Hump Dayyyyyyy!

Came across this financial checklist over at Personal Finance Junkie this morning (how good is that name?) and thought it would be fun to see how many of these bad boys we can check off.

She says they’re good goals to hit by the time you’re 40, but really they’re great goals to achieve no matter your age, so whether you’re 20 or 60 let’s see how you’re looking so far…

I’ll go first, then your turn!

15 Goals to Hit On Your Way to Financial Freedom

#1. Build a starter emergency fund of $1,000. Check! The first step to getting things stabilized, and probably one of the hardest when you’re first starting out. Especially when you’re making minimum wage and stuck in the checking and savings shuffle game… I was king of that! ($50 into savings today, $50 back into my checking account at the end of the month when I’ve run out of money!) And the worst is that your brain only remembers the “saving” part, making you feel like you’ve saved when you haven’t ;)

#2. Organize your important financial information in a binder or eFile. Check! I still wanna do that Legacy Binder idea because it’s nerdily bad ass, but for now we keep our important $$$ and Life info into a centralized Google Doc, as well as partially printed out and stored in our safe. I do need to be better about keeping everything updated though as info changes all the time!

#3. Develop a monthly budget habit. Fail. What??? On a site called Budgets Are Sexy??? How is that possible?? Well, it’s possible because I spent 5+ years watching every penny and eventually got good at predicting my expenses without needing to look at it anymore :) I still think budgeting is one of the most important things to do when starting out, if not THE most important, but the good news is that once you’ve got a handle on everything you’re allowed to do whatever the F you want, haha… Even if you end up spending a little more had you continued to track it all :) So yeah – definitely still a huge fan of budgets and you gotta know where it’s all going, but my “budgets or die!” mantra has since eased up over time, and now I tend to focus more on the overall snapshot and trends (i.e. Net Worth) than I do tracking every transaction. If you’re a budgeting beast though and it’s working for you no matter what stage you’re in, more power to you!

#4. Pay off all of your debts. Fail. No budgeting and DEBTS?? What the hell kind of $$ blogger are you? Haha… An enigma? Wrapped in a conundrum? :) I don’t really know, but I have been known to go years without any debts whatsoever, so I guess this checklist caught me on a debt-year. Though does it make it better if I can pay it off at any time if I wanted to? (It’s our car loan – no credit card debt or anything)

#5. Build a mid-level emergency fund of $10,000. Check. You probably do need to be out of your teens and early 20s to hit this level, but fortunately as the years – and job skipping/promotions – continue, it gets easier and easier to start padding this boy. Though watch for kids and first homes and that bitch of a creeper, lifestyle inflation!

#6. Cut your expenses. Check. We could definitely be better, especially with the big three: home, car, food, but I’m giving us a pass here because we’ve come a far way over the years and planning on changing at least the home one significantly when we move next year. We’ve also been cable-free for over two years now – woo! (And iPhone free for over three!)

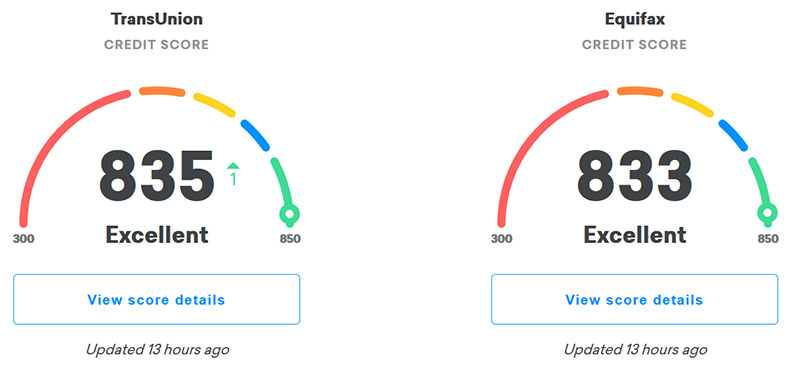

#7. Be aware of your credit score. Check. I use a combination of grabbing my free Experian score from USAA (currently 829), and then also my TransUnion and Equifax scores which uses the VantageScore 3.0 rating from Credit Karma (currently 835 and 833). There’s a ton of different scoring systems out there, but really as long as you’re monitoring one of them consistently over time you should be fine. If it moves sharply in any direction you know something’s up!

(Don’t forget – you can always get your free credit *report* every year too through Credit Karma as well as AnnualCreditReport.com! (I know that last one sounds sketchy, but I swear it’s legit :))

#8. Earn extra income. Check. My “day” job and my “hustle” jobs are pretty much mixed these days, but I have recently taken on more consulting jobs so I’m gonna go ahead and count that as extra since I had stopped for a handful of months. Big thanks to FinCon for letting me judge the FinTech Competition which brought in a wave of new business!

#9. Read the top personal finance books. Check. Although I’m much better about reading the top personal finance blogs since they tend to be more fun and relatable :) You’ll have to check out our books directory though over at Rockstar Finance as we recently polled over 100 financial bloggers on their favorites and then built a place to feature them all. Let me know what you think: PF Book Directory

#10. Automate your savings. Check/Fail. I automate a little of it, like when using Digit, but I tend to do most things manually these days just to have more control over it and appreciate it more. Like for example our new Spavings Experiment we’ve just started. Automation can be great, but don’t discount the power of consciously moving things over yourself too!

#11. Automate your bills. Check/Fail. I automate the bills that never change, but for everything else I just go in once a month and knock ’em out in one sitting to make sure all is kosher and the accounts have the funds needed when anything unusual is going on. Similar to the automation of savings and other areas, it makes me feel better manually handling stuff and forcing myself to check in at least once a month.

#12. Automate investing. Check/Fail. (Are you sensing a pattern here? :)). I automate some stuff, like our kids’ 529 investments and when I was experimenting with Acorns, but by and large I manually push money into my SEP or Roth IRA when it’s time again for all the reasons listed above. Although for my wife’s TSP plan (the gov’ts version of the 401(k)) we automate that fully, and I highly advise everyone else doing the same who has access to it, if not just to grab all that free $$$$ most employers give you!

#13. Write a 5 year financial plan. Major Fail. Haha… If there’s one thing I just cannot do no matter how hard I try, it’s to forecast my future. It’s amazing I’ve made it this far in the career/money world to be honest with you, as I can barely plan 5 weeks out no less 5 years! So anyone who can answer this question with a resounding “Yes”, or even a half-assed yes for that matter, gets major street cred in my books… I admire you greatly for being able to do that!!

#14. Start maxing out your retirement account every year. MAJOR CHECK!! Whew – ending on a good note here! My only rule with $$$ is to max out both of my retirement accounts every year ($20,000’ish total), and I’m proud to say that I’m now on year #7 or #8 so far and still going strong :) It’s pretty much the entire backbone of my net worth, and so long as you can do that you get a free pass at sucking at everything else, haha… it’s just a matter of time until you become a millionaire even if you do nothing else!

#15. Complete your emergency fund so you have at least 6 months’ expenses saved. Check. I dip above and beyond this number depending on what month/year you catch me, but as it stands we do have enough to last us if another penny didn’t come in over the next 6+ months… This is a tough one to pull off for sure though, especially if you’re doing #14 above. At least once you hit it though you don’t have to touch it until an emergency comes up!

So there it is! 15 financial goals to hit by 40 (or whenever)!

Looks like I scored a 10.5 out of a total possible 15, woops, haha… Someone take away my blog card! But it’s true – I could certainly improve in a number of areas, not gonna lie. Always something to work on, right? Life would be boring being perfect, or something like that? :)

A good exercise to check in on yourself though, whether you feel like sharing your results with others or not. All that counts is that you’re aware of what’s going on and striving to get better! And I’m rooting you on over here!

For those who do want to share though, let us know in the comments below what you scored, and how old you are if you dare :) Can be as easy as this, “I’m 37 years old and I scored 10.5 points out of 15. Yay?”

Thanks for the stimulation, PF Junkie!

Get blog posts automatically emailed to you!

Oh no! A car loan? Is it @ 0% interest?

My major fail is that the last time I checked my credit score was 5 years ago when we were buying a house and applying for a mortgage! I need fix this ASAP!

Luckily it’s a pretty fast fix :)

(And nope – not 0% but it is low around 2%-something (too lazy to look up right now :))

I scored an 11ish, but I’m good with that! Life is not about being perfect!

I sort of have my financial information written out, but it could probably use some updating and tweaking!

I have no interest in keeping a budget, but I do track my spending. In a year or two, I plan to stop tracking so intensely too.

We aren’t totally debt free, but I hardly count my mortgage as debt :)

My extra earnings are so low every month, they probably don’t count!

Good point about the budget! We’re in a similar stance; we do track everything automatically and ensure we can cover each month’s expenses without impacting our goals as much as possible. But it’s difficult to ensure you always follow a fixed amount in categories A, B, and C each month (even if you adjust / reset what those categories might need to be each month if they’re not a static item).

Totally agree – I feel the effort of tracking and budgeting, while keeping tabs on where you can cut expenses while working towards your goal is more important than making sure to hit each one.

It is much better to buy $50 of chicken when it is 50% off, than to wait until next month because of your budget and buy it full price.

11 is a major one for me. I have payments automated whenever possible. I have a BestBuy card that I typically use for the interest free periods. One of those periods ran out, and I didn’t realize it. I actually paid interest for 3 months until I looked at the statement. I almost died.

I paid off the balance and realized automation still requires manual effort to review statements.

Ouch! Sounds like you caught it way before it went to collections at least!

Boy, #10 was a KILLER. I’d pay everyone else, but even with an automated plan, I kept borrowing back money. Until one afternoon, I was looking at my budget and realized I’d succeeded at fulfilling everyone’s financial goals except my own. I needed money in the bank, and I had very little. That’s the day I set aside my “spending habit” and started a saving habit.

I figured if I could spend it, I could DECIDE to save it, and the result was HUGE.

Just by looking harder at what I really wanted, I got more savings for me. Great idea, automating it… When you really have to think about where it is, you might leave it there. :D

Good for you for turning things around!! quite a statement – “I’d succeeded at fulfilling everyone’s financial goals except my own”

I got a 12. Hated to fail on #4 (No Debt) since we had paid off our mortgage and were 100% DEBT FREE until 3 months ago, then decided to take on a mortgage for cheap flexibility. Since we have all of the cash sitting aside to pay it off, can I mark it complete? If so, I’d be a 13. Wait wait, 13 is unlucky, right? Whew, glad I took on that debt. I’m a 12. Definitely a 12…..

Haha… As you know I’m a-okay with carrying debt when you know what the hell you’re doing ;) So I say you stand proud at your solid 12!

10.5 is pretty good in my opinion. Mr. FAF and I are maxing out our 401k. We also have an intermediate emergency fund. We don’t have a monthly budget, but we try to stay under limit, and it’s been working out ok so far.

I will double-check this list when I get home from work today hehe

11.5ish here (age 34), but I don’t budget. I took your friend Paula Pant’s advice and use the Anti-budget! If you save your desired percentage off the top, you can spend the rest however you want. I usually end up saving some at the end of the month, too, because “scarcity mindset”.

Yup! A great way to do things as well. Pretty much the whole “pay yourself first” deal.

I am 30 and got a 10 – Yay!

Debt will be gone next year, followed closely by the maxing out of both our 401ks!

Will never get a 15 though – budgets ewwwwww

I’m over 40 :) and got a 12, soon to be a lucky 13. Good list!

In my mind you’ll always be 39 :)

I’m 34 and scored 14 of 15. All I need to do do is actually earn a dollar or two from my blog. Fun list. Thanks for sharing.

Well $hit – if that’s you’re only “problem” i’d say you’re doing pretty well! And so far hold the record here :)

I’m 35 and scored 11! I should hit 14 within the next two years or so. The debt one is going to hang around for a while though.

Because my eldest daughter is just 2.5 years away from college, I’m actually running a 7 year financial plan with full budgets for each year. We’re on the verge of being in the unenviable position of having a kid in day care and one in college while also still paying on two sets of law school-sized student loans. There’s no way we could navigate all that without a plan in place.

I feel the same way about maxing out retirement accounts being the backbone of our financial strategy. No matter what else we do from year to year, as long as we don’t mess with that we will be millionaires. Plus just by following that one rule we’ve already saved enough that we could retire comfortably at 65. That gives me tons of peace of mind.–Tasha

Woww – a kid in preschool AND college! You don’t hear that everyday… My wife is actually the youngest of 7 and I think when she was born the oldest sibling was out of college and i wanna say already getting married? Interesting lives people lead :)

Interesting list of items – thanks for sharing.

I’m 33 and 10.5 overall.

Breakdown:

(1) check, (2) check, (3) check/fail, (4) check, (5) check, (6) check/fail, (7) check, (8) check/fail, (9) check, (10) check/fail, (11) check/fail, (12) check/fail, (13) fail, (14) check/fail, (15) check

Pathetic Attempt to Rationalize My Lower Than Desired Score:

– (3) Budgeting and (6) Cut Expenses: we track everything via Personal Capital, but besides ensuring we spend less enough to ensure we pay our credit card balances in full each month AND meet our investment goals, we don’t set aside buckets or categories. We could do better here.

– (8) Extra income: just started and work in progress

– (10-12) automation: like you J, I like to track and monitor what’s going on. We do DCA on a number of apps / investment platforms, but I also lump sum invest when extra $ is available or when we’ve set aside $ within in account for a potential time to take a position. Overall, we call our accounts our (Semi-)Automated Ecosystem. I have a lovely drawing / mapping of them all – check it out :)

– (13) 5 year plan: no excuse here, just need to do it.

– (14) Max retirement: we just recently made a hard but definitive decision to STOP contributing to retirement accounts except the minimum match. I smacked myself for thinking this (no really, I did). In short, we want to build up our taxable accounts. Just posted on this a couple weeks ago.

I’ve seen your money map – I love watching how others do it!

Very interesting on your taxable vs retirement account idea… will have to check that one out as it’s a first in our FIRE world :)

Thanks, J. – I also like seeing how people coordinate their respective account set-ups.

Regarding the taxable (non-retirement) vs. non-taxable (retirement) accounts, I’m by no means an expert but we’ve found it to be an important consideration for our respective circumstances. A few points (more to come on a future post):

– (1) While certain circumstances enable access to funds without penalty in retirement accounts, Mrs. BD and I review these as “long-term” funds that we (hopefully) won’t need to touch until “traditional” retirement age. We plan to let compound interest work its magic as long as possible.

– (2) We graduated in 2007 (both 33 now) right before the market crash. After multiple rounds of structured lay-offs in several months, we managed to stay employed. With the markets at such lows and realizing we were just starting our careers, we went “all out” toward retirement savings and neglected other areas (emergency fund? what’s that? = not such a good idea looking back).

– (3) With an aggressive launch into our retirement accounts first, we’re now looking backward from traditional retirement age to today and thinking “damn…there’s nothing in between now and then.” So while our early retirement account efforts work their magic, we’re doing a short-term sprint in non-retirement accounts (though still contributing to retirement accounts via DCA for full matches and lump sum investments during bonus time to lower the higher tax bill).

– (4) I’m still new to the FIRE world (it’s HOT by the way!), but I’d be surprised if others haven’t discussed similar topics. Besides short-term / emergency savings or a “down payment” fund, the idea of a middle of the road investment bucket came to me from:

The Ultimate Financial Plan: Balancing Your Money and Life by Jim Stovall & Tim Maurer (I’m sorry, I can’t underline or italicize the book title…my high school AP literary teacher would be scolding me right now).

This book is dense. It has an enormous amount of detail around the intersection of money and life. A lot of ground is covered: saving, investing, and insurance, as well as various details on different accounts, products, and strategies. I found it very useful after establishing a foundation from some of the other materials I’ve read first.

– (5) Another item we considered is uncertainty – no one knows what will happen with future returns, tax rates, etc. Having funds in 3 types of accounts might be helpful to one’s respective needs in the future. Example:

– Pre-Tax / Traditional Retirement Account (401k, 403b, IRA, etc.) = currently at ordinary income tax rates for qualified withdrawals

– Roth (401k, 403b, IRA etc.) = currently tax free for qualified withdrawals

-Taxable Accounts = currently taxed depending on asset type, etc.

Throw in HSAs and other account types, and you can have quite the mix for your respective needs.

Overall, as you frequently mention, this will always be unique to each respective individual’s personal situation, goals, timelines, etc.

More to come soon :)

– Mike

Man, so thorough! I think you guys are going to be just fine in retirement later and be able to cope with whatever comes your way with analyzation/forethought like this :) I hope you do blog all about it for your readers to benefit from!

I was revisiting this post from last month and just realized that you replied again! I’m sorry for not reverting sooner.

We posted about balancing account types a couple weeks ago, so I hope it’s useful.

Also, I know we connected via email the other week about comment notifications (your response “it’s me – not you” cracked me up), but I’ll let you know if I come across any good solutions / plugins.

haha, thanks man – appreciate it :)

Hi J, What’s a mid level emergency fund? I still need to tally my score. Thank you for putting this together!

Hello Deanna,

I remember reading this in some finance book (am sure others can chime in too)

Emergency Accnt — Need in 0-3yrs

Short Term Accnt — Need in 3-5yrs

Wealth Accnt — Need 7-10yrs after retirement

The mid-level emergency fund listed here is $10,000, but honestly it really depends on your own expenses and lifestyle and general comfortability. Some people sleep better with gobs of money stashed away, while other prefer maxing out all their money into working for them and are cool using credit cards or other manners for emergencies. So I’d just choose something that makes the most sense for YOU and then shoot for that :)

#6. Cut your expenses, I feel like this isn’t really a check or fail thing. What I mean is that I feel like annually or quarterly reviews of expenses to make sure they are in line with your goals is better than just saying cut your expenses. Its really a continuous thing, because expenses are always find a way to creep in, and unchecked they fester and grow, much like a disgusting boil…

Yup yup – excellent point.

This is so true – lifestyle inflation check ups every few months!

Boom! Great list and hit them by 37….nice. Having a doctors salary without a doctors lifestyle definitely helps. Nice work on your end too. Major passes and minor fails.

Nice – you hit *all* of these??? If so, you have the new record here! :)

I am at 11,5 but then again I’m 62! We did borrow money on the 150 acre farm we bought 4 years ago, but that is down to less than 75k now. I’m not surprised by some of the experienced folks backing off on the hard core budgeting because the habits in their lives now support their financial goal (improving net worth). But for the rest of us, a doable and usable budget (even one that is fairly loose) is still a key step to getting on, and staying on, the financial improvement wagon.

.And I do automate every expense I can, even those that slightly fluctuate each month. I love reconciling a bank account that has NO outstanding checks each month!

Ooooh your farm sounds GLORIOUS though!!! I bet it’s so peaceful over there!

Love this list! Can’t wait to go through and answer these for ourselves.

21 years old and got a 10! Working on paying off the mortgage… Personally I find tracking expenses to be enough of a “budget” as I am pleased with our savings rate and monthly expenses for the most part. Good reminder to lookup credit score!

21 and already bought a house?? Impressive!

I’m at 15/15, but I’m 52! Regarding #13, I drafted out a lifelong financial plan at age 21 as soon as I graduated college. (Yeah, I’m a planner! ;) ) I still continue to tweak/update it every 5 years or so as situations change, but it has certainly helped to keep me on track over the years,

You. Are. Amazing.

I like this check list! I’m 33 and got 11 out of 15. Wahoooo! I still need to max out retirement accounts, cut more expenses, build a 6 month emergency fund, and make a 5 year plan. Thanks for the info about Legacy Binder, gotta look into that.

Take pictures of it and then blog about it if you end up creating one! :)

I’m at an 11…damn you, Legacy Binder! I am also a very bad money nerd because I haven’t read many of the most popular money books. I feel like there is so much contradicting advice it is best to keep my head down and keep plugging along. That being said, like you, I read a bunch of blogs (more contradicting advice but in smaller doses ;) )!! And kudos on your credit score! Mine is in a fluctuation period but it popped over 800 a couple times this year…not bad for having 4 short sales just 4 years back!! Time heals all. :)

Whoahhhh i didn’t know you had those! how come 4? playing the real estate investing game? You’ve turned things around like crazy now :)

(1) fail, but in progress, (2) check, (3) check, (4) check/fail, (5) fail, (6) check, (7) check, (8) fail, (9) check, (10) check, (11) check, (12) check, (13) fail, (14), fail, (15) fail

I’m 22, just graduated from college, and I’m at 8.5/15! I still have a lot of work to do, but everyone’s gotta start somewhere. I have an automatic 12% of my income deposited into my IRA and 4% deposited into my emergency fund. I am a recent graduate, so I still don’t make a ton of money, but I am currently working to plan well enough to max out my IRA by next year as well as to find a way to earn some extra income.

The one I was a bit lost on was the 5 year financial plan.. I have some goals, such as maxing out my IRA by my 23rd birthday. I guess a lot of the things on this list that I have not yet completed will be the beginning of my financial plan.

You’re doing great!! especially considering you’re reading FINANCE BLOGS right now haha… that was the last thing I was doing at 21 :) (and i wouldn’t worry about the 5 year plan stuff – so much is going to change in the next 5 years for you, so as long as you’re going in the general direction you want to be going you have plenty of time to strategize better later)

45 – 7.5. The one that triggered my attention was the Legacy File. I’ve made some decent progress in setting up my kids, but I need to work on how they’ll find the information they need should they ever need it. Crap, now I’ll be clicking links all day researching this!!!

Well on the plus side, once you’ve done it the first time it’s just updating every now and then! And even if you forget that part like I do usually, haha, it’ll still save everyone dozens of hours :) Just make sure you tell them *where it’s located* as without that it’s all for nothing!

I am about 10 at 51.

*My midlevel EF and 6 months expenses are one and the same and one of the few benefits from my recent divorce.

*I don’t have everything fully automated for similar reasons as J.

*I have a car loan. My teen’s hand-me-down 96 minivan croaked. So I got me a new car and handed mine down to him. #NotSorry. While I have a history of keeping my cars for 10 years, as a single woman, reliability will be a very important part of the car replacing decision. Public transportation is few and far between in my area and being cut back regularly.

*I do not have a side hustle, just a well-paying primary job.

*I need to catch-up on more recent financial books. I have read the classics. My I do follow the blogs.

I am very happy that I am now able to handle my finances in every way I see fit.

Good!!! You cracked me up at that #NotSorry line, haha…

Hit 11 which I feel pretty good about, 12 if you don’t count mortgage as part of the debt one. (age 30 FWIW)

We don’t yet have a 6 month EF. We have probably 5ish barebones months right now, but we’re making progress. By March we’ll have a healthy 6 months of regular expenses saved up!

I got 11! Fail at the budgeting, automation, and 5 year plans. As much as I love obsessively tracking my expenses, I’m actually not a fan of budgets. They are more useful in the beginning of your journey but later on its better to prioritize your spending instead. I also don’t do much automation for investments. I prefer to be conscious of what I’m doing (like you are). Useful for taking care of repetitive tasks but never a great idea to turn your brain off and let automation take over.

Great list, J! Thanks for sharing.

I think you’re allowed to do anything you want when you’ve reached financial independence haha….

I’m a 9.5, but with the exception of getting my financial info to a central document, I feel great about what I am doing. I became a widow unexpectedly 4 years ago and it took me about 3 years to fully seize the reins of my personal financial destiny. I pay every bill on the day it comes in and schedule my mortgage payments a month in advance. I fell I have more control of what’s going on that way. I don’t budget, but like you I have a strong handle on regular and seasonal expenses and have a set aside fund to pay those when they come up (insurance, property taxes). My only debt is my mortgage and I am starting to pay extra towards getting that paid off by the time I retire in 7 years. I have used your advice to start tracking my net worth and know I will be ok in retirement with my current contributions. I have cash set aside for emergencies and living expenses. I don’t care to predict my future, because life is too unpredictable ( as I am living proof- becoming a widow at 53).

dang, i’m sorry to hear that :(

i agree – life is just too crazy to predict!

love that you pay all your bills right when they come in and even longer for your mortgage. much harder to forget to pay stuff since it’s not all piling up over time!

Good list BAS. I got the house left as a debt and had six months saved but took half and invested.

Peace,

DFG

Awesome list! I’m 34 and got about 14 out of 15. The two items that I’m only about halfway on are:

#11 Automate your bills — Most are automated like Internet, Cell Phone, Netflix, but the variable ones are not and I don’t think they can be. But its only two monthly (electric and gas) and one quarterly (water).

#13 Write a 5 year Plan — This is also about halfway. I’m sort of a perfectionist and maybe that’s it, but I feel like our five year plan is a vague notion of “keep doing what we’re doing and hopefully retire in five years”. I’ve written some semblance of yearly targets but its not a comprehensive “written plan” like I would like it to be.

Haha…. I say the same thing to myself actually on the retiring/keep going part, even though I haven’t run the numbers in quite a while :) And i’ll probably be way off now that we’re expecting another kid (!)

I scored a 12. I would like to earn some extra side hustle money, but have not yet. I can, but don’t want to automate my Roth IRA contributions. I enjoy doing it manually every other week. I use automation for paying monthly bills and funding my work retirement saving through a payroll deduction. I have some debt still, but not much. Our debt to income ratio is less than 5% and we could pay it off at any time.

It’s a fun way to spend your money – throwing it into retirement accounts vs bills, right? i always get a nice rush from it :)

Great checklist bro..

I think you will success more than you know..

Build a checklist ain’t easy.. I’m also fail on budget too

Great list. I’m not doing as good as you, probably 9 out of 15 but some of those I’m okay with not doing. I have a mortgage so the debt in that case to me doesn’t matter, at 3.2% interest I’m good with that math.

One that I couldnever do is the 5 year financial plan. I just don’t think into the future that way. To me, life would always throw things at you that you have to adjust for, so I don’t know if it’s worth the time but I could see it helping other people.

Fantastic list!!! Word to the wise everyone – it’s NEVER too late to get your financial life together. My finances were a mess about 6 years ago (47 now) and I have 12 of the 15 goals underway.

It was hard has hell but worth it!!! There is no better feeling of liberation then not owing anyone especially a bank a damn penny!!!!

Keep up with the great posts and words of encouragement!

WORK IT!!

What in the world… I’ve never heard of #2. Um….wow I missed that completely, having backup is super important. We have 14/15…actually I think mortgage is debt? 13/15! Not bad! Thank you for the heads up on LegacyBinder btw!!!

Hahaha I think it’s actually really refreshing to hear that you’re not a budget nazi and have some debt. And yes, it does make it better that you can pay off that loan at any time ;) I only scored an 8 out of 15 and I’m 29. I’ll take that as a win though considering I only started to care about my personal finances 11 months ago. Can’t wait until that final debt is paid off, the emergency fund is fully stocked, and I can start focusing more on investing! This was a really fun read, thanks for posting!!

Rock on! And the fact that you’re now BLOGGING about money will only push you ahead faster as well – very smart :)

I can check off about 2/3rds of those. Sadly I’m pushing 50 rather than 40. Six months emergency savings has always seemed like a pipe dream to me. And I’m thrilled the years I can add anything to my IRAs. Fortunately I maxed my 401ks when I was younger and in a traditional job, so I have a good base. Freelancing is hard on the retirement front.

Thanks for the future post idea. I know that I have some work to do .

My score = 9/15, at age 36. Love the nerdily badass Legacy Binder.

I got 11, I’m almost 40, but they tell me I look 32! Does that count? ;)

Big fail on #4 as we have 2 mortgages on investment properties (but hope to pay them off in the next couple of years).

Not great at automation too. I really do like to ponder what to do with the money we save, and don’t like the idea of having money going somewhere every month. I tend to invest a lump sum every few months or once a year. It might not be the best way to do it for some people, but I much rather think about it and be really conscious about my choices.

You’ll always be 32 in my eyes :)

Ahhh…Thank you! ;)

8 out of 15 at 25 I feel ok with that.

11/15 and 30 here. Guess I have some work to do! But, I’m moving away from a budget. Too much work for this old man here… guess 30 is kickin’ in!

I use the DSS budget. Don’t spend sh/t. Very easy to keep track of! I wonder if that qualifies for the point? No budgeting or reconciliation. Just try not to spend unless necessary and unavoidable. Wish I could get the wife and kids on ma budget, but alas they refuse.

Haha…I’m going to have to steal that one.

#14. Unfortunately I didn’t start this one super early. I’ve only been at it for 4 years. I’m pushing nearly $100k with the awesome market and the company match though. My goal is to max the HSA in 2018!

Your 10.5 rocks J!

Conservatively scored a 11. #’s 4 and 14 are major fails for me. Have a car loan/mortgage and as I try to pay off the car loan, retirement savings and emergency funds are bearing the brunt.

5 year plan – career, life, money…it’s all just too variable. My longest job at 1 place was my last one 4.5 years. My side hustle I keep having opportunities come up and I will make more in November than I’d estimated (which isn’t bad), which makes 1 year of predictions / planning tricky let alone 5.

(Disregarding current tax mumbo jumbo) The changes in 401k & HSA limit increases also make it an unknown how much I could save.

I guess my ‘long term plan’ is save a bunch, spend a little. Since life will end eventually gotta enjoy the journey not just save. :)

I like that plan :)

I’m 28 and I scored 7ish. I wrote out a monthly budget guideline several months ago and started tracking it but then stopped. But I still make the same and I somewhat spend the same every month, I just dont take the time to officially track it like I used to. I’m getting ready to start earning extra money as a freelance copyeditor/writer soon, so once I buckle down and stop procrastinating on starting that, I will be able to check that off and hopefully make enough to check off the midlevel EF and max out my roth IRA. I think just having a retirement account while I’m in my 20s should count for something though, right?

I’ll give you a point for it :) But only because you’re also about to kick ass w/ the freelancing!

14 of 15 for me, I think having no debt is not necessary unless you are ultra conservative but thats just my opinion. Did you get a good deal when financing your car why did you decide to go that route?

I didn’t have the cash reserves at the time to buy it outright, and I don’t mind carrying around a little debt so long as I can comfortably afford it.

#2 is so underrated. I started organizing my financial info, taxes, general life documents online a few years ago. Helps me track progress and gain easy access to important information. Can’t say it directly helps me save or make money, but staying organized saves time!

Not to add another Fail for you but you can buy Gift of College gift cards at Toys R Us to invest in your children’s 529 accounts. The $5.95 activation fee becomes 1.1% if you hold off until you have the maximum $500 to invest in a single plan. The reason this is great is that if you use 2% cash back card you make a little. It’s far better when using to meet minimum spend for the big bonuses.

Hah – nice trick!

I’m getting close to 40 and scored a 13.5. I’m the same like you about automating bills where I automate bills where the amount is the same like our internet and others I check manually like our credit cards where I want to see how we spend during the month.

The other one I failed on is earning extra income. I started to look into monetizing my blog so hopefully I can start earning that extra income.

That would be nice! Most bloggers who start blogs for *passion* first are always much more successful later monetizing it than those who just start up blogs for the $$$ :)

This is a good list. I have a five year plan, but it has a lot of contingencies for things shifting. Very soon I will have that mega Emergency Fund and no credit card debt. It’s going to definitely reduce anxiety around money.

I’m 22, and I’ve hit 8 out of the 15.

Thanks for the list! This will be a great way for me to create some new goals going forward.

Good! You’re doing much better than I was at that age :)

Over 40? Is that age, IQ or waist size? My bday is soon & I think my IQ is catching up with my age. I’m 94 & scored a perfect 15 which means I have no life. Just kidding. I scored a 10 so it looks like I still have some work to do so I’ll get right on it after I get home from the bar tonight, LOL biggest downfall, car loan. Couldn’t resist 0% financing even though we have the cash in the bank to pay it off anytime. Also have a big fat mortgage but paying extra principal each month that will almost cut the term in 1/2. We max out our IRA’s & automate all fixed bills. As you said, we don’t budget every penny but have a good handle on how much is in our budget for various things like groceries, gas, & necessities like beer & wine (LOL just kidding). We cut the cable cord years ago & our cellphone plan is cheap too. Love Credit Karma to keep up with credit scores plus I just filed our taxes for free using it. This list gives me some ideas of other things to work on. Thanx!

Good! And it seems like you’re doing much better than others in the world, so try hard not to be too down on yourself with things :) I mean, after all you ARE on a $$$ blog right now like a true champ! Haha… (and I say that while literally drinking a glass of wine right now which makes your comment even more interesting to me, haha…)