Mornin’ mornin’!

So last week we went over 15 great financial goals to hit if you wanted to be ABOVE average in this wacko world of ours, but today I thought it would be fun to see just how close we are to being AVERAGE average compared to others ;)

Because why not, right? What else are we going to do today?

Stats are below in bold, followed by my own thoughts & answers… I’ll let you decide which areas you actually want to be average on, and which you don’t ;)

10 Financial Statistics of The Average American

(The data is mostly from 2015 and chock-full of other variables that we should probably pay attention to, but take them for what they’re worth and just play along with this blogger here ;) Big shout to The Motley Fool where I borrowed these stats from.)

#1. The average American gross household income is $71,258

Pretty decent… Our household income this year will be around $110,000 between my wife’s new job and my online projects, but obviously if there’s only one of you in your household it’s going to skew your results :) Verdict for us: above average

#2. The average American household with debt owes $132,529

Dayuuummm… Although it *does* include mortgages and student loans, cars, etc, so it’s not ALL credit card debt. We’ve opted to go back to renting so we don’t have any mortgages, but we do have a car note with $12,142.79 left which makes our verdict here below average.

#3. The average American gave $5,491 to charity in 2015

Pretty good!!! Probably because the higher earners skew it, but still – no shame in trying to keep up! And outside all the gobs of time I spend helping people with their $$$, we fail here with only giving about $1,000 in cash and donations last year… Though we did give out over $14,000 so far with our Community Fund I helped launch, and my $20/mo charity trick is now auto. pumping out $100/mo to 5 of my favorite organizations, so we are getting better! Verdict: below average (but not for long!)

#4. The average American has a FICO credit score of 700

Much better than I’d expect? I’m not exactly sure what my *FICO* score is, but I do know from last week’s checking that we’re at 829 with Experian and 835 w/ TransUnion and 833 w/ Equifax. So I would assume we’d be in the 800’s as well with FICO. And man are there a lot of different scores out there? You can learn more about most of them here, but again as long as you’re at least monitoring one of them consistently you’ll be just fine. J$ verdict: above average

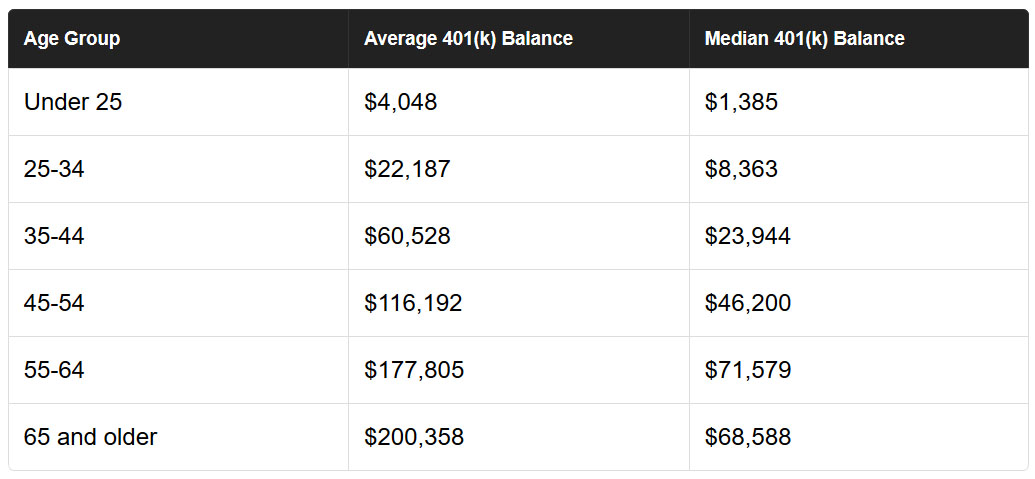

#5. The average American’s 401(k) balance is $96,288

I no longer have a 401(k) since becoming self-employed, but I do have about $504,000 in my SEP IRA which is an equivalent (minus those glorious free matches!!!) so it’s safe to say we’re way above average here too. You could also probably include IRAs and any other types of retirement accounts here which of course paints a much bigger picture, especially if you don’t even have access to a 401(k) plan.

Here’s a cool graph Motley Fool included that breaks down the average totals by *age* – which is a much fairer comparison. It comes from Vanguard’s 2016 How America Saves report (PDF):

(For more thoughts around this, check out my postings on Twitter and Facebook where there were some pretty lively conversations going in response to this graph!)

#6. The average personal savings rate in the U.S. is 5.5%

Ugh… Although apparently this is up from 1.9% in 2005, so yay? I’m never quite sure exactly how one goes about calculating their savings rate (do you use pre-tax money? After-tax? Does investing count? What about debt payments?) but here’s what I get depending on what I’m including – all based on pre-tax income:

- Actual “savings” rate: 0% (all our extra money goes to maxing out retirement accounts and debt)

- Investing rate: 26% (SEP IRA, ROTH IRA)

- Investing + debt pay off rate: 34% (SEP IRA, ROTH IRA, Car loan)

Verdict: above average

#7. Only 18% of Americans actively contribute to an IRA

Double ugh… I’m not sure what’s considered “active” here (I usually contribute only once a year to max it out vs monthly deposits) but either way not good, America. Not good! J$ verdict: above average

#8. The average American’s tax refund in 2016 was $2,860.

I know people either LOVE getting refunds or think it’s asinine that you “give the government a loan,” but as far as I’m concerned a nice surprise is always better than an ugly one. And I find that when people get a *chunk* of money vs smaller more frequent ones, they tend to apply it more towards bigger goals anyways since it seems to make a much larger difference. So to me it’s all in HOW YOU USE THE MONEY vs when you get it.

As for our typical returns, we usually break even since we pay taxes quarterly, however last year we got an unexpected return of $5,000 when we overpaid on part of some money that came in at the end of the year. Which of course went right back into investments! And again, a much better surprise getting $5,000 back than the opposite ;)

Verdict: above average (not sure how to color code this, haha…)

#9. The average American pays an effective federal income tax rate of 13.5%

Wow! Wouldn’t have ever guessed that! Not that I pay attention too much to this stuff (borrrrringgggg). And similar to the whole savings rate thing I wasn’t quite sure how to calculate this puppy either, however a quick Google search shot me a fast answer and was able to figure it out nicely.

Per Investopedia:

An individual’s effective tax rate is calculated by dividing total tax expense from line 63 of his 1040 Form by his taxable income from line 43 of that form.

Easy enough, right? For 2016 that came out to 17% for us (much lower than usual probably due to us taking a loss when we sold our house earlier in the year, as well as my wife maybe going back to work?), but for 2015 it was quite higher at a whopping 43%! Can that be right?? This is exactly why I use an accountant as I don’t trust myself to calculate crap haha…

(UPDATE: Per a commenter there is no possible way I can reach 43% tax unless I’m making over $1,000,000/year which I am most certainly not… So pretty much, I don’t know what the hell I’m doing here haha… (And even more reason to have a CPA! :))

Verdict: above average (I’m gonna say this is both good and bad: bad cuz we’re obviously paying more than the average, but good in that it typically means we’re also *earning more,* as well as giving more back to support our state/country too)

#10. The average American’s Social Security retirement benefit is $1,363/mo

Reason #38 to make sure you’re saving and investing on your own!! Can’t rely on anyone to support you in retirement :( I cant find my login/password to the site at the moment, but here’s what our future payments were estimated at two years ago. I’d imagine it’s only gone up?

(I like how “early retirement” is 62 btw… surely they haven’t come across FIRE blogs! ;))

You can easily access all your own social security stuff these days here: socialsecurity.gov/myaccount (provided you remember your password!). It’s also helpful when trying to run your Lifetime Wealth Ratio too that I conjured up :) Divide your current net worth by your *total earnings* over your lifetime and see what % of it you still have left! Just make sure to have a box of tissues around as most times it’s pretty depressing, haha… Verdict: above average

#11. Bonus: The average American will spend $165.14 on Thanksgiving expenses this year (via LendEdu)

If only that read Christmas! :) We’ll probably only be spending around $30 or $40 for gas and some side dishes to the dinners we’ll be attending this year (thanks mom and dad!), but I know some are flying all over the place which I’d imagine gets pricey pretty fast. Good thing we love our friends and families! Verdict: below average

(my favorite all-time gift, given to me by Baby Penny!)

BTW, right before I went to publish this I got two more T-Day stats emailed to me, by Ebates:

- 22% of Americans plan to begin their Black Friday shopping online after Thanksgiving dinner

- 11% of Americans admit to shopping on their mobile phones during Thanksgiving dinner

Wow…

So there you have it! The average financial stats of your fellow man and woman :)

Where do you land? More average than below average? More below than above?

It looks like I’m mostly above average in the right places and below average in the others, but areas of improvement can be found in both the charity and the effective tax rate areas… I’m still amazed by how all those early retirees pay 0% in taxes btw, even though they’re all millionaires!! Talk about being crafty!

See this post here by Go Curry Cracker to see what I mean: Never Pay Taxes Again (hint: you’ll need to live on far less than you’re probably doing right now to pull this off)

Thanks for playing along! No one else in real life likes talking about this stuff with me ;)

****

PS: Here’s the link again to the Motley Fool article if you want to learn more: 10 Incredible Financial Statistics That Sum Up the Average American

Get blog posts automatically emailed to you!

Wow, some of those surprised me and some of course depress me. I would have never thought that the average FICO score would be that high in America. Overall, this list makes me feel pretty good about my financial standing right now. However, like you, I need to start giving more to charity. Now that I’m in semi-retirement I hope I can do more of that with my time, as well as money.

I think I’m better off comparing myself to PF bloggers. The average guy makes me feel successful, warm, and fuzzy.

PF bloggers challenge me, keep me on my toes, and give me great examples to try to copy.

EXCELLENT point. Especially as the warm and fuzzies go away when it means that the country isn’t doing all to hot :(

Agreed; I’ve long stopped comparing myself to the average for my age group (currently 29), and used PF bloggers as my benchmark

Thanks for putting together and presenting the stats so neatly, J! I’ve seen different stats for average household income (i.e. 54k, 67k). Maybe it depends what metrics people use to measure it.

Below are our results:

1. Above

2. Below

3. Below

4. Above

5. Below

6. Above

7. Below

8. Above (I actually don’t remember exactly >_<)

9. Above

10. Not sure :D

With my 30 year mortgage in a high cost of living area that I pay off as slowly as possible, I’m way above that average debt number. It’s the only debt I have other than credit cards that are paid in full every month. Sometimes I really wish I lived in a place where you can buy a home for under $200K.

ME TOO!!! Haha…. If only you could chose where your friends and family are :)

Bah, who wants to be average? We definitely are similar to your results, but I’m trying to not keep up with the Joneses or Mustachians anymore! (note to self: Don’t try to keep up with J Money either…)

Fun topic! We will not be spending that much for Thanksgiving. $20 for our food contribution, $30 for a tank of gas, $10 for Friendsgiving and work celebrations, and $30 to go to the bars with friends on Friday and celebrate. It does add up quickly!

Wow, Baby Penny is quite talented.

Some of those stats are quite surprising such as the credit score, the 401K balances, the charity contributions,..they are all higher than I expected!

Eye opening stuff here. By the way, I’m not sure if I should admit to liking the Victoria’s Secret side bar ads here, since those are usually triggered by search preferences. Mrs. Cubert must’ve been working on a Christmas List. Still, a happy morning.

Anyhow, it’s interesting on the effective tax rate being so low. I think it shows how skewed the average is, when well over half of Americans fall into the lower two tax brackets. Would be interesting to compare this list again the median statistics.

Hah! Maybe next some items from your own wish list will start appearing and you’ll know she’s hooking you up ;) (On top of the Victoria Secret hook-up of course, a gift more for you than her – hah!)

1. Above, barely

2. Below, total on 2 homes <100K, <50% of home value

3.Below

4. Above, a little over 800

5. Below, The average 401K balance seems misleading because there are a lot of extremely high balance ones that skew the average up, the median is only around $26K. Mrs. C. and I combined are almost average between all retirement accounts.

6. Above at 47% of net income, that's something we gotta change as a country, the average guy at 5% isn't making much progress. I'm also concerned that this is similar to the 401K, that higher income people with higher savings rates skew the average up, where the median may be only 2% or 3%, or worse yet negative.

7. Above, max each year

8. Below, roughly $1,000

9. Effective Federal rate (not including payroll taxes) is around -1.5%. 4 kids and a lot in 401K/IRAs.

10 Right around average

11 Below, less than half that. No travel needed, but hosting for 13 people.

A negative percentage rate – hah! They’re pretty much PAYING YOU to invest and have babies :)

We are above average on about half of those. Unfortunately, above average on debt too – which I thought would have a higher average. But we are also self employed so that means we could change our average-ness by this time next year. I’m going to write these down and do a recheck in 2018.

Oooh good idea! Will you do me a favor and come back here in a year to post up your answers then so we can see how it’s changed? :)

Very cool post. Okay, here goes….

1. Income – above average

2. Debt – below average (for now, until we take out a mortgage)

3. Charity – below average

4. Credit Score – above average (virtual fist bump!)

5. 401k balance – below average for all Americans, but above for our age group

6. Savings Rate – above average (give me another virtual fist bump!)

7. IRA – above average

8. Tax Refund – below average (but isn’t that a good thing?)

9. Tax Rate – above average (ugh we need to work on getting that down)

10. Social Security – not sure

11. Thanksgiving – below average (my parents are cooking, and we’re just bringing a couple dishes and some wine)

This was fun!

*fist bumps*

For once, I’m above average :), notably:

#2 – I only have a mortgage & it’s balance is = to an average car loan

#4 – My score is in the low 800s

#6 – I consider my weekly 401K & savings account deposits plus my weekly mmkt transfers as savings (I “skim” off my checking account & transfer it to my money market).

Beautiful!

Mostly positive ratings. We’ve been trying to get our tax return lower every year but each year something new throws us off.

Great points everyone need to think about.

When it comes to the total debt calculation, I wonder if it includes investment debts. If that is included, I will be way below average. Now, the question is, if you’re below average because you borrow to invest, is that a bad thing?

As long as it all increases your wealth I think you’re just fine :)

@ Leo Ty. LY — I was asking myself that question as well. I’m on the same boat as you! hah.

Checking these numbers it seems, that unfortunately, my country is below average. Shame on you.

I’m not sure how to color code some things too! It’s like spavings x)

I don’t think any of these numbers are bad. The only bad one is how dismal the US saving rate is @ 1.9% before??? What the heck…

Our mortgage is way above the $100k average. Does that really include the mortgage?! I don’t remember houses being that cheap.

1.9 seems so wild. I’d love to hear more about the why and who all is included in that.

If you include someone who saves 0% but also has a much lower income, they are really skewing the high saver results

For the most part we are above average, except for debt since we owe less than $100,000 on our house. This is a fun list. Thanks for sharing!

#1. Way Above average

#2. So above Average that is negates #1 (Gotta love those DMV housing prices)

#3. Way Below average. Terrible but I feel like I need to get to a place where a significant amount of giving is sustainable.

#4. Somewhere in the 800s

#5. About double of the average and triple in my age range.

#6 about 25%

#7. yep

#8. Tax Refund….HAHAHAHAHAHA……

#9. I think we got it down to about 15% last year, still too much…

#10. I think I’m just about at max.

#11. Probably about $20 bucks, multiple family pot luck style.

The last 3 are tricky. I’m pretty sure our tax rate was below average in 2016. This year, it will probably be around average. More income, more taxes. I guess I can’t complain too much.

Hey, you should log on to My Social Security and get an updated number. $2,100/month is pretty good.

1- Above for the first time ever. Coukd’ve done it before but who wants to eork that much OT.

2- Below

3- Above

4- Above

5- Above since my parents once told us we’d better stsrt saving since they fully intended to enjoy their retirement so we should expect no major inheritance.

6- Above

7- Above

8- Below since last year I messed up and had to pay. But at least I had it in savings.

9- Above, but barely. Hey you got me to do some tax math, ugh.

10- Below, but barely

11- Above, but maybe I coukd move this to the giving column since most of it is for a big community dinner my church gives and the other is entrance fees my nephew and I to do a charity run/ walk Thanksgiving morning.

“my parents once told us we’d better stsrt saving since they fully intended to enjoy their retirement so we should expect no major inheritance.” – Haha…. your parents are my new favorite people :)

Very useful to see – thanks for sharing. Agreed with a few of the comments that it would be interesting to see the median (vs. the average) figures for some of the categories (#5, 401k balance, and #6, personal savings rate, in particular).

On our responses (either above or below):

#1. The average American gross household income is $71,258

= Above

#2. The average American household with debt owes $132,529

= Below (we no debt of any kind)

#3. The average American gave $5,491 to charity in 2015

= Below (we’re giving more away each year though so headed in the right direction for us).

#4. The average American has a FICO credit score of 700

= Above

#5. The average American’s 401(k) balance is $96,288

= Above

#6. The average personal savings rate in the U.S. is 5.5%

= Above

#7. Only 18% of Americans actively contribute to an IRA

= Above

#8. The average American’s tax refund in 2016 was $2,860.

= Below (this is an odd one; as you mentioned, some people think it’s good to get a refund and some people do not. I’m happy if we’re + or – $1,000 either way; we try to stay flat).

#9. The average American pays an effective federal income tax rate of 13.5%

= Above (to clarify, we pay a higher effective rate)

#10. The average American’s Social Security retirement benefit is $1,363/mo

= Above

#11. Bonus: The average American will spend $165.14 on Thanksgiving expenses this year

= Above

Wow, nothing like a pick me up in the morning to know that we’re doing a-ok.

It does make you feel a little sad though. Because math, on average, this is how well everyone is doing who you interact with daily. Imagining the stress I would be under in these circumstances, it’s their reality every day. Makes me feel blessed and also a little more understanding of what others are going through.

Exactly :(

Looks like I need to seriously uplevel on my charitable contributions!

As for Thanksgiving, I’m buying a tank of gas and some sweet potatoes and black beans, so I should be well below average there. #vegetariansavings :)

When I make food from scratch is it amazing how much money I save! If I buy veggie ham roasts or Field Roasts en croute in the box…not so much!

Dang, I fared well in most of these, but the 3 that caught my attention, and they should’ve all correlated to all come in above average, are #’s 1, 5, and 6. My income is just about average, but a single income household, and my savings rate is above average and I plan on continuing to bump it up, but my 401k is in sad shape after some missteps post double-income (postdoubleincome would’ve been a great blog name). This is one area I’d like to work on in the next couple years. My employer match is decent, but I gotta get my butt moving on this!

I just checked and postdoubleincome.com is available :)

Just calculated my ratio of net worth to social security earnings. 80%. Not bad. I’d love to know the average of that number.

nice!! You beat me by a good 30% or so… :)

Average is such a weird number. I mean Bill Gates walks into a room and everyone’s a billionaire, on average.

But that being said. We’re pretty good I think. The taxes are tricky and I don’t plan on digging out our 1040s with my tea.

I agree with someone above, comparing people in this community to Joe schmoe is a bit like watching Maury and saying our marriage is fantastic!!! Not saying I don’t watch Maury for that exact reason.

You’re too smart for this blog ;)

Wow thanks for showing these!!

I’m doing pretty well on many and have lots of room to improve on others.

My biggest help would be getting more income based side hustles, as they directly would go to savings + investing !!

The number that jumps out at me is an average effective tax rate of $13.5%. What?!?!?! I just calculated mine at 21%. How do others get it so low? Mortgages and charitable giving?

Am I missing something?

Also, regarding the average 401k balance – just remember that the average American has multiple accounts from various employers, rollovers, etc. This makes the average balance is very misleading.

For example, I have 6 total 401k accounts: 4 with my current employer (because of the weird way that they make contributions), an IRA rollover, and a very small old account. As a result, my highest 401k balance only has about 1/3 of my total retirement savings in it.

Yup yup – lots of different variables with these stats for sure. Across the board.

Woo-hoo – above average… who’da thunk it?! I guess if you actually care anything about your future, then you should be above average or working hard toward it!

It’s sometimes sad to see stats like these, but while a lot of us focus on the subject of money, there are too many folks out there who are just uninformed and don’t care enough. They think everything will work out fine for them in the end. And as we all know, that’s fairly unlikely.

Fun post, J!!

— Jim

I love comparison articles like this, but I’d much rather know the median numbers than the average. I also question the definition of “charity,” because I assume most of that figure comes from religious tithing, and as an atheist, I don’t consider churches “non-profit” organizations.

That said, here’s mine!

1. Household income: above ($127,000, single)

2. Debt: below (debt free!)

3. Charity: below (aiming for $2,000 by end of year, or 3% of take-home pay)

4. FICO: above (796)

5. 401(k): below (but I’ll hit $100k by the time I’m 30)

6. Savings rate: above (over 30% of gross income)

7. IRA: above (maxing out Roth)

8. Tax refund: below (I prefer to have greater withholdings)

9. Tax rate: above (20%)

10. Social Security: don’t know, don’t care since I’m not relying on it

11. Thanksgiving: above ($290 for flight to visit family)

Killer income! Especially at your age – well done :)

(And why wouldn’t religious tithing count in your book? wouldn’t any giving to benefit others count towards charity, religious or not?)

Thanks!

I guess it just depends whether you believe religion actually “benefits others.” ;)

Ahh I see what you’re saying. Well if it changes anything, only a portion of what you tithe goes to the actual church-church :) A lot of it goes to helping and feeding the poor, among a number of other things that directly impact the community for good that are non-religiousy. For what it’s worth, anyways…

These are amazing numbers! Some of them make me feel great, and others make me feel like I have some work to do. It’s hard to have a $96k retirement total when you’re 25, but that’s my next goal. ;) The 5.5% savings rate is abysmal, but wow, $5,000 for charity?? I feel like I need to be way more generous!

Sorry, J Money, averages are pretty worthless for this exercise — I think what you’re looking for is a median. If three households make $0 and one household makes $100,000 then the average household makes $25,000 — but three households still make $0! However, the MEDIAN household income is $0. With wealth and income inequality on the rise over the past 40-50 years, I think a median would be much more informative if you want people to compare themselves against it; even though the phrase “average American” is still what we refer to.

That would have been a fun comparison as well – if I had those numbers :)

Very interesting! This made me think the average American household was doing a lot better than what’s depicted in the media. That being said, I think some of the comments had a good point in that maybe the median would be a better representation. I still think it’s interesting to use it as a baseline measuring stick to have a general idea of how you’re doing. Thanks for sharing these numbers!

Man I’m shocked at the average giving to charity. We are way below in that category. I would like to see median because I got think Bill Gates is making me look bad here.

Haha, no doubt.

My results: Above, above, below (bad), above, above, above, above, below (good), above (bad – 19%), above if we get SS, above (not by too much, but we’re hosting).

We’re mostly above but that’s not always good (*cough* mortgage and tax rate). I’m working on some tax strategies with our CPA to make sure that we are being most efficient with our money the next few years, though that all might go out the window if the tax bill passes and I’ll have to start all over.

That’s all you can do! I love my CPA and always trying to optimize the best we can… (And she always puts up with all my random questions around business too which I’m sure I ask the same stuff over and over again haha…)

here is where i stand

1. above

2 below

3 below

4. above

5. Above

6. above

7. above

8. Above

9. Below

10. above

11. above

We’re blessed to be well above the American average in nearly all the aspects listed.

I can’t say I ever enjoyed being ‘average’, why start now?

Wow, the average FICO score is above 700 in America? That’s better than I thought. I expected to be hovering around the low to mid 600s.

Most of my answers were above average with the exception of debt, charity and tax refund. With debt, we don’t own a home yet so when we do buy one, we’ll most likely be above.

#1. Below

#2. Above

#3. Below

#4. Above

#5. Below

#6.Average

#7. Above

#8. Below

#9. Above

#10. Not Sure

#11. Below

For a hardly quarter life american, it somewhat makes sense to be average after all =)

1. Below Average – but I’m single so I’d be curious to know what the average income is for single people.

2. Way Below Average –

3. Below and Above – I work for a Nonprofit and outside of the money I donate I work plenty of non paid OT. Think that should count for something :)

4. Above Average –

5. Below Average –

6. Above Average – 21%

7. ? I contribute to a 403b

8. Below Average – My total refunds from last year (State and Federal) just under $800

9. Below Averge – 15.5%

10. Below Average –

11. Below Average – I spent $30 for the 10 pounds of Brussel Sprouts… the only dish I need to make

Brussel sprouts! Can’t say I’ve had those in decades!

Roasted Brussels are the best thing ever!!

J.Money, great post. Quick question. How are you contributing to IRA? Aren’t you and your wife earning too much combined to qualify? Are you doing that back door thing I’ve heard about? I still haven’t figured that out yet.

Nope – the income limit is $186,000 (if you file jointly) and we’re still aways from that. So we can max all we want! :) (Though the whole back door conversion stuff is hot for sure – tons of FIRE bloggers do that and blog about it)

I’m sorry but your #6 is totally skewed ! You’re not saving anything

True, we’re *investing* it instead of actually saving it, which I noted in my response :)

When you tally your 401k is that just for you or you AND Mrs. Money? Sometimes you say “we” and I never know if it’s a joint savings or just yours and you would use your 401k to support your family.

I feel like mine is low for my age (40’s) so I need to ramp that up. Also my investing amounts could be higher. :/

I just figured out my sad retirement account ($370k vs the avg $116,200) but both of those sets of numbers are depressing. My investment savings is a paltry $29k – gotta get on top of that. I feel like I should have so much more money invested/in retirement!

yeah, sorry about that – it def. gets confusing when talking about household money :(

for these answers here I just kept it consistent with the question – so like for the household ones I counted both mine and my wife’s stuff, but when it was focused on *individual* stats i just included my own.

so to answer your question about 401k $$$, my answer there ($504k) was from my own account. Which is much higher than my wife’s since she’s been in grad school and helping me pump babies out for the better half of a decade and only recently started working again :) Although of course it’s all *both* of our money.

That makes sense re your method for answering! I was just curious. My bf and I have separate finances but our coupled friends vary in how they handle that stuff so I never assume.

I am kind of embarrassed now that I’ve seen your 401k at how low my retirement (and investing) is! Got a lot of work to do.

Hey – we all start in different places! No shame in that at all. What matters is that you’re trending upwards and doing something about it all :)

1. above average (but we live in Chicago so we feel below average).

2. above average (again, the mortgage in the city puts us significantly above average but working on it).

3. Unfortunately, below average, working on this.

4. Above average, we’re both in the mid to high 700s.

5. below average

6. below average

7. below average

8. ugh! 2016 was a bad year for sooooo many reason, including a surprise pay in for federal taxes.

9. above average, who the hell only pays 13.5% federal taxes! I’ve been through many different income ranges and I’ve never been below 20%

10. above average

11. above average

#1. The average American gross household income is $71,258

= Above (285000)

#2. The average American household with debt owes $132,529

= Below (we no debt of any kind)

#3. The average American gave $5,491 to charity in 2015

= Above (Around 10K, we should give more).

#4. The average American has a FICO credit score of 700

= Above (830 plus)

#5. The average American’s 401(k) balance is $96,288

= Above (700K)

#6. The average personal savings rate in the U.S. is 5.5%

= Above (around 50%)

#7. Only 18% of Americans actively contribute to an IRA

= Above (max out both our IRAs and do backdoor Roth)

#8. The average American’s tax refund in 2016 was $2,860.

= Below (I always pay a couple of grand in taxes).

#9. The average American pays an effective federal income tax rate of 13.5%

= Above (20%)

#10. The average American’s Social Security retirement benefit is $1,363/mo

= Above (2918/mo at 67)

#11. Bonus: The average American will spend $165.14 on Thanksgiving expenses this year

= Below (10 lb turkey, sweet potatoes, pumpkin pie, cranberries salad, green beans, stuffing :-))

Dayumm – y’all are killing it!

Look at that Social Security difference if you wait to file until 70. It’s more than $1,200 per month – granted you have to wait. I did the math and the breakeven point for waiting to file for Social Security is 13 years. That is if you plan on living past 83 you should wait to file until 70 (all things being equal). Gonna keel over at 75? Then take that money at 62. Of course no one knows when they’ll die so this is just hypothetical. Nice post J – above average.

I wonder what happens if you don’t touch it until 100? :)

The problem with averages is you have guys like Jeff Bezos (congrats on the $100 BILLION!) skewing everything up. So that means that the real “average” person isn’t doing as well as the data suggests.

So if you’re “above average”, you’re doing much better than the real “average” American!

Haha a great way to look at it, yes. And either way even more reason to check and make sure you’re above-average, or getting there, or else it’s even worse then! :)

I guess I am not average then. I max out my ROTH IRA accounts and want to open more. Also, I save on average over 60% of my income. I plan to retire early and not spend my healthy years in a cubicle.

Killin’ it!

I’m above average in a lot of the good categories. Still unfortunately above average for debt since I’m at $150 in student loans + some credit card for dental and business. Life insurance will help me get to average here in the next few months.

I am actually surprised at the average household debt number. I have more debt then that due to a mortgage, I would of guessed others would as well. I do live in a HCOL area though.

Fortunately, I am doing better than the average person. If you are lagging, don’t let that bring you down. With some budgeting, any of these categories can be improved upon.

Wow. I’ve never been so glad to be not average at all!

Haha…

I think I’m above average where it counts. To your point, savings rates are incredibly subjective. I do “after tax” and based only on my “salary” and actually don’t include my AirBnB side hustle income since I wouldn’t be making that money if I wasn’t living in an expensive house that cost me that much money… :)

Wow, I am not doing as bad as I thought! I still have a ways to go though

It is impossible for you to have had a 43% federal income tax. The top rate is 39.6% and even with the ACA tax it maxes at 44.3%. Of course the first 400,000+ is at a lower rate. So unless your income was well in excess of $1,000,000, you didn’t even come close to touching 43% overall.

I honestly question the 13% average as well. 47% of households are at 0% and if you’re under $200,000 as a married family than you are under 13% if you just take standard deduction and personal exemptions and nothing else.

Under $200,000 is around the 95% of families in the US. I guess the extremely high earned income families might pull it up but it takes a lot of 44.3s to bring up 47 0s to 13.

HAH! Then I totally blew those calculations and must have looked at the wrong #’s or something… We def. don’t earn over $1,000,000 and have all kinds of deductions due to my online biz haha… But it’s good to know that it can’t get any worse than I already thought I was at! ;)

“The average American household with debt owes $132,529” COMBINED WITH “The average personal savings rate in the U.S. is 5.5%” absolutely terrifies me. I don’t think there has ever been a generation where personal finance is more critical to master than it is in today’s world. Aid in the form of pensions has all but dried up for the typical worker entering the workforce and social security could be next to nothing by the time some are allowed to draw from it.

Since 401(k)’s became famous for company retirement plans and pensions went out the back door, the onus was transferred to the employee having to be the major contributor to their retirement. Sure employees still had to contribute to pensions and still do for social security, but pensions guaranteed you a payout for the rest of your life. The payout now for the future retiree is whatever they put away in their retirement investment accounts!

Thanks for sharing!

I know – it’s scary, right? :( At least *some* employers automatically set up 401(k) contributions for their employees where they then have to go out of their way to un-check/tweak it (which study after study shows they don’t! Which is great!!). But even still – 3% + a match won’t do the trick if that’s all people ever do…

You’re 100% correct! Only putting in up to the employer match will never get you to where you want/need to be. Why our school systems don’t make it a requirement to teach 18 year olds entering the workforce/college about personal finance is way beyond me…

I actually wrote a blog post on that :)

https://budgetsaresexy.com/better-way-teach-financial-education-schools/

But I think it would only work if they make it *relatable* and *fun* for students! As no one cares about finances at that age, haha… (Call it “how to become a millionaire 101” though and there will be a line out the door to learn!)