Hey guys!

Hope you had a nice and warm holiday weekend! :)

Thought you might like some more goodness to digest today, so let the festivities continue as we serve up a tasty platter of other peoples’ finances!

Featured in this round are: a single 32 y/o woman from Arizona, a pair of high earner engineers out in Baltimore/DC, a team of lower income SINKs with a disabled spouse, a 40 y/o lesbian couple with two dogs and a cat, a recently married couple in the Chicago area, and a separated 40 y/o whose ex turned her onto this blog ;) At least he did something right!

No kids in the mix today strangely enough, but the theme here is pretty evident: tracking your money makes your money go up, and not tracking it makes it go down… or at least to places you have no idea about BECAUSE YOU’RE NOT TRACKING IT!

So good job to everyone who knows where their money is sleeping right now, and I hope these snapshots below hits you in all the right places.

Thanks to everyone who shot these over!

*******

Single 32 y/o Woman in Arizona

Some background:

Hey J-Money!

Background on me: I am a single, 32 year-old woman living in Arizona. Debt-free outside of my mortgage.

I have been following the blog for exactly three years now! I thought I should share my net worth snapshot for all of the other voyeurs like myself who are interested in FI.

I came across FI and your blog in a random post from an old co-worker on Facebook. The post was actually about an Elite Daily article that had come out about how if millennials are saving money in their 20s, they are doing it wrong. The article says young people should be out networking, traveling, etc. My friend had a major eye-roll moment about this story (she happens to be a Journalist), so she shared her dissent and within the comments section, others brought up this blog.

I started reading your blog, MMM and Afford Anything from all of the suggestions and immediately wondered my own net worth. I was 29, had just moved to Arizona and bought a house. I went back and tracked three months of expenses and almost threw up when I saw I was spending over $1,000 a month on food and alcohol.

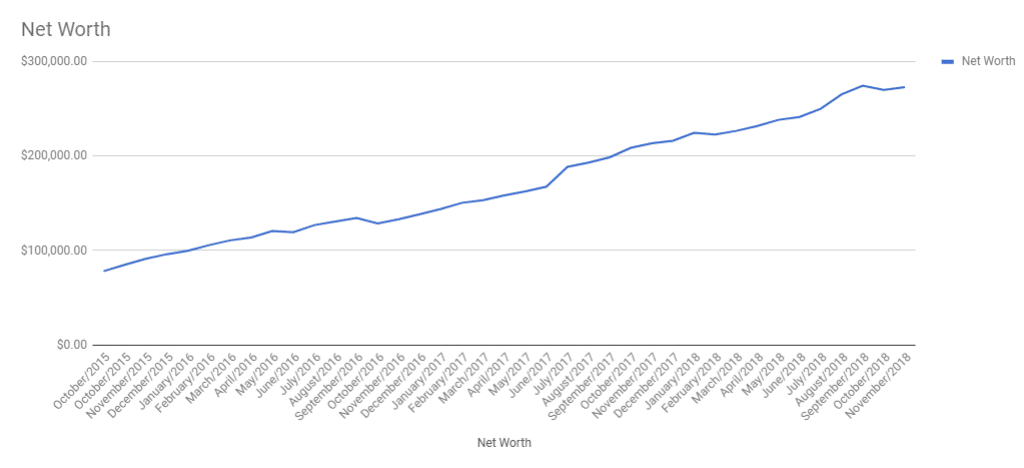

My net worth in October of 2015 was $78,084.60. I had sold my home in Vegas, paid off my car, no student loads or credit card loans, but I was spending so much money on food (that I hardly remembered) seemed like a giant waste.

I started budgeting, but still trying to live a life of enjoyment. I now spend my money on prioritizing the things that bring me real happiness like travel, spending time with friends and family, and renovating my home. I’ve cut waaaaay back on my expenses but have still managed to travel to Hawaii, Jamaica, Mexico, Seattle, Boise, and many more short trips in the three years since I started tracking.

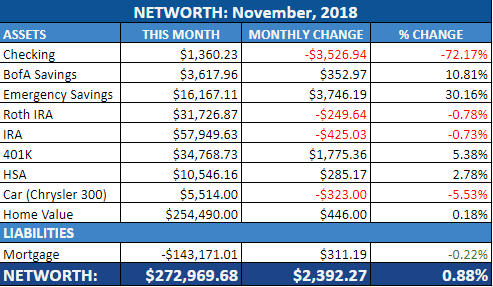

Today, three years later, my net worth is $272,969.68.

I have maxed out my 401k, Roth IRA and HSA every year since 2015. I track my net worth every month (I stole your template, thanks!). I also started asking for raises and changed jobs when I couldn’t take “no” for an answer anymore. In 2015, my salary was $62,000 and today I am at $120,000.

Keep up the great work!

Did you catch that last part??? She doubled her salary in three years! Killer!!

We tend to talk a lot more about frugality and all the ways you can save here, but there’s something to be said about focusing your energies on the *income* side of things even more. And it’s not always about taking on additional Side Hustles either – it’s possible you’ll get more bang for your buck by just concentrating better on your current 9-5! And keeping your nights and weekends in the process!

*******

Lower Income SINKs with Disabled Spouse

More background:

- 31 years old

- SINK (Single Income, No Kids) with disabled spouse

- Tracking net worth since Dec 2016

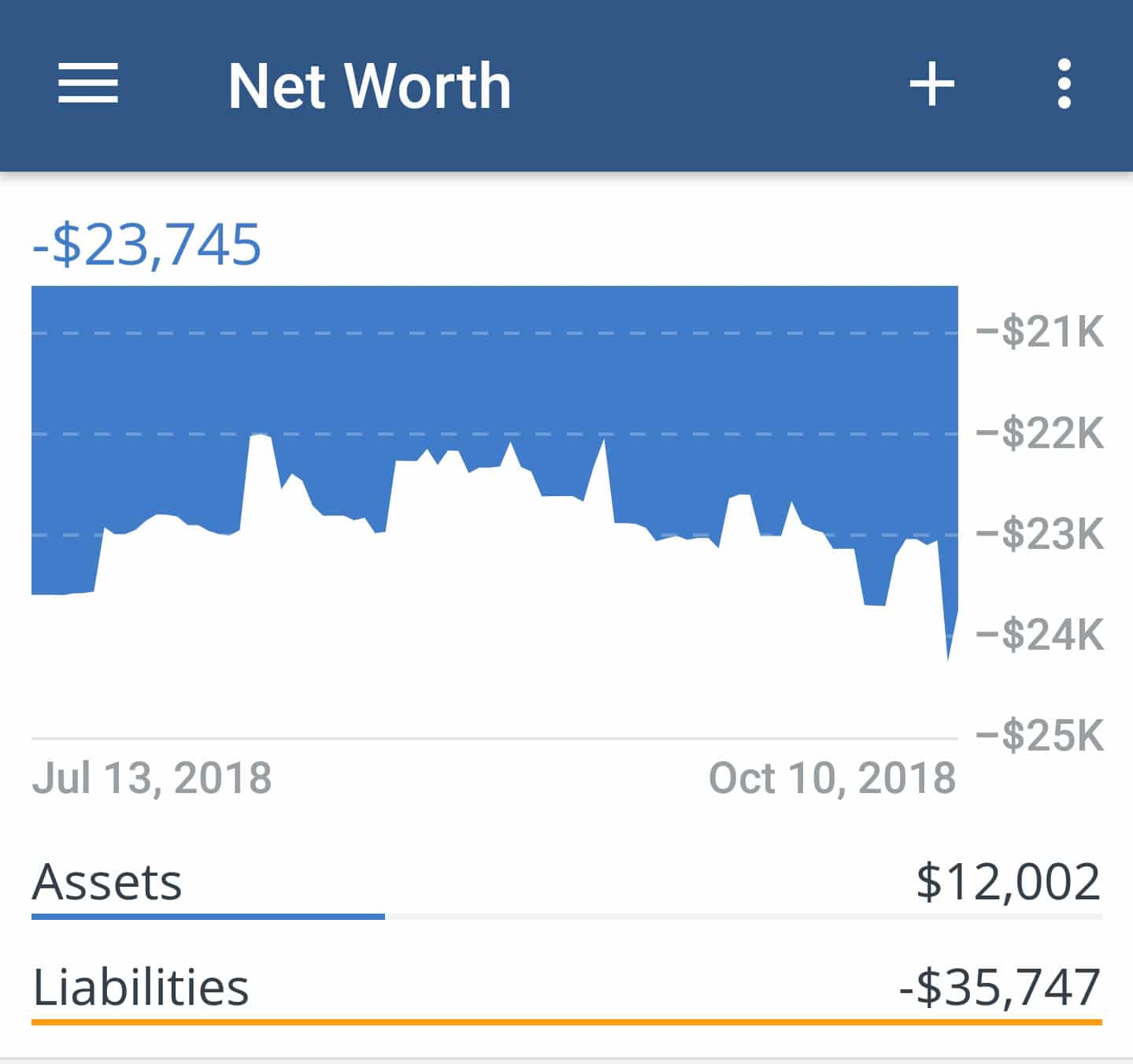

- Started at -$43,531

- Now at $-23,684

- Never made more than $40k per year (gross or net)

- Strong supporter of low income FIRE

I love this snapshot so much because it’s a reminder that you don’t *need* to make gobs of money to make progress in your finances, even though we just saw that it of course amplifies it.

These guys are paying off $10,000 of debt/year which is beautiful in itself, but even more so is the fact they’re only living off of $30,000 a year – in TOTAL! And we all know what that means – the less you need to live, the less you need to hit financial freedom.

Using the popular 25x rule, this couple will need $750,000 to reach FIRE, whereas someone like me who spends a little over double that every year will need closer to $1,750,000. That’s a difference of $1,000,000! Pretty powerful to think about.

*******

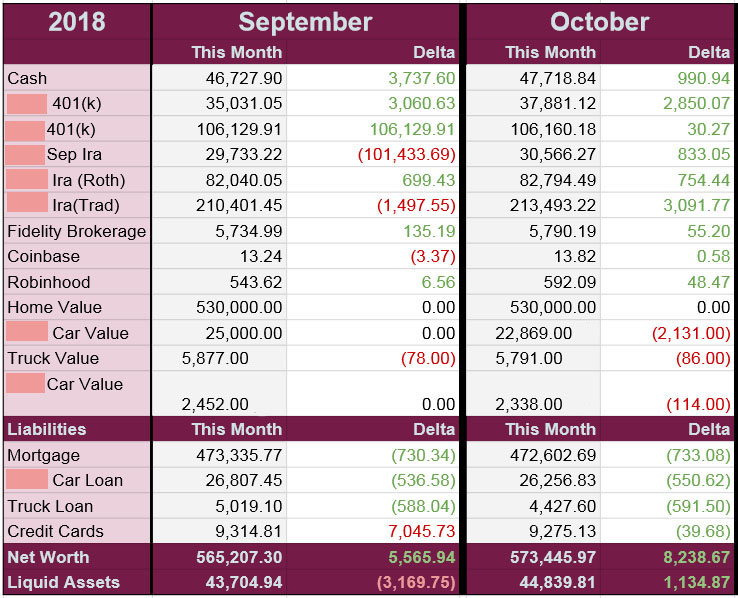

40 y/o Lesbian Couple in Texas

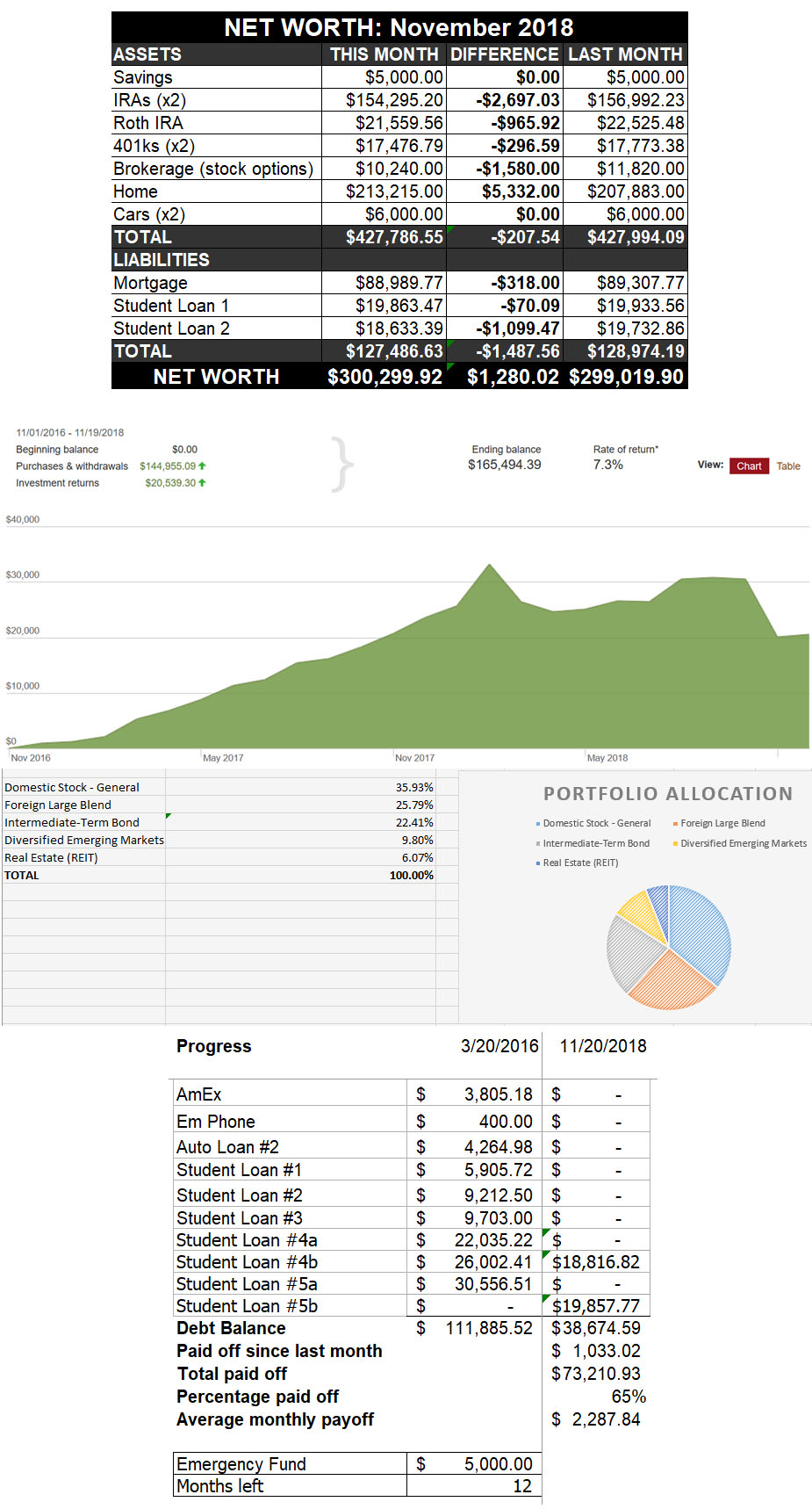

So many graphs, love it!! Especially that last one tracking their debt journey so far… Look at that 2nd column there showcasing where they’re now at with it all – pretty amazing!

Here’s more on their background:

Hello J Money!

I love your blog and the emails – we can’t wait until you hit a million and are rooting for you! It gives us hope to peek at what you were up to (via your net worth snapshots) when your net worth matched where we are now (roughly $300k). You are also one of our major inspirations for starting our very own blog (Big Girl Bucks) over the last month.

My wife and I are working to pay off our student loans and working towards FIRE. Here are some facts about us:

- 40 and 37 year old couple, married in 2014

- We live in Texas with two dogs and a cat

- Our occupations are Content Analyst and Massage Therapist

- Current household income is $120k

- We have a mortgage of $89k @ 3.5%

- In March 2016 we were staring at over $111k in debt: student loans ($103k), car ($4.2k), credit card ($3.8k) – the student loans were for two undergrad degrees (one each) and an MBA and were crippling. We’re now down down to $38k.

- We took Financial Peace University for the second time (first time was in 2010) and this time it lit a fire under our butts to pay off the debt!

- We found the Bogleheads before we found the FIRE movement, and are very appreciative of the advice and suggestions those fine people provided when we were setting our initial asset allocation, etc.

- Since we started budgeting, monitoring our net worth, and cranking away on our debt, our net worth has doubled!

- We are still looking for side hustles that fit just right and so far have tried: driving for Uber/Lyft, delivering late luggage from the airport, cleaning out our house and selling things, building cornhole sets, donating blood plasma

*Our investment performance is lagging the VTSAX, I have allocations to VBTLX, VEMAX and VTIAX. I may reallocate but am trying not to make a rash decision as a result of markets being down. The brokerage is where I’m tracking vested stock options and that thing swings all over the place!

Sentence of the year right here –> “Since we started budgeting, monitoring our net worth, and cranking away on our debt, our net worth has doubled!” #BOOM.

And as you can see, it wasn’t a straightforward journey either… They had to take Financial Peace University *TWICE* for it to finally sink in!! And did you catch that mortgage of theirs @ only $89,000?? They’re getting that debt-killing down, haha…

*******

Separated 40 y/o with No Kids (or Debt)

Back story:

I just want to tell you how much I LOVE your site, tips and looking at Other People’s Money – so insightful to see how other people think about it and learn/see if I am doing well or need to improve. My ex who is a finance wizard turned me on to you as you make things so much easier and simpler for those of who just don’t get finance.

I wanted to share my money picture as I am pretty proud of what I have accomplished. I started tracking my net worth in 2009 and I was worth $10,000. I was HORRIBLE with money. Almost 10 years later I am worth almost $500,000. Comparing to friends who make WAY more than me – I have more saved for retirement than 80% of them. I come from a lower-middle class family and never thought I would make more than $50K a year in my life. I make more money than both my parents who have worked for 40+ years.

More about me:

- Turn 40 in Jan

- No kids

- Make decent money – but by no means rolling in green stuff

- Left my long term partner of 14 years with nothing (leaving behind a stake in a $1MM home)

- Have no debt

- Don’t own a home now – but will in the future once I am settled after the separation

“I make more money than both my parents who have worked for 40+ years” – I bet her parents are so proud of her too! That’s all we can hope for our kids, right? That they are better off than we are? And how bad do you wish you knew what she did now? Haha… Totally should have asked, my bad…

*******

Recently Married Couple in Chi Town

Background on the happy couple:

- My wife is 29, I am 27

- We have been married 1.5 years and we do not yet have any kids

- She is an actress and I am in sales training for a home appliance manufacturer

- We rent a 2 bed 1 bath apartment in Chicago, IL

- I think the Listen Money Matters podcast and website was my first exposure to all things personal finance

- I now use Personal Capital, YNAB and my own personal finance spreadsheet in Excel.

Whereas last month I thought the couple who had a million accounts was overly complicated, this one I can understand more because they’re all separated out *savings* accounts! And sometimes seeing your funds nice and clear like that is super motivating :) (And probably feels easier to spend too, knowing that it’s been allocated and doesn’t affect the other goals? Like that plump Emergency Fund up there?)

I’m always reminded of the guest post we had here where Chenell talked about why having only *one* savings account can be bad… I personally prefer the simplicity, but she brings up some excellent points: 6 Reasons Having One Savings Account Can Be Bad

*******

High Earner Engineers in The Baltimore/DC Area

I’ve saved the whopper for last :)

Hey J. Money! I love seeing the snapshots of other people’s finances! I thought I’d share what I’ve been tracking for the past 5 years!

My husband and I are engineers in our mid-thirties living and working in the Baltimore/DC metro area. I make $150k writing software and he makes $120k designing fire safety systems for large construction projects. We haven’t been able to have kids yet, but that just lets us continue saving and living the cushy life. We have 3 crazy dogs that make our lives the best kind of chaotic.

We’ve never really budgeted, but we pay ourselves into savings first. We pay off our cc balance monthly. We’ve only accrued interest once in 2 years of combined finances, and that was due to an oversight on our part, not a failing in our financial habits.

2016 was when we joined finances, sold my old townhouse, and bought a rancher in a good neighborhood, with the hope of having kids and the knowledge that I have bad knees and would benefit from single story living. While the cost of living here is expensive, I’m able to pull an incredible salary and benefits that are geographically tied to this area. 100% family coverage of medical, 6+% matching, 100% coverage for STD/LTD, 30 days off a year (that we’re encouraged to take), company equity, and I never need to exceed a 40 hour week.

2016 is also where we “froze” our lifestyle. We decided that we were able to afford a very comfortable lifestyle where we never felt deprived and every raise and bonus has gone either straight to savings or to DIY home improvements that add more value to our house than they cost while also making us prouder of our home. I don’t have an algorithm for how regularly to update our home value, so I have a *super* conservative value in the chart and just leave it be. I think we could realistically sell it for $30k more than I have listed but real estate markets feel too fake for me to want to update my spreadsheet and see a giant jump. We bought it for 500k, so not doing too bad in that department.

We do know that if we needed to cut back we could easily do so in many areas, but we are happy with our current savings rate and enjoy the conveniences and time that hiring a lawn service and such grant us.

I sort of track our separate net-worths and then track my lifetime earnings thanks to the social security website. I’m at ~30% lifetime savings right now, which I’m hoping to start to see go up going forward with how much we have in retirement accounts and our increased savings.

My husband and a partner are buying his company owner out in the new year, otherwise a large chunk of our savings would have been sitting in our brokerage account. We have $10k in laddered CDs as an emergency fund (only lose interest if we cash out early) and we keep 3 months of expenses in our Bills checking account so that even if we lost an income, we would have time to readjust our finances before that account would be in any amount of risk. This is probably more conservative than we need to be given our job security in the region, but we run our finances by the rule of “the more conservative partner wins.”

We both max out our respective retirement plans yearly and our income is too high to contribute to a Roth IRA. I’m still young, so I’m choosing to contribute 100% into a Roth 401k. My husband doesn’t get that option at his work.

In addition to tracking my spreadsheet monthly, I log onto personal capital almost daily to keep an eye on our daily spending and keep an eye out for fraudulent activity.

Total current monthly expenses: $6,236 (overpaying both vehicles with loans on them)

I don’t know how long they’ve been making this money, but damn! $270,000 total/year is impressive! And leads me to believe it’s only been a few years since they’re only spending $6,000 of it a month which leaves a looooot of room for wealth growing. That’s pretty much the same amount we spend every month, only with half the income, haha… Am I allowed to blame my kids on that, or no?! ;)

They’re gonna be sitting pretty when/if they end up having kids though for sure. Which is really the whole point of paying attention to all this money stuff, right? To have the ability to make big moves in life without having to be slaves to money? It’s a beautiful thing for those of us fortunate enough to achieve it.

*******

So that’s today’s sneak peeks! Thanks to everyone who got financially naked for us!

If you love this stuff and itching to share your own numbers, just pass me a note and we will gladly showcase you in our next round :)

Hope this helped!

![]()

******

PS: For past articles in this series:

Round III: Featuring a 33 y/o with 3 kids all under the age of 3, a breadwinning pharmacist mom, a 43 y/o half-a-millionairess, a married couple with a million-and-a-half, and a pair of 60+ year old GDINKs (Gay, Dual Income No Kids) living out in the San Francisco area.

Round II: Featuring a Hebrew software engineer, a traveling ICU Registered Nurse, a millionaire who doesn’t feel like a millionaire, and a 64 year old real estate investor who used to be homeless and penniless just 18 years ago, and is now a budding millionaire herself!

Round I: Featuring a newbie financial advisor, a risk taker who loves to gamble in bitcoin and poker, the budget of my wife circa 1995 (hah!), and a woman from Kyrgyzstan who only needs $808/mo to live off!

Get blog posts automatically emailed to you!

Oooh gay and lesbian net worth stories are the most interesting profiles to me personally. Low income/Barista FI is interesting too. Everyone’s doing great on their own terms. Thanks for sharing such an array of diversity as always J❤️❤️❤️

Haha glad you’re liking!!

How the heck did you get those hearts to show up here?? Pretty cool!

//100% family coverage of medical…//

And I spent the weekend helping my adult kids get healthcare.gov quotes so I can kick them off my company “provided” insurance that was going to go up $6000 next year minimum if I didn’t do something different. I’m still going to be paying $1350 a month, which is a platinum PPO plan that weirdly works out cheapest for us on an annual basis by about $4000. Health insurance makes absolutely no sense.

Ugh, yeah… I do NOT miss those days at all…. It was fine when it was just one or two of us, but you start bringing in all the kids and it gets crazy, fast! I think we were up to the $900/mo range until we moved to my wife’s plan when she went back to work… So glad she likes 9-5s or else I’d be right there with you still :)

Maryland passed a reinsurance program last year which, while it did not make the cost go down significantly, it did prevent a 33% rise. that being said, a silver level HSA is still a shade over $1400 / month (for a family of 6) . You best believe I’m getting everything checked out in 2019…

“Health insurance makes absolutely no sense”. Too right you are. Is it possible to have an intelligent conversation about single payer health care? Unlikely in the USA.

17.9% of the GDP goes to health care in the USA. It’s 11.3% in Canada, 9.8% in the UK, and 9.7% on average in 15 other EU countries. And does the USA have measurably better health outcomes than those other countries? No. It, of course, may be possible that one’s discrete health care outcome may be better than those in single payer systems. But as a matter of public policy there is no questions what is better for society.

Suggest a single payer and people will name call: “socialist”, “liberal”, etc. No, an intelligent conversation isn’t possible. In the meanwhile the American public will continue to be fleeced by the medical/insurance industry. I have no dog in this fight: I’m not an American, and I’m not part of the industry. Just an observer.

I agree with the single payer sentiment. In fact I sat last year out of the marketplace and went with a commonly suggested (in the FI arena) health share. The issue I have is there is consistently 4- 6 months between the bill submission and reimbursement and I still don’t fully trust them to pay for anything significant. Long story short, there are no good choices. I’m switching back primarily out of fear and the guilt I would feel if one of my kids had to suffer because I decided to save money on this.

I firmly believe that healthcare is a basic human right and I also think single payer is the best way to go. The greed of these healthcare corporations should not go unchecked. Additionally, from purely an expense perspective, there is no way I would be taxed annually as much as I pay in premium + deductible.

I don’t know enough to debate on either side, but I will agree that the system’s jacked. And the ones most affected are always the less fortunate ones :(

Great charts and letters. Everyone is improving their finances. That’s the way it should be.

Nice job!

It was all on the up and up, wasn’t it? Maybe next time some people who are struggling more will share with us so we can make it more balanced :)

Nice profiles. May adjust my spreadsheet to reflects more detail. Like the debt tracking aspect of Texas couple. Being retired and feeling a bit stressed over my finances trying to focus on debt elimination and side hustles as not trying to go back to working a 6 – to whenever I felt like I could leave and have accomplished enough.

The debt paying/side hustling combo is definitely a good one :) You can always print out those charts and pictures where you *color them in* every time you pay off/earn a certain amount too. That seems like a fun way to track stuff and stay motivated!

https://budgetsaresexy.com/great-way-pay-off-debt/

Hope to be at the type of comfort level the last couple is in when we get to our mid 30s. :)

J, chrome keeps telling me you aren’t secure. Https coming soon?

Not sure why that’s happening, I’m sorry :( I’ve considered moving to https a couple times in the past, but every time I talk with people it seems to have more potential cons than goods. But at some point I’ll probably have to do it, just trying to prolong :(

Great spread of success stories. Inspiring stuff.

“Budgets are sexy”. “Getting financially naked”. Your website’s not safe for work damnit :)

I know, haha… spam filters love it too!

Did not think things through when I started it 10 years ago :)

I hate health insurance costs. I also feel like the whole system is broken. Why do we wait until we are sick to go to the doctor then they give us pills to “fix” the symptom, not the cause. It makes no sense to me. So frustrating!

I love seeing other peoples’ finances. My best friend is very open about theirs and I love it!

What a cool best friend!!! You guys can have so many more in-depth convos in life due to that – awesome!

Man, these features are so interesting! I’m almost mad I didn’t think of this type of post myself haha ;) I don’t know what it is about being nosey and seeing real numbers from real people’s finances is so intriguing to me… Anyways, great content as always and I’m excited to see what’s next!

You should copy it man! This stuff needs to be spread around more! :) Incredible you’re only 17 too and already interested in $$$ and blogging (just checked out your site). You’re gonna be sitting pretty by the time you’re an old man like me!

Thanks man, I think I might just have to haha. I’ll send it over when it’s published!

Deal.

I suppose the next set of profiles will see a blip in their net worths due to the stock market pullback/correction. It’ll be interesting to read those when the market is not coming up roses.

And we’ll gladly post those up too :)

Just as we did mine when I took a blood bath last month!

https://budgetsaresexy.com/red-wedding-net-worth-report-842k-down-60k/

Love the low income FI profile. My husband, baby, and I live off one modest income and while our FI path looks a lot different than dual-income professionals, we are still slowly but surely kicking butt (if I may say so myself). Like you mention, the FI principles are amplified with a higher income, but still work wonders at every income level. Love your blog!

Keep on kicking butt!! We are cheering you on! :)