Morning hustlers! Got a piece of juicy mail come my way over the weekend, and thought I’d hit you with it to further encourage your voyeurism ;)

This letter came courtesy of the Social Security Administration, and was a stark contrast from the other notice I received at the same time pretty much telling me I’m getting kicked out of my health insurance plan by the end of the year, ugh… Looks like it’s finally time to check into Obamacare and see what the fuss is about (double ugh?).

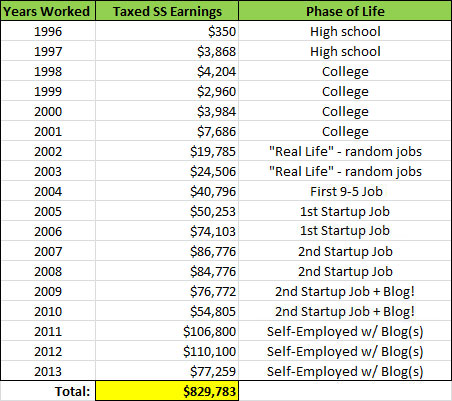

Anyways, the more positive piece of awesomeness I’m referring to is of course the Social Security Statement that sums up all your reported (taxable) earnings over the course of your lifetime. I’m not too sure why I’m still receiving it via printed mail when I thought you could only get it online nowadays (www.ssa.gov/myaccount) but in either case my inner nerd was doing back flips. It’s not every day you’re reminded of all your income here on Earth! Or, perhaps more accurately, all of your income that you’ve since SPENT!

(BTW, I highlight “taxable” here as it’s not really how much you’ve earned your entire life (which would be *gross* income), but how much you’ve paid taxes on. Which could vary drastically depending on your sources of income/set up/etc. Still, it’s pretty damn interesting to know.)

The last time I shared my total earnings was back in October of 2010, and by that point I had earned a tidy sum of $489,400.

Here’s What My Total Earnings Look Like Now:

I added in a column there to the right to put things in better perspective… A million dollars sounds good, but does it change when you know it covers almost 20 years? Or that incomes may not be totally stable? Or that you’ve been living in an expensive part of the country where salaries are higher?

You’ll remember from Friday’s post that the important part is what’s saved vs. what’s earned. So that’s the real telling point to fully appreciate the achievement or not (though of course you could still give yourself a pat on the back for managing to get someone to pay you so much over the years regardless ;)). It may be sexy to earn a hot million or two, or even 10, but if your bank account’s showing $15 in it something else is certainly going on… like, you’re having a helluva time pretending to be a rock star!

Introducing the “Lifetime Wealth Ratio”

Since the Social Security Administration would have no idea how much you’re saving in comparison to this income, we’re left to come up with our own means of figuring how good we’re doing or not. So today I introduce to you the newly coined term – and future buzzword – the “Lifetime Wealth Ratio™”

Which is calculated like this:

Net Worth ÷ Total Income Earned

We’ll use my pal Jacob from iHeartBudgets.net as our first example. You may recall a post he shared on this site back in January where he divulged his total lifetime earnings over the years too. He went all the way back into childhood which isn’t included in these S.S. Statements (you know, like gift money, lawn mowing hustles, inheritances, etc), but to this best calculations he figured out he had received a staggering $601,600 by the time he hit 27. Nothing to sneeze at by any means. His total net worth at that time? $55,000.

This would give Jacob a Lifetime Wealth Ratio™ of approximately 9%. Is that good? Bad? I dunno. I’m just the guy who makes up terms on the fly ;) (And then fake trademarks them) But, I can tell you it’s a helluva lot better than 0%! And if you’re really forcing me to come up with some sort of ranking system here, and, well, I know you are, then twist my arm no longer.

I would suggest rankings as so:

- 0%-10% – Meh

- 10%-25% – Now we’re cooking!

- 25-50% – You’re on fire, baby! Give me your number!

- 50-100% – Marry me.

- 100%-1,000% – How do I get into your will?

(You probably couldn’t tell, but it took me all but 15 seconds to make that up)

What you’re shooting for, of course, is to have as high a ratio as possible. This would show how good you are at saving/investing/blowing up your money/etc. And if you’re asking yourself how it’s possible to get a return of more than 100% with this calculation, well, Google “compounding.”

J. Money’s L.W.R.

(Look at that! It already has its own acronym!)

To put this ratio to an even better test, let’s see where I personally stand myself…

At the same age of 27 like my boy Jacob, I made a total of $232,495 according to this same S.S. department when added all up. Almost 2/3rds of what Jacob had earned by that point – so far not good. Since this was right around the time I started tracking my net worth too, I can also tell you that it was exactly $58,769.65 at that point. Almost exactly the same as Jacob – we’re twinsies!

Running the ratio, however, paints a different story. If you divide 58,769.65 by 232,495 you’re left with an LWR of 25%. More than double Jacob’s 10%, and barely into the zone where I ask for my own number! Ow ow!

Now of course I jest in fun as Jacob’s a good friend of mine and has already acknowledged he was horrible with money years ago (if you’re a follower of his blog you’ll know that’s definitely no longer the case) but this should help put things in better perspective. And surely the ranking system could use a little fine tuning based on your own judgement.

(Keep in mind everyone tallies their own net worths differently too, and that there’s much more to it than just “saving money.” All the usual suspects to growing wealth will play a part here – investing returns, real estate, business ownerships, etc)

Let’s run my numbers again, only this time with current totals. At the ripe age of 34 (another variable to consider) I’ve made $829,783 of taxable money as shown above, and have a net worth of $456,140.18 as of September (new net worth comes out this week).

According to this trending new ratio everyone’s talking about, I’m now hovering at around 55% – double the growth! And now apparently time to marry myself, haha… As you can see, I’ve been getting smarter with my money :) And *that* is something I can be proud about.

Here Are Other Interesting Facts S.S. Shared With Me:

- If I continued working until full retirement age (67), my payment would be $2,314/mo

- If I worked until 70 it would shoot up to $2,870/mo

- And if I cut out early at 62 it would drop to $1,625/mo

(No mention of what you get if you retire early ;))

They also stated I’ve received “enough credits” to quality for disability benefits. I never really consider what would happen if I got disabled, because, well, it’s horrible to think about (and thus disability insurance has been on my to-do list for years now, bad blogger!), but God forbid something does happen, it looks like I could start receiving paychecks of $2,278/mo right this second. Which is almost exactly what I’d get if I started pulling money at 67!

That’s pretty crazy…. And probably why there’s so much fraud with this stuff, eh? If people could collect pretty much the same amount of money but 30-40 years earlier for gaming the system?

It also looks like I’ve earned enough credits for my family to receive “survivor benefits” too should I pass away at any point. And that I have thought about before, as I poured my heart out to everyone in my “If I die I’d be a happy man” post of mushiness the other week :) I also made sure years ago to pick up life insurance policies for both the wife and I as soon as we bought our first house so we’d always have enough to pay it off. Something for you guys to consider too when large events happen in your life (homes, kids, marriages, etc).

Here’s what my family would get if/when that fateful day comes:

- My child (#1 since #2 wasn’t born yet as of 2013): $1,836/mo

- My wife who’d be caring for this same kid: $1,836/mo

- My wife if I die when she’s 67: $2,448/mo

All of which can’t surpass $4,286/mo total a month for my family. That’s a $52,000/year salary! Wow… For pretty much doing nothing besides just working like you’re supposed to do anyways…

While that’s all fine and dandy, of course I’m not counting on any of it. My wallet would greatly welcome it in, but we all know the system’s flawed so we continue hustling away and stashing that money as if it were us against the world. I would much prefer a nice surprise later in life than a nasty one if you know what I’m sayin’. Can’t get caught with your pants down!

All interesting stuff to learn about though… never know what types of freak blogging incidents could be around the corner ;)

Your Homework This Week…

Your homework this week is to do yourself a solid and find out what your own Lifetime Wealth Ratio™ is. And for that you’ll need your two numbers:

- Total lifetime earnings (you can find it here if you don’t have a recent statement nearby)

- Your net worth (if you’ve never run it before, here’s a quick and dirty spreadsheet I use w/ my money coaching clients… extra credit for filling out the budget part while you’re at it too)

Run the calculations (worth divided by earnings) and then see how it makes you feel. You can share it with us below if you’d like, but really it’s just a number for you personally to stew on. And the silly rankings I made up don’t matter that much either. What does is that you know where all your money’s going and you’re consciously applying it to reach your goals. If the ratio makes you happy – then great! Keep going! And if it pisses you off, well, time to do something about it.

At the end of the day, all that matters is that you’re on top of it and continuously working towards better financial lives. Now go grab your L.W.R.™!

UPDATE: Many astute readers have mentioned that it’s more accurate to calculate your ratio with “taxed medicare earnings” vs “taxed SS earnings” due to capping that goes on with SS earnings. My numbers are the same in both sections so it doesn’t make a difference, but if you’re a baller and make a lot more where you’d be capped, consider running w/ the medicare earnings number instead.

UPDATE #2: Our wealth ratio just got mentioned in a NY Times article! Look what my new favorite journalist said about it ;)

“This number represents one of the best ways I’ve seen to close the gap between our past and future selves.”

UPDATE #3: This should help with motivation: Proof you can live off 50% of your income!

—–

PS: Anytime I share my numbers with y’all please know it’s for educational purposes only. I don’t divulge any of this to brag or compare myself to others, yada yada yada , it’s all in the name of transparency and to show you real-life numbers from a real-life person. Even if my name really isn’t J. Money (how’s that for ironic? Being secretive to be more transparent!). The one thing that drew me to blogs years ago was open discussions with money, so this is why I share my entire financial life with y’all. It’s my favorite way to learn, and hopefully it helps you guys in the same way.

[Photo cred: FDR Presidential Library & Museum]

Get blog posts automatically emailed to you!

This is one of the main concepts in Your Money Or Your Life. Last time we calculated it was towards the end of last year and it was a little below 70% (it should be higher now since this year our net worth has grown by more than we earned). I actually graphed it over time and it was kindof crazy to see that even as recently as 2010, the ratio was more like 15%. What a difference we were able to make in just a short number of years!

Man you guys are going to make me calculate my own after reading all these comments… I’ll be back in a few months once I can dig up all my returns…

Hah – good! Peer pressure ;)

@Mrs. pop – Congrats!! That’s huge!!

Well apparently we are getting married, where should we register? I’d like a new Belgian waffle maker. I guess I’ll brag about my LWR, but mine is skewed because I hardly earned anything out of college my first four years. Then when I started to earn some real money is when I started to invest hard core (maxing out everything) and the market was heading down and so it was the perfect storm of making money and buying low.

Ouch- looking at my history of earnings is grim. But it makes me feel awesome about having a net worth of 35k! If I’ve been able to save and invest that much on my puny earnings, I’m gonna be rockstar as I start pulling in the BIG bucks ;)

Exactly :) Once you learn how to rock money it sticks with you forever!

What a great idea! I actually was just on the SSA site last week checking to see my expected benefits in an early retirement scenario. It’s more than I would have expected!

So I ran my LWR (TM) (hah!) and came up with the following:

42.55%

Couple of caveats:

I don’t have Mrs. FW’s lifetime earnings handy so I just divided our net worth in half for the purposes of deciding what % of our net worth was “mine”.

I included equity in our primary home in our net worth, but not appreciation since the time of sale.

Kinda cool to think I’ve saved almost half what I’ve earned my entire life. Woot for being on Frugal Autopilot (TM) (see what I did there?) ;-)

I did, I did ;) Keep hustling!

Ugh, I’m not sure I want to know our LWR given our debt situation. But, very cool! Gives us more motivation to kick the debt to the curb ASAP. :-)

I feel the same as Stefanie. I definitely thought WTF when I pulled it up… and I want to look at how some of these numbers come up a little closer. There are 3 years there where it shows me making less than $5,000 and I was full time employed… which really freaks me out that I somehow totally botched my taxes.

On the flip side, with a lifetime income of less than $60,000, I’m surprised I would still pull in over $600 a month if I were disabled. There are plenty of places in the country where I could actually get by on that.

That is weird, not sure why it would show that for you?

The earnings numbers on the SSA site don’t come from your tax returns, they come from what your employer reported to the IRS and paid taxes on. In my early years I worked for a shady restaurant owner who scammed the government and didn’t pay taxes on the wages he paid me. My W2 forms from the restaurant were correct and I was able to send copies to the SSA to get them to correct my earnings for those two years when I apparently earned zero dollars though I was employed full time. There is a link at the top of the Earnings Summary page that tells you how to correct errors.

Woahhh good to know, thx for taking the time to share!

Wow! Nice work on increasing your LWR so much over the last few years! That’s got to feel good! I’m off to dig up my own lifetime earnings so I can check mine out! I’m also hoping to see a big increase in recent years :-)

Cool info on the LWR! I’m looking a bit on the low side because of my debts but will try this out soon. Thanks for sharing!

I’m also dragging my feet about getting disability insurance! Usually I only remember to do it while riding my bike through a crazy intersection. Thanks for the more peaceful reminder!

Great concept J. Another helpful tool that goes right nest to the “rule of 300” in my financial tool box.

I calculated two. The first from the SS Earnings life time gross and the second from life time savings Net (after taxes, social security, insurance, 401k, etc). 33% & 55% respectively. I completely agree that compounding helps drive the ratio. More importantly, the compounding interest can be free from taxes if you are stuffing your IRAs, Roths and 401k to the limits of your capability. The lower number gets me a bit prickly because of all of the taxes that sucked out.

The Net LWR is a figure that puts control back into my hands and more meaningful to me.

Good! Glad you liked it :) Every now and then I have a nugget worth sharing, and then I’m flat out of ideas for a while, haha… so I’ll be soaking this one up!

I like the idea! I am at 40%…..I included only my earnings and my savings. I wonder what it would be if I included the hubby’s income and savings?

Ask him to run it and see! Tell him you’ll “reward him” later for doing so ;)

Haha! I would, but I’m not sure he realizes how obsessed I am with our money and early retirement! Maybe I will bring it up when we have a bit more time to discuss, though I am sure he would love the “reward”!

Thanks much for the mention sir, though I wish it was for different circumstances. :) Nice work on killing it on the upswing in your percentage over the past few years. My wife actually got her letter a few months ago and wondered the same thing about getting in online – but you’ve given me some homework to get done this week so I’ll be checking it out the site so I can run the numbers.

I like the concept of the LWR and based on your calculations, I am around 40%. As a side note, though, I personally hate to get the social security statement in the mail (which they will soon not come at all because of governmental cutbacks and you will have to go online). I hate to see it because I don’t believe the government when they say I will get the number they project. It’s like a big tease.

Haha true… on the flip side, it’s good we don’t have to find out anytime soon since we’re not old ;)

My LWR is over 20%. But considering I’ve had a six figure income for 7 years I should be doing better. We debt behind us, on to bigger things!

With a quick calculation I am at 40%, but is not entirely accurate. I did and do not pay FICA during the school year for employment that is part of my academic work (which is much of my income), plus it does not take into account rental income and such. But I like saying I am at 40%. ;)

I’m jealous you still get your statement in the mail! I too thought it was only online now. I would love to get that piece of mail. I would use it to as motivation to make more money than I did the previous year.

When I calculate my LWR, I get 45%. I don’t have the wife’s numbers, so I am just looking at my income and my investments. It will be interesting to see how it changes when I add in all of her stuff.

Ours is 35% is probably lower since our NW is from my wife and I but I don’t have her numbers. Still not too shabby and it’s increased a butt-ton since we started using YNAB and tracking our net worth.

I hate that SS website since it requires you to put in a new password every 6 months! COME ON!

“increased a butt-ton” – that needs to be the official slogan of YNAB, haha.. I’m gonna tell Jesse that ;)

I like the idea. I just calculated mine and I am near 36%, which is much better than where I was two years ago. I guess I can give you my number now. Can you text me later?

Interesting idea, I like it! Based on a quick estimate, ours is about 40%. Just curious, does the income from your pre self-employed days include employer match on retirement savings?

I don’t think so? Cuz they only get the #’s you paid taxes on yeah? But don’t quote me… I’m too lazy to look it up ;)

Nice! I’m not going to calculate mine right now cause I’ve been in school the past 6 years so it would look pretty awful, I’m sure… but as far as the SS goes, I hear people talk about “delaying” SS until 70. That doesn’t technically mean you have to work until 70, does it? It just means you are delaying taking the money.

That’s a great question! I honestly don’t know… I’d probably lean towards “just not taking the money.”

It means delaying taking your payments until 70. You can retire whenever you want and the longer you wait to take social security, the higher your monthly payment will be. As soon as you start withdrawing, you are locked into that monthly number until you die.

As a Canuck I’d have to pull up the Quebec Pension Plan amounts and I think I will do just that! I would need to work 10 years and pay taxes in the US in order to benefit from SS so we’ll see how life pans out and I will likely earn partial benefits from both countries. You are doing so well J. and have worked hard to put your family in a such a healthy financial position.

This is a good idea and something I constantly rant about on social media. Calculate the total earnings to see how much you’ve saved is a good way to judge overall saving and spending behaviors. After thinking it over the LWR can be skewed due to the fabulous market returning 35% on various years, so Net Worth is not a true measure of what you saved. The market returns inflate the LWR figures. Don’t kill the messenger! Besides that it’s still cool to know your ratio.

For sure – lots of variables to consider here. Main point is of course to just get a good idea if you’re on the right track or not. Which will be different for everyone.

In the “marry me” tier! Woohoo! Based off of my 2013 lifetime earnings and net worth at 12/31/13, I’m at 69.5%.

However, I owe that all to my parents. I was fortunate to be able to graduate debt free. Additionally, my parents were (and still are) big advocates of getting going on retirement early, so in my first “real jobs” (internships in college), they would match my Roth IRA contributions. (i.e. if I committed $2,500 of my earned money, they would gift me $2,500 to max out at $5k.) Considering I earned $6k-9k those two summers though, $2,500 was not an insignificant amount to me!

I fully anticipate this percentage to take a dip in the coming 5-10 years when I will purchase a home, but it’s an exciting number for the time being!

Work it! That’s awesome regardless of where the $$ is coming. You still had to stash some aside in order to get those matches form your parents, right? I like that idea of helping to motivate you to start early. My dad told me to start contributing from day one but it took me years to finally listen to him :( That match would have helped! :)

Great article and something I’ve never thought about before. Right now I’m at 50.8%, not too shabby considering I come from a family of VERY bad money managers and I’m a widowed mom (no life insurance from hubby) with two school age kids. Actually, I sat down and calculated everything I have going on in investments, pensions, etc. and I’m sitting very pretty for retirement, even if I stopped saving now. Time to work on health, I want to get to retirement age healthy enough to enjoy all those hard worked for savings!

Way to go!!! You’re doing an excellent job :)

36% if I include home equity, 28% if home equity is excluded.

Cool. I didn’t even look at my numbers. If I add in the cash in my pocket, my net worth is over the 1/4 million mark for the first time (home equity included).

That’s a good milestone to hit :)

I like where you’re going with this. I’ll have to look back at my statements and see where I’m at. And I’ll have to prepare myself to be sad when I see how much money I’ve wasted over the years.

BTW – SS website does have an option somewhere in one of the tabs where you can find out how much money you’d receive if you decide to retire early. You just have to make some assumptions about your age, income, etc.

Well that’s cool! Thx for the heads up

Damn. You made me look…90%

I think you’ve just won the prize for the day :) Congrats, baller.

Hey, is that net worth the house hold net worth? Then you need to take your wife’s earning into account too. Also, there is a cap on earning taxed on social security security. It’s probably more accurate to look at the taxed medicare earning if you made 6 figures.

My estimated benefit at 67 is about $2,100. Not sure about ratio because I need to look at my wife’s earning too. It’s probably around 70%.

Ahhhh good point! Totally left out the wife’s info, d’oh. Though most of our net worth came from me as she’s been in grad school pretty much the entire time we’ve been married, haha, so it’s prob still pretty accurate… Would be interesting to have her get her SS #’s though and then merge ’em all to find out. Too bad she hates talking about money (!!!).

(Oh, but also, that would mean we’d have another stream of income coming in if SS really is still around when it’s retirement age time from her… so that’s pretty cool. We’re just looking forward to the day when school is over and she’s got a 9-5 again. Can’t even imagine what it’ll feel like with a 2nd full-time salary again! Our kids are decimating all my earnings, haha…)

Hah, good lookin’ out man. I really like that calculation, as it doesn’t just show how much money you’re rolling in now, but it shows how much you’ve held on to.

It’s a sobering look at “how well have I don’t with my money over the years.”

Obviously, mine is TERRIBLE, and it’ll take a LONG time to bring mine back as I’ve blown through a CRAP TON of cash. But just looking at it now, I’m up to 14% (up from 9%), so already feeling a bit better.

Obviously, you’re a HUSTLER at 55%, which is awesome. It shows you put your money into assets and investments, not mall food and Reeboks (oops).

I can’t wait to get my SS statement, love combing through that thing! :)

^

done*

Ugh. Spelling non Mondays sucks…

^

on*

SERIOUSLY?!

Haha… thanks for being a good sport, mon.

I mean *min*.

I mean MAN!

;)

Just did mine… let’s just say “no you can’t be in my will”

OMG, this article sent me down the BEST internet distraction spiral ever. I now have the “lifetime earnings” for both myself and Will, which is fascinating info …

Good!! There’s not many things I’m good at, but apparently making random ratios up does the trick, haha… glad to have brought some joy into your nerdy world ;)

Yay, this was fun! Sounds like you’re taking on several new spouses, J. Money ;-) Question on Total Lifetime Earnings — as you note, the SS tracking caps this at the SS annual cap, so if you’re earning over the cap, shouldn’t you really be adding your gross income there? Doing so would, of course, end up lowering the LWR since the Total Lifetime Earnings is in the denominator. Thanks also for the link to the SS site to create an account and access my numbers.

Or if not replacing taxed SS earnings with gross income, then perhaps replace with taxed Medicare earnings?

Interesting indeed… I haven’t thought that much into it to be honest (kinda made it up on the fly – hah!) but I say work the numbers how you feel makes it more accurate :) My taxed medicare earnings were the exact same amounts, so not sure if my numbers are being capped or not. But you’re right – gross would probably get it closer, even though it’s not possible to SAVE gross money which then leaves you at a disadvantage there. So maybe it evens out?

Taxed medicare earnings seems like the more appropriate column to use for those that hit the cap on SS earnings. 210K/664K=31.6% at the end of 2013 (28yo). Estimated 42.0% at the end of 2014.

I’m Canadian, so a lot of this post was news to me. Especially the disability payments, yes I can see why people would game the system. That being said, we have something similar up here, but I’ve never really looked into it…

I had no idea that you could check to see your lifetime earnings for your social security account. I haven’t been working that long so I probably have no where near your total but still, that is pretty nifty knowledge o have at your finger tips.

You might not have the same hefty total, but you could very much have a better ratio depending on your habits! And that’s really the key here in this exercise. To see how much of the earnings are being put away into “wealth.”

I haven’t seen one of these in the longest time. I think I need to go to SSA.gov to check out my statements…and then feel shame at my low ratio. :) Great concept though, J Money. Do you count your home equity in that as well, you think, or should I take that out?

I think half of people will say it doesn’t belong and then another half will say it does, so there’s no real answer there I’m afraid. Just depends on your reasoning for tracking net worth and what you’re trying to get out of it.

Personally, I want a good snapshot of where all my money and assets are, so I most def. include it because it’s the biggest asset on the books (I don’t call it “home equity” though, I just list what it’s est value is in the assets column, and then what the mortgages are in the liabilities column – which in effect gives you your equity). I always find it weird to not have the house listed since then you can’t account for all the debt that’s then owed on it, unless the house is already paid off. Either way I’d just pick one for now and then roll with it. You can always change later :)

Personally, I sure DO count my home equity (and the mortgage on the liabilities side of things) — because I live and work in one of the 10 US cities with the highest home prices (most of the 10 are here in the SF Bay area), and once I retire I fully plan to sell this nice home and move to some other State where real estate prices are less than 1/3rd as much as here (that would be more than 90% of the US, I believe:-).

So that chunk of cash (difference between the price at which I sell the home here, and the price at which I buy a home elsewhere) will definitely be part of my retirement stash — would be silly not to count it (as it would be, BTW, not to count present expected values of pensions and annuities, including social security — but, that’s another story!).

For really top-notch accounting practice (as an accountant I’m very keen on that:-), I should probably add a “phantom liability” for the median price of a US home (less than $200k today) because I will have to live SOMEwhere (and renting is no cheaper). But living in a ZIPcode with median home prices over 5 times the overall US levels (in Palo Alto) that’s actually a minor (even though still important) adjustment.

Accounting requires more judgment and common sense than many other professions, at least when you’re striving to accurately reflect reality, rather than legally minimize taxes or make a business look shiny to potential investors. If your home’s value is roughly in line with median US prices then it may be better not to include in your “net worth” as selling it and buying somewhere else isn’t going to give you much, if any, added cash at retirement (though at that time you might consider a reverse mortgage, if you don’t much care about what if anything is going to be left for your heirs). Ditto if you’re planning to retire in one specific area with costly homes! But in a situation like mine, reality based accounting demands a pretty different approach…

The best part of this was seeing my earnings in the year 2000. Thanks Dad for hiring me to work at minimum wage for 36 hours one week ($187).

Since I’ve only had a few years of meaningful money making experience, I am going to wait until I file my taxes to calculate this for real.

Did you consider your wife’s lifetime earnings too? Even though me and my husband have different retirement accounts we have combined real estate investments, and combined expenses, so we probably should just have a combine LWR.

Hah! Go Dad.

No, I didn’t include my wife’s lifetime earnings in it mainly just because I didn’t think of it :) It would skew the numbers a bit, but she also only worked a few years full-time before going back to school so wouldn’t be that drastic of a change, at least I don’t think. Perhaps I’ll go back later and do more of a robust calculation and then post again about it… It’s all rather fun calculations! Haha..

Despite my love/hate relationship with net worth, the LWR certainly paints a picture of where you have come from financially. That number is all after your deductions and your taxable income only, which in your LWR certainly promotes saving and saving tax deferred.

Yup! I can’t tell you how many years I fully maxed out my 401k too (like, entire $16k or whatever it was back then) which shaves off a lot of thousands off the bat. So many vehicles out there to really take advantage of if you can!

I halved our net worth to get just “my” L.W.R, and it’s 23.6%. If I include hubby’s SS history and our total net worth, we go up to 27.4%. I had a few years of no taxable income during grad school, and it’s funny seeing those 0s on my SSA statement.

I’ve been reading all your posts for the last year and very excited about where my financial health is going. This number really made a huge impact on me as I’ve got a L.W.R. of 30% and I’m 25 years young now. I’ve read your reading list and many others so this really shows me that I’m actually making a difference with all your knowledge!

By the way when I talk about money with people I pitch them your blog because you’ve made such an impression on the way I look at my finances.

Thanks so much Martin – what a kind note! Thanks for telling me so today, totally made my night :) And way to go on all your saving! Keep going, you’re doing much better than I was at your age!

$984,562 earned for a whopping 60%. Uhhg, should be higher, then I’m off to Rule 72T!!!!!!!!!!

Is it bad that I had to google 72T?? :)

I am impressed with your LWR and tracking skills! I’m a bit on the low side because of my credit card debts but I will definitely try this out soon.

The LWR is another great formula to check progress. I added it to my never-ending spreadsheet and will use it going forward. I dropped this in just below an existing formula I found in The Millionaire Next Door, by Drs. Stanley and Danko. Borrowing a page from their book (literally), here is the formula:

So, how much money does a person need to be classified as being “wealthy”? This is actually highly subjective, in that “wealthy” to one person will have an entirely different meaning for someone else. However, as a rule of thumb, use the following quick test:

Index = (your age) x (annual pre-tax household income) / 10

Now compare your actual net worth with the index figure to classify your current financial position:

• A successful wealth accumulator has an actual net worth of about two times their index figure.

• An average wealth accumulator has an actual net worth right around the index figure.

• An under-achiever in the area of wealth accumulation has an actual net worth of one-half or less of the index figure.

Key Thoughts

“Building wealth takes discipline, sacrifice and hard work. Do you really want to become financially independent? Are you and your family willing to reorient your lifestyle to achieve this goal? Many will likely conclude they are not. If you are willing to make the necessary trade-offs of your time, energy and consumption habits, however, you can begin building wealth and achieving financial independence.”

— Thomas Stanley and William Danko

Great calculation (and quote) indeed! I love it so much that you have your own spreadsheet with all these in it too, haha… totally nerdy in all the right ways.

Thx for sharing, man :)

This was so great you really do make finance easy to learn.

I accepted your challenge before you even got to proposing it. Just too tempting to keep reading with out knowing where I stand.

Well at 27. I’m in the now we are cooking! With 18%!

And that is while servicing 60k in debt student loans and car note( note just sounds so much more sophisticated!)

Can’t wait to recalculate it next December!

Haha glad you liked! Let us know what it changes to in December :) We’ll have to do a recap later on to remind everyone to keep on sticking with it!

I’m mad I didn’t come up with this myself…..but, I’m at 37%

Also, btw, I read recently that most people didn’t signed up for the online access, so they resumed mailing paper statements every 5 years, at ages 25, 30, 35, 40, etc if you’re not registered online.

Interesting…. that would make sense, too. I do know that the quality of paper they now print them on is much worse – and in black and white – so at least they’re saving money there ;) And I’m pretty sure they printed them off in “draft” mode too – it looked/looks pretty bad, haha… I’ll gladly take it though!

Wow! you have done great since 2010. Wishing you nothing but continued success…but with as many tax shelters as you can find along the way. :)

Best Wishes! AFFJ

Thanks AFFJ :) You too.

This math is interesting. Consider – Say I made $40,000 in 1985, and saved just 10%. My employer matched 5%, so $6K saved. From 86-2013 the S&P was up by a factor of 17X, or $102K for the money saved that year. 30 years, and patience will reward me.

That said, our net worth is just over 50% of our lifetime earnings. Over 60% if you include the house. (Note – for my purposes, net worth doesn’t include the house, I need to live somewhere, but does include the remaining mortgage, it still has to get paid.)

As always, great article. Did you really trademark LWR? I love it!

Thanks brotha :) Nah, didn’t really trademark it but that would be pretty funny if I did! Just trying to have some fun…

This seems like a bit of a nonsense number as it is entirely age dependent assuming you earn any return on your investments. Basically LWR is smooshing together a few different metrics in away that is obfuscating instead of illuminating. A young person could be at 10% but actually on the pathway to an early and comfortable retirement while an old person could be at 70% and going to be soon eating dog food if they retire.

There are really two useful metrics:

Your savings rate tells you how well you are doing at saving relative to your consumption rate and this forecasts the total number of years you will need to work to support your living standard through retirement.

Your portfolio size combined with a safe withdrawal rate can give you a number of easy rules/metrics to give you a “retirement number” or other portfolio target that allows you to measure your progress towards retiring.

Those two things are useful starting points for savings and retirement planning and are relatively invarient or else self correcting to a number of idiosycratic parameters for a given worker. This proposed LWR on the other hand has strong variance with the time in the labor force and a number of other parameters. The proposed table of percentages is in fact meaningless since for a young worker they imply things are much worse than they are and for an older worker give a false sense of security.

For sure, there are tons of variables that go into this stuff if you’re seriously using it to figure out if you can retire or not (which this obviously is not set up to do, esp. considering I made it up on a whim ;)), but I do think it gets people to stop and pay attention to their money and habits which is never bad. And if your % is 5% vs 50% well it definitely tells you something more than not. I’ve seen far worse and complicated calculators that people won’t even touch out of being confused, so if this one gets you to take action and get a grasp of your finances, well, I think it’s done it’s job.

I agree on the accounting side of your post, but take exception with the “eating dog food” meme. I often shop at Sprouts near closing time (long working days, well remunerated though:-) and I notice a small crowd of elderly (though dignified) people waiting. I once got curious and asked. Turns out that (not an official policy, it appears, but a pragmatic reality), the local Sprouts at closing time inventories perishables (bread, vegetables, fruit) that wouldn’t be sellable tomorrow — and `sells` them for nominal amounts (like, 10% of displayed prices, I believe) to those elderly people. That’s cheaper than any dog food you could buy around here — and healthier for humans, of course; I guess that’s how you survive here in Palo Alto (if you have a place to live — rents are crazy) on SS alone; I’m sure Sprouts is not the only grocery store with a similar unofficial-but-pragmatic policy, by a long shot. There IS something humbling in reflecting that, “there, but for Fortune, go you, or I”… and on the fact that those elderly people love Palo Alto SO much, despite its crazy high cost of living, that they’ll go to such extremes, rather than sell here and move somewhere with a reasonable COL. (I like Palo Alto but as an immigrant myself don’t share that deep, undying love — once I retire, years from now, I’ll sell the crazy-pricey home here, and move somewhere, anywhere!, with a sensible set of real estate prices and other COL aspects!-)

Hi J,

Huge fan and love all your posts. Curious, any reason why we don’t use the “Taxed Medicare Earnings” # instead of the “Taxed SS Earnings”. I don’t believe the numbers on the SSA,.gov website truly reflects our lifetime earnings especially for high earners that reach the SS Earning cap.

“For 2014, the maximum amount of taxable earnings was $117,000. In 2015, the maximum amount of taxable earnings is $118,500.”

I think the Taxed Medicare Earnings is closer to true lifetime earnings since the cap has been lifted.

“In 1993, the Omnibus Budget Reconciliation Act removed the taxable wage limit for the Medicare tax beginning in 1994 and years thereafter. Therefore, there is no maximum employee or employer contribution amount for Medicare tax for 2014. All covered wages will be subject to Medicare tax at a rate of 1.45%. Employers will match the employee’s tax.”

Just a suggestion for your readers who want a better lifetime wealth ratio.

Dan

Yup, great idea. I didn’t really pay attention much to the two earnings columns because they were both exactly the same for me. So for you ballers out there it would be the better option :)

You might want to adjust your net worth figure to account for the fact that much of it may be subject to significant taxes (income taxes for deferred accounts and capital gains taxes for investments in taxable accounts), and so only ~80% of the total figure may actually be “yours”. But 100% of cash is definitely “yours”.

Sure, once you sell investments or the house/etc you’ll end up with less, but for now it’s 100% mine and I prefer the simpleness of just tracking the balances in all columns vs tweaking each one and complicating it more. I’ll burn out from doing that and I know that it’s not an exact science at the end of the day so for me it still does it’s job. If it makes you more comfortable (or any others reading this) to account for the different variables, by all means rock it! These worths are really only for us anyways, so set it up as you feel fit :)

Just stumbles onto your website and saw this article. You made me sign up on the SSN website (which I never know it existed till today) to pull my earning data. Combining me and my wife earnings, it’s a little over 200%

I have been tracking my NW since 2007 on a spreadsheet and recently entered everything into mint.com and personal capital.

Nice man! You guys are killing it – congrats! I guarantee tracking it all for the past 7 years has more than helped get you to where you are too – well done :)

Interesting post and good info on the SSA, I had no idea that resource existed.

My LWR for 2013 is 22% but I think it will be even higher for 2014, it will be interesting to see how it turns out at the end of the year. I check my LWR for the last couple years and it really bounced around alot, but that was due mostly to life changes…

Fun experiment

Good stuff J! Are there social buttons on mobile? I’m trying to tweet it out but can’t find da button.

sorry :( I suck at optimizing this site… thx for wanting to share though!

I like your writing and perspective!

Since I’ve been able to get through 50 years with just under $1.5M, and doing OK, it makes me wonder about the next 40-50 years (I’m at 25%). Especially since longevity is looking more and more probable for some folks. Enjoyed the article.

Hey, thanks Todd – appreciate you saying so! And liked that you dropped your total $$ and ratio too – us number nerds love seeing stuff like this :) Hope you’ll stick around and drop by future articles too.

I had never calculated my own lifetime wealth ratio before this. Hell, I had not even paid attention to the figures on the social security lifetime statement. It was eye opening to read this and then realize how much I earned, and how much I no longer had.

Certainly puts things in perspective, but motivates me to improve going forward. On another note, congrats J. Money on the last 3 strong earning years as a full time blogger. Trading time for money (aka the 40 – 60 hour work week) many of us have done is not sexy by any stretch, and your 100k reported earnings is considerably more when factoring in the write offs. :)

I’m thrilled to have stumbled upon this website and your concept of the Lifetime Wealth Ratio. Now that this has been invented, I think it would be really helpful and interesting to hear some thoughts regarding what the LWR would ideally be by certain ages or stages of life. For example, to be on track to a comfortable retirement you would want to ensure your LWR is at least xx by age 40, yy by age 50, zz by age 60. This probably isn’t as helpful to those that had good financial discipline when they are younger, but it might provide some useful guidance to those that are attempting to make up for lost time. Just a thought…

I think any time spent reviewing their money or this Ratio is time well spent :) It’s hard to put a number by the decades without generalizing, but I admit it would make for a fun and good exercise to do. I think what’s most important is just that your ratio continues to go up alongside the years. As long as that happens you know you’re at least on the right track. Your monthly expenses are a major part of this.

This should help with motivation though :)

https://budgetsaresexy.com/2014/12/proof-you-can-live-off-50-of-your-income/

First timer on your blog and love it! I wish I found it a few years ago. I stumble through my own money management (self tought, read a lot) and love to get more ideas without having to pay someone else to manage my money.

Here are my stats:

6’2″, 215 lbs

Age: 35

Married, 2 kids (boy and girl)

Credit score: 816 (found by using your recomendation, credit sesame)

Lifetime Wealth Ratio: 53% (you got me beat! Now I have something to shoot for)

Keep it comin’!

I am in line with your New Years resolution. I need to break away from the electronics and enjoy life a bit more. I am well on my way with my money, now I need to live (and find a few more income generators for fun :) )

Haha… Love the physical stats there :)

Hope you’re doing well with the electronics so far this year! I don’t know why I’m just seeing this comment now instead of when you dropped it 3 months ago (sorry!) but it totally made my morning.

Stay in touch!

This post inspired me to finally look at my SSA information. I was quite surprised by my record of taxable earnings but everything looks accurate. My Lifetime Wealth Ratio is 42%! Not bad if I do say so myself since I’ve never been a high-earner. Love this post.

Nice!!!

Way to take the time to look into it.

Should be a fun thing to track as time goes forward :)

LWR: 66% I have never looked at money this way before! Thanks for this post!! There is still room for improvement, but I am on the upward trend!

Yeah you are!!! 66% is dope!

This just in…

My LWR based on my Taxed Medicare Earnings: 41.85%

Here are the numbers:

Net Worth: $425,000 / Taxed Medicare Earnings $1,015,460 = 41.85%

Wow, what happened to that other 58.15%? I’ll chalk it up to living the good life. At least, I finally got my act together. I look forward to tracking this metric. Good article J$!

Love it, sir! Always nice to see an older article getting some fresh views again :) Especially tools you’ve made up!

Long time lurker, first post ;) Just ran this formula and I’m at 15%, which is far better than I expected! Excited to see the progress as we’ve made changes to our spending and saving habits. Thanks for the read!

cool! good job running the numbers :)

Another long time lurker, first time poster.

I was looking over this article and realized that I need to connect with the other half of my revenue generation to see what her Lifetime earnings are. Without her, we aren’t in our current house or have the emergency fund we do.

A great vehicle to talk about our financial landscape (which isn’t her fav.).

Thanks J!

haha don’t worry, my wife doesn’t enjoy it either :) so it’s good one of us does!

Wow you know this was a good piece when it’s 4 years later and people are still commenting. You’re livin’ my dream J!!! :O

I’ll peep at Jared’s because I’m only here as a house cat representative…92%. Do you want to marry my J, J? xD

XOXO :)

Wow. I’d never seen this post before. I was expecting mine to be around 50% based in the comments. It’s 72.2%! Not bad for a state-employed teacher. :-) I may make it my goal to get to a >= 1.0 ratio. Just for fun.

hell yeahh!!! you’re killing it! and will most def. hit 1.0 at that rate :)

Are you happy to add earnings from ten years ago as if it was last year, without any adjustment to the figures? I’m ancient, and your calculation puts me at over 100%, when I did nothing positive about wealth generation and spent most of my life teaching – a well known career for great pay. Is that ‘good’ ratio then simply a facet of age? Or could it be that surviving more than one boom-bust cycle makes a difference outside one’s control?

In theory time shouldn’t matter if you’re just saving everything you’ve earned, but realistically, yes – if that money being saved is actually in *investments* compounding like crazy over the years (which I’m guessing is your case?) then yeah – time most def. plays a part :) And is really the only way my ratio here is as high as it is too – the banked money keeps making more money to make up for all that I spent as well over the years! Haha…

It’s kinda nice that this is built into it though, right? That you always have a way to increase your wealth even if you messed up early on? If that wasn’t the case we’d all be screwed :(

I just wrote about this same topic yesterday, I swear I did not rip this idea off! Stumbled upon this on Twitter.

I called it “lifetime savings rate” which I know isn’t an accurate term but seemed simple to me. I like “lifetime wealth ratio” much better. Certainly deserving of that trademark!

I ran my numbers, looks like I have a LWR of 46%! Can’t complain about that one bit!

Not at all – congrats man! Awesome you wrote something similar too – makes me feel even smarter now, thanks, haha….

Hi Jay!

I have been wanting to write and seeing your Social Security income chart spurred me on. I connect with you on money because I love tracking it, saving it etc. I learned this from my parents who did a great job with and I am so thankful for their wisdom in all of this.

My income chart looks like yours… from the time I was 16 years old until I retired at age 55 there is only one year on the chart that shows no income and that is the year I was hunkering down to finish my degree to become a kindergarten teacher for 25 years.

It’s not what you make, it is what you save because teachers don’t make a lot but by age 50 I was able to build my dream home and I am living in it now and very happily retired.

I love saving because I love making my dreams come true and to me, that is what money is for.

I enjoy your site so much! Thank you!

Hooray!!! Congrats on not only retiring early, but being so HAPPY in life too! That is the key right there :) Really glad you’re enjoying the blog – thank you so much for letting me know!

Thanks for creating the LWR. I just calculated mine. I’m at 50%. I am very frugal. I put myself on a spending diet for the month of July. After calculating my LWR, it makes me feel good and reconfirms what I’m doing is worth it.

Very nice! Now challenge yourself to increase it by 1% every year until you hit 100% ;)

Hey J.

I was wondering this the other day as I was adding up the total compensation in my lifetime vs. my net assets. I am 70 and at 100%. Never saw or though about this ratio before.

Thanks for the article.

Heyy very cool! It’s as if you saved every last penny your entire life ;)

I think a better number would be GROSS wages and other income, which would not show up at all on the SS statement. You’d need a number for the gross income from Quicken, or a homemade spreadsheet, or paper records/ tax returns. The FICA number is misleading and does not take into account source of income (cap gains etc.) and reductions to income (personal exemptions and other deductions) If you own a small business many things are deductible, and would affect your net, but you earned the money. You also pay both sides of FICA so that’s a handicap that won’t show up in net. There are so many variables from household to household that the only way to make it useful is to start off with ALL money, made from ANY source.

My two cents.

BTW, my number using your method is 62.79%. Using my proposed tweak it’s 37.21%.

Cheers

Totally – the more accurate you can make it the better! (And even more impressive if you have all that data dating back your entire life ;) Unfortunately all that most people have are these SS statements – and many don’t even know they have those!)

I am scared to go through the same exercise because I think I will be depressed after doing it. At 41, it will just cause me to question everything, especially my current path where I am trying to play what I think it’s a long game. But great insight and gives me a lot to think about lifetime earning potential and what it means to me.

Love it, sir! I was looking over this article and realized that I need to connect with the other half of my revenue generation to see what her Lifetime earnings are.

Are you happy to add earnings from ten years ago as if it was last year, without any adjustment to the figures?

Not sure I understand the question?

If I found extra money that I didn’t include previously I’d go back and add it in yeah – whether it changed anything or not, just to make sure I was using all the data I had :) And these days with the stock market being all crazy I’m sure it wouldn’t improve anything much – hah!

I do something similar with my college students. They consider what their net worth is, and then I explain that that is their life savings. And for those with nothing, I say, “Over $XX,XXX has passed through your hands, and you have nothing to show for it.”

It really opens some of their eyes.

That’s a great exercise for young people. Thank you for helping students like this!

The older you get, the $$ number gets scarier and scarier. It’s good to keep this in mind as you just start building wealth.

Cheers Chris! Have a great weekend!

You can now calculate your benefit if you retire early on the SS website.

I entered $0 for future earnings (if I retire today) and it gave me the benefit amount I will get at age 62 etc.

This is assuming you’ve already earned the 40 credits which is generally 10 years of working.

This is awesome! I didn’t know this actually – thanks for sharing!!