[Oh do I have a good story for you guys today!! I hope you like long-form posts, because my man Ryland from TheHiddenGreen.com stops by the blog today to pour his heart out to us… Amazing how much your life can change when you find something that *clicks*! And shockingly, it wasn’t a budget that did it for him ;) Take it away, Ryland!]

********

I was 23 and crying.

I had just graduated college after working my tail off.

I had received $100k in scholarships to pay for school, founded a nonprofit while there and won numerous awards for my work.

I thought I had done everything right.

But I missed one piece of the puzzle – my finances. And there I was, in my black 2007 Nissan Xterra, with tears in my eyes because of it.

This is where my financial life started, and I owe it all to a little journaling.

Here’s the story of how I went from broke to over $100,000 in my accounts and completely changing my life in the process.

Zilch Financial Knowledge and $7k of Debt

In 2007 I had just walked out of an accounting office.

I had been told I owed almost $7,000 in taxes – of which $7,000 I did not have, nor with any income to pay it back.

That $7k may sound small to some, but I can tell you it’s enough to make you drop your head in your hands and wonder how the hell you got there.

It’s enough to feel scared.

I’ve always been someone who worked hard and tried to do the right things, but I’ve also always been someone (maybe behind the scenes) who struggled with money.

Let me give you one example.

In college I was up to get an award for my work and needed a suit. So I went to Nordstrom and tried on the $200, the $500 and the $800 suits.

Which did I get?

The $1,271 suit.

And at that moment it was hitting me…

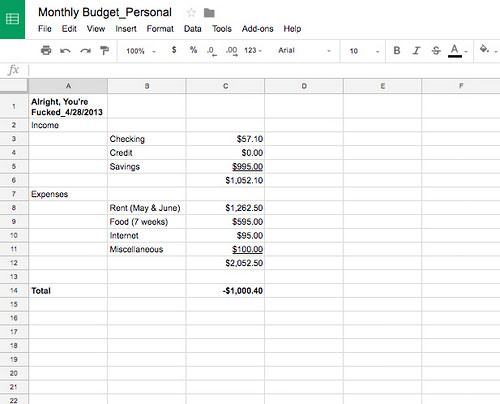

I sat there with tears rolling down my cheeks trying to figure out how I could pay it off.

When I got home I pulled up a Google Sheet (this exact one here) and gave my first petty attempt at building a budget.

(Sorry, J. Money. I guess I’m just into other things…)

After a few hours of thinking it through, I decided to sell my car, most of my surfboards, as well as my professional trumpet to pay it off.

That sucked.

But it forced me into an uncomfortable place and brought about self-motivation to create a better life for myself.

Stop Budgeting, Start Journaling

About a month later I got my first job.

It was one of those jobs at a company that makes your mom proud.

Here look. She even took this picture of me on “Ryland’s first day of work.”

To be honest, I was excited about it too, but I knew from day one that it wasn’t going to be my end-all-be-all.

I wanted to have more time to work on the things I was passionate about. I wanted to take a few trips a year without breaking the bank. And I wanted to make enough money to live a fun, yet simple life.

I remember thinking, “Is that really too much to ask for?”

No way.

But the biggest thing holding me back at that time was my money situation.

I didn’t know how to make it work for me.

I tried budgeting and that (obviously) didn’t work. I tried putting cash in categorized envelopes, but that didn’t work either.

Everything I tried just wasn’t for me.

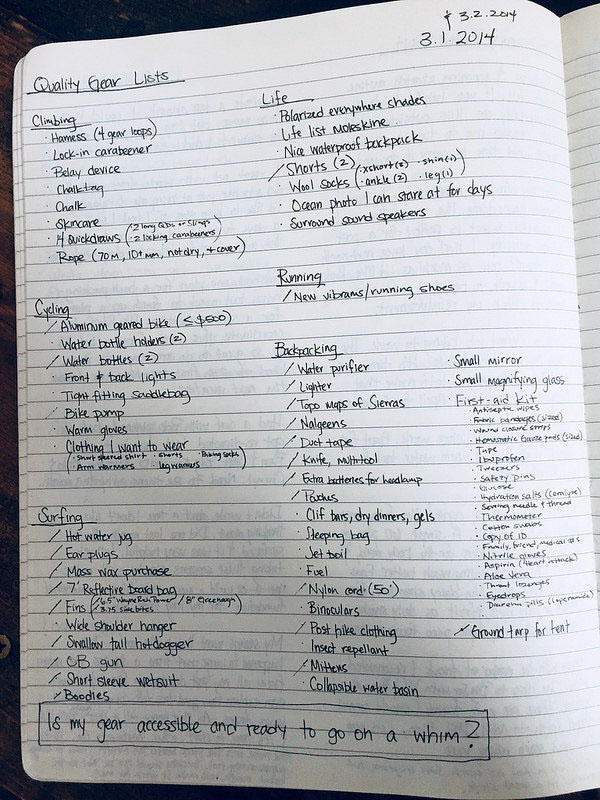

But what was for me was writing lists.

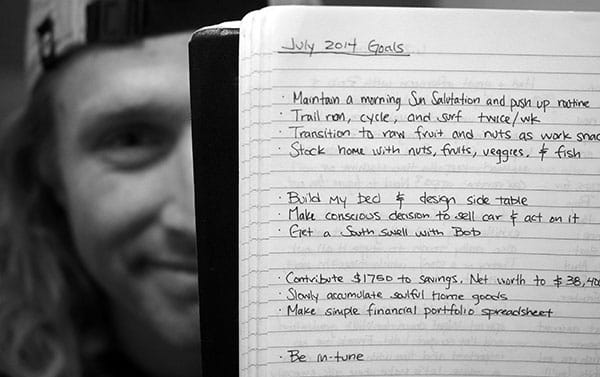

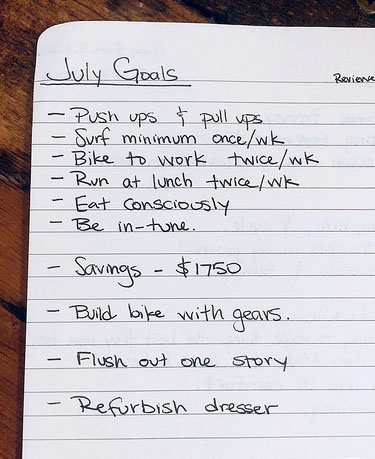

I wrote one almost every day. I still do. Here’s my list right now.

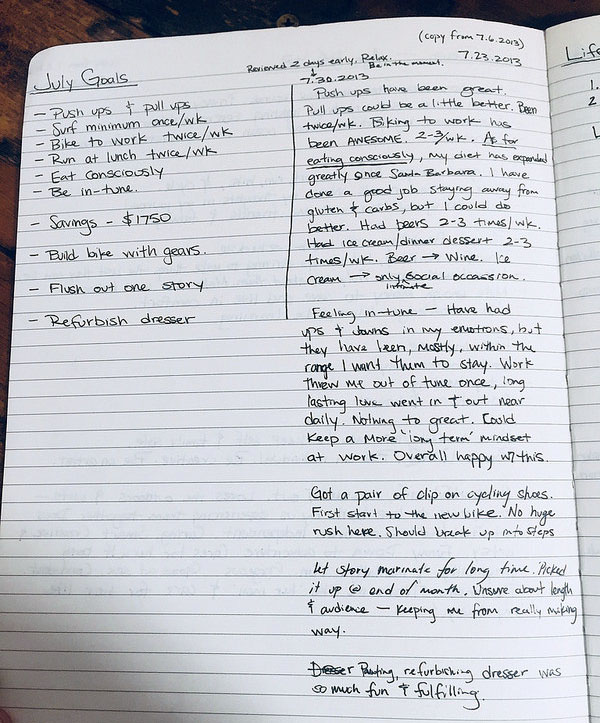

So back then, while stuck in my hard place, I decided to write a list.

I wrote out a few lines in my journal of what I wanted to accomplish just for that month.

Here’s exactly what it looked like:

A few weeks after, something interesting started to happen.

I noticed myself going back to look at the list every few days. In it I’d see the things that deep down I wanted to accomplish, and almost subconsciously my mind would refocus on how to bring them to fruition.

It was so helpful that at the end of that month I wanted to do it again.

But when my fingertips began writing the next list, my mind kept looking back at the old one.

I had unfinished business.

The old list was calling for an honest reflection, and so that’s what I did.

But that didn’t matter. The only thing that mattered was continuing to write – continuing to bring the life I wanted into reality.

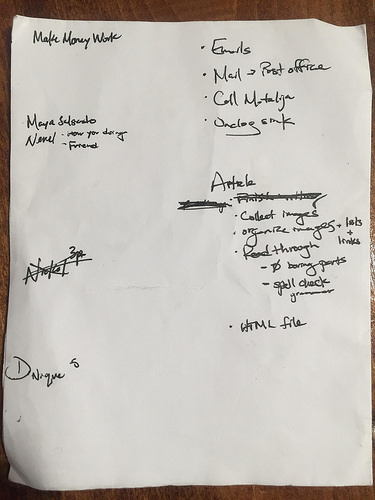

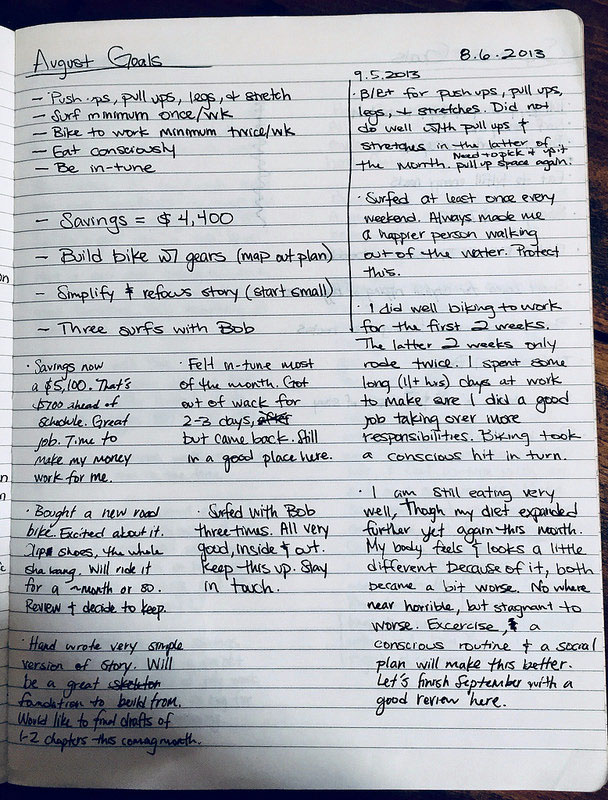

So I wrote next month’s list and at the end of that month, I wrote about how I did.

Here’s a look at that one too:

This is my life. It doesn’t fit perfectly inside anyone else’s lines.

My goal became one thing: Write.

Every. Damn. Month.

And that’s what I did.

I wrote down things like “eating only nuts, fruits, veggies and fish,” and other things like “doing push ups, pulls ups and stretching” each morning.

Along with those things I wrote down how to make money work.

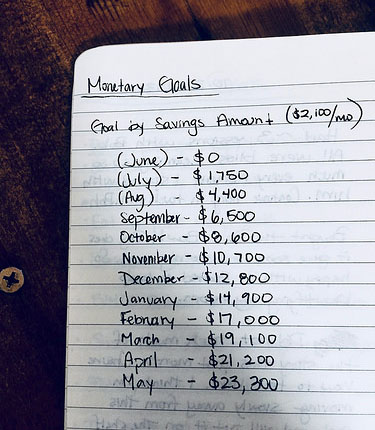

I wrote out where I wanted my savings account balance to be at the end of each month.

Did I write like clockwork on first of every month? Hell no.

But I did it.

Slowly and surely things started to change. Here’s what happened.

Getting a Grip on My Money

While writing my goals, I began wanting to learn how other people accomplished the things I wanted.

I Googled everything I was interested in, and came across a whole underground movement of people that were designing their life for the things I was after.

It was magical.

I came across the legends: Mr. Money Mustache, J. Money and The Mad Fientist.

(I linked to my favorite article by each of them above, if you’re interested)

And I read everything. Seriously, everything.

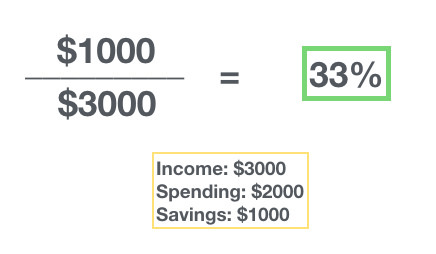

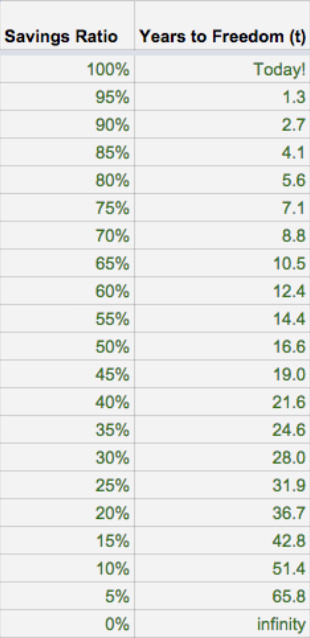

One of the most important things I learned was the importance of hitting this number called your “savings rate” every month and year.

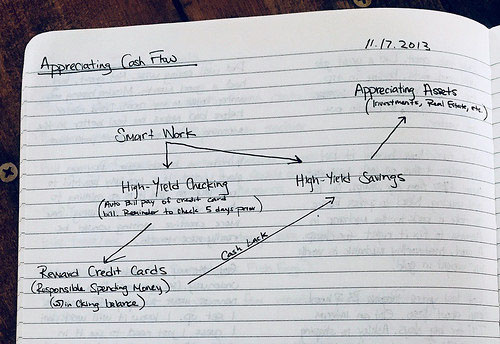

All I needed to do was hit that number and I’d know I was on track. I went off and built a whole automated system that became my personal financial dashboard.

From it I could see my net worth.

For the first six months, I just shoveled money into my savings account trying to hit the balance I wrote in my journal each month.

That worked great, but I began wondering when I should start investing, 401k-ing, Roth IRA-ing…

You know, all that adult-ing stuff.

That’s when I came across the godfather of this underground movement, Jim Collins.

(Even with a comment like that I still couldn’t get her to read his stuff!)

From him I learned 90% of everything I’d ever need to know about investing, and I figured out what to do with my money. [Editor’s Note: Jim was the catapult of my (J. Money’s) investing strategies as well. Great teacher!]

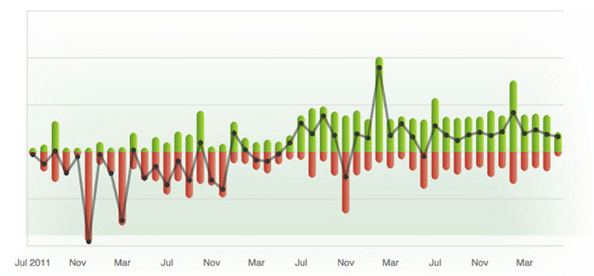

To jump four years ahead for one moment, here’s a look back at where I put my monthly net income (savings) each month.

The only thing I might recommend you change from the list above is the investing related lines.

Why?

Because I’ve learned that once there you have three paths to choose from: Paper Assets (aka The Stock Market), Real Estate or Business.

By doing a little research you can choose the investment class (or combination of classes) that’s best for you. (I’ve linked to the three best resources I know in those links above to point you in the right direction)

So this is how my puzzle pieces began coming together.

But I want to make one thing clear.

My whole journey above didn’t go down smoothly. It was messy, hard and even disappointing at times.

It was life.

I just kept writing. I just kept going.

Here are a few real-life highlights from how it went down.

What You Write Becomes Your Life (And $10,000 Mistakes)

I really don’t believe my life was that different than my peers.

But there were differences.

I’d say the most helpful differences were how I handled these three parts of my life: Housing, Cars and Travel.

Let me tell you what I mean.

Housing

“I will never move back in with my parents.”

I said those 9 words hundreds of times to my friends in college. In my mind there was no way, no how that I’d move home after graduation.

Welp…

That was the first thing I did.

One unforeseen benefit of the job I had landed was that the office was about 15 miles from my parents’ house.

I remember driving home from college with my dad and all my stuff in the back of his truck. We pulled into the driveway and my neighbor came out to say, “hello.”

I couldn’t believe I was moving back home.

We met with a brotherly handshake, and one of the first things I said was “Yeah, man, I’m only going to be here for a month. I’m already looking for spots in the city.”

Wrong again…

I ended up staying for 11 whole months.

But this action made a huge difference for me, especially at the start.

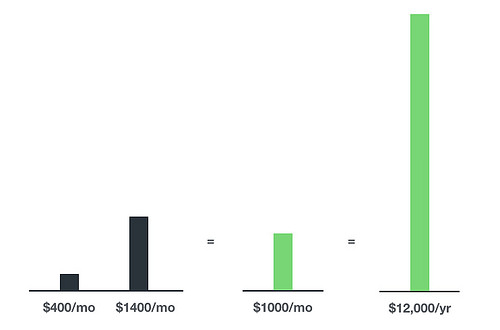

I was paying $400/mo in rent while my peers were paying $1,400/mo for rent in San Francisco. That put an extra $1,000 in my wallet every month ($12,000 over a year).

I know this option isn’t available for everyone.

But if I could talk to my old self without the “move in with parents” option, I’d tell myself to reach out to family friends, extended family or whoever I could to see what is possible.

In the end though, my parents are my parents and I needed freedom.

I wanted to live in an awesome apartment in the city. For me, that was one near the beach, close enough to bike to work and shared with great people.

I started asking friends and coworkers if they’d want to move into a place like that if I found one.

Key point – “If I found one.”

I didn’t want anyone on a 14-day or 30-day time schedule to make the jump. I wanted to move only if the perfect apartment came up.

I ended up finding two great coworkers who loved the idea and hopped on board.

Together we hacked Craigslist to send us any new listings that matched our “perfect apartment” specifications.

And in one month here’s what we found:

I took the small office room that was connected to the living room by a sliding door for $1,000/mo.

It was a great price, but I’d be lying if I said that room was perfect.

There were definitely nights where people wanted to stay up many hours later than I preferred. But for the most part, I was respectful about hanging out with everyone late and my housemates were respectful about the noise.

(Pro tip for noisy rooms: Earplugs. They saved me numerous times.)

All in all this rent kept me well below the city’s average rent, giving me an extra $400/mo ($4,800/yr) to stash beyond my peers.

Living in that apartment with good housemates at that price was another huge help.

But not everything went that smoothly…

The Car. The F—in’ Car

Maybe I’m weird, but I’ve always had this love-hate relationship with cars.

I love the flexibility they provide for my life, but I hate how much they cost when things go wrong.

Let me tell you why.

Three months after starting my job I started searching for a car. I searched and searched and searched, and felt like I’d never find the right one.

One day I came across some ol’ Swedish wheels — a 2001 Volvo XC70 (a wagon) for $5,400.

I was so tired of searching for cars that I decided then and there that I’m just going to buy this thing.

Wrong decision.

After eight months, a Baja California surf trip (that ended with a tuna can lid duct taped over a missing piece of the engine) and $6,500 in unforeseen maintenance costs later, I sold that piece of junk for $1,900.

I still facepalm when I think about that.

From that day forward I went into car-diac arrest for nearly a year.

I sold it a few days after I moved biking distance from work (5 miles), and began using my bike as my daily mobility for 3 months.

After a few months of that I bought a 125cc Yamaha Vino Scooter for $1,800.

Getting the scooter was the perfect transition into getting a car (and the ladies totally love the goofy looking scooter vibes).

This time I thought through what I needed the car to do.

I wanted something that I could pack up with gear, throw surfboards on top and drive to Big Sur for weekend adventures with a friend or two.

I then used these guidelines to help meet my money goals:

- Buy a car that’s at least five years old (here’s why)

- Find a car I like from this list of the top 10 cars for smart people

- Get a peer-recommended mechanic to look at the car before buying

- Toyota or Honda. Period.

What’d I get?

(Scion is a less expensive brand of Toyota)

Compared to the average new car price, that purchase saved me about $26,000.

It’s taken my girlfriend and I on a 2,000 mile road trip through the Western US, has taken me on multiple surf adventures and, after 3 years, is still running strong!

Travel

For my first year back I didn’t do much “plane” traveling.

Instead, I did tons of weekend trips. My usual schedule looked like this:

I’d pack my surfboard, bike and running shoes in my car and take off at sunrise to Santa Cruz.

I’d surf in the morning, eat a little food and then do a run nearby. In the afternoon I’d meet up with family friends for lunch or tea or just write in my journal overlooking the sea.

Then on the way home I’d go for a small hike, walk or bike ride, sometimes with friends.

But as time went by I definitely wanted to go on more longer term, faraway trips.

Here’s how I handled that.

I’d always heard about people collecting hundreds of thousands of points from credit cards and using them to fly for free, but I never understood how they did it.

I thought they were wrecking their credit score or going into debt and just wrote it off as something that wouldn’t work for me.

Until this new phase of my life.

I did some Googling and ended up finding a way to safely travel hack.

I made this video to show you how:

Not bad!

Once I saw how much money I was adding to my wallet with these type of acts, I started pushing my limits with it.

And consistent with “Ryland” fashion I pushed it a bit too far.

Girlfriend Ain’t Having It

What do I mean by too far?

Well, I got so into this “spend as little as possible” mindset that one day I became too paralyzed to even buy my girlfriend a birthday present.

To say the least, my girlfriend wasn’t having it (and rightly so).

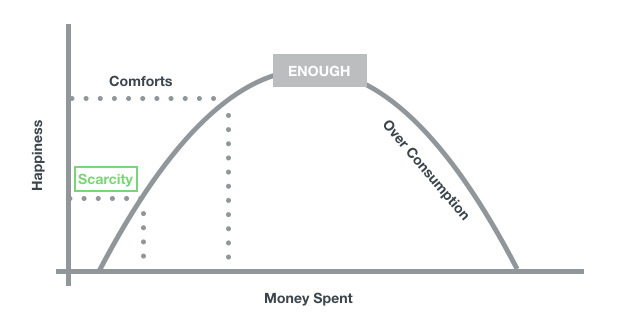

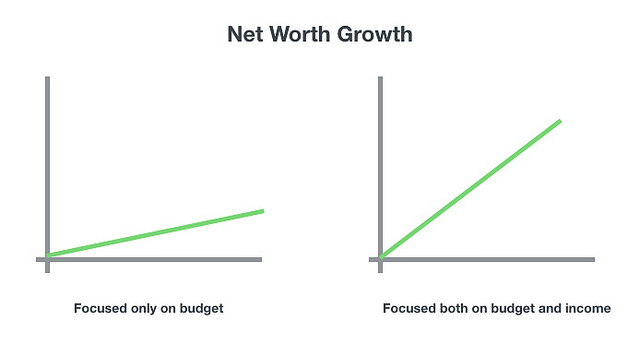

At this point, I had become overly focused on the “control my spending” side of the game.

I learned in that moment that the issue with only focusing on controlling my spending is it’s limited — I could only budget so far until I felt scarcity.

I was after freedom, not constriction.

So if I was to continue on my path, I had to turn my focus to the other side of the game — increasing my income.

That’s the ultimate goal — making enough money doing something you love.

So off I went.

How I Handled My First Job (It Wasn’t Pretty)

I’ll never forget my first interview.

It was in this tiny, awkwardly quiet white-walled meeting room.

One of my future colleagues came in and it seemed like we had a good conversation. As we were wrapping things up he asked, “Are you willing to shovel shit?”

It was kind of a test to make sure I had grit.

Like any good interviewer, I said, “Give me the shovel.”

Horrible answer.

I got the shovel and my first job title became “Chargeback Support Representative” making $47,000/yr.

You know when you see a charge for $132 that a fraudster stole from you and you call your bank?

I was the person who picked up the phone.

The thing was, I loved the company I worked for and I really believed in its mission, but I couldn’t stand my position or my boss, and my work suffered because of it.

I wasn’t a team player, I did C grade work on my daily tasks and I just wasn’t myself.

For two years I felt as if I would show up, do a couple tasks and accept the normal small raises for being a warm body in a chair.

Then, right around that “birthday gift” incident, I finally switched positions to one I knew I’d enjoy more.

I was excited to come into work, happy to go above and beyond and loved supporting my other teammates.

This newfound energy led me to two raises in 10 months from $55k to $70k with bonuses.

If I could summarize the top things I did to get those raises it’d be:

- Asking my boss what the #1 thing I could do to be successful in my position. (Then doing it)

- Asking my boss what’s the biggest thing she and the team needed help with outside my roles and responsibilities? (Then doing that also)

- And being kind, uplifting and helpful to everyone.

Seriously. That’s it.

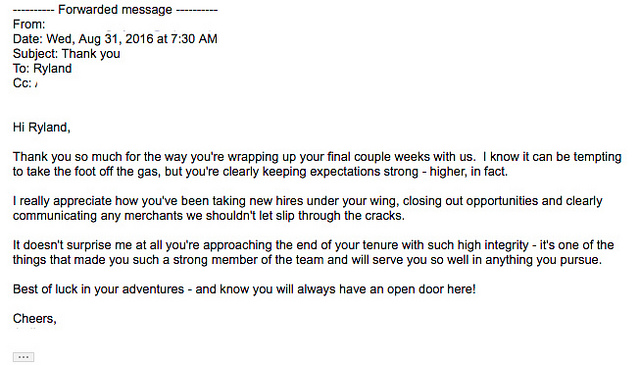

And when I decided it was time to transition away to work I enjoyed even more, I got notes like this:

In other words, when I started adding value to the team I wasn’t just getting paid more, I was also building my personal capital.

Think of it like this.

Say I go to work each month to work on a house. Every two weeks rent comes in.

If I put in new carpets, upgrade the utilities and paint the rooms while at work I could charge more for rent (increase my income) and know that the value of my house was going up (my personal capital).

Everything was better with this new job.

But within a year, I was ready to move on again toward my financially independent life.

Living a Financially Independent Life (Before Financial Independence)

A financially independent life.

WTF is that anyway?

Three years ago I would have told you I’d be financially independent the moment my passive income covered my lifestyle cost.

Today I believe it’s totally different.

Today I believe I can have a financially independent life as soon as I have enough money to have the confidence to walk away from any situation that doesn’t benefit me.

For me, that moment hit about three years after my first journal entry when my girlfriend asked me this question, “Why not now?”

“Why not take off on your millennial adventure? Why not quit and start your own thing? You have the money.” She said.

She stumped me.

(That girl’s probably been my best financial advisor, haha)

I had saved almost $100,000 (not including investment growth) and had a net worth that could cover 7 to 8 years of my lifestyle cost.

She was right — why not now?

I took it to heart.

I started writing my own blog about financial independence. I started helping my friends with their money situations just because I loved doing it. And I put up a page on my site about coaching other people in similar situations toward financial independence.

One day a friend I had helped posted about working with me on his Facebook page.

From that group, my next two clients signed up.

I gave my heart and soul to ensure every person I talked to kicked ass. Then when they became clients I continued with that kind of help which brought in new subscribers and new clients.

While all this was happening I took my girlfriend’s advice, amicably left my job and gave a full shot at aligning my income to what I love even further.

Today I’m still giving it that shot.

It can be tough at times, but I know as long as I continue helping people as best I can the income side will follow.

And beyond money, I’m now working on the things I’m passionate about. Like taking a few trips a year without breaking the bank. And I’m on my way to making enough money doing something I love to live a fun, yet simple life.

I got here only because I kept going.

That’s it. That’s the secret — keep going.

I started this whole journey with tears rolling down my cheeks trying to build a budget that ended up looking like this:

I just started writing.

Goals. Reflect.

You can do that.

You can start right now.

It might make you a bit uncomfortable. Great! Embrace it.

Tell me the 4-6 things you want to accomplish deep down this month in the comments below.

Don’t think. Just write.

I’ll hang out here for the day, reading your comments and doing my best to help you out.

Thanks for reading,

– Ryland

**********

Ryland is a writer, outdoorsman and surfer. He’s also the founder of The Hidden Green, which helps young professionals (the ones who’d choose a mountain bike over a Maserati) do well with their finances. You’re invited to take The Hidden Green’s FREE mini-course — Do What You Love Finance or reach out to Ryland at ryland@thehiddengreen.com.

[UPDATE: Blog and course/email no longer active :( ]

Get blog posts automatically emailed to you!

My husband and I don’t buy each other real gifts anymore. He gave me potting soil when I turned 25 haha. You should give your girlfriend a savings bond or something so it’s not really spending. That would be cute!! Can’t say no to $$!

Haha… I miss getting savings bonds from my grandparents :) Of course, didn’t appreciate them AT ALL growing up! (Here – take this free money, but you can’t spend it for 20 YEARS!!!)

As much as I think that’s an awesome gift, I think she’d prefer the potting soil! haha :)

An awesome post, I love the handwritten journals, and such neat handwriting. More importantly, thanks for sharing your journey with us, sounds like you have come a long way, and are much, much happier and enriched now.

Thanks, Ms ZiYou! It didn’t happen like a Facebook or Twitter style company, but instead it was long-term, slow sustained growth (both financial and personal!). And I’m quite happy it worked out.

Thanks for the handwriting compliment. I’ve gotten that since I was in middle-school, but, to be honest, I just don’t see it. lol :)

This post is awesome! I love the journals, I have a chalkboard wall and do something similar!

That scooter is adorable btw. Glad to hear other FI bloggers are creating courses to help the community move forwards :).

Chalkboard walls!! Awesome!

Neat. I love whiteboards and chalkboards. Maybe you could write the goals and then after you reflect take a photo of the board (Month 1) and pin it next to the board. Then erase and start with month 2. That way you have a nice record of where you’ve been and you get the ease of use with the chalk board. :)

Also, see it’s true! The ladies totally dig scooters, guys… No need for the soop’d up Harley. ;)

Who knew writing a journal would be so life changing. I’m glad you realized that it was time to change your finances.

Congrats on your net worth and new love for finances!

Thanks, Ms Frugal Asian Finance!

Great story. I think there is something really therapeutic about journaling. And oddly something different happens in your brain when write it out with pen and paper instead of typing it onto a screen (but I’m old school that way).

I’d also throw Hyundai into the mix of cars to buy. I’m a former Honda owner and loved my old civic, but I’ve been thrilled with my Sonata. At 230k miles now, hoping it’ll last to 300k.

Thanks for sharing your story!

I’m old school like that too. For whatever reason, I’ve always found it to reach below the surface and stick.

Nice work on that Hyundai! Love it. Thanks for the kind reply.

I love mapping out our money! The visualization helps knowing where everything is coming or going.

I was never really good at journaling but I guess that’s what I’m doing nowadays. It helps me think things out before taking action with my finances and life. I’m heavily goals oriented too. There isn’t a set of goals I want to do this month specifically but I’m eager to get other goals done like maxing out our accounts and starting a brokerage account.

Rad. I found that after about 18 months I started doing every other month and then quarter by quarter. Seems more similar to where you’re at with the maxing accounts stuff right now.

Curious, what money stuff have you mapped out?

The quote for jl collins being your uncle LOL!

Thank you so much for sharing your story, writing something really makes a difference than just typing or thinking about it for sure.

Lol Every bone in my body told me she’d be like, “Wow, he sounds awesome! Can I meet him??”

Instead I was met with pure crickets. lol

Thanks for the kind comment, Chris. Appreciate it, man.

Daaaaaaaaaang, that was a great post! It’s crazy how much can change in a matter of a few years. And to think it all started with a busted budget!

I had to laugh at the shoveling shit job. Reminds me of one of my first jobs out of school.

I think it was the longest post we’ve ever featured here before :) Outside that time I tried to post one million “$” marks to show just how big that number actually is! Haha…

https://budgetsaresexy.com/what-one-million-dollars-looks-like/

Here’s the post – although it might crash your browser as apparently blogging wasn’t meant to hold a million characters in one article ;)

hahah From my research for this article, I learned that J. Money does awesome, hilarious stuff like that.

Here are my two favorites. Well worth the clicks for the laughs.

http://whyyourepoor.com/

http://motherbudgeter.com/

Love it, J!

Thanks man – gotta spice it up and keep people on their toes, right? ;)

Thaaaaaaaank you, Defined Sight! ;) (Love that name, btw!)

And yeah, sometimes you just take the shovel and start moving shit around to get somewhere. lol Seems like we’ve all done something like that in our lives, but done with intention you pretty easily start shoveling dirt, rocks and other much more fun stuff. ;)

Wow! I salute you for writing a journal. That really takes a lot of self-discipline and commitment to do. That’s one area where I am really bad at. If not for computers, I probably won’t have a record of a lot of things financials. I agree with you on only buying pre-owned cars. In fact, even a 10-year-old car for me is not that old to buy anymore. Cars are better built nowadays in my opinion.

Thanks! Computers store 99% of my financial records too, but it’s always nice to leave the screen for a bit. :)

Wow thanks for sharing your story Ryland! That is so awesome that you had the courage to step away from “stable job” and dive into your passions. We desperately need financial educators, since our school system does absolutely nothing for that, so I think you have a BIG market demand to fill! Best of luck in your endeavors, the PF community is cheering you on.

Thanks, Budget Epicurean! I simply hit my point where “money” couldn’t be the excuse anymore for living how I wanted.

Thank you for the kind words and stay in touch!

PS — Love the hidden Stoicism in your FI name. Good stuff!

Wow this is such a great summary of so many different aspects of financial independence and how to live the life you want to live. Your story is very inspiring Ryland! I think my favorite part you touched on is: “Today I believe I can have a financially independent life as soon as I have enough money to have the confidence to walk away from any situation that doesn’t benefit me.” This is so key. Personal Finance writers and experts don’t just talk about early retirement and financial independence because we want to see a certain account balance or net worth. We want to see our financial situation bring us to a place of freedom where we can live life the way we want to instead of making compromises.

Thanks, David. I really tried to touch on as much as I could in the story to give someone new a full picture of FI.

I love the part you highlighted. It’s probably the biggest thing I’ve taken away from my 4.5 years going after FI.

And I 100% agree that PF and FI writers don’t talk about it enough too. We don’t go after money for money, we go after it for the freedom to live the life we want.

(I love your stuff, btw. Been a silent follower for a while. :) )

Great job Ryland. That’s a pretty amazing turn around you had. I’m jealous that you started off so young. A lot of people get stuck in their job and the cycle of lifestyle inflation. That’s really tough to escape once you get used to it. Writing your goals and inspiration down is so important. It helps so much.

Really cool that you started your own business. It sounds like you’re helping a lot of people. My motto is also – keep at it. Everything will keep improving if you work at it.

Hey Joe! I love your stuff, man. Neat to see you here.

Thanks for the kind words. It didn’t happen overnight, but with that “keep at it” mentality it definitely did happen. Now I’m doing my best to help others keep at it too. :)

If you think any of your readers’ might find the story useful, feel free to share. Cheers!

I like the journal idea. I use to do hand written notes every day to keep myself on task so I get it. Sometimes putting it in writing makes it more real and drives you to do it. And evaluating how you did allows you to improve.

Keep on moving!

Writing it down always helps sink it in more for sure. I used to go through like 800 sticky notes a week, haha…

hahaha That’s epic. Would love to see a pic of that

This was such a great post! “I believe I can have a financially independent life as soon as I have enough money to have the confidence to walk away from any situation that doesn’t benefit me.” This quote completely resonated with me and made me think of financial independence from a whole different standpoint because it is SO true! Awesome story, Ryland! Thanks for sharing!

Thanks, Kendall!

Figuring that quote out for myself may have been the biggest change in my life over the past few years. Glad you like the story and hope it helps!

Thank you Ryland for your excellent article! Here are my immediate goals:

Get all my airline miles/points from the 3 credit cards. I overextended a bit so I need to watch the spending to be sure I make the minimum amount. I overextended a bit since I was initially declined for Amex Gold, but called to request a reconsideration and got an acceptance email two hours later.

Plan for travel to Cuba or Hawaii with my existing points.

Start writing a financial/life journal like you. I’m similar to you, I like lists.

Refinance my car. It’s a high rate now since my credit was bad 3 years ago. I kept holding off since I was wanting to privately sell my Honda and get a used Pathfinder or Tacoma, something 4WD, but I’m getting no inquiries for the Honda despite a good price.

Switch over to Aspiration bank for my money HQ: direct deposit, redirect to Betterment, pay bills, etc.

Nice! It’s going to feel soooo good condensing and getting everything super efficient! I’m down to one bank account and one credit card and one of pretty much everything these days and find in incredibly freeing, while still reaping 80% of the rewards of a more fancier setup. And the beautiful thing is that it’s so much easier to maintain and not even think about anymore :)

Love your writing Ryland! I really enjoyed your post.

I’ve been working on defining my goals for about 6 months now. It is amazing what happens when you start writing things down. I’m working on my own blog and slow and steady seems to be the way of this path.

As for my other goals I definitely want to pursue self-employment down the road, lso finally paying off the rest of our debt.

learning, growing, and making sure enjoying life along the way including fun ways of being healthy.

Hey Alexandra, Thanks!

That’s awesome. I’ve found that it’s not about making “the perfect” set of goals. It’s just about making the goals, even if it’s messy. If you do that simple each month (Goals. Reflect.), then it’s perfect. :)

Sounds like you are on a good path. What’s the biggest thing holding you back from being self-employed now?

Hey Craig, Nice! Those are rad.

If I were you, I’d prioritize building out that money HQ. Automating everything like that is one of the BEST things I’ve ever done.

Also, nice work on those CC points. That is the way to get you to Cuba/Hawaii worry-free.

Keep me posted on how things come!

Wow! First of all, your girl sounds like a keeper. :) Secondly, good for you for doing what makes you feel fulfilled. And for having the financial means to do it. Third, your picture of the moped….Can we just talk about how clean that garage was??? I mean, really. I am SO impressed.

The top things I want to accomplish this month? Ironically, look into CC for travel points. We have this insane goal to visit all 50 states before the kids graduate college. And the more help we can get in free airline miles, the better. We are almost half way there, btw!

I also want to calculate my net worth. I have only done this once before, and it was so motivating. At the beginning of the year, I wrote it down as a goal to do at the end of every quarter.

Lastly, I would love to do more research on finding my number for FI. I would love to hear of any resources that you think I should check out!

YOU BETTER TRACK THAT NET WORTH!!! :)

Thanks! She is. :)

That garage photo… I know! haha I had just finish building that board rack and putting in storage racks in the back. Along with the bike racks too. When it looks like that you got to take a photo!

Those CC miles will totally make hitting that travel goal possible. You should definitely start!

Figuring out my FI number was an awesome moment for me. It’s just ~25 times you annual spending. So spend $40k/yr? You need $1M. etc. Here’s my favorite article on it: https://www.madfientist.com/safe-withdrawal-rate/

Also remember that you can have that “FI freedom” well before you hit that number. Money is all about empowering you with the confidence to walk away from anything that doesn’t benefit you. Make sure to keep that in sight as you work towards that 25X number.

Stay in touch!

Great Post Ryland! I love that you graph your savings rate. I do my net worth but savings rate would be a great addition and is an early indicator of net worth.

Loved the way you used your journal as a self reflection tool and reference point as to what is important to you.

Thanks, Laura! Exactly. Savings rate is a great early indicator of everything else that’s happening with your money.

Glad you found a few things useful, and hope it helps you on your journey!

I love this! I really like the 2 column strategy: goals and reflection. I keep a journal with financial (and other) goals for the year. Then, every payday (2 weeks) I record each expense and how much is going toward whatever the current goal is. Right now that goal is paying off credit card debt and a car. I do a monthly net worth statement to monitor overall progress.

The important things for achieving goals: write them down, have a deadline (timeframe), and make them challenging but achievable.

Love it! Sounds super similar. It’s really awesome to look back on it and see where I was at the start in 2013.

Love the post.

The initial thoughts (I’m not moving back in with my parents) and then the feelings when you moved back in were so real. Life teaches us many things (that’s not an original comment by me, so you can use it!).

A lot of your choices were perfect ones. And honestly, you lived a quality of life that most want but can’t have. Not because they can’t, but because they choose not to. You enjoy the outdoors and found ways to bike and surf on a budget. Love that. What good is saving if you can’t live and enjoy life?

Thanks, Lisa. I 100% agree with you.

Focusing on your finances is all about living and enjoying life even more. If it’s doing anything else, you’re doing it wrong.

Hi Ryland & J.Money,

Thank you both for having your blogs/websites set up. Ryland, this post really hit me because I remember having those days (even recently) where I’m crying because I don’t know how to solve certain financial issues in my life.

I’m 35 and only recently learned all about finances, passive income, emergency savings fund, Roth IRA, etc. I wish helpful websites like yours existed when I was 18-21, because that is when I made the worst mistakes and started bad money habits that led me to where I am now ($20k cc debt, $30k grad school debt). It’s not too late to fix this, right?

4 things I want to accomplish this month:

1. Build emergency fund to have 3-6 months’ worth of expenses – this is on its way! I arranged for my tax refund to be auto deposited into a savings account (that’s in a different bank than my everyday checking account) so I’m $1k closer to the fund goal.

2. Publish my first blog post – i have my domain and website up and running, i just have to turn the draft I wrote into an actual live post. I’m a little scared – did you guys experience this when you wrote your first post? My blog is mainly funny anecdotes on my life lessons thus far.

3. Incorporate Google Adsense (or some sort of ad revenue) into my website. Do you guys have any recommendations for this?

4. Complete 1 WordPress class on Skillshare

Thanks again!

Cheers

Rock on!!! My finances changed dramatically once I started my blog because it kept me so accountable blasting my info to everyone! Haha… so hopefully you find the same :)

As for tips, all I’ll add is to just throw yourself out there and have fun with it all… If it ends up making money later and turns into a “business” – great – but it’s a long path and if you don’t enjoy it you won’t even make it to that point.

So blog about stuff that makes you HAPPY and whatever you’re in the mood to do, and your audience will build around that if they find it helpful! And regardless, your money will get better just for thinking about this stuff a lot more! So go for it!!! :)

(And yes – the first posts are definitely scary, haha…. but then when you realize NOT A SOUL even knows it exists and hasn’t visited it in weeks it tends to wear off rather quickly, haha…. Until you get your first hater – then it REALLY hits you ;) (But that’s also when you know you’re onto something!!))

Putting pen to paper is a powerful thing. It takes abstract thoughts and crystallizes them into sound plans. Like you, I once had a little bit of debt in my early 20’s.

Knowing that I owed the bank $6000 freaked me out. I said to my self that I would never do that again. That little bit of debt changed my whole view and approach to managing my finances.

“I believe I can have a financially independent life as soon as I have enough money to have the confidence to walk away from any situation that doesn’t benefit me.”

Favorite line of the whole post. Been working on applying this mindset to my own life.

AGREED :)

We bought each other precious metals pure silver or gold coins (.9999) as gifts these days. One they appreciate over time, two they are tangible and actually feel like you own something together, but most importantly, we look at these coins as our retirement pocket money.

I wholeheartedly agree with your claim – what you write becomes your life. My father was a very active journal writer and he passed that passion to me. I often look at what I wrote – goals and comparing notes – it propels me to not just sitting on my butt after a 10-hour work day but just keep going to accomplish what I need to do. Thanks for the validation :-)

LOVE that you guys give each other bullion like that!! (And even more so that it’s in form of coins, as an active coin collector myself :)). Was just thinking the other day that it would be a good way for me to diversify more and maybe even include in my net worth… Feels silly to include a “coin collection” in there, but maybe just the silver/gold values since they’re easily liquidable? I wouldn’t go as far as cashing out stocks and putting all into gold/silver, but a % can def. help diversify more :)

We own several ETFs and gold/silver stocks, cryptos and some long-term dividend. Mr. Dragonfly is an avid reader on precious metals and has been tracking several companies throughout the years and have various portfolios on their performance. We are not stock analysts but we do our homework before we put in money. We cashed out some bullions at our local jewelry stores and got the market value back, and more. It’s a good investment with gold/silver.

We have recently started downsizing – selling several furniture that we no longer need. It’s liberating to see my room/floor. This is not a long-term strategy but it brings a different feeling when you can part with “things” – the “what you own, own you” is valid. You feel free when you are no longer “owned” by anything:-)

HELL. YES.

Love that more minimal feeling – so good for the mind and the wallet!! :)

Great article and very insightful. #1 things I tell everyone I find struggling in life is to ‘write it down’ but maybe I should tell them to start ‘keeping a goal related journal’. Hah

I want to put up a fence to keep a stray I have adopted from being picked up by Animal control. I want to get a part time job to pay for such fence. I want to attend the job 3 days per week for 4 to 5 hours each time. I want to enjoy a trip to see my daughter graduate. I want to stay saving with my first paycheck.

Does anyone know if there is any way to get Ryland’s course? It looks like his squarespace site is no longer active!

dang, sad to hear that…

let me reach out and see if I can get any info :)

UPDATE: my email for him now bounces :(