[As part of our new weekly column by Mr. 1500 of 1500Days.com]

*****

Did you know that the Titanic almost didn’t sink? Here’s what happened:

The captain took corrective action when the ship was about 1000 feet away from the iceberg. The starboard (right) side of the ship brushed the ice, tearing open five compartments (the ship could sustain damage to four and stay afloat). The rest of the story lies at the bottom of the North Atlantic.

The Titanic came very close to missing the iceberg. Remember that it didn’t hit the ice head on; the ship merely brushed it. If evasive action had been taken 2000 feet out (1 minute earlier), the same maneuvers would have been enough to avoid the iceberg completely. If the iceberg had been spotted 3000 feet away, the captain would only need to have given the wheel a little nudge. And from a mile out, a very small input would have been enough.

Are you saving like the Titanic?

Early actions are powerful and the same concept applies to your savings and retirement. Let’s go through an example with the following assumptions:

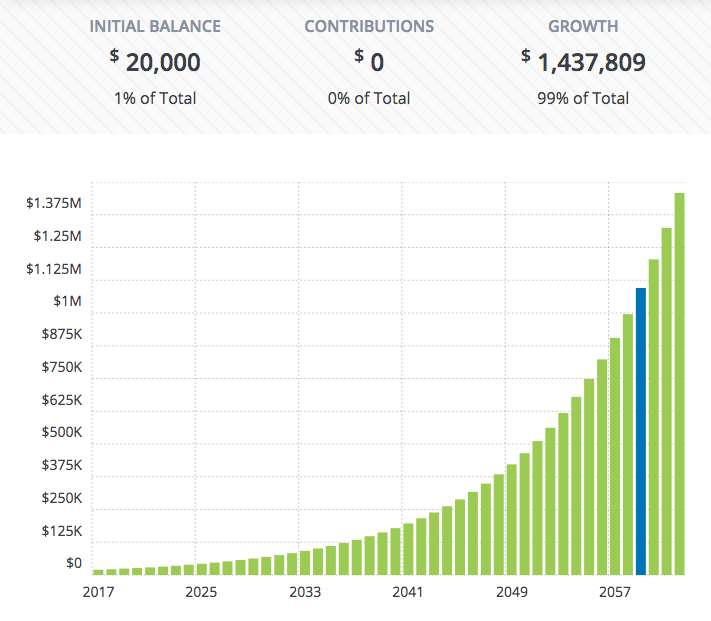

- Saver Sam puts away $20,000 at age 25

- Spender Steve also puts away $20,000, but waits until age 50

- Neither contributes additional money

- The rate of return is 10%. (This is consistent with the long-term return of the S&P 500 with dividend reinvestment)

Even though Saver Sam never contributed anything after the initial $20,000 at age 25, he’s going to retire at 70 with a healthy nest egg of over $1,400,000:

Spender Steve’s retirement isn’t looking so great. Since he waited until much later to take action, his nest egg sits at only $114,550:

Spender Steve, do not pass Go. Do not go to Boardwalk or even Marvin Gardens. Do not go to the golf course or the beach. It’s time to start looking for a side hustle!

The Problem (and how to solve it)

Just like the Titanic, waiting to save and invest until late in the game is a very, very bad idea. Having to earn income at age 70 isn’t as bad as drowning in the frigid North Atlantic (and may actually be a good thing; work keeps the mind and body active!), but it’s a lot better to work because you want to, and not because you have to.

The problem is that too many folks don’t think long term, which is one of the fundamental keys to success for acquiring wealth (if not the most important one). Never forget this:

You can always work for money, but it’s much better to let money work for you.

And the sooner you put those dollars to work, the more time you give those little guys to multiply. Give them enough time and they’ll earn far more money than you ever will.

The way to convince yourself to save is to consider the future value of every purchase. Allow me to illustrate with a real-life example:

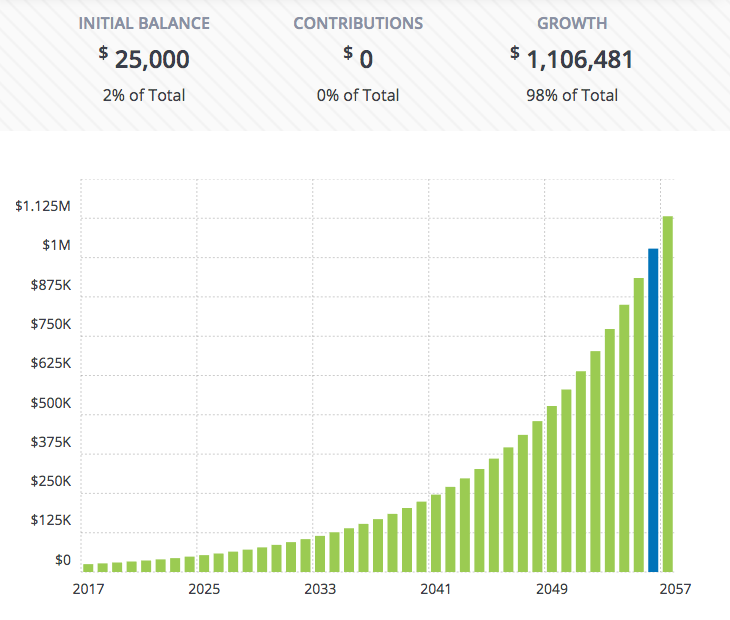

A family member (I’ll call him “John”) made a Titanic move recently. Instead of saving, he traded in a perfectly good car that was paid off for one that costs $25,000. The trade-in, with only 30,000 miles on it, had loads of life left in it. When I asked John about this curious transaction, he replied:

Well, I just wanted the newer model and I have a good job. $25,000 just doesn’t seem like a lot now that I’m out of college.

He took out a loan for the car, but to make the math simpler, we’ll assume he paid cash. It won’t make much difference in the final number. Here is what the $25,000 would be worth at age 70 if it had been invested:

Painful, isn’t it? John’s car didn’t cost him $25,000, it cost him over $1,000,000. And that’s not including the higher insurance premiums either. Sigh…

Don’t be like the Titanic

Know that I’m not telling you to never have fun. I’m only asking you to prioritize saving by doing one or more of the following:

- Keep your old car: It got you around fine in college. Keep it for another 5 years.

- Choose housing wisely: I hate the phrase “starter home.” Why can’t a modest home be a forever home? If you’re young and don’t have a family yet, get a roommate.

- Take advantage of free money: 401(k)s are incredible tools for building wealth. They reduce your taxable income and many employers provide a match (free money!)

Very small inputs early on can have huge effects down the road (or ocean). If Captain Smith had known about that iceberg from 2000 feet out, the Titanic would have sailed on its happy way. There would have been no movie; Leonardo DiCaprio and Kate Winslet could have been in Batman and Robin instead! (Sorry for planting the visual)

If you don’t start saving, you won’t die a horrible death, but you may very well end up working far into your golden years. And that’s a visual I’m not sorry to plant in your heads.

Get blog posts automatically emailed to you!

Nice post. It is so important to start saving early. To use the analogy of the tortoise and the hare, in the savings game, it is better to be the hare and race out to a big lead (save a lot of money when you are young). Then you could let the engine of compound interest carry you to the finish line.

-WSP

Finally – he wins for once! :)

Wow! Such a powerful story that perfectly parallels how our journey to financial freedom is. This analogy with the Titanic is surely memorable. Even though I’m already making my way to financial freedom, this has still struck and inspired me a lot! Will definitely share this! :) Thanks, Mr. 1500!

Yes! Oh man, we got some crazy looks when we traded in a SUV with a payment to have an older used vehicle that was paid for. Then when we had more kids, we paid cash for an older minivan, while my sister got a loan “because there was such low interest rates”. I love her, but I can say that my financially minded husband has definitely taught me the numbers behind our purchases.

I also don’t like the term starter home. As if moving isn’t bad enough, why pick a home you only want for a short time? It doesn’t make sense to me.

“Oh man, we got some crazy looks when we traded in a SUV…”

Some modern SUVs are almost as big as the Titanic!

And nice financial moves on your part. Cars are such a money drain and modern ones are so good, it isn’t scary to buy used or even high miles now.

Thanks for the post J. Money. Just a pity I didn’t hold to those truths when I wore a younger mans clothes. For me its the side game from now. Fortunately I love travelling and photography, so will find it in there somewhere

“when I wore a younger mans clothes” – haha… I like the way you describe that :)

“when I wore a younger man’s clothes” is from Billy Joel’s Piano Man.

“I will lease it for the first few years to keep the payments lower then buy it outright” was what I heard Monday night at softball – talking about a 2017 truck…… It hurt just hearing that rationalization.

Even though I understand compound interest, charts and examples like this still impress me, now I just need to distribute the o my softball team without offending The lot

You really laid out that point nicely. The last thing I want to do is starting planning for retirement with 1000 feet left. Over the next few years, I’m excited to see how much my investments grow through compound interest.

The third point about free money is the key to growing your savings exponentially. I think that saving money sucks sometimes. However, when I get free money just for saving, I am like a kid in a candy store. I will save as much money as I could whenever I get free.

Saving money doesn’t have to suck. Just find your motivation for saving. Once you discovered your motivation, saving money is as easy as 1-2-3.

“However, when I get free money just for saving, I am like a kid in a candy store. I will save as much money as I could whenever I get free.”

Yeah! Never understood how folks can leave money on the table! I mean, would you leave a $100 in the grass at the park? Of course not!

I like the analogy – a small correction in saving now avoids huge problems later.

I have an analogy I like – I think of each $1 saved as a factory worker that keeps on producing for me forever.

Fortunately, I did start saving when I was young so I’m FIREd now.

Nice man! And great analogy too – I like that one.

I’m having a hard time balancing investing in retirement and paying off mortgage early. Ideally, we should do both, but we have been focusing solely on the mortgage. I have a retirement account which my employer has been contributing to.

But that will change soon as my husband is starting a new job. We will need to think about our retirement more seriously.

I love mortgages in this low rate environment. Mine is a 15 year at 3.25% and I don’t put a dime extra into it.

Same struggle here. I do contribute 15% to 401K and double up on monthly mortgage payments plus some extra bonus help pay it down. I’m 51 and want to have it paid down by 55 so I can retire with no mortgage.

This is exactly why I didn’t order the Tesla Model 3. I knew that the money I would be using to buy it moves out the FIRE date and throws us into another loan.

I’m so glad I made the choice not to buy it! Now I have a nice USED car and growing retirement accounts.

And nothing stopping you from buying the Tesla 19 once you hit FIRE…

I hear those will give you the option to drive over water and clouds :)

I like your 3 examples of how to make better choices and save money at the same time. A lot of bloggers would tell you what not to do without offering any advice. Saving money toward financial freeedom has to be a continuous process but the big ticket items are the most important.

I’m more like 2000 feet out, or at least it feel like 2,000 since I don’t want a traditional work till I’m dead career… I didn’t take my 401k seriously in my 20s, now I’m just glad I’m self employed so I can load that SOB up right now $18K +25% match = 45K/yr right now, 54K next year. Even so, I’ll probably have to work till I’m 50-55 to hit all my goals… We will see, never really know where life will take you.

Paul. $45,000/year into your solo 401(k) is a beautiful thing!

This analogy rocks! We get so wrapped up in our little lives in the here and now that we often don’t see obvious icebergs in our future. Look up!!

We saved a bit in our 20s, but looking back I wish we had done a little better. Hindsight’s 20/20! We’re already showing charts like this to our kids in the hopes that they’ll learn from our mistakes and do better.

Thank you Jamie for the kind words!

What a great analogy. It really highlights how little changes early on can have a real impact on your life later on. Time is one of our most valuable assets, both in life but also in investing.

Luckily, I saw the light pretty early on in my working career. I was maxing out my 401k by age 24 and now, Mrs. NFF and I have built a pretty decent nest egg. We still have a long way to go before FIRE, but it is nice to have a good head start.

Staying small in housing is definitely the way to go. I started out big in a 3 bdrm house, then went to a 2 bd apartment, then into a 1 bedroom basement unit, and then into a studio. It’s been somewhat useful though to figure out exactly how much space I need. 3 bedrooms is way too much, and 2 bedrooms would be great if I could get a good deal. I think of how much money I wasted renting fancy places and wish I had sucked it up and gotten a roommate the whole time.

That would be SUCH an interesting post to read, Gwen! If you haven’t done one on all those downgrades over time – super cool :)

This is nice. :) I love the bit about it being easier to let your money work for you–it’s so true. I don’t have a lot of passive income since I’m still paying off debt, but from the little passive income I do have, it’s been crazy to see how it grows over time. :)

Great to see 1500 here on a regular basis. “The Titanic” is a great analogy to explain compounding. Creative chap, and a nice addition to J$’s menu.

Thanks Fritz for the kind comment! Life is good here on BAS!

Yeah, saving early is huge. I’ll make sure to drill that into our kid’s head.

I just read a book – The Unbanking of America. Really opens my eyes on how Americans are doing. The income just isn’t high enough for most people to save. I’m grateful I made good money when I was young.

Sounds like a fascinating read! Clever title.

I learning to retrain my brain to think about the economic costs of my decisions. For example, we were thinking about pulling from savings to take a last-minute trip. But that spontaneous $2,000 decision would cost way more than $2,000 in the long run. More like $20,000 come retirement time. We decided to plan better, and save the trip for next year. This way of thinking should be taught in schools! I have wasted so much time and money over the years. Oh well, you live and learn!

Krystal, if everyone thought like you, we’d all be a lot better off financially!

Ah the small things in life…they are good and they are powerful. Like any other type of improvement, making those changes early have the biggest effect. Why wait until you have a heart attack to improve your diet. You would be better off doing it in your 30s. Same for working out. If you start maintaining flexibility in your youth, you will have less back and joint pain when you are older.

You just convinced me to go sell my house. Now I have to get the wife on board….

(and now I have to go work out – damn you!!)

Love posts that show numbers like this. Very eye opening for many! In our buffer to share.

Ahh the classic waiting too late to invest.

I think people want to start investing when they have more money. They don’t realize they can start investing using the extra cash in their wallet or purse.

Once they take the first step step towards investing then everything else will fall into place.

Ah, how easily life is after some money is saved up. Not sure why more people don’t save more over a lifetime.

Congrats for your regular contribution on BAS btw! It’s like intertwined machine after the partial sale. Hope business and lifestyle for all have gotten better. I’ve gotta do some more outsourcing now. Hard to keep pace anymore.

Oh yes, me and the real world are finally getting reacquainted again :) Almost forgot there was life outside the internet!

Poor John, headed for an iceberg with that financial logic. Great metaphor though, as lifestyle inflation can really cause opportunity cost in the form of lost compounding interest. Over time that new vehicle will depreciate while the money spent on payments could’ve been working towards the end-game…. whenever that may be.

Loved the article, totally sharing this on my Facebook. I need the Ok, your 40 and you don’t have a million dollars in the bank, here is what you do article. LOL

Haha… you know what they say, the 2nd best day to start saving is today! The best one was 20 years ago ;)

To further the analogy, make sure you are the captain of your own ship. Vet every person/investment to make sure they are working for you in the way you need. Vigilance is important, because a key worker that slacks off won’t sound the alarm as they are supposed to.

Great analogy! I never really thought about it like that. Right now I save about $760 per month towards my retirement and I am 28. I was thinking about dropping it because I want to put even more towards my house fund but I am afraid of what the outcome may be when I am ready to retire.

That’s a good chunk every month!

Great post! Right now we’re maxing out Roth IRAs and are beginning to invest in 403bs, but unfortunately have pretty crappy options (high fees) at our schools. Hopefully by starting to save for retirement in our early thirties (the twenties boat already sailed), we will have a good size nest egg by the time we are ready to retire in addition to what we will receive as pensions.

Awesome way to illustrate the power of compounding interest and the importance of saving for retirement in a digestible way! I’m glad I learned this lesson recently and have been able to start saving early in my 20s. Thanks for sharing!

Loving the blog name :) Make sure to submit it over to our Blog Directory!

http://directory.rockstarfinance.com/submit-blog

I so wish I had done more saving when I was young. A friend used to make fun of me. Now she is 71 and trying to catch up. She now “hates to admit I am right.” I do ok, but wish I’d done more sooner.

Ouch… that’s a harsh one at that age.

Good analogy for compounding interest. Though it won’t work too well today. You’d be lucky if you can get 0.1% at a bank.

Also did you know the people who would have been against the Federal Reserve was on that boat. Saving money would have been a lot easier just like in your example. Plus we’d be saving in gold.

Fascinating!

And by “saving” Mr. 1500 is really talking about investing it all once it’s saved so it can grow.

Time value of money + compounding = win!

Getting a roommate is definitely a huge saver for me, especially if you can find someone you get along, life can be more fun too.

Hell yeah – I would totally go out and get a roommate if my wife allowed it :) I always joke about living with my parents (built-in baby sitters!) but so far no one is in except for my mother and my kids… 3 down, 2 more to go!

“I hate the phrase “starter home.” Why can’t a modest home be a forever home?”

Ohhh my God that is soooooooooo true. You know who is getting pay off this concept? Agents and their RE firms. We brought our current home thinking it’s just for 10 years but now obviously its a lot better financially just to stay put. Plus we love this house. And we’re lazy to deal with selling, closing, buying, packing up and moving. What a hassle. Stay put people!!!!

I just read a BRILLIANT article around this!! Agree 100%!

https://www.laurengreutman.com/why-the-term-starter-home-should-bother-you/

Love the analogy BAS! It just has me thinking why I hadn’t come up with such an analogy (kidding). But this easily shows the power of compounding and why it is critical that you save at a younger age and start the process of having your money work for you. Each decision should be made with a long term perspective and you cited three examples at the end. But a car that you can drive to 200k and can last well over 10 years. Buy a house you may never have to leave. Don’t incur those RE fees, the costs of financing, the cost of moving, etc. My wife and I are getting ready to move into our first house. We made sure we had a house that we knew would be big enough for our family not just 3, 5, or 10 years from now. But also for 20+ years. We will most likely never have to leave (until we are ready to downsize). Sorry, got on a rant there! Thanks for the great read.

Bert

Beautiful man! Congrats!!