TR2050 and thinking of going 100% VTSAX.

Yep!

No plans on changing anytime soon, at least :)

Don’t know anything about TR2050 but I do like that it’s with Vanguard. Might be worth calling them up and asking an adviser what they think about moving it over? Might give you some good insight? (If you do it – come back here and let us know what you find out paleeeease!)

Hey J,

I’m preparing to open a Vanguard Roth to squeak into 2015, (depending on my tax return I’m looking at being able to fund $3000-$5500). For now (for 2015) I’m thinking of VTSMX. Two questions, can I simply start or open the Vanguard account, (maybe throw $0-$500 into it) set up as a Roth but not yet invested in any funds till I have a minimum $3K? I imagine the money just sits there like a savings account until I’m ready, yes? Also, if $3K is the minimum, is that pushing it as these index funds go up and DOWN? What happens if my VTSMX drops my balance under $3K? Finally, once this account hits $10K does it automatically switch to VTSAX or do I or can I switch to that myself?

Great questions!

I have guesses to the answers to them, but probably best you just call them up directly and ask so you know they’re 100% accurate :) And then if you get favorable responses, they can literally help you open up an account right on the phone! That’s what I did when moving everything over – I just asked them to do it all for me and was nice and easy :)

I can tell you that yes – they do automatically bump up your status once you hit the $10k or whatever minimum it is for admiral shares. I think they check quarterly and then switch it for you, but I’d just call them up once you notice it and ask for it to be done just so it’s accomplished faster for you.

Great question on whether the market dips and what happens to minimums – never thought about that! I feel like what counts is the amount *you put in* (so, $3k in this case) and then whatever the market does it does. But again, best to just ask them when you’re on the phone.

Here’s their #: 1 (877) 662-7447

Let us know what you find out if you remember!

J. Money,

Thanks for posting this. My entire portfolio of $75,000 is also comprised of only VTSAX. I was glad to see that other people have the same idea. I may eventually add a Bond and International fund, but for now I’m sticking with the one fund.

Cool! Makes me feel better too :) (And I may add in bonds/international down the road at some point too… but prob not for a while)

I was just thinking the same strategy for my 401k. Move everything to an S&P 500 Index Fund.

All of this makes me queezy, not for the investment value risk but for other reasons. I was reading earlier today that even if the mutual fund company, such as Vanguard, went bankrupt, my investment would safe. I’m still not sure why. The other part that concerns me is “fraud”, not that this has ever happens on Wall Street. Call me crazy, but what if it did? Could a fund manager somehow with help from the other employees manipulate the fund, fake the numbers, move out of the country under assumed names with a huge hunk of my money?

I mean, anything’s possible for sure, but in that case you might as well never invest in anything :) Def. a balance between feeling comfortable and taking calculated risks. There are other ways to invest in stuff outside of the stock market too.

I’m basically doing the same strategy but it’s the VIGAX fund. Any opinions on that fund? I have like 2500 shares and I’m 33 and really have no idea what I’m doing…

Well you’re doing something right if you’re sitting on all those shares!

And being on this blog ;)

Although unfortunately I’m not well versed myself in this area (I copy all my smart friends and heavily lean on their opinions/research) but I think if you like keeping it simple and being invested in the market as a whole, you’re on the right track with indexes. Whether VIGAX or VTSAX or any others.

Check out JLCollinsnh.com or any of the other early retirement bloggers to see what they say – they live and breathe Vanguard.

Appreciate the vote of confidence glad I stumbled across a like minded individual. See you at the future millionaires softball game…

I’ll save you a seat :)

I’m consolidating all my IRA’s to Vanguard as well. My standard IRA will be 100% vwinx. The Roth will be divided up in half for vwinx and vwelx with annual contributions. Less volatility, plus higher income payout(like a annuity). My taxable account are in indexes for tax efficiency.

Hi! Would like to pick your brain about Vanguard when you have a moment. I am intrigued! My 401K has the following Vanguard options: Vanguard 500 Index FD Admiral (VFIAX), Vanguard Mid-Cap Index Fund Admiral (VIMAX), Vanguard Small Cap Index (NAESX), and Vanguard Tot Stock Mkt Index (VTSMX). I put 100% in the Vanguard Mid-Cap Index Fund Admiral but I am wondering if I should I split up between these after reading your article. I do have a choice of Vanguard Target Retirement too. Any insight you could provide to a novice would be wonderful. Embarrassed to ask but decided to go for it anyway!

Thank you!

Don’t be embarrassed to ask – this whole post/investing idea came out of ME asking people! :) Though unfortunately I’m embarrassed now by not having an answer for you, haha… I’m not sure what your goals are or how old you are/etc/etc, but VTSMX is pretty much the same thing as VTSAX which I’m fully invested in, just a different “class” and different expense ratio. So naturally that’s where my heart is, but I honestly don’t know enough about the other funds – or what you’re trying to accomplish – to really be able to advise. Check out Jim Collins’ series on stocks though – you’ll learn a ton! And most of it is about Vanguard funds:

http://jlcollinsnh.com/stock-series/

I am about to take the plunge. Just opened a vanguard Account TODAY markets are freakinout over the brexit thing so good time to invest? I.e. Jump in while others are jumping out! That said how much should I keep in cash reserves so I can sleep? 6 months of expenses or more? I know we should have an emergency fund of this in cash but didn’t know if all my other pennies should be working or some as jhcollns says laying In the sun being lazy doing nothing! am trying to get better at letting my money work for me instead of just sitting there in checking account. Btw I just discovered jhcollns by the way of your blog it’s great!

Oh, great!!! Yeah he just came out with a book too – check it out:

The Simple Path to Wealth: Your road map to financial independence and a rich, free life

As for emergency savings, it really depends on what you’re comfortable with, but you def. can’t go wrong with 6 months :) The peace of that to me is worth the few extra dollars you may be missing out on… (I know others that do 3 months and then even 12 months btw! As long as you think it through and feel good about it you’ll be fine…)

I just have to tell you that with all the research and reading I’ve been doing this past year to educate myself about my money, possibly the most reassuring thing I’ve read is in an earlier comment of yours on this thread: ‘I suck with calculation stuff.’ Me too: so if I share that issue with a successful investor and finance blogger like you, I’ll worry about it a little less. Big thanks to you for your honesty and transparency.

Awww, well I’m glad! And it’s totally true – I suck with a lot of this investing/numbers stuff! But when I see something that makes sense and excites me, I run with it :) And so far this Vanguard indexing route has been amazing even after two years… Def. plan on keeping with it for the long haul.

Thanks for stopping in and saying hi! Hope you enjoy the blog :)

Took inspiration from your post and my latest readings would also agree…get the fees and expenses down!

One question: USAA individual accounts in my Roth IRA and mutual funds seem hard to find. I have a brokerage account where account # is clearly listed but I can’t find east account numbers anywhere. Any idea where to find that? Thanks!

Weird, yeah! Just logged into my wife’s USAA account (she still has a Roth there) and you’re right – def. tough to find!

I had to go into documents and bring up one of the statements – try that, it’s in there :)

Glad you’re enjoying the blog!

Hi your write up is great ,you have a new fan i like the way your brain works..

and i love the sound of the

VASGX [

56.1% — (VTSMX) Vanguard Total Stock Market Index Fund Investor Shares 24.0% — (VGTSX) Vanguard Total International Stock Index Fund Investor Shares 16.0% — (VTBIX) Vanguard Total Bond Market II Index Fund Investor Shares 3.9% — (VTIBX) Vanguard Total International Bond Index Fund]

It is very much in tune with my final investment portfolio and its 7 components after much research..

from my research i would fit into the Non residential alien status.

I am a non us citizen with a business ad or tourist business visa,i have a multiple entry 6 month longest stay visit on each entry however i am building a hedge fund company in Africa that operates through an investment portfolio 2 platforms 1.Global All weather -(4 components)

& 2. African Special (3 components) total 7 components.

Now based on my business model ,My no 1.Global All weather -(4 components) platform will be optimal if i base it in the US to that effect i have a couple of questions.

1.How can i purchase VASGX as an NRA that will stay less than 183 days on each visit to the USA?

2.From your article and i quote “Vanguard has an “Investor shares” version of the fund too, fyi, for those who can’t invest $10,000 or more into the fund (VTSMX)…”

Does vanguard have Investor shares for the VASGX as well? {I have to start small for a proof of concept as mystart up seed capital is not that much}