What up finance nerds! Who’s ready to get into some credit score action today? Who wants to try and dethrone me off the highest score I’ve ever received in my life? :)

I hope it’s you.

I won’t get into the 101 reasons why it’s important to know your score and what goes into it all, but please believe me when I say it’s an empowering thing to know – even if you never plan on taking out debt again (and big emphasis on “plan” there). Your score can tell you a lot about how good you are with your money, and more importantly whether you get a kick-ass interest rate or not on future loans. Where a 1% difference can literally be a matter of tens of thousands of dollars more compared to the pretty boy next door’s loan who just happens to have a plumper score.

In this case, and this case only, it’s okay to be like that pretty boy :) And even more so if you’re trying to *get out of debt* too which is why these interest rates are so dang important! The more efficient your payments, the faster you become free and the sexier you’ll feel. Not unlike the almighty budget.

But there are thousands of credit sites out there – which should I use??

This is one of the most annoying parts to it all. It seems every day new places pop up promising free scores and fancy reports and yada yada yada – all of which only helps confuse us even more. Especially when the industry is strife with scammers.

Now I haven’t tested all of them, but some of the more legitimate sites are CreditSesame.com, Credit.com, Quizzle.com, and of course CreditKarma.com. The one that I personally love the best, as alluded to in this article’s title ;)

All of these places give out free credit scores, whether from Experian or TransUnion or the becoming more popular – VantageScore 3.0 – and you’ll probably be fine with any of them. You could also go to MyFico.com and others to get your FICO score too, however that would cost you and my personal feeling is that as long as you know roughly where you stand in the game you’re fine (vs pulling every single score out there and driving yourself mad!).

You may also find your score these days attached to other services you’re already using like Discover Card or Bank of America, or even my fave – USAA. But the only thing you get there is your score.

It’s also important to note that your credit *score* is different than your credit *report*. The score tells you where you stand, and the report tells you WHY you’re standing there. I.E. your credit history and every last credit line you’ve ever had opened along with the current statuses on them. They can literally be 60 pages long depending on how old you are and how much you love travel hacking ;)

You can get your credit report for free once a year at AnnualCreditReport.com too. Which sounds shady as hell, I know, but trust me they’re legit. And actually the only place authorized by federal law to exist for consumers.

So, Why Credit Karma?

For starters, they’re the only credit place I’ve gone back to more than once after setting up an account :) Like I said, the others are fine, but these guys are better. And I’m not just saying that because I’m now an official ambassador for them. In fact, that’s *why* I’ve decided to partner with them – their $hit is awesome! And apparently others agree too since they’re literally the largest of the group with over 50 million members and having given out over a BILLION free scores since launching in ’07. #BOOM.

So they definitely know what they’re doing. But here’s why I love them, exactly:

#1. They make it EASY for you to stay on top of your score (for free)

You literally log in and it’s right smack there in your face. Your VantageScore 3.0 from both TransUnion and Equifax. They update it once a week for you, and it’s completely free.

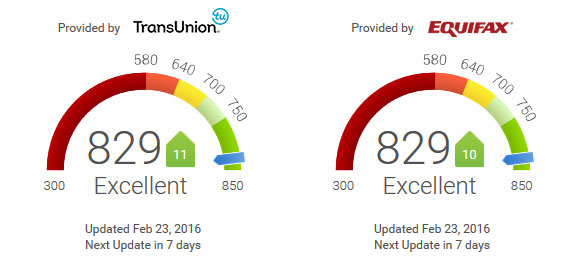

Here’s mine so you can see exactly what I mean:

As you can see, my score jumped up 11 pts since last week! The highest it’s ever been, coming in at 829 out of a max of 850. Not too shabby… And all I had to do was get rid of the biggest loans of my life, haha… We’ll see what happens when the bigger of the mortgages finally gets wiped away too :)

Btw, to learn more about the differences between all the different types of credit scores (FICO, Experian, Equifax, TransUnion, VantageScore 3.0) click here.

#2. They make it easy to stay on top of your credit REPORT (for free)

While you can also get it for free over at Annual Credit Report.com, those 60+ pages are NOT fun to look at. What I love about Credit Karma is that they import it right there for you *in your same account* so you can check that anytime you wish too. All under one roof.

They also make it drastically easier to review so you’ll actually DO IT, rather than print out your report because some financial blogger told you too and then promptly shove it in a drawer somewhere cuz it’s annoying as hell. Which it is :)

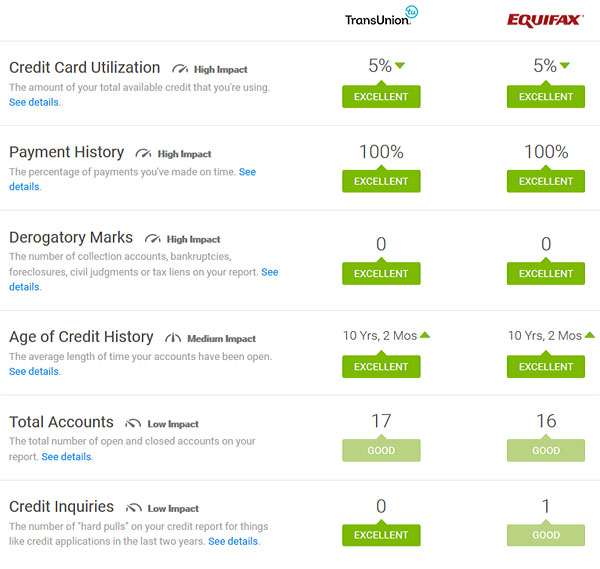

But again, w/ CK it’s literally just a matter of scanning our eyes downward once you’re logged in and seeing all the pros and cons to your history right there in the same spot. And believe me – your credit report does NOT do that. It looks like it comes from one of those old school dot matrix printers, haha… Only slightly better.

Screen shot again of my account so you can see:

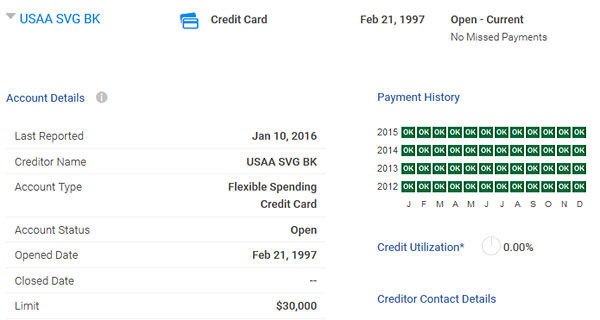

And then if you drill down into one of the categories there, say “Total Accounts” so you can see if one of your cards was closed okay or if there’s some error anywhere, you get this:

And then if you drill down into one of the categories there, say “Total Accounts” so you can see if one of your cards was closed okay or if there’s some error anywhere, you get this:

(Of course I found the account of ours that’s perfect, but we all have our skeletons ;))

Other great tools and resources:

They also offer a slew of other helpful things such as:

- A credit simulator — To show you how future decisions can affect your credit

- All kinds of calculators — Home affordability calculator, debt repayment calculator, simple loan calculator, amortization calculator, how-to-be-sexy-like-j-money calculator (hint: track your net worth!), etc

- An area you can track your spending if you’d like — Similar to Mint and all them, you can attach your accounts and watch for spending trends inside your Credit Karma account too.

- And recommended products — If you’re wondering how CK makes their money, this is it :) As all free services online do these days (while your score is free for you, it costs them money), they feature specific products they feel are good fits for your situation based on the info they’ve collected from you. So you’ll see the “best” credit cards, loans, refinance places, etc pop in here and there throughout the account. I personally ignore it all since I’m not in the market for any more cards, but you might find it handy if you are on the prowl for such things.

So in a nutshell you get your credit score, your free credit report, and access to a bunch of tools and calculators when you connect with CK. All of which is free and easily accessible.

My Challenge to You Today:

My challenge to you today, whether you use Credit Karma or your own favorite place, is to pull your score and throw it in a spreadsheet so you can start tracking it over time just like you do with your net worth (which I know you’re doing, right? RIGHT???). Or better yet, add a spot there in your spreadsheet so it’s all in one spot and you can easily update over time!

Then if you’re feeling ballsy, drop your score down below so we can all ooh and ahh :) Bonus points if you can beat me too – a fun little game my wife and I play, only one of us ever has fun at it, haha…

If you do end up checking out CK, make sure to tell them what you think below! They’ll be watching this so be as open and honest as possible (and feel free to ask questions). You can sign up easily here: CreditKarma.com

And remember, regardless of what your score is it’s mostly important to just KNOW where you stand. We hope to never need it again since it means we’re not planning on adding more debt to our worlds, but better to be safe than sorry if we can help it. Life has a funny way of changing up our plans, eh?

Happy credit’ing!

*******

PS: Checking your score with CK won’t affect your credit at all – it’s a “soft” inquiry.

PPS: As noted above, I now have a relationship with Credit Karma which means I’m compensated for spreading the word. Y’all know by now that I’d never pimp anything I find lame or hurtful to anyone, but gotta put it out there so you’re aware. I don’t rep brands lightly!

(Funny aside – as an online guy I always pay attention to the mistakes people make when trying to get to our sites, so to see how on top of it they were I typed in CreditCarma.com and sure enough it redirected to CreditKarma.com ;) That’s also a trick hackers/spammers use btw, so anytime you launch something important online try and scoop up the blatant mistakes people could accidentally type in and then redirect them to your main page! You might have seen this in the news recently with JebBush.com forwarding to Donald Trump’s page, haha… It’s since been taken down, but not Loser.com ;))

Get blog posts automatically emailed to you!

First, the Jeb/Loser thing is all really funny.

Credit Karma is FANTASTIC. I always cringe when I hear people use those pay for services. I get an e-mail near-instantly when I sign up for a new credit card. Additionally, it nudges me to check my score every few weeks. It’s cutting edge compared to having your brick and mortar bank do it, and it’s awesome. They push all the credit card options (and I have found that they aren’t the best sometimes), but it’s free so you just have to understand what you’re getting and why. *Off to check my credit score*

Very cool about the emails! I don’t get new cards often (ever?) so didn’t realize they did that. I want them to send me one if i ever hit 850 just to congratulate me :)

My son total me about the Jeb Bush web site. Pretty funny, seem like a internet prank that no one has taken credit for. I’ve been using credit Karma for over a year now. It’s got everything I need to keep an eye on my score. Thanks for sharing.

I love Credit Karma… I’ve had the app on my phone for years. It definitely gives accurate information, too. Too many people fall into the trap of using one of those services that end up charging you on a monthly basis – I think those sites are just scams.

Great write-up, I encourage everyone to get on Credit Karma if they haven’t already.

The one caveat I’ll give though… Don’t confuse a high credit score with a free pass to take out loans you can’t afford. Banks will give you a loan based on your credit score alone (a loan/alone… #wordplay), in many cases, that you simply can’t afford. I’ve seen it hundreds of times. Be smart!

Yup! Gotta trust yourself – not a bank. They all in it for the $$$$

I’m a fan of Credit Karma! Over the last year or two the website and app have gotten a lot more user friendly and clean and the information is incredibly valuable. Now if only my age of credit history would grow faster, I would be all set :)

I want it to grow SLOWER so we don’t get older along with it! ;)

Hey, J, our credit scores match! My credit card gives me my credit score monthly but only from Equifax. I like having Credit Karma for another source for the info. Credit Karma does ding me on total accounts – I don’t have or haven’t had enough apparently. Jeez, use credit wisely, live frugally and within your means and you’re naughty!!

I know, backwards system in parts for sure ;)

I like them too. I feel like they are similar to Credit Sesame but I haven’t delved into “investigating” the differences What do you find different between the 2?

Also have you read The One Week Budget by Tiffany the Budgetnista? I started following that plan recently

I tried Credit Sesame years ago but could never remember to go back and stay on top of… Not sure how they are now, but I know they didn’t have everything CK does going on! It’s the score + report that really makes it more worthwhile to me. I like stuff all under one roof. And even more so when it’s free :)

Thanks for the recommendation J. I had set up an account with Credit Karma a year or so ago but haven’t logged in since, I don’t remember what I didn’t like about it. Instead I’ve just been tracking the monthly Transunion score that comes with my Capital One card. The last I say it was only 768 :( two weeks ago. My credit history isn’t very long, but its getting there slowly. When we bought our house 2.5 years ago my score was just over 800 but instantly dropped to the mid 700’s once I had a mortgage. Getting two cards for travel hacking actually raised my score about 20 points, but I’m planning to close those accounts as soon as I get back from Kilimanjaro.

That always amazes me that card hacking can INCREASE scores when you’d think it’s the opposite (and maybe is for some people). Way to get a trip out of it – I suck at all that stuff :)

Travel hacking this trip did add stress to my life but it saved me at least $1,281.

As an update, I logged into CreditKarma and was very pleased with the information displayed by them. Between the two my average score they gave me was 769.

And then there is the ‘No credit card/I don’t care about credit score guy’ forcing everyone to tear up their cards! You should do a case study on how many people really tore up their cards in the class and how many are suffering today with higher interest rates because they erased their credit score! I don’t have anything against that guy. He is a genius in helping sucka consumerist ‘Murican to get out of the dumpster but equally stupid to force them erase their score.

Consider someone in the dumps with below 600 score. Once they take the class or clean up their act, their score can easily jump to 750+ which qualifies for an awesome interest rate!

I teach DR’s curriculum to high school students and personally follow much of what he teaches and I got out of debt in less than two months. Ultimately, I believe we give way too much power to banks and credit card companies and a single number is not a reliable measure of anything other than how a person handles debt. I have a great score but I also gave a lot of money to many different creditors. I would gladly trade the high score for the 1000s of dollars I gave the banking and credit industry. It pains me to think of how wealthy I could be now if I would have exercised some discipline early in my adult life.

Yeah, pros and cons with the “no score” route. I have a friend swear he’s going to buy all his cars and houses in straight cash which in theory means his score doesn’t matter as much, but I have still yet to see him pull off the house thing :) Cars he’s done and says even with renting them/renting places/etc there are services you can use to avoid needing a score, but all too annoying/extra work for me to stop caring about it. There are ways to increase your score too and still not use credit cards for those who don’t trust themselves with ’em.

I have friends with zero scores who are doing great. Bought their most recent home with manual underwriting, can buy card, and use debit cards as needed easily. Credit is not king, though I don’t think everyone needs a zero score either.

I’ve generally been satified to see my credit score with my credit card statement, but you make CK sound so sexy, I may have to take a look!

I haven’t tried it, but I’m going to check it out. I do get a score in the credit card dashboard, but this looks like it has more information. Thanks!

When my husband and I got engaged, he was kind of a financial mess in the sense that he thought ignorance was bliss. He had basically no credit and subscribed to lots of other money myths – basically because no one taught him any better. I showed him Credit Karma, and he still tracks his credit score religiously using their app even years later. His score is now knocking on the door of 800, and I think he might throw himself a party if it crosses the threshold. Needless to say, we have a friendly little competition going to make sure my score stays higher than his ;)

YEAH HUSBAND!!! WAY TO GO!

I know about where we are thanks to a refi last year. They told me our credit scores. They weren’t as good as yours (around 720, I think) but that’s because someone had put us into collections without notifying us we owed money (grrrr).

It’s paid off, and hopefully in a couple to few years it’ll go up.

That’s ANOTHER reason to track at least your report – you find out quick when someone is doing something shady… I got sent to collections TWICE within the last two years and they weren’t even bills I owed! They did shoddy research and attached them to me who happens to have the same name as another person in this great big world of ours – imagine that??

I signed up, and my credit score according to CK is 4-10potins higher than the one provided by Capital One Credit Tracker (altho that one updates monthly). I like the idea of being able to check once a week, and see how the weekly debt payments and paying off the week’s CC expenses are making a difference, both in my score and in my remaining balances. Thanks for the tip!

Speaking of Captial One Credit Tracker, I just got an email from them saying they are switching to the VantageScore 3.0 and going to officially start updating weekly. Should be rolling out in the next few weeks they said. I got a secured card from them to help my credit score and in 6 months my score has gone up about 45 points, all from a recommendation from Credit Karma.

nice!

Long time reader, first time poster. I’m on the opposite side of the spectrum of where I want to be currently but working on recovering from the early years of financial mistakes. Anyway, want to say that I am a big CK fan and BAS, of course. I signed both myself and my wife up a year and a half ago. Been monitoring our scores weekly ever since. It’s great to use and easy to see how your score creeps up from paying off debt. I also have to give a big shout out to CK for one of their sponsors/ ads/ recommendations area. The private loan recommendations are pretty great if you have the use for them. I was able to kill off some credit card debt by getting a private loan that offered a much lower interest rate. Keep in mind the term to pay off the loan is a lot shorter than paying on the credit card but it works for me because it forces me to pay extra towards that debt and it’ll be paid off 23 years sooner!

That’s so awesome! Thanks for taking the time to chime in and for reading the blog :) You keep that up and you’ll be growing that $$$$ in even fewer years, yessir..

I just signed up. The site’s very easy to navigate, much easier than our credit union’s free score. I am unfortunately lower than the hubby, but still solidly over 800 on both scores. I’m sure he’ll be rubbing it in, though.

800 is dope!

Credit Karma is also a good way to continuously monitor that your credit data is correct. My wife recently saw another name (not hers) showing up on her report. We reported it to the Credit Bureaus immediately. Our fingers are still crossed that it’s simply a mistake and not identity theft-related. I’d recommend logging in to CK at least once a month to check your verify the information. It doesn’t take much time to do so.

838 here! :). (About 2 months ago shown by one of my credit card accounts online)

AND during that same time period, I was denied for a new credit card because I didn’t have enough debt. We are debt free and mortgage free. Strange!

HAH! At least you can now say to everyone that you’re crushing J. Money’s score ;)

Well, truthfully, this was about a month ago and I have canceled two cards since then, so it has come down a little but still in the 800’s.

You win for now. But, I’ll be back. -Arnold impression-

I’ve been using CK since they came on the scene and I’ve always enjoyed them. I use the mobile app a lot. 808 and 805

My scores are up this month! I just started taking out credit a couple years ago, so my average age of accounts is my biggest limiting factor right now. Nothing to do but wait, and avoid opening new ones.

I do have something that I would like to see on the credit factors information pages though. I’m looking at the Credit Inquiries page, and I have some from almost 2 years ago. How long do I have to wait for those to “fall off” my reports? I think I remember 3 years from when I last looked it up. I know Google is free but it would be nice to see that directly on the page instead of searching myself. Thanks!

Hi Kyle –

Great question! Hard inquiries actually remain on your credit report for 2 years – they should fall off automatically after that. Hope that helps :)

Wow 829, you should soon become the CreditRockstar Super Master of the Universe !

They will probably have to raise the limit because of you !

Good job.

Hah! It only counts if I can *keep it there* now ;)

I love Credit Karma and have used them for years. Even though your credit score isn’t everything, it’s always a great idea to keep track of it. Keeping an eye on your credit score will go a long way in keeping you safe in case of identity theft as well.

To be honest I was pretty hesitant to sign up but now, having done so, I’m glad I did. My credit score is pretty good for my age (793) but I love the Credit Factors page where I can see what can be done to improve my score. The credit simulator was fun to play around with as well. Overall, the site provides great information while being easy to use and navigate.

So glad you liked it and gave it a shot!

I was using CK back when they only gave one score. Should be pointed out its even better now that they added the second one for comparison.

And speaking of comparison..I got you beat J$.. My score was 844.

OK, just kidding. It’s 791. You’re knocking it out of the park!

(I almost spit out my coffee!)

Just signed up to CK! 810 & 811, which is higher than the 795 reported on Mint yesterday at my free 3-month update.

Congrats!

Dang, I’m already in a competition with PiC and now I have to beat you too??? ;D I’m 792, it’s “low” because I do a slow credit card churn (1-3 cards a year) to finance half of our travel, and I tend to cancel the churn cards after a year or two.

If you have a Discover card, you can get your FICO score for free (https://www.discover.com/credit-cards/free-fico-score/). I use this, as well as http://www.annualcreditreport.com, to make sure everything looks good.

I may be paranoid, but I hate having my SSN out in one more place so I try not to :)

No shame in that :)

I’m so glad you posted this! I tried setting up a CK account this morning and it said that it was unable to verify my info. I was directed to annualcreditreport.com where I found out that Transunion still has my info under my maiden name. Weird! Gives me something to work on this rainy day though!

Great timing!

Yet another place not available to us Canadians. Boo. :(

Back to riding my polar bears and building igloos.

CK sent me an email at the end of this past year congratulating me on improving my credit score over the course of the 2015! I thought that was really sweet. I also have used the simulator to help with goal setting and used the site to get a 17mo 0% intro interest rate credit card!

Well look at that! They actually seem to *care*… If only others would follow suit!

First time poster… Just signed up for CK and my scores were 821 and 822. Not bad!.

Thanks for posting! And congrats! :)

FICO score is what counts and is accurate. I signed up for Credit Karma June 2010. I use it to see my activity but not my score. I would caution anyone not to get caught up in the score because it is NOT your FICO score. I would also caution people from posting your score because fraudsters troll the next looking for identities to steal.

It is best to check with Discover, AMEX and your mortgage company such as Nationstar because they offer you your FICO Score MONTHLY for FREE.

The difference between my FICO and Credit Karma is 125 points…yes, 125 points, so get your FICO.

Hi Susan! Hope you don’t mind me replying to your comment. Obviously, I work at Credit Karma. :)

Definitely true – Credit Karma does not provide FICO scores. Problem is, at last count, there were 49 FICO scores. So no matter where you get your score from, it’s likely not the one your lender uses to determine whether or not to approve you. The system is messy that way.

I agree with you that focusing on the score isn’t useful in itself. Personally, I watch the score for fluctuations and dig into my credit report details to make sure everything’s as expected. Sounds like that’s more your style, too. Great work staying vigilant!

Bethy @ Credit Karma

Thanks for replying. Yes, there are 49 FICO scores, but I’m thinking when most people apply for a mortgage, for example, it seems like the lenders, from my experience, are looking at the FICO score related to mortgages as opposed to a Credit Karma score. However, I still find great value in Credit Karma, which is why I have been a user for 6 years. It’s just that I’m more concerned about the different FICO scores from The Big 3, since that seems to be what drives lenders’ decisions.

I’ve been using CK for awhile and check my score regularly. And today it’s at 830! My wife is lagging behind at 826…I thought we were the only crazy ones who compete with each other for the better score.

While I can’t claim to beat the great and wise J$, I still came in at a solid 803/808 TransUnion/Equifax. Just have to continue the slow, steady march upwards. ;-)

Beers on me for crossing into the 800s :)

First time poster… I get our credit scores from our credit cards (discover and amex). My score as of Feb was 842, my wife was at 850 – three months in a row.

The credit card sites just give you your score. CK has a lot more detail. I will have to check it out.

I was at 850 back in 6/2014, haven’t been back since. I haven’t been carrying a balance from month to month -must have something to do with the amounts I am charging when I am trying to earn rewards points.

I make more money now, have a higher net worth, lower debt than in 2014, no new loans (i.e. I am a much better risk now), but my credit score doesn’t seem to reflect it. Arghhh!

How about an article on how to improve your score? I have ideas!

YOU ARE KILLING IT!! Way to go!!

Also – here you go :)

https://budgetsaresexy.com/2015/09/how-to-improve-credit-score/

788 and 773 on CK, I like that they used to have a historical record… I suspect it’s still in here somewhere but I can’t seem to find it!

Indeed, it is. (Hi, Jim!)

Log into your account and go to this URL: https://www.creditkarma.com/myfinances/scores/transunion-archive (accessed by clicking on your TransUnion score and then clicking the link below the score to the archive)

There’s an explanation of the switch to Vantage 3.0 as well as your history of the previous score version on CK. On the main credit score section you can see your history of Vantage 3.0 only. Enjoy! :)

Im around 773 and I’m really ok with that. I think 1 day I will eventually be ok with not really borrowing as I get in retirement. But that’s still 10-12 years away. Good luck beating J with his score.

I guess I get bonus points today J. Money, lol, as my score is a nice 850. I get that from my credit card. I also don’t mind going directly to the (big three) sources for my reports. I know Credit Karma is legit and a great way for people to stay on top of their score, but I’d rather not provide my social security number and just do it directly. Thanks for the overview! I always wondered what kind of detail and information folks received from CK!

Y’all are baller with your credit scores. I WORK at CK and some of you are beating me. ;)

I will say though, I’ve been working hard to hit over 800 for a while now. Wouldn’t you know it – I logged in today and surpassed the 800 mark with BOTH of my scores! Woohoo!!

This is terrible advice. Your credit score is useful, sure, but it is not something to spend time worrying about, and certainly not obsessing about. It is a tool used by people who want to lend you money to make sure they make as much money off you as possible.

Also, Credit Karma isn’t doing you a service, they are buying your entire financial history from you by giving you a number that may or may not actually be the one that’s used when you try to get credit. There’s no way this is in your interest.

There are many, many, many other things you should spend your financial energy worrying about. Reduce your expenses, pay off your debt, pay your bills on time, spend less than you earn, invest wisely (and often) and spend less than you earn (it’s important so I listed it twice). Trying to nudge your credit score higher, and watching it obsessively should be somewhere around 10,000th on a list of things to do financially.

I don’t think anyone here is trying to obsess over their score – it’s just good to *know* what it is and then watch it over time. You track your ifnances don’t you? Even though it’s not the root of all happiness? I’ll take the hate on helping people pay attention vs burying their heads in the sand all day ever day :)

The comments thread is full of people posting how their score went up or down by this or that much this month. Yes, that’s obsessing.

I also actually dispute that it is good to know what your score is. Unless you are going to take some action specifically designed to raise your score, or use your current score in decisions on borrowing, then knowing your score isn’t helpful. And I don’t think it’s a good idea to do either of those things, just pay your bills on time and do financially positive things, and your score will go up without you watching it. And going on Credit Karma, where they bombard you with ads based on their knowledge of your credit history isn’t going to have a positive effect either.

Yes, I track my finances, because it’s a measure of how much money I have, which tells me what I need to do to meet my goals and needs. My credit score isn’t a measure of anything useful to me. It’s a measure useful to companies trying to sell me things and earn interest from me. That’s the difference.

Agree with the ads/companies trying to sell us stuff, disagree w/ the knowledge part. There could be worse things to be tracking, and the majority of people who read $$ blogs *are* interested in doing something about it vs just looking up their score and then calling it a day. We’re all here to improve our situation and knowing what you’re dealing with is a part of that. Now can you leave it all be once you get going and have systems/habits in place? Of course. The ultimate goal is to not deal with money at all once you’re financially free. But no harm in paying closer attention in the meantime, at least in my opinion. Def. a balancing act though as anything extreme in one direction or another isn’t typically good.

J- I hope this doesn’t happen to you, but I sold my house in August and my credit score dropped 28 POINTS!!! In December, I bought a new house, and my credit score dropped 9 POINTS!!!

Nothing else has changes, haven’t closed or open cc’s, have no new debt, and continue to pay all my bills on time.

Yeah, buying/selling large items def. makes things wonky no doubt. Just sucks it went down right as you were needing your score to be high the most – I’m sorry :(

Hey J.Money – you’ve got me beat…I’ve got 824 and 822. We’re about to put our house (bought around the same time as yours) on the market though – so if/when it sells, we’ll be debt free! yay!

I’ve been using CreditKarma for a year or so, and track it on my net worth spreadsheet. I also get my FICO scores from 2 different credit cards, and right now they’re showing 835 and 842, so I guess they’re pretty close.

Thanks @Bethy for the explanation of the different FICO scores – I was wondering how they could be different!

Good luck on offloading the house!!! SENDING POSITIVE VIBES!!!

Wow, you are killing it. I wish my credit score was above 800! And I didn’t know that having more credit cards help . I’ll check out credit karma. I hope it works in Canada.

Hey J,

As requested, consider yourself “dethroned”. :)

I got 830/830 edging you out by the narrowest margin possible.

Also noteworthy: there are a couple of places you can get your FICO scores for free.

Digital Federal Credit union gives you a monthly Equifax FICO score if you keep the right savings account with them.

Walmart gives you a free monthly Transunion FICO score with their credit card.

It’s nice to see a FICO once a month since they tend to be used more for credit decisions. But I still use Credit Karma for day to day credit report changes.

And that’s how to get all your credit monitoring on the cheap.

Gene

Rock it, Gene!

I play the credit score “competition” game with my husband as well and he always beats be my a few points! Uuurgghhh. Right behind you at 820.

Love Credit Karma been using them for years! Keep up the good work folks!

I had to do a short sale on a house last year. My credit score dropped from around 820 and kept dropping each month for about six months, to a low of 712. Now it’s back up to the 745 range according to USAA. I really expected to lose about 200 points with the short sale, but it ended up being a little over 100. I think the fact that I never missed any mortgage payments on that house helped my cause. Unlike you, I could not afford to do the repairs and upgrades necessary to rent that house until it was no longer under water. I sold the house last May. I am interested to see where my credit score will be one year after the sale.

I must admit, I’m very envious that you have such a useful tool to be able to track your credit rating. Here where I live, credit ratings are hidden in the mists of time, and are much much harder to get a hold of. There’s nothing magical about it, and in reality they should be easily accessible.

Dang, that sucks :( I hope they finally catch on down the line!

I love Credit Karma. I used their website when I went on my recent app spree to boost the husband’s credit just in case we need to buy a home or rent a different place sooner than we thought.

Ok, I just signed up and looked at my credit report. It’s a good thing because there is an open account that I wasn’t aware of. Not sure why it’s still open because I think it’s a school loan that was paid off ages ago. Balance is 0. I’ll have to look into this. Thanks J Money!

Good catch! Hope it’s an easy fix :)

Love Credit Karma! I also write for them, so may be biased. ;) Everyone seems to have such high credit scores! Mine is listed at 764 on CK. I did just pay off my student loans and close a few travel hacking credit cards, though. My score has gone up by 40 points in the past few years.

This sounds like a great tool. I will look into it.

Thanks for the heads up.

NDQ

This is awesome! I’d been using freecreditreport.com to run my report but I think you have to buy your score. This is a lot like personal capital – great free service so they have the opportunity to present their paid options to you. Thanks bud!

Yeah dude – check it out! I still love freecreditreport, but you’re right in that you have to pay for the score(s) afterwards.

I first signed up for Credit Karma about 4 years ago. Our credit was less than ideal….440ish rating. My husband had heart problems that required surgery, no work for him for quite sometime. I worked 3 jobs (my main job, and 2 side jobs) to try and keep the bills paid. We worked our butts off to continue to pay off bills but some were late, some really late and you know the rest of that scenario, your credit rating starts running backwards like sand runs out of an hour glass. We moved from St. Louis to Locust Grove Oklahoma (I was able to keep my main job and work from home) as my husband was offered a job in the area. Once we were all moved, I signed up for Credit Karma and went to work diligently monitoring both of our credit ratings, and reviewing the negatives on our rating. I challenged 4 negative ratings and they were removed and never put back on. I took a Dave Ramsey course offered through the Cherokee Nation which helped with my Budget skills. We were paying cash for everything. I applied for a credit card in my name and would use it and pay it off. I saw my credit rating move up. I applied for a nominal secured loan, put the money in the bank and used it to pay the loan off in 6 months. I saw my credit rating move. We then did the same for my husband. Our credit rating is now moving in the right direction. We do not own, I’m in your corner on that aspect J-money! Although we want to buy some land and put a tiny home paid in cash so we do not owe on a mortgage. The best advice I can give you if you think it is hopeless (which I thought it was too) is to step in with both feet and put a game plan together. It won’t be easy, it will make you sick to your stomach, you will throw up, but then when you see your credit rating move 2-4 points, you will start to feel more empowered to be able to make that needle move even more!

YES!!! So motivational!! Way to hustle through and make it a priority! I was nodding my head the entire time reading this – thank you for sharing Nancy :) Going over now to check out your blog!

Hope you like it!

Can I claim you copied me?? I just posted about Credit Karma on my blog 2 weeks ago! http://www.hartzogswag.com/2016/02/karma-and-credit.html I’ve been pimping them out in my office lately. I’m more than proud of my 770! #noshameinmygame

The average age of my credit just took a hit because I signed up for an AmEx – the 6% cashback on supermarkets was calling my name! With my meal prep business, I spend oodles of cash on groceries each week. However, the credit limit the new card gave me puts my utilization at well under 5% each month – take that!

#hartzogswag

Hah! Nice!

Loving your swagness btw, you’re so hip over there ;)

Awesome credit score J. Money. You just wrote this post to brag :-). Seriously though, credit monitoring and understanding ones credit score is really important. Most of us on sites like yours are budget minded people. However, I bet some don’t think about how much they can save in a lifetime with a great credit score. No annual fee credit cards, zero percent interest on car loans, low mortgage rates, etc. It all adds up to a lot of money that can be invested instead of paid in interest.

Indeed it does! Knowledge is power is savings, baby… And such an easy thing to keep track of too!

I’ve used both Credit Karma and Credi Sesame for a while now, and I’m a MUCH bigger fan of Credit Sesame. I think the scores are closer to what was reported when I apply for credit and am sent the scores used in decision making, and the UI is much better.

Bottom line is they’re both great though! They both send me credit alert immediately (as in seconds to minutes after it happens), unlike the paid credit monitoring I’ve been given for being a victim of various hacks. I find Sesame to be a bit faster in alerting me, but minutes don’t make a difference in user experience, unlike waiting till the next day. It just leads me to believe they’ve put more thought into their software architecture.

I agree – either place is great :) And either better than none!

Very nice and informative review!

I’ve been stuck at an 800 on credit karma. Patiently waiting for it to rise. Considering I was at a 690 in 2014, I’ll take it. Must… Keep… Hustling.

800 still pretty damn sexy!

I’ve been using Credit Karma for years. A couple weeks ago I logged in and noticed someone had opened a credit card and charge $1700 and its wasn’t ME! I was able to report this as fraud immediately.

But I have noticed when I get my “real” score that its 50 – 60 points higher that what is reported on Credit Karma. I check to make sure the score is going up, but I don’t make any decisions based on CK score.

Ack! I’m glad you caught that error!! Just proves again how smart it is to watch this sorta thing – could have been much worse!

There’s no customer service. What a waste of time. They screwed up your account and you can’t fix it. Use credit card service instead.

Yikes, sorry to hear man! Haven’t had anything too terrible happen with my account yet, but I’m sure $hit happens… I’ll ping them and see if I can get someone to reach out to you and hopefully fix up :(

Hey!

I’m April, and I’m part of the member support team over at Credit Karma. I’d be happy to take a look at your account if you are still having any trouble with it.

If you haven’t already, you can also submit a support request here: https://help.creditkarma.com/hc/en-us. You can go ahead and write that you were directed there by me, April, in the subject line and I can make sure to take a look at this as soon as possible.

We appreciate your feedback!

Credit Karma does have its flaws. In the past month and a half I’ve experienced technical problems. In the total accounts category I been unable to view all my credit cards and loans. It keeps on saying that I hit a technical snag and to try again later. I notified Credit Karma of this problem a few times and still to this day they refuse to acknowledge the problem!!! People try nerd wallet or credit sesame, you might be better off!!!!