[Welcome to the new Early Retirement Series we’re starting here! Profiles of hustlers who have cracked the code and now living the dream on their own terms. We’re starting with my boy Jeremy from GoCurryCracker.com who not only shares the intimate details of his journey, but also how – exactly – he was able to reach this financial freedom while now traveling the world with this wife. Enjoy!]

It had only been an hour since I sent my “Retirement” email around the company, and my inbox was already nearly 400 deep. Even the guys that were always triple booked wanted some one on one time.

“Dude! Can we get a coffee?!”

“When I get back from China we have to get a beer. This is crazy!”

“WTF bro! Let’s get lunch, I’ll cancel my lunch meeting.”

What’s a guy to do with such overwhelming demands for his time? Milk it for all it’s worth, that’s what. I scheduled as many free coffee dates as I could!

Just 2 weeks earlier, thanks to a little encouragement from my employer, we had finally built up the courage to quit our jobs and travel the world.

How it Came To Be…

“This is bullshit”, I said as calmly as I could muster, before walking out of my manager’s office.

I felt like I had just been kicked in the nuts. In a game of corporate politics, I had made a calculated decision. And lost.

A year earlier, I was the golden child. I had been pulled in to save a failing project, and delivered. Afterwards our Vice President had come to my office, “If you want or need anything, anything… just tell me. I will make it happen.” I cannot even begin to describe how incredible that felt.

I was asked to take on a greater challenge. We were severely understaffed, our schedule was completely irrational, and yet… after a year of 80-hour weeks, sheer determination, and a great amount of luck, I had under promised and over delivered.

My manager struggled to get the words out, doing his best to avoid contact. “We love what you are doing. I don’t know how you got the team to deliver the way you did. It’s just… we need you to be more of a politician.” I felt the life drain out of me.

I had ruffled some feathers. I said “No” to the wrong person. For the first time in a long time, my performance review went from an A to a B.

I used to get B’s fairly regularly. I did my job, doing what was asked to the best of my ability. Then one day it finally sunk in: I didn’t need this job. I had enough money in the bank to fund several years’ worth of expenses. I was more confident to take risks. I challenged things, offering ideas, a better way, a faster way.

Now I had just been punished for what was once a reason for praise. I felt betrayed. It hurt in my gut.

The Day it All Went Down.

My wife Winnie was out of town visiting family, so I called. “We’ve been planning for me to quit working… How do you feel about today being that day?”

We talked and talked. And talked. A lot of people have disagreements at work, should I just man up and accept it? We thought I would quit 3 years ago, should I work 1 More Year to be safer? Could we really retire this early? It’s one thing to think you can, and another thing completely to actually do it.

They say you should sleep on a big decision, although I didn’t sleep much that night.

I understood the politics, even the specific issues that brought us to this point. I even knew how I could make improvements, resulting in much stronger relationships. I would have even been a better person for it. It’s just… I had no interest in doing so. And more importantly, I didn’t have to.

The next morning I made myself a nice breakfast, rode my bike 23 miles around the lake into the office, and had a long shower. My manager was right. I was not enjoying work anymore, and it showed. I had been too aggressive in getting things done, and stepped on toes and hurt feelings. I was impatient and quick to anger.

The time had come. I went to my manager’s office, apologized for my rude behavior the previous day, and submitted my resignation.

Coffee Dates, Questions, and More Coffee Dates…

The next week was a blur, one coffee meeting after another. I didn’t know if I was high on life for finally taking the plunge, or overdosing on caffeine. Probably both. The accountants at Starbucks were certainly confused about the surge in coffee sales.

But for so many unique conversations, the questions were surprisingly similar

“You aren’t really retiring, are you? Which company are you going to? … Are they hiring?”

No, I’m definitely retiring. We really wanted to start traveling a few years ago, but I got sucked into this project at work and we just kept finding excuses.

“You must have made a killing in the stock market! What’s your secret?”

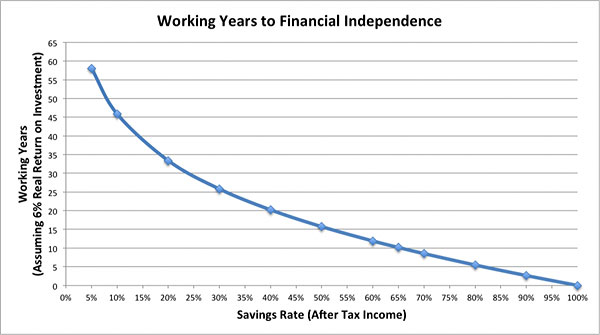

Haha, that is really funny. We “lost” about $400k in 2008 in the Great Recession, and are just now getting back to whole. We did normal stuff, contributing the maximum amount to my 401k and our HSA, and saved the rest in a Brokerage account. We primarily invest in index funds, so our performance has just tracked that of the broader market. Interestingly enough, when you save a high percentage of income, things like investment return, inflation, interest rates, and dividend yield matter a whole lot less.

Most of our financial success can just be attributed to a high savings rate.

“Isn’t there a penalty on 401k withdrawals before Age 59.5? Plus, aren’t withdrawals taxed just like income? You’ll get murdered on taxes!”

You know, US tax law is very kind to retirees, especially ones that retire young. There are several ways to get funds out of the 401k penalty free, and for many people dividends and capital gains are taxed at 0%. I’m formulating a plan to have $3 million in income over the next 30 years, and pay absolutely ZERO dollars in tax.

It’s almost like Uncle Sam wants us to retire really young.

“Wow, that is crazy! Wait, how old are you?! You are at least 10 years younger than me and I don’t think we can ever retire?!”

Well let’s see… I just turned 38 and Winnie is 5 years my junior… Retiring in your 30’s is conceptually quite simple, albeit not easy. We made improvements in our spending until we were saving 70%+ of our income, and did so for the past decade.

If you think about it, the math makes sense. Save 50% of your income, and after 1 year you have enough saved to fund a whole years’ living expenses. Saving 70% of your income, it takes only about 9 years before your investments can pay most of your cost of living. These past 2 or 3 years, our dividends and interest have paid for all of our expenses, so I’ve just been depositing my whole paycheck into our brokerage account each month.

“Wait a second, how is it even possible to save such a high percentage?! With the mortgage and car payments, we barely manage to save anything.”

Yeah, we live in a high cost of living area. We did somewhat unconventional things in order to save.

Houses around here are pretty expensive, and after doing the math we decided that renting was much better financially. Houses have a way of surprising you with expensive maintenance or upgrades. Remember when you were telling me about how much you spent on your kitchen remodel? I didn’t say anything at the time, but that remodel cost about the same as a year of rent for us.

We were very careful about where we rented. You remember our little apartment near the University when you came over for a dinner party? We are only a block from a grocery store and weekly farmer’s market, a few blocks from the library, and a short distance to a large park. We can walk everywhere, and it is right on the bus line to work although I bike most days. It’s so convenient we don’t own a car.

We’ve easily saved $100k+ over the past 10 years by riding bicycles, walking, and taking the bus. It’s also been really kind to our waistlines.

I remember how much you loved Winnie’s beef bourguignon and home baked bread. That’s our normal daily life, eating great food at home with fresh ingredients from the Farmer’s market. The local grass fed beef, free-range eggs, and organic local and seasonal produce are fantastic. I’m certain Winnie’s cooking rivals anything you can get in a restaurant, and at 1/4 the price. That’s also why I bring my lunch to work everyday.

Really, I think we lived a much more luxurious lifestyle than many of our peers, we just did so much more efficiently.

“But without a job, what will you do about health insurance? (This was pre ACA)”

I just bought a HDHP (High Deductible Health Plan) on the open market. It’s only $233 a month. But in practice, we will probably never use it and will just pay cash. Healthcare outside the US is really affordable. I went to the hospital in Taiwan once for a chest X-ray and EKG and the bill was only $50. I think that is the price of one aspirin in the US.

When the ACA becomes law, we’ll just get a similar plan on the Health Exchange if/when we return to the United States for longer periods.

“You are just going to travel around the world, doing whatever you want whenever you want?!”

Exactly! That’s the plan. We’ll start in Mexico and go wherever the mood takes us.

Unlike a typical vacation, where you jet in and stay in a nice hotel, filling every hour with high excitement activities, we intend to travel slowly, immersing ourselves in the local culture for up to a year. We want to study local language, art, and music, eat local cuisine, and become a part of the community.

Traveling in this way can cost a lot less than a typical life in the US, and even less than our own relatively low cost of living.

“Really? How much do you think you will spend in a year?

I’m not 100% sure. I did a lot of research on this, and it was hard to find good examples of people doing long-term slow travel with clear budgets. It will cost us a lot more to travel through Europe and Australia than it will through Central America and SE Asia, but I’m not sure what the total bill will be. We are starting in Mexico instead of Paris because we know it will be under our budget, which will allow us to get used to spending instead of saving.

Along the way we can make adjustments based on investment returns, and even balance time in expensive countries with time in low-cost countries to average out our costs. If next year the stock market is through the roof, maybe we will spend the year in Western Europe. If the economy isn’t as strong, we can explore South America. We can even take advantage of currency fluctuations as we decide our next destination.

Maybe I’ll share all of our expenses on a blog to make the planning process easier for others.

“No, really. Which company are you going to? Maybe I’ll go with you.”

A Few Weeks Later… (and The Start of Our Blog)

A few weeks later, we started our blog www.GoCurryCracker.com, to answer these questions and more. Some of my coworkers made a bet, guessing how long it would be before I returned to work. Now I have to keep writing or they will think I just went to another company :)

That was over 2 years ago. We’ve since been through 6 different countries, made some incredible friends, swam with whale sharks and rescued baby turtles, studied Spanish and Mandarin, guitar and flute, oil painting and jewelry making, climbed volcanoes, biked around entire countries, witnessed incredible sunrises and sunsets… and decided to have a baby!

I’ve continued to study the concept of Financial Independence and Early Retirement. You can do a lot of thinking when you have the time. I’ve hacked the US tax code and now plan to Never Pay Taxes Again, and put together a fool-proof way for anyone to Retire 20% Faster.

When we were ready to have a baby, we used our location independence to our advantage. We were able to save 80% off US prices for our IVF treatment, a great example of Medical Tourism. When our son is about 6 months old and ready to don his own little backpack, we’ll hit the road again.

I have no idea how we ever had time for jobs!

– Jeremy (and Winnie)

gocurrycracker.com

UPDATE: Jeremy and Winnie’s story just landed all over the internet starting at Forbes.com and onto the front pages of Yahoo and MSN and more… About time everyone catches on! Who’s article is better? ;)

——

PS: Looking back, the journey to financial independence was longer than it should have been, and more difficult than it needed to be. Most unfortunate of all was continuing to work in a job I no longer enjoyed out of fear; fear of change, fear of the unknown, fear of failure. Unfortunate because anybody with the fortitude to save and invest a high percentage of income for many years can overcome any problem that comes his or her way.

By the way, what was in my Retirement email that caused so much excitement in the first place?

See for yourself:

From: Go Curry Cracker <gocurrycracker@gmail.com>

Subject: for the tldr crowd. Rated R. I’m retiring

Date: October 3, 2012 at 2:16:40 PM GMT+8

To: Company – AllMy last day at work is Oct 5th. I plan to take a few months to decompress, after which I intend to do absolutely nothing.

As I began explaining my future plans to a few friends, I found that I was having the same conversation over and over again. It seems the idea of just doing nothing is a bit difficult to grasp, since it flies in the face of conventional wisdom. To save myself time answering Frequently Asked Questions, I decided to film one of these conversations to share with others.

Unhappy with the quality of the film, I hired paid actors. Playing the role of me is Samuel L. Jackson. Playing the role of you is John Travolta. Enjoy.

If you are offended by foul language and adult themes, or otherwise disinclined to participate in activities HR may disapprove of, do NOT click on this link. You have been warned.

Get blog posts automatically emailed to you!

Most of us just consider financial independence as the only ingredient to retire early. This to me is just like looking at the one aspect of retirement and hoping that everything else will fit in with enough money in wallet. Health, relationship with family and friends as well as the meaningful activities to do in retirement are important too.

In all a really nice story.

Hi Adnan,

I couldn’t agree more. I wrote a blog post called Twice as much Money won’t make us twice as Happy. Having enough enables so much opportunity to exercise/eat well/reduce stress, and spend time with friends and family and pursuing interests that you love and are passionate about.

Cheers

Jeremy

So true!

Incredible story Jeremy! Nice work! I can really identify with how you felt that last year of work; there are a lot of similarities to things I deal with every day. My wife and I are counting down our 10 remaining years to our own early retirement. Though we’re not saving 70%, we are stashing away a pretty substantial amount.

Out of curiosity, what was your target critical mass for savings? Have you ran your expenses vs savings through FIRECALC? If so, what were the results?

Hi MMD

I’ve used Firecalc. I think I like http://www.cfiresim.com better, its more flexible and easier to process the output data.

Anything above an 80% success rate I consider to be imaginary. There is no such thing as a 100% guarantee. But by any metric, we have enough. At some point we will have to figure out our endowment plan

10 years will go by in a flash. I would sometimes look at our Passive Income Milestones to help with the tough days

Cheers

Jeremy

Well done Jeremy and Winnie. Great story – it’s all about the savings rate – once you figure that out it’s a one way ticket to freedom!

Also happy to hear you are planning to keep travelling with your little one, we’ve been on the road since our son was 4 months old. He’s now 2.5 and is an intelligent, compassionate and well-spoken little dude. I’m sure at least some of that is from travel (and the rest from his fabulous genes – hehe).

Heading over to check out your blog now.

Absolutely, savings rate trumps all! For one thing, you aren’t becoming accustomed to a higher cost lifestyle. And then of course you are putting away massive piles of cash and letting compound interest do most of the work

It is super cool that you are traveling with your boy. I’ll have to check out your blog for some tips

Love this post! While I have not retired early (yet), it is something I am aiming for. The freedom it brings just seems amazing, and I know I would enjoy the financial independence :)

Great job!

The freedom is hard to describe

I have so much respect now for people that work while pregnant. It is a huge luxury for us to focus only on the pregnancy and Winnie’s needs. She is completely exhausted at times, and doesn’t sleep well at night because our little guy is practicing his kung fu all night. I can’t imagine if she also needed to juggle a career

Thanks Michelle!

Wow, great job Jeremy! I am super impressed with your story! We are currently saving about 60% of our income and hope to reach financial independence within the next decade. I always love reading the stories of those who are already there. Thanks for inspiring me today! Oh and, by the way, I love that you put a clip from Pulp Fiction in your resignation email. That is beyond awesome!!

Thanks Dee! A 60% savings rate is impressive, well done!

That clip perfectly captures many of the conversations I was having at the time :)

Can you believe I’ve never actually seen Pulp Fiction? This clip makes me want to though! :)

What?!?! Now we know how you can pass the time through the east coast snowstorm :)

Awesome story Jeremy! My story is different int that my wife and I started our own business several years ago, but felt largely the same way when I left my job. People just didn’t understand it as it was outside their accepted realm of what’s considered “normal” and can only imagine it was even more so for you. We’re not at 70%, but we’re definitely in the neighborhood of it and it gets us excited to think of what we can do by continuing down that path. Love the email, just classic!

Hi John, thanks!

I love being the weirdo on this. I still get emails from old coworkers from time to time as they start thinking about making changes. It is great to be able to point them in the right direction

Congrats on your high savings rate! That is a recipe for success

Cheers

Jeremy

Jeremy, that takes an awful lot of awesomeness to quit like that and do what you want – retire. Saving like you and Winnie did is a ton of discipline too. Kudos to you. Enjoy, enjoy, enjoy.

Hi Kim

One cool thing about saving discipline, is after awhile you don’t even notice anymore. We could spend much more than we do, but really have no idea what we would do differently that would make us any happier.

Thank you!

Jeremy

You hit the nail on the head with the savings rate. So many people focus on the next “hot” stock to quintuple so that they can turn into millionaires overnight. It’s much easier than that. Invest in tee broad market as you have done and just focus on your savings rate. That is the ultimate factor for building wealth and retiring early.

You said it

Our 10 years of saving was during a horrible economy, a stock market crash, a housing crash, record low interest rates, and a record low dividend payout. Factoring in inflation, the stock market hadn’t even returned to its high in the year 2000 by the time we retired.

Nicely done Jeremy and Winnie! Love the Retirement email and can see why it generated a bug response. I’m sure a lot of people in your office were looking for answers to that scary question.

Thanks Brian

I still get emails from coworkers, trying to figure it out. It is great to be able to help

Excellent story! Looking forward to more in this series. Congrats on the new addition to your travel plans. What an amazing life for a kiddo!

Thanks Rebecca!

GCCjr is going to be a true citizen of the world. Most likely he’ll be trilingual, Mandarin, English, and Spanish

Love it! The bringing lunches to work comment cracked me up–people are always asking us how we save 71%, and the answer is always, well, we just don’t buy very much. I love that you just quit when the moment was right. No sense in prolonging a job you weren’t enjoying. And your travel is inspiring–almost makes me want to delay the homestead in order to do the same… Congrats on living the dream!

Thanks Mrs. Frugalwoods!

Maybe we’ll come take care of the homestead while you hit the road ;) We could go for some hiking and nature time for GCCjr

Funny thing about buying stuff… I can’t think of a single thing that I would buy right now (except for maybe some cheesecake, we are noticeably low on that necessity.) We already have everything that we want, and none of those are things

So inspiring. While I’m not as big of a fan of slow traveling since we really want to be with/near family, I love the idea and your methods. The tax stuff alone is great info!

Slow travel isn’t for everybody.

Somebody commented on our blog recently about that, saying they noticed they spend more time with family now while living abroad than when they were living in the same town. People come visit for weeks at a time, and they can just be together without interruption. Back home, everybody was “too busy” to get together except on holidays

I could relate to that. My Mom and Grandma are coming for 3 weeks after the baby is born, which will be a lot of fun!

Ha ha ha, awesome! What a way to make an exit. I generated a lot of confusion when I left. “What does that mean “he’s retired?”. Keep on enjoying what you earned, bro!

I’m still trying to figure out what it means :)

Thanks Justin!

Wow what an inspiring story! I’m really happy for your family!

Thanks Tonya! GCCjr will join us in just 8 weeks or so, and then the real adventure begins

Great post! I’m definitely hopping over to your site to learn more about your journeys. Thanks!

Thanks Fervent Finance!

I like to geek out on the finances of early retirement and financial independence, so you’ll find lots of good stuff on those topics over there

Wow that’s an awesome story! I completely get Jeremy’s dilemma with corporate politics. Being political is an entire art and sometimes it can consume your job.

Some people love it and thrive on it. I would rather travel, play guitar, and write. The hours are good too

Thanks Savvy

J$ – “Early Retirement Series” — fantastic… great idea!

Re: this first article, I’m almost feeling like there is a lot he seemed to have left out… but I am happy for him and beyond impressed that he saved 71% of his income — and for 10 years straight. Holy cow. He does have great points, though, about the high costs associated with both car and home maintenance.

Last time I was at a resort in Playa del Carmen, Mexico, there was this group of early 30s folks vacationing there too, and we (husband and I) were overhearing that one of the 30s guys had retired– supposedly he had been a pharmacist, which is obviously spelled pharmaci$t. If it is true, again, just impressive! Now I have to go look at my budget and figure out how I have been going so wrong…….

Playa del Carmen is beautiful, and the cost of living is very budget friendly

We spent about 9 months in Mexico in 2013. We even almost bought a home there to use as a base

There is still so much more to tell. I should write a book :)

You definitely should. You already have an audience who’d be willing to buy it the second it comes out!

Congrats Jeremy and Winnie!!! I definitely understand the stresses of working in the corporate environment and sometimes it’s just not worth your sanity to have to deal with it day in and day out. We have my son’s college education to pay for (it’s an important goal of ours); however, after that, we are looking forward to embracing our financial freedom as well!

Thanks Shannon!

If I ever need a taste of corporate politics, I can just look on Facebook at all of my friends complaining about their jobs :)

We have been figuring out college expenses as well. Fortunately we have 19 years for compound interest to do its thing

Great post — I love finding new blogs and this one looks amazing!!

I’m still not on board the early retirement train, I just love my job and the rat race too much right now. But I DO love working towards having the option to leave whenever I want. I’m not quite there yet, but will be in the next few years. I’m 29 and my fiance is 28 and we’ll hit our first million in our 30’s, at which point “working” will just be a lucrative hobby.

Great job on your early findependence!

Hi Bridget,

Congrats! Hitting $1 million is a huge milestone

I too loved my job. Until I didn’t. It’s a very powerful thing for work to be optional

Cheers

Jeremy

You’ll enjoy his blog, Bridget. I read 150+ articles a day for Rockstar Finance and I swear I learn something new with almost every one of his blog posts. And when I’m not learning, I’m sucked into the interesting ways of thinking about stuff. (ER stuff mostly)

Thanks for posting this – It’s a total inspiration and hard shove (a nice hard shove, of course) to save, save & save some more.

I’m a HUGE fan of medical tourism as well – I recent got a boatload of healthcare done in India for less that $300 that would have more than maxed out my $6,600 deductible I have on health insurance here in the US.

I can’t wait until my investments start paying off – I already live a nomadic lifestyle, but you guys are taking it to the next level – Cheers & Congrats! :)

Isn’t the price of medical care outside the US amazing?

I paid $3 for a Doctor visit in Mexico that would have cost $200 in the US.

Winnie had some dental work done for about $20 that would have cost $300 in the US

Our IVF treatment cost about $7k and would have been closer to $35k in the US

Keep rocking the savings Chelsea! :-)

This was a great post. Wow, great story-telling, and great story to tell! My partner and I are just on the verge of launching a Mustachian-aspiring lifestyle together. This is great to have this kind of role model.

I’m really impressed too with your ability to leave “hooks” to drive traffic to your blog… I’m headed there now!

haha, thanks superbien!

Hope you love the blog!

THANK YOU, Jeremy and J$, for sharing this motivating story. I hadn’t thought of medical tourism before – sounds like it could be a smart choice in many circumstances. One thing we are doing to keep medical costs as low as possible is to eat really well, exercise and in general take care of ourselves.

Thank you Laurie!

It is really amazing the quality of care we have experienced outside the US for a fraction of the price.

I completely agree with you though, the best healthcare is preventative, taking care of yourself so you don’t need expensive drugs and procedures in the first place

Great post! I think I almost cried! Lol Rest assured, my story will be on here one day! Til then, let the savings continue!

I cried on my last day of work, no lie

The last thing I did before leaving was stop by our VP’s office. He gave me a hug and wouldn’t let go, and said “You can come back whenever you want. The door is always open”

Megan, we’ll be glad to feature you here :)

Jeremy – crying = being a man! love it.

Great Story.. If only I had this incite 20 years ago. A truly inspirational post.

Thanks Future Millionaire! It all starts with saving

Thank you J$! You asked me to dig deep, to share the whole truth, the details, the complete emotional journey. This is the most raw and unfiltered I’ve ever been, thank you for pushing and for the encouragement

I’m excited to see the new Early Retirement Series develop, and appreciate the honor of being able to go first

The number of warm and positive comments already is overwhelming. Wow! I will get back to everyone and answer any and all questions in the morning. It is already past 1 AM here. Early retirement is exhausting and I need to get some ZZZzzzzzz…….

I’m so glad you were willing to “go there!” This is definitely one of my favorite guest posts of all-time on this site… and we’ve had over a hundred.

(and you’re bastard, hahah.. “it’s exhausting”)

I was glued to this! One day…here comes my boss, gotta go!

Haha, boss alert! Cracked me up

Amazing story and a perfect case study of small decisions having a huge impact. I hope to be in the financial position to make (or not) this decision in the next 5-10 years.

Having the option is an amazing powerful place to be. I was better at my job and more impactful when I was there because I wanted to be, not because I had to be

I think I’m going to like this series! A great story, very inspirational! Life’s too short to be living in fear. Thanks for sharing your story. Genius email.

I am going to like this series too. There are so many people that have figured out their own unique way to live life on their own terms

Hey J$…

You could not have chosen a better couple with whom to launch your new series.

I’ve been a huge CCG fan for some time now. Their travel posts are inspirational and when their pen turns to financial topics, I’ve learned it’s time to sit up straighter and take notes.

Thanks Jim! More financial posts coming

After that I’m afraid it is going to be mostly baby pics haha

@Jim – you want to be next? :)

Sounds like I’ll need to be not just financially prepped, but also emotionally ready to retire. Good thing I’ve got a lot of time until then! Er…

Also, you’ve found a good purpose with your time in retirement and mapped out the tax and health care situation. Great stuff for anyone’s early retirement checklist!

It is really amazing how, when your finances are structured in the right way, that you can have incredible income levels and pay no tax

A lot of people have trouble making the leap. People even have a name for it, One More Year Syndrome

Usually a year or two later, everybody wonders what they hell they were worried about and why they didn’t quit sooner. I’m guilty of that :)

I was thrilled when I realized that this first post in the Early Retirement series was Jeremy from GoCurryCracker. His blog is one of the first I found when I started researching the whole Early Retirement thing, and I’ve been reading ever since. He was truly instrumental in convincing a natural skeptic like me that it was possible. So now we save 65% of our income, in an attempt to retire early and travel the world s-l-o-w-l-y. We have about 6 years left of an 8-year Early Retirement plan, and we can hardly wait to send our own announcement emails…

Wow, thanks Laura! Best. Compliment. Ever!

Congrats on your 65% savings rate. Impressive!

One of these days if you are in the same neighborhood, beers are on me

Love that Laurie!! 6 years is nothing compared to how long we’ve lived on Earth so far :)

Very nice and inspirational article…thanks for sharing! Over and over again, from those who have succeeded in getting out of the rat race, they attribute their success to a high saving rate. Coincidence? I highly doubt it.

We are trying to save a minimum of 50% of our income each month to save and invest. To be honest, it can sometimes be painful when you see others around you spend so freely. But with our eyes on the prize, we know that our daily sacrifices will allow us to enjoy early retirement someday. :)

AFFJ

50% is great. A high savings rate is key. You can’t control investment return, inflation, or the economy, but you can control what you spend

What a great story. Been reading GoCurryCracker for a while now and it’s always awesome to learn a thing or two about their journey.

Love that retirement announcement email. :D

Hi Tawcan!

I hope one of these days we’ll rent a house in Whistler for the winter and get in some awesome fresh tracks everyday. Maybe we’ll see you there!

Fantastic!

But maybe you should have just told the VP you wanted whoever’s toes you stepped on to be fired. Hehe. But seriously, great ‘I quit’ story.

Haha, that would have been fun :)

This was great!

I’ve read a bit from them but thus will get me clicking over more.

I’m jealous… But its not bad. I just wish I was there already. But we are working on it so I know we will get there some day. I realize that we need to hustle more and kick up the earnings a notch. So we can reach that 70% savings rate.

What really strikes me is how there are so many people who did already practice this before MMM.

Jeremy did you read someone who sparked this idea in you. What really got you rolling in that direction. That was the day you quit. When did you start laying down the foundation

People have been retiring early for decades, and I’ve learned a lot from others who have lead the way

Paul Terhorst wrote a book called Cashing in on the American Dream: How to Retire at 35. They retired in 1984

Billy and Akaisha Kaderli retired at 38 in 1991. I met them once in Chiang Mai Thailand and read their book

There has been a forum http://early-retirement.org for at least 15 years, and I used to read that from time to time

And so on…

For us, it started one day when I realized I was tired of working. Then I just started reading, trying to figure it out. I wrote a 50 page business plan that was super naive, but got me started in the right direction. I’m still trying to figure it out, although I’m better at explaining the idea today than I was even a year ago

You know you’ll have to publish that 50 page biz plan now, right? :)

One massive blog post with edits to what was bad and what you now know?

I want to… I have to find it. This was before I met Winnie, so a long time ago. I remember having really simplistic thinking of investments and the idea that if I could just get a job as a scuba instructor I could pay all of my bills.

I definitely needed to read this today. At this exact moment. Yall are awesome.

haha, thanks Cat!

I’ve never watched Pulp Fiction..but worked out that was the movie clip at the end. I love it!!! Sums it up so well.

If you haven’t seen it, rent it this week, there are some really cool other scenes ;-)

Pulp Fiction is easily one of the Top 10 movies of all time

Don’t worry, Ko – I haven’t either (*gasp*)

It is amazing to read about people saving like that, really 70%?!, at younger ages. I wish I had your mind set at that age then I could travel before 50 too.

Thank you for sharing! I too asked right away ‘how long will he last?’ just because it is ingrained in us that we have to work. All my family and friends would think this is crazy so I am so glad to hear your story.

There is a 0% chance I’ll be back in any normal job. Being a Traveler, Blogger, Student, Husband, Dad is more than a full time job

I had a recruiter emailing me every few months after I changed my job title on LinkedIn to “Beach Bum.” After awhile I emailed him back with a link to our blog, and said that while I wasn’t interested in any new opportunities at the moment, I would be happy to get on the phone with him and figure out how he could be in a position where he no longer had to send recruiting emails. He politely declined my offer, but he did stop sending me mails

Hahahhah…

YES! Brilliant!

Congrats on your retirement and living the dream. I’m really excited to read more on your blog. I wish I’d done this from the start of my career.

Thanks Kim!

The best day to start is today. We made a lot of mistakes along the way, and I did normal consumer stuff early in my career too. But once I knew it was possible all of that changed

This is just awesome. Our savings rate severely declined these past 2 years, but this is our overall plan too. Congrats!

Thanks Crystal

It isn’t always a one-way street, just keep the focus on and you’ll get there. Good luck!

Same here Crystal. For us it was losing an income and gaining two kids! Those little boogers are cute, but destroy a wallet ;)

Dude, words can’t express how awesome your story is. Dope! Certainly validates what I’m working towards.

Cheers,

Josh

Thanks Josh! It was a lot of fun to share our story too, I’m glad you liked it

I am very impressed with you Jeremy. I wish I could be like you now so that I could enjoy and travel around the world. That being said, I gotta focus on my dreams and grab my financial freedom any time soon.

Thanks Jayson,

Exactly like you say, focus on what you can control and you’ll have financial freedom before you know it. It came faster than we thought it would

I had a pretty cool job, but working ‘for myself’ is clearly 100 times better. While we’re not where you are (husband is also working on his own small business), such stories make us get more focused towards financial independence. Keep up the great work and congratulations for all you achieved.

Thank you Ramona. That’s awesome that you both have small businesses! Congrats

Well done, Jeremy! Thanks for showing us that it can be done. Enjoy your baby! What a lucky little guy to have two stay-at-home parents – not that any of you will be staying at home : )

Thanks so much Prudence! Only 8 more weeks!

That youtube video pretty much sums up any discussions with others about early retirement. That is what I have been waiting for.

Quentin Tarantino is a mad genius

Who knew he had early retirees in mind when he came up with that scene

Very inspirational, Jeremy and Winnie. And instructive. Makes early retirement very appealing! But- don’t you miss working even a little bit? Or has the feeling of “a job well done” become less important?

I’ve been asked that question many times, and honestly…. I miss two things. My friends and an excuse to go for bike ride each morning (I loved my commute, weird, right?) But other than that…. I don’t miss it AT ALL

I get way more joy out of things like J$ saying, “Your story makes me want to push harder on my own Financial Independence, would you write it up to share for a new Early Retirement Series on Budgets Are Sexy?” I did a happy dance when he said that

And almost every day I get emails from people saying that they are making changes in their investment plans, or investing more, or asking for reassurance that they really do have enough and can finally quit their job, all because they read stuff on Go Curry Cracker. There is a HUGE amount of satisfaction from that, helping real people

Everything I do now is because I want to (well, except picking my socks up off the floor, that is because my wife wants me to.) My relationship with time is completely transformed, I often don’t even know what day of the week it is. I sleep when I’m tired, create when I feel inspired, and learn when I’m interested. It is a truly amazing feeling to do whatever you want, when you want, because you can’t think of anything you would rather be doing. The level of joy is on a completely different plane. I imagine this is what childhood felt like

Well, you certainly can’t argue with a life through which you help real people. I share the same level of satisfaction in helping my clients, as well as my colleagues in the field. It would be wonderful to get that day in and day out.

In addition, the joy that you describe is something to shoot for. I know that life has its ups and downs, but I’m sure that the joy you have makes the ups feel much better than when you were working.

I do have another question for you, if you don’t mind staying on this track. What about a daily discipline for personal growth? Doing what you want when you want is ideal, but at the same time, we need to “remake” ourselves from a self-development point of you. And that involves doing the push-ups, or going for the run, or sitting down for the meditation, or whatever other “work” on ourselves we need to do. Without such a discipline, we can get mentally and physically soft, and less effective in our life’s work.

Is there a place for this in your life? Do you feel it is important?

Hi Steve

It’s an interesting question. I’ve haven’t tried to articulate my thoughts on this before

As a kid, I had maybe 5 hours a day of school, a couple hours of physical activity (sports or whatever), and about 4.5 months off per year for summer vacation, spring and winter holidays, etc…

Then at some point, it was decided that I should work 40-60 (or 80) hours a week and have 2 weeks off a year. If there is anything that stymies personal growth, I think it is this unhealthy focus on one aspect of life. The work world can consume everything

But if people have an abundance of time, without need or fear of failure, they will naturally seek opportunities for growth and self-improvement. It doesn’t need to be a daily thing, and it doesn’t always need to be forward progress.

For the past year, I’ve been studying Chinese 3 hours a day plus homework. My Stairway to Heaven guitar solo has become quite respectable. I’m easily 10x more knowledgeable about investing and taxes. I lost 17 lbs while increasing strength and biked 900 km around Taiwan.

I don’t really see it as a discipline. All of those things just happened out of the natural human desire to learn and create, and the opportunity to let it happen naturally. There is no profit motive. Some days I do nothing “productive.” Those days are equally as rewarding as the days I “accomplish” a great deal. Structure probably does as much harm as it does good

Hi Jeremy,

Thank you so much for your thoughtful reply.

I shared your frustration in having an artificial structure imposed on my life. One big reason I became self-employed many years ago was to have more control over my time. In the process, I have been able to devote myself to “higher” causes such as self development, family, and community.

Did these interests develop organically simply because I was able to cap time spent working in business? That is a very provocative question you raise. If people are free of time, needs, and fears, will they naturally seek to grow? You have certainly broadened yourself in many areas (though I would like to see you take on Alvin Lee in your next guitar solo :)

I will say this: every successful writer I know writes, writes, and then writes some more. Same with every other performing artist, martial artist, and all other creative people. You always reach a point where you just have to practice cause you have to practice, even though there are other things you would rather be doing. It has nothing to do with profit, and frankly, it really doesn’t have to do with love. It has to do with a commitment to a way of life that nourishes and sustains you.

The downtime you speak of, which is “unproductive,” is really integral to that lifestyle. It is the passivity that lies before the activity, the restfulness that is needed before the wakefulness that comes. A battery recharge.

My own experience has been that even those “off” times have to be planned and structured, otherwise they will get swept aside all too often. My life then falls out of balance.

Does this make any sense to you?

Deep thoughts by Go Curry Cracker:

How do you define successful? Is a musician successful because they have found a commercial audience for their work? Does that make them better than a talented musician that has no interest in publishing professionally? Better as defined by whom?

Like any skill, you need to practice. Agreed. But how many people start out with a loathe for writing, and then decide they want to be a famous/successful/talented writer? My guess is not many. If the interest isn’t there in the beginning, no amount of forced practice will result in success (of any type, financial or otherwise)

Certainly not every practice session is equally joyful, but the journey must certainly be or else why even start.

I can’t relate to the need to structure off time. My wife prefers to schedule things, although much less so now that she has unlimited free time. We balance each other in that way

I’ve heard some people say they worry about too much free time, because they are afraid they will devolve into a primal being that cares only about eating, sleeping, and sex. “What will you do all day?!” is a common refrain. Maybe they need a higher purpose, or a structure, sometimes imposed by an authority figure or deity. I can’t relate. Rather than idle hands being the devil’s playground, I find the opposite to be true

Back to your original question: I don’t miss work in the least, and find that unlimited unstructured free time brings out the best in me. ymmv

This is an enriching exchange, Jeremy. Thank you for your very provocative questions.

I define success the exact way you do: when I can bring out the best in me. If a commercial or business venue can help me do that, then I devote myself fully to it. If not, then I have to find another one.

It’s a really interesting point you make about the original motivation of somebody to start something. I have found that some people are fortunate enough to find they like something right off the bat. That enjoyment sustains them.

Then again people can have other interests that keep them going. I have a friend who took up martial arts because he had a stroke and ran out of insurance money to cover physical therapy. He tried kung fu to see if it would help him with his rehab. He spent a number of years falling on his face 10 times during class but he stuck with it because at least he wasn’t bedridden.

Now he really appreciates the work, and it’s not just because he’s grateful to be moving. He has learned to love “walking the martial path” for its own sake. It’s the same kind of joy in the journey you describe. Yet at the same time, he knows that if he deviates from that path even for a few days, he could suffer a setback.

Multiple interests, ranging from emotional to intellectual, can all keep us going.

With regards to the need for the structuring of time, you and I differ perhaps only in degree. Neither one of us needs an authority figure or deity to tell us what to do when. For that matter, I don’t think really anybody does.

At the same time, however, I think we are all bound by natural rhythms. The earth has cycles and our bodies and emotions are tied to them. Night and day, asleep and awake. Summer and winter, hot and cold. We each have to find our balance in the mix, and we each need more of one than the other. But we do need both. And that balance is maintained through a set pattern.

One prime example: raising a baby. Soon you will have that mind-blowing experience. Read all the literature about proper training for an infant. They thrive on a set schedule. Sleep training is especially key. As they grow, the schedule is modified to accommodate that new growth. But a schedule remains, nonetheless.

If all works out well, then they have learned how a schedule can be set and managed as needed. They run the structure – the structure doesn’t run them.

Love that there will be a new series on early retirement…it’s definitely something that I’ve been really interested the last few years. It’s also great that the Go Curry Cracker couple did it in a relatively high cost of living area. I thought that one of most significant issues with me is that I live in the NYC area and it’s very difficult to get to a 70% savings rate. We’re pretty frugal, though I’m sure there are probably some more things we can cut, but still tough. Would love to hear more details of how you guys got there. Glad you are posting much more frequently these days.

Glad you like the idea for the series. Been wanting to do one for a while and rapping with Jeremy here pushed me over the edge!

I can’t wait to read the future posts, this series is a great idea

I’ve been to NYC a few times, and found many things to be cheaper than Seattle. The farmer’s market in Union Square was much cheaper than the yuppie market’s in Seattle, food at Trader Joe’s was the same, the public transit was about the same but more convenient, and there were so many free or cheap activities. Even the Metropolitan Museum is by recommended donation (We paid $1.) NYC is flat too, so great for biking versus Seattle’s 7 hills. But housing and dining out were much more expensive.

We actually looked into moving to Manhattan for a year. Friend’s of ours were going to rent a 5 bedroom house in Alphabet City, and we would rent one of them for $1300/month. I just checked an old spreadsheet, and estimated we would spend about $1000 more per month over Seattle. Health insurance was 2x, and of course there is the ridiculous city income tax

Andrew, if you read this please send me a mail with what kind of details you are interested in

Hadn’t been over to GCC.com in a few months, so it was nice to see your story pop up here. I have Red’s “I hope” monologue from Shawshank Redemption tacked up on my credenza, and everyone around me knows I cannot wait to kiss this office and the 9-5 good-bye. Folks like you, MMM, jlcollinsnh, Early Retirement Homepage, etc. have opened my eyes the past few years to the endless possibilities. Looking forward to future posts.

Hey dude! Great movie! Zihuatanejo is a great place, and that quote is so inspiring

I’m writing up a storm these days, as it forces me to think through a lot of stuff I’m trying to figure out. I think I learn more from the comments than the other way around

Awesome story, Jeremy! I’m looking forward to following your blog from here on out :)

Thanks Ben! Yeah come check it out, we geek out on finances all day long

@J. Money love the new series, please put me down for July 2020, thank you.

@Gocurrycracker this one was really fun to read enjoy the back and forth convo, you are growing on me as people I like and read, not that it makes a difference in your world, but another reader none the less.

If blogs are still around in 2020, you’re on :)

That is only 5 years from now! Blogs will be so over by then

Thanks Steven! And thanks for linking to GCC in your own great posts

Inspiring to read your story!!!! It’s so great to see that other people have done it and know that it’s possible.

Hi Christine, glad you liked it! I’m excited to read other people’s stories in this series too

So where in the world are you currently calling home?

Great story!

Looking forward to following your blog.

Thanks for starting this series J Money. Looking forward to future stories in the series.

Cheers!

We are in Taipei right now

http://www.gocurrycracker.com/where-in-the-world/

Hard to say where is next, Thailand and Spain are the places we are talking about most

Wow, great job Jeremy! Your story really inspired me, as of now, I’m saving every penny that I have.

That’s how you get there, one penny at a time

Very inspiring post Jeremy. I often wonder if I’m the only employee in my organization focused on retiring early and not simply putting in time in order to qualify for a full pension. Best of luck to you and your growing family as you enjoy the fruits of your hard work!

Thanks James. I was definitely the minority in my org too. Lots of interest from people after the fact but not enough to make change for many

I can see the appeal of the pension, but never had the option

Great Job! I am not that far away from retirement, but will not be in my 30s. On the other hand, I should be able to spend more, not less…

Right on, sounds like you have a solid plan in place. Being able to increase spending over time is definitely a good thing

Wow! What a story. I still dream of quitting my current job to work for myself, but even better would be to “retire” fully instead and only “work” whenever I want to… Now to get rid of my debt so I can get going on my dreams.

Thanks for sharing your story Jeremy. Sounds like a high savings rate is the key to it all. Right now student loan debt is my enemy, so when they’re paid off in a few years I can just invest it right away and supercharge my savings rate.

In the post you mention that your dividends and interest cover your living expenses. I get the dividends part but where do you get interest payments from? Is it CD’s, savings accounts or something else?

Keep up the great work and have fun with the little guy on the way. Boys are the best, trust me.

Thanks Syed,

We might go for a daughter later. When we started the IVF process, we were secretly hoping for one of each

Student loans are a pain, but hopefully they come with a better job and higher income. It took me 5 years to pay off mine. If I had $1.19 in my bank account at the end of the month, I paid an extra $1.19 to the loan

My loans were 7-8% though. My brother’s loans were <2%, and I recommended he never pay them off… just pay the minimum and let inflation destroy the debt

At the same time, I was contributing enough to the 401k to get the employer match. A 15-25% tax savings, employer match, and tax-deferred savings were enough incentive to get me to prolong the student loan payoff

Our interest is primarily from a seller financed mortgage from a failed real estate investment. As soon as that balloons out, I'll put that money into stock

Cheers

Jeremy

Soo basically

1. make lots of money

2. Save lots of money

3. move to a cheaper area

I don’t know why I didn’t just write it that way in the first place :)

There are a lot of comments so all I’m going to say is- I love your story and I hope it gets people to think about how to change their own situation. Rock on.

Great story! I often fantasize about resigning. I dislike my job but like the money it makes me, and I think I’ll be so much happier if I was able to just quit. Unfortunately we are not there quite yet, and even if I quit, I’d have to find some other job to do or buy some businesses. Early retirement with enough passive income is still far away.

It’s good you’re starting to think about it now though :) I’m only in year 2 of really paying attention and figuring it out, so I imagine in a few more we’ll both be much more aligned to hit a nice target date!

Wow, such an inspirational post. I’m myself targeting a retirement in my 30’s, but I feel it’s still a long road. We’re definitely not saving 70% yet, but trying to aim for above 50%.

I would say just the fact you’re planning on retiring in your 30’s puts you well into “kick-ass” territory :) Once you get on a mission the rest seems to fall in place when you try hard enough.

Jeremy (and Winnie)

Thank you for this. I’m siting on a plane for a business trip and sent this to my girlfriend and thinking about how I could follow in you and Winnie’s footsteps and all that you’ve described is so within our grasp. We just have to have the balls to take it!!! Thank you for the inspiration.

Fondly,

Bruce Hsiao

3/31/2015

Bruce, you just made my day

This is why we blog! Awesome! You can do it

Hey love the post! Just curious, you said “You know, US tax law is very kind to retirees, especially ones that retire young. There are several ways to get funds out of the 401k penalty free, and for many people dividends and capital gains are taxed at 0%. I’m formulating a plan to have $3 million in income over the next 30 years, and pay absolutely ZERO dollars in tax.” Do you have a post that goes into this more in depth?

Here you go :)

http://www.gocurrycracker.com/never-pay-taxes-again/

http://www.gocurrycracker.com/go-curry-cracker-2014-taxes/

Good info. I am 38 and we are on track for me to quit working a regular job this year, but I will continue with some extras I enjoy like fixing up furniture and reselling it. My husband is 32 and he will be able to retire at 40, the year our younger daughter graduates high school. We plan on buying an RV and travelling after that.

I laughed a little at your comment that you went to the hospital for a chest x ray and ekg and it cost you $50. I did the same thing here a couple months ago, I have great health insurance, and my portion was $879. That was after my health insurance paid 80%.

This is sweet! Way to go out and live your dream! My wife and I are both 26, and we now live in Granada, Spain. You can live in Western Europe without paying an arm and a leg. (Just stay away from Paris!) We live so much cheaper here than we did in the US. Our phone plan are 10€ a month each. We pay 400€/month for a 2 bedroom apartment. We eat healthier because fruits and vegetables are so much cheaper. Just bought 15 kiwis for 1.50€. I live so much more relaxed just being part of the culture. It’s not out of reach!

That’s awesome!

I’m trying to do the same thing at gettingtoonemillion.blogspot.com

Go for it. I retired at 56, some years ago, and knowing what I now know, (isn’t hindsight wonderful?), I could easily have gone at 46, but definitely not in my 30”s. So, well done you! Based in the UK, as retirees, my partner and I spend 1 or 2 months in a different European city each year, along with 1 or 2 long hauls to Caribbean, US, Asia, Australia, NZ each year. Even given a series of very poor years, it will take us at least 20 years to munch through our investments, excluding our house. So I can just say, living within your means, investing, and taking one or two ‘opportunities’, is the recipe for a successful post-work life! By the time I run out of money I will be about 95 at earliest, so probably not a huge worry!!

Beautiful!

You know, US tax law is very kind to retirees, especially ones that retire young. There are several ways to get funds out of the 401k penalty free, and for many people dividends and capital gains are taxed at 0%. I’m formulating a plan to have $3 million in income over the next 30 years, and pay absolutely ZERO dollars in tax.

It’s almost like Uncle Sam wants us to retire really young.

Can you explain this part? I thought you had to retire at 59 1/2 or 10% penalty.

Thanks!

Here you go:

http://www.gocurrycracker.com/never-pay-taxes-again/

Great post from him back in the day that explains a lot of it :)

Hi Jeremy… Congrats! Amazing story! If you’re willing to say…. when you retired at ages 38 and 33 how much total did you have put away at that point? You mentioned you were expecting $3MM in income over the next 30 years, so I’m guessing you had socked away about $1.5MM?