[As part of our weekly column by Mr. 1500 of 1500Days.com – a fellow blogger who retired at 43!]

******

Life is good in retirement. I’m thrilled to have a net worth of $1,900,000 which enables me to live my life on my own terms. Instead of answering to Mr. Bossman, I wake up and do whatever I want.

On some days, I’ll ride 40 miles into the mountains. On others, I’ll spend hours at the library. Money is a wonderful facilitator. Sometimes, the money even enables questionable purchases like fancy cars and human kites. But I digress…

If I could give you one piece of advice, it would be this:

Never stop learning.

Once you become stuck in your ways, you become an intellectual deadbeat. Don’t do it.

I have enough money so that I no longer have to pay attention to it, but I’ll never stop learning. I discover things about money every week that surprise me and make me a better saver/investor.

Today, I’ll share some of my favorite money hacks with you. I’ll also be sharing questionable underwear choices. Don’t worry, it will all make sense. (Or worry, because there are pictures!)

Money Hack #1: Writing every transaction down

Until recently, I never kept track of my spending. A couple of years ago, I started recording every dollar that went in and out. To state that I was shocked by my spending is an understatement.

Having to answer to a spreadsheet is a powerful behavioral changer. I suggest at least partially automating the tracking which brings me to my next tip:

Money Hack #2: Using a spreadsheet to track your spending

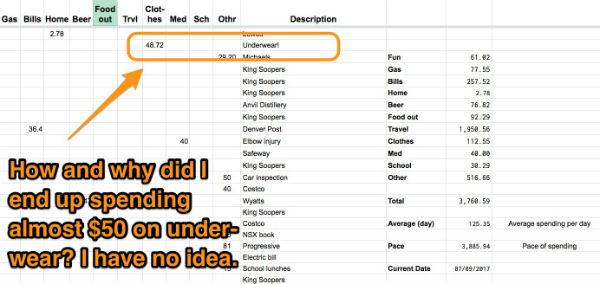

I created a spreadsheet on Google Drive which adds up my spending as I go. Here is my real spreadsheet from April where I blew a load of money on underwear and travel:

If you don’t like the hassle of a manual spreadsheet, you can also use software like Mint or Personal Capital to track your dollars.

And what do I hear? You want to see what $50 underwear look like? No, I probably shouldn’t… You really want to see? OK, brace yourselves sensitive readers. It was a 3-pack:

Money Hack #3: Loving Credit Cards

I wade into dangerous territory here. Credit cards are like nukes. Use them responsibly and they do wonderful things. Use them carelessly and:

BOOM!

People ask me questions like this all of the time:

How much should I sacrifice when I’m saving for financial independence? Should I skip vacations?

You don’t have to sacrifice anything. Here is proof:

What does that have to do with anything?

I took that picture on the Eastern Coast of Kauai where I traveled with my family of four. We woke up every morning at dawn to watch the sunrise and frolic in the surf. We’d hike and snorkel in the afternoon. At night, we ate dinner on our patio, listening to the waves roll in.

In case I’m not painting the picture correctly:

It was one of the best weeks of our lives!

And the best part? All four airline tickets set us back less than $200. We were able to do this using credit card points.

Now, travel hacking is a voluminous subject. If you’re not learned in the ways of travel hacking, check out the Travel Miles 101 course (free and great!) or J’s one-on-one interview with Brad. And if you need a card, you may want to check out Mad Fientist’s credit card tool.

But wait! Before you even consider any of this, you must raise your right hand and repeat after me:

I will use credit cards responsibly! I will never, ever carry a balance!

Don’t let credit cards nuke your finances. Do let them take you to Hawaii.

Money Hack #4: Never thinking of purchases in terms of *present* value

Nothing drives me crazier than when I hear someone say this:

My new car is only $25,000.

It isn’t $25,000. Money invested in the markets typically takes less than 10 years to double. Unless you’re close to death, big ticket purchases can set you back hundreds of thousands over the long term. Think long term to fully appreciate the impact of all purchases.

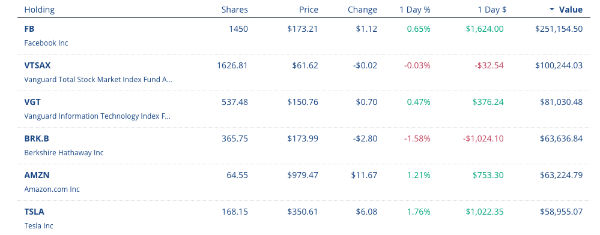

Money Hack #5: Using Personal Capital

Life is complicated, and so are your finances. Between my 401(k), savings, checking and investments accounts, I have my money in about 3,384 different places. At least it feels that way.

This problem is easily remedied with a Personal Capital account. Personal Capital aggregates all of your accounts into one place. Here is a screen capture from my own Personal Capital dashboard (it’s OK to look, no underwear pics this time):

Best of all, Personal Capital is free. Who doesn’t like free?

Money Hack #6: Studying computers

This one actually came from my grandmother three decades ago. She knew computers were going to be a “thing” and would say this to me every time I saw her:

Study computers!

My grandmother was crazy in a lot of ways, but this was some of the best advice I ever received. There are loads of unfilled computer jobs. And you don’t have to go back to college for a degree. There are boot-camps all over the United States where you can spend under a year studying and come out with a good job. Many will even refund your money if you can’t get a job.

I did this myself – dropping out of pharmacy school to attend an accelerated program. 30 weeks later, I had a great job and never looked back.

And if you’re still unsure about why you should study computers, consider how many folks in the financial independence community had jobs in high tech. Mr. Money Mustache, Mad Fientist, Go Curry Cracker!, ThinkSaveRetire…

What hacks do you have for us?

I’ve barely scratched the surface here. I’d love to hear about some of your favorite financial hacks? What makes you clamp down on your spending? What tools do you use to grow your wealth?

Hit us in the comments so we can all learn more.

*****

[Bikosaurus painting up top by my awesome artist friend, Madalyn.]

Get blog posts automatically emailed to you!

“Never spend less than $5”

Before I started tracking my spending, I was constantly left with that feeling of “where did all of my money go” at the end of the month. After a month or two of writing down every transaction, I quickly realized how much I was spending on the little things that somehow would always add up to a large amount of money. Furthermore, those purchases were adding almost nothing to my life in terms of happiness.

By stopping myself from spending less than $5 on any transaction, it eliminated the slow bleeding of my budget. It also forced me to be more conscious of how I spent my money and to plan for replacing those small purchases. Things like making my own tea in the morning or packing my own lunch did wonders for my savings.

Good tip here and above! I think writing things down and being acutely aware of what you’re spending your money on is key. I would often log into my account and wonder where my money was going because I thought I’d done a good job limiting spending to see it gone to smaller purchases as you’ve stated.

I also try to think about the dollar value I’m spending today and what it would be worth in 10, 20, 30 years if I didn’t spend it. That often times deters me from spending.

Fascinating! $5.00 would def. kill off a looooooot of random purchases, you’re right. I’d like to think I could do that, but I’m just not sure (as I sit here drinking a starbucks coffee, haha…)

Lol get the biggest cup available

That is so simple! But I can see how it would save sooooo much money. I can’t even count how many times in a month, I stop for a quick snack or drink or fill-in-the-blank. But it is usually something under five bucks. THIS is genius! And I am so stealing it!

For me it’s picture what you value, does whatever your buying fit that bucket. Can I picture myself still needing it six months after marketing newness wears off? Or am I going to be longing for the next big thing while it languishes in a corner or a closet or a garage. If the answer is the latter then I have no business buying it.

Writing down transactions and tracking…yes!!! Those were both huge for us! We are very interested in credit card hacking, but haven’t stepped out on that one yet. And I’m loving the advice from crazy grandma!

A huge thing for us has been monthly budget meetings, so we can both understand where we are financially. I don’t love to sit and talk deep into finances like my husband, so this is our way of doing that and keeping on the same page.

Another thing was when we instituted fun budgets. We’ve saved money! Which seems odd, but we know we only get xx amount of money for hobbies, eating out, etc. so we budget it well. Plus, we can both feel better because we don’t have to pop the other persons bubble when we tell them something isn’t in the budget.

“but we know we only get xx amount of money for hobbies, eating out, etc. so we budget it well.” Yes!!! That’s not weird at all that you’re saving cuz of it – you brain can easily sparse the info needed to determine what to spend and what not to – it’s brilliant!

My favorite hacks have been automating my saving and investing (before any $$ even hits my checking account!) and trying to have “no spend” days to cut back on frivolous or impulse buys. The more mindful I am, the more I realize I can get by without the extra purchases, especially for silly things that sound good in the moment!

Automating! Now that’s one I can get behind!

Hi Mr1500,

Great post as usual. I agree with you about studying computers. Mr99to1percent is a programmer and companies/clients & recruiters chase after him 24/7.

Regarding your underwear, if Mrs1500 is not complaining, then you are good

Give up booze, junk food, and cigarettes. It sounds like such a bore but honestly, I’ve never felt, richer, hotter, and more sorted in all my adult life!

I think if people can even just cut ONE of those they’ll be more happy all around :) (i score a 1.5’ish. I don’t smoke, but I do drink one or two beers a week and partake in a little junk food as well..)

Wait, what? No Flamin’ Hot Cheetos!???

Love you’re grandmother’s advice about studying computers. The sad thing about great advice is that it’s rarely acted upon. Kudos for being coachable. I’ve found that’s been a key success factor for my own FI journey.

As far as hacks go, I love investing small chunks of money I would’ve otherwise blown on something i wanted in the moment. For example, I love going out to eat. So, whenever I get the urge, I force myself to eat at home and give myself a financial reward by transferring what I would’ve spent dining out into my investment account. So far it’s worked like a charm!

Mrs. Mad Money Monster

Beautiful idea :)

Thanks so much for the tip. I struggle mightily with eating out. I like the idea of immediately transferring money not spent to savings (right now, adoption fees.)

These are great hacks! We use credit cards too! I like that I can get cash rewards for the things I would buy anyway. It also helps us keep track of our purchases. Mr. FAF and I don’t really have a detailed budget, so we rely on our credit cards to us how much money we spend each month.

I just started documenting our food expenses after I started blogging. It really helps us keep track of how much we spend on food!

I love this list and can get on board with all of these items. I’ll add one more to it. You need to have Goals! To me it’s much easier to save if you are saving for something. Saving for financial independance or even a vacation will get me to cut spending way quicker than saving just because.

This is random, but your icon there totally looks like a Pabst Blue Ribbon logo :)

I would love to hear more about these boot camps and where they can be found. I’m ready to make a career change.

Hit up the Google! I searched a bit and there doesn’t seem to be one central directory.

Another tip: Take an introductory programming class or do an online tutorial to make sure you’ll enjoy the job.

I don’t do many money hacks, I just do the ordinary things very welll and have a very disciplined money mindset. The most important thing that I prioritize is to pay myself first.

For every pay period I just contribute to my retirement account to get my employer matching and pay less taxes at the end of the year. When I get my tax refund (in the five figures) I invest all of it to generate more income sources.

After 10 years or so, this becomes second nature to me and I never made any sacrifices as I never had access to the money from the very beginning. These actions took very little effort. It just takes discipline.

Scary, but I’ve used every one of your hacks. We’d always used “Forced Scarcity” to save (divert savings first, live on the rest), and I never tracked our spending. As we approach retirement, we decided to track every penny for a year to make our retirement cash flow as accurate as possible. It was very interesting to see what we were spending $ on, and we made some structural improvements as a result (Good bye, insurance company. Your prices suck!).

Great post, I’m enjoying having you hang out with J$ every week.

Nice advice Mr. 1500!

You could say I studied computers – I have a Masters in CompSci. That knowledge was definitely one of the things that helped us FIRE:)

I use and love Mint and I don’t use Personal Capital. I know lots of people love Personal Capital and I need to look at it further. But I’ve also spent lots of times reducing the number of accounts that we have. I still have a ways to go. :)

Simplicity Is Sexy.com!!

What is at sexy.com? I’m afraid to click over… But tempted… I’m in a public area and other people are around… Must. Resist. Can’t. AHHHHHHH!!!!!!!!

Haha… the joke was SimplicityIsSexy.com :) Which I doubt works, but you never know?

(Damn – Now I gotta go click on it and see!)

Yessssss. Viewing expenses from the perspective of my Future Self has been really helpful. It helps me get out of the “gimme this NOW” mindset to prevent impulse purchases. I’d also add that I did a cash-only envelope system for a while and it helped as well. That was back when I had zero self-control and had to learn about needs vs. wants the hard way.

I disagree with #6. Pharmacists do very well. An average pharmacist probably is better off than an average computer geek. I’m sure you would have done well as a pharmacist.

I’m onboard with the rest. :)

Oh yeah, pharmacists do very well. However, computers are a lot more interesting than pills and there are a lot more jobs. Also, you can learn programming in less than half a year where pharmacy takes years of school.

The other thing is that pharmacist pay is capped, but a really good programmer can me more than $400,000/year in the valley. Hell, there are some billionaire programmers (Jeff Dean).

Oh oh #4! Best hack ever if you have the moolah and organization. Then it’s like free money!! It’s no chump change, we were credit card hacking for a year and it added up to at least $2,000 in gift cards, miles and cash back.

Dang it Lily, I mean #3. But #4 is my second favorite :)

Great article! One hack I use is: Before going into any decision, whether it’s financially related or eating healthier, if you could just consider what is just one small way I could improve this decision, you’ll end up saving more money. Many times, the decision will simply be that you don’t need it at all. This is a strategy I used to start eating healthier. If instead of getting a burger and fries, you get a burger and side salad, you still get to indulge a bit but have made the meal healthier. Over time, it will compound, and you’ll end up getting grilled chix and a salad. Finance is the same way. I’ll be writing a post on this very topic within the week!

I couldn’t wait – so here is the post “iPhone X vs Your Future Self” – https://retirementviewpoints.com/iphone-x-vs-future-self/

HAH! Awesome – love the idea. And even more so how fast you can pump out an article like that?? It takes me 4-5 hours to do it and their half the size! :)

We travel hacked our way out here to Longmont to do some great learning (and hang out with some awesome folks) using credit card points and our Southwest Companion Pass. And like you, we’ve NEVER tracked our spending. Our frugal habits got us to FIRE without even realizing it! BUT – we are tracking our expenses on this trip to Colorado and it’s making me crazy! I’m just doing it in a notebook – so I need a better plan :) But it is very clear that eating out is the place where your budget goes right out the window. For two of us – to have a burger, beer, and a tip (and that’s just one beer – which is hard to do in these great craft breweries!!) – it’s always about $40. We rarely eat out at home – so it is crazy to think about how much people spend on eating out! And even crazier to think of if you have kids. Eating out 3 or 4 times a week can add up to a good part of a mortgage payment!

If you figured out how to retire early you have full permission to never track a thing again :)

The only hack that worked for us is if we didn’t see the money at all. Automated or taking a lower salary (by intention) meant that we didn’t see enough in our checking account. I noticed that whenever balances are high, my Amazon bill tends to go up. The other hacks – like writing or using a spreadsheet worked only in the short term. I’d invariably go back to my “old ways”. Did I mention I was lazy?

When I was four or five years old I had a hack for saving my allowance. I would get my allowance in coins and I would scatter the coins in my underwear drawer then mix everything up. Whenever I wanted to buy something I would go searching through my underwear drawer. Finding the coins would take some doing (and I never knew if not finding any meant that they were all gone or I just hadn’t looked hard enough). As a result, how much I searched depended on how badly I wanted whatever I was thinking of buying. If I couldn’t find enough money I would toss it all back and mix it up again. This not only made saving (sort of) automatic but it also helped me set my priorities.

I’ve been trying to figure out something similar to do as an adult but so far haven’t really found anything (of course, as an adult I have somewhat better impulse control than I did as a kid). One thing I thought about was getting some gambling software and using discretionary funds to create the bank. If I want something frivolous, I’d have to win enough money to purchase it. Sounds like a foolproof way to save. :)

HAH! I love BOTH of these ideas haha…. so clever and fun at the same time :)

In fact, i did something similar w/ the latter one there – I gave myself $20 to start playing poker with friends, and I was only allowed to play with the money I earned from that point forward. After a few months I had about $100 in reserves at any given point in time, and of course some times I’d be up a lot and others down. But it all started with that one $20 so it was free entertainment!

Reward credit cards FTW! My wife’s entire family is on the West Coast, which can be pricey when we live on the East Coast. We have easily saved thousands of dollars just in traveling to see the family by using credit card rewards. And that’s not even including money saved on vacations. This allowed us to increase our student loan payments and investment contributions throughout the years. So who knows how much money credit card rewards actually made us.

Nice chonies! Never underestimate the power of good undies. Sometimes you gotta fork over the cash in exchange for maximum comfort! Lol!

I love love your philosophy on credit cards! Once all my credit card debt is 100% paid in full, I plan to use a travel rewards card responsibly for exactly the reason you do.

My own money hack is a pretty simple one but it works for me every time. I am currently on a journey to become debt free so when I get tempted with an impulse purchase I stop for a moment and ask myself a simple question: “Is what I want NOW more important than what I want MOST?” If the answer is no (which most of the time it is) I walk away from the purchase. Simple and easy, and it helps bring my goals back into perspective during that time of weakness!

Is what I want NOW more important than what I want MOST?”

Whoah, nice way to put it!

Tracking savings was key for us. When we first started getting frugal, we started with trying to reduce our monthly credit card spend. It got paid off every month, and we were investing on top of our 401k’s so NBD right? Except that by tracking that spending and asking ourselves if it is a “want or a need” we eventually trimmed off ~$2k/mo from our credit card frivolous spending…

It was embarassing how much we were just frittering away on this and that and stuff that made no positive impact on our lives. That was literally another $24k we were able to invest each year simply by being more mindful of our spending.

That and we implement “allowances” so that way we can splurge on ourselves, use it for hobbies, clothes, restaurants out, or whatever and not tap into our overall general funds for those purchases. That has worked well for us.

Tracking spending was our key though. It’s shameful how easy it is to needlessy waste so much money each month and not realize it…

Can I go back in time and drop out of medical school to study computers? Seems like a good plan.

Personal hack…maybe pay yourself butnalso treat yourself. Good to save save and save but don’t deprive completey. You never know what tomorrow brings.

Can I go back in time and drop out of medical school to study computers?

Hmmm, I’ll bet cardiologists make pretty good money!

Great blog post! I completely agree with #1. During our first year of marriage, my husband didn’t believe how much we were spending on coffee and drinks at the bars with friends until I showed him an Excel spreadsheet of every transaction for the month. We didn’t give up the socializing, but he cut out 90% of the coffee expenses by brewing a cup before going to work.

Funny that you dropped out of pharmacy school. My mom wanted me to leave IT consulting (100% travel and/or working 6 – 7 days a week because of crazy deadlines) to follow my dad’s footsteps to go to pharmacy school. Ten years of IT, I left and started my own financial coaching business.

One of my money hacks that I’d love to share – Track your net worth, excluding your home. I started doing this over seven years ago and have been amazed at how much we’ve been able to accumulate once we started shifting our mindset to net worth versus salary.

When I have my financial coaching clients calculate their net worth for the first time, many are shocked…and often discouraged when they realize that despite the six figure salaries, that they have a negative net worth! Depending on their personal drive, many of these clients end up kicking it up a notch and get rid of debt fast, seeing drastic improvements in their net worth.

YESS!!!

That was the first thing I did w/ my clients too, right after asking what they REALLY truly wanted in life. It’s amazing what you learn about them after going down each account with them and tallying it all up. Oftentimes what they *say* they want and what their *numbers* point to them wanting are two drastically different things, haha… I always told them the numbers never lie so no more fooling yourself! ;)

You can add me to the list of bloggers in high technology! Most of these “hacks” are focused around tracking your spending. This is important for people starting out learning about personal finance. However, once you’re experienced it starts to become a waste of time. If you optimize along the way you don’t have to track later. Tip 7: Optimize Spending Along the Way

Haha yup… I’ve stopped tracking all my pennies for years now myself once I finally “got” it. I probably spend more than I should cuz i’m not 100% lazer focused, but it’s a fine trade off so long as you’re conscious of it and everything’s trending up :)

One of my favorite hacks is signing up for the checking and savings bonus you can get when opening new accounts, my wife and I will earn somewhere between 3-4 grand just on these bonuses this year! And the nice thing about most of them is that it is not a one time bonus, most allow you get the bonus again if the account has been closed 12 months.

The 2nd one is the travel cards, I got into it big time about 4-5 years ago and have made and redeemed millions of points and miles. We have been on 5 continents and over 25 countries the past 3-4 years. Flying international business and first class flights that cost tens of thousands of dollars for almost nothing. This one can take some work and you have to be very disciplined to take advantage of it but the rewards are out-sized, I only wish I learned about this 5 or ten years earlier!! ( and no, I don’t do any flying for my job, all the miles and point were from CC signups and spending).

Love your site, keep up the good work!!

$3,00-$4,000 #KillingIt

A load of malarkey. Anyone who knows the bank bonus game quickly runs into Chex System rejections. You can make decent bonus for first year, but quickly get rejected once your Chex file fills up.

And you’re probably not “saving” any money with your FF points – most tend to rationalize that the money they “save” not buying those first and business seats can then be used to spend on other items (lile nicer hotels and extras).

My fav money hack was simply to work. If you’re working, don’t have time to spend money.

“My fav money hack was simply to work. If you’re working, don’t have time to spend money.”

That pretty much sums up my last 10 years starting this blog, haha…. Anyone who says it’s passive income is lying to you. You’d not only be lucky to earn ANY income, but it can easily take 40+ hours a week and you still don’t get everything done. But you’re right on the money with how much it SAVES not being out on the town or shopping on all your free time! Much more productive :)

Opening a business has been great for me. Legitimate tax write-offs have been helpful as I build it up. Later on, it will be helpful that I can access a SEP IRA and throw a ton in, if I make a ton.

That’s awesome. I love entrepreneurship.

And forget the SEP IRA. A solo 401(k) is superior (allows you to put much more money away) and easy to set up. Let me know if you need any help.

This is great advice! I did LOL at the three-pack of men’s underwear for $50… that’s a single women’s bra if you buy one of sufficient quality that it’ll actually fit right! But the point is well-made. And I can’t wait to check out the travel hacks recommended here – that’s something I haven’t figured out yet and would love to!

J Money’s Monthly/Net Worth Excell sheet is the BEST! I’ve used it over 1 year and have seen my net worth climb at a shocking rate. Once you actually pay attention to your money, you can control it. My own hack it to use a “MAIN” checking account as an In-Box. From the main, I transfer a fixed amount into my 2nd account when I’m paid (Bi-weekly). This 2nd account is used for food, clothing, and incidentals. I’m also much less worried about this account getting hacked since my important bills are paid from the Main account. When the deposit is gone, it’s gone….no more $$$ until the next payday! Forced rationing! My wife and I find this works well. The mortgage, Utilities, and Car expenses like Gas and maintenance all come from the main as they are pretty much predictable expenses (No car payments). Also use Capital One and have $$$ sent by direct deposit each check for forced savings. One of these is my Auto replacement account which gets $200 per WEEK (Over $10K yr)…..NEVER borrow $$$ to buy a car !!!! As far as credit cards go, we only use Debit cards…..research shows you spent 15-18% more when using a credit card. I’ll keep the 15% and buy my own airline tickets. My debit cards don’t send me monthly bills to pay ;-)….and that my friends is a good thing.

So glad you’re finding the spreadsheet helpful!! I like the “forced rationing” method too :)

My hack- when I finished paying for something, like a car loan or my mortgage, I added that amount to retirement saving or some other goal. I was able to retire at 56. When I was done with daycare, I put that money into 529 plan. My kids were able to “borrow” from me to pay for college.

Oh man, those daycare costs probably shaved off 10 years of working for you! haha… Those are no joke (and I’m sooooo glad to be done with one kid already!!! Just one more to go – woooo!!!!)

I love that there is a category on your list for Beer….

Ha ha, that category was an eye opener…

Nice money hacks, and nice underwear!

That brings up a great money hack — don’t wear underwear and save yourself the $50. As this is ‘budgets are sexy’ I think it’s fine to say that’s a pretty sexy money hack.

I can get down with that :)

You are an idiot! Buying nice cars (and kites) will leave you with little money in a few years. 1.9 million dollars is really not that much money and will not last a lifetime. Your advice is hopeful at best. My advice to you, go back to work and save more money.

I challenge you to ask anyone off the streets if $1.9 million “is not that much money” and see what you get back ;)

I’m happy to say I already use all 6 of these hacks! This may just be me splitting hairs, but I do wonder (constantly) about the value of using travel credit cards vs. high-reward cards like Fidelity and Citi Double Cash, both of which return an immediate 2% cash back, no questions asked, no complicated math required. Reason being:

– travel companies are notorious for masking the value of a point

– prices (flights especially!) change constantly and are subject to the whims of demand/fuel costs/distance for when and where you go

– points can devalue over time depending on inflation

– to actually realize the savings from flight/hotel points, you’re required to travel somewhere and spend other money on food, rental cars/taxis, entertainment, etc

Were you able to calculate what % savings the travel rewards actually got you (signup bonuses included), and/or do you think just getting 2% cash back on every single purchase you make is at least a competitive (if not better) option? Thanks!

I started using YNAB and while it’s been a short while, I actually find it’s helping curb my spending as I work toward paying bills with last months money

Also, budgeting only with my money I actually have vs what I’m anticipating getting. This means budgeting 2-3 times a month but it’s working for me. I’ve been hyper aware of sticking to my budget

“Also, budgeting only with my money I actually have vs what I’m anticipating getting.”

That would solve a loooooot of people a loooooot of stress if others did that same thing in this country. Good work!

I’ve been using Mint for almost 10 years (used Manilla for 2 years before that) and Personal Capital for over 3 years. It’s amazing how just keeping tabs on all of your accounts can help the net worth go up and up!

I’m a big fan of the Anti-budget that Paula Pant talks about. Save your desired percentage off the top and don’t fret so much about where the rest gets spent. If I spend $200 on groceries or $200 on restaurants, who cares? It was allocated to be spent anyway! I also find that I still have a desire to save some money anyway, so that gets tossed into my taxable brokerage (VTSAX baby!)

Agreed. But better *after* you first track it for a while and figure out where all your money is currently going, as chances are it’s not where you think it is :) Then after you wrap your head around that, start the ol’ anti-budget now that you’re cognizant of everything.

Really funny post!

How do you do that number 1. (writing every spending down) Its quite hard.

I love the advice – never stop learning.

Thanks

What are some good online courses to take in terms of studying computers?

I’m also a big advocate of using credit cards. Some sign-up bonuses are huge and some rewards programs make it hard to pass up using a credit card to pay for everything. As long as you don’t pay interest, I see no problem with it!

Curious on what accelerated computer course you took for 30 weeks?

If you’re a coffee-lover:

Instead of Starbucks, Panera or whatever, buy the best possible coffee (ours is the bulk stuff, when on sale at Sprouts), then get a coffeemaker you can program to start automatically in the morning. (Get a grind-before-brewing option…you’ll taste the difference.)

No more wasting money on the black stuff in a cup these places sell.

I do like the automated idea – it’s much better than an annoying alarm clock! Haha…