(Guest Post by Joe Taxpayer)

Ever watch movies that have those great car chase scenes? The Fast and Furious series for instance? At the very end of the movie, we see a disclaimer something to the effect of “the stunts were performed by professionals on closed roads, don’t try this at home.” As a financial blogger, I have to preface today’s post in the same manner: Attempt these things at your own risk!

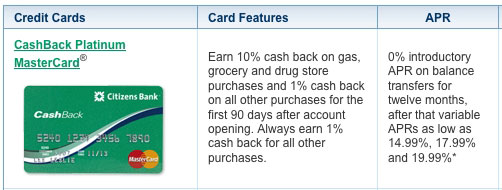

Earlier in the year, I received an offer in the mail by my local bank (where I had my mortgage and checking accounts), offering a cash back credit card with no annual fee. The thing that caught my eye right away was:

Get 10% back on all gas, grocery and drug store purchases for the first 90 days.

Not too bad. My wife and I already spend about $400 each on gas every month, and about $200 on groceries each week too. So after our normal spending of $1600 there alone, multiplied by 3 months, we’d be looking at a cash reward already of $480. But is it worth the trouble?

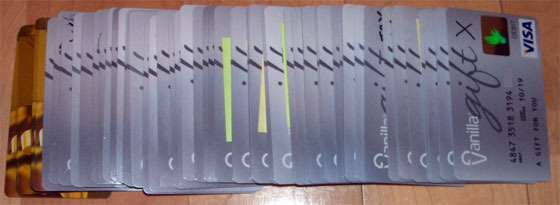

Then, I saw the rack. You know, the rack of gift cards for everything from iTunes to Home Depot to Target, etc? And there they were – Visa Gift cards. You can load them with up to $500 max, and then pay a fee of $4.95 to activate them. I wasn’t sure at first if these would generate a rebate, so I took a chance, bought two of them, and then went home to read the fine print. No exclusions! And two days later I saw a credit of $101 hit my account.

Over the next few weeks I learned the following things:

- CVS will request ID when making large purchases of gift cards like these.

- While the credit card companies (Mastercard and Visa) have rules that prohibit making ID a condition of purchase, I decided to not be a jerk and cause an issue every time I bought one.

- I also learned that some card issuers will freeze your account if the purchases look suspicious. Buying $4,000 worth of these cards in one day went over the line.

- Last, I learned that I must have been the first person to think of this, as two weeks into my shopping spree I noticed the deal wasn’t available anymore to any new customers.

The punchline is that I bought $50,000 worth of these cards. Including some Amex gift cards, as Costco doesn’t take Visa. I bought 100 of them at $500 each, racking up a total rebate of $5,050 and netting me a total profit of $4,550 (after taking into account all those $5.00 activation fees).

What have we been doing with them all? Methodically using them for all our regular expenses, as well as reimbursable business expenses. When I consider all the deals that people chase – the coupon cutting, the mailing in rebates, the Groupon purchases – I think this deal was one I couldn’t walk away from. $4,550 is close to the median monthly family wage. A month’s wage for a stop at the drug store on my way home every 2 or 3 days…

Could anything have gone wrong? I suppose. If any of the cards I paid for didn’t load properly, I’d have to spend the time and effort to make a claim to the issuer which would have been tougher than for a regular credit card. It’s also taking a bit of effort to track the spending and balance remaining on all of the cards too. Turns out, though, that supermarkets are pretty good about accepting partial payments off a gift card and letting you use up the small balances that might remain.

Will I get rich by deals like these, or with other zero interest credit card offers? No, not likely. But I’ll also not get rich walking by hundred dollar bills left on the ground waiting to be picked up either :)

———

Joe is a personal financial blogger, and when he’s not chasing crazy deals, he writes at www.joetaxpayer.com.

EDITOR’S NOTE: I asked Joe if having all these gift cards now made him spend money faster since it doesn’t seem “real” anymore, and he actually told me he’s spending LESS! So there’s even more savings that’s not calculated into the overall numbers yet… Pretty interesting (and bold) stuff!

Get blog posts automatically emailed to you!

I’ve heard of people ordering money from the mint using their credit cards to get the rebates, then depositing the money into their bank accounts, but that ended up being disallowed.

Don’t know if we would ever do this – it feels like a pretty risky proposition. Where does he keep them? That feels like $50K in cash sitting around.

Also – how many months worth of expenses is that? Is he losing out on having money in an interest bearing account as a result of it?

Very cool! I’ve thought about something like this but my Chase card doesn’t consider gas station convenience store purchases as gas station purchases. Glad it worked out for you though. I’ll have to keep my eyes out!

I’m going to have to keep my wife away from these silly things:) She loves using credit card rewards. We’ve picked up about $1,200 this year from using new cards she applies for. I don’t think I want her spending 50K outright!

So Joe, how are you paying off the card? Do you have the cash to front that? From reading the article, I thought you might have indicated that there is a 0% introductory rate. However after looking again, I see that the 0% is only for balance transfers. Am I missing something?

If you paid off the card right away, mad props to you. However, I do not think this will work out for many individuals. Just seems like risky business.

I feel like I’m missing something. Unless you’re able to pay your gargantuan credit card bill with those gift cards then spending $50000 to get back $4000+ hardly seems worth it.

Haha, this is amazing! I am going to have to keep my eyes peeled for stuff like this.

Wow this is very interesting! I don’t have $50K to spend on gift cards but I feel like we would spend more if we had them. Congrats to yo for actually spending less!

People are doing this with the Chase INK cards at office stores since it is 5X points all the time. These deals are slowly getting killed off since it doesn’t make the credit card companies as much money.

The best deal was the mint… Purchasing coins at face value and depositing them in the bank. There are some great stories of people doing that and order pallets of coins at a time!

Doing this with gift cards seems more complicated than necessary. I know of people that put all their day-to-day expenses on a credit card and pay it off in full at the end of each month in order to cash in on rewards. I’ve considered it, but I already have a pretty awesome spreadsheet set up to track all the activity in our checking account, and I feel like if I switched to using credit cards for everything, I’d have to have one spreadsheet for credit card stuff and another for balancing the checking account. Too complicated. :-P

I think I’ll still to my current method of using the checking account for day-to-day expenses and cashing in on rewards points for online stuff and also large purchases – I was able to rack up some major points by using a credit card for the taxes and fees on the car I bought at the beginning of the month. I get to earn a (very) little interest for another month while the cash I’d set aside for that expense sits in my savings account, and I just got a lot closer to getting a gift card with my rewards points!

I don’t see the point of using gift cards or using a credit card to buy the cards. I guess I missed something like the above people??? Most gift cards have a use-by date and a lot of stores around me won’t use the gift card unless you know the exact amount left on it. Like for instance you purchased $50 worth of stuff, but know the gift card has around $10, they won’t take it unless you know the exact amount- except for Target that is. Besides not knowing the rate of the credit card or your payment details, it looks like you went on a spending spree with a new card. I have enough cards and that would just screw up my credit. I don’t see a point to this at all. Lame.

@ Mrs Pop – Our credit card spend averages $6000/mo (including business expenses) so just over 9 months to use the cards up. The misses interest was nothing, short term rates are so low.

@ Lance – Agreed, I was surprised when the online statement showed the $100 credit when I grabbed the first two cards. But it worked. And it’s over now.

@Greg – This actually made my wife more aware of her spending, and the months we used these spent a bit less than average.

@Adam – the deal was for 10% for first 90 days of purchases in the three categories. The card had a $15K line with 0% interest for a year. So I used our savings to turn $35K savings into the cards, and the normal bills we didn’t get (i.e. the regular card) went to replenish savings.

@Ashley – With normal spending, the cards are all but gone now. If you had a budget of say $1000/mo in spending to run through a credit card, you might have chosen to buy up $10,000 worth of gift cards, and then just use them for that cash flow every month.

@Michelle – Thanks! If the deal were still available, see my answer to Ashley. The bank took it down when they caught on to me.

@Brian – I saw the Mint deal, now that seemed crazy, too much carrying coins to bank, waiting on line.

@Stephanie – Understood, I talked to my wife first to see if she was in it with me. $4500 cash profit was too god to turn down.

@LB – The cards were “Vanilla Visa” which function like a regular credit card. They had a 2018 expiration. I admit, using the card up was a bit of a pain. When they dropped below $100, they were used at the grocery store, who easily rang up the last bits, even $1.49 and then showed the new amount owed. Again, the rate was zero, but if it weren’t I’d have simply paid this card in full.

In summary – I turned $50K in cash into a $50K pile of ‘cash load credit cards’ for a net gain of $4550. Yes, a bit of effort along the way. $4550 tax free would take over $7500 to gross, and this was to good a deal to walk away from.

I still love it that you went all in like that, Joe. One of the best stories I’ve heard in a while – thanks so much for writing it up for my audience! Big fan of yours :)

I guess if you have $50k in available cash that makes sense. Most people don’t.

Thanks so much J$ for letting Joe tell his story. Joe, this was a very good topic. I’ve learned something for you!

@JoeTaxpayer – How is the $4550 tax free? Won’t it show up as interest income (or similar) on your bank’s 1099?

Sounds incredible and unbelievable. I’m surprised you bought $50,000 worth of cards. That just seems scary to me, but free money is free money right? :)

Hey Joe Taxpayer- I used to work for a credit union in their VISA department… you can actually do a “cash advance” on VISA gift cards at any bank teller window. There shouldn’t be a fee since it’s a gift card. When they say treat it like cash, they mean it and you can easily transfer it to cash.

Okay, I will definitely admit it’s a cool story. But you left out one detail:

How are you dealing with the $50,000 sitting on your credit card bill? The offer you show a pic of doesn’t mention 0% APR on anything other than balance transfers. Or did you have $50,000 in the bank?

Also, I have to agree Eddie: You won’t get the funds tax free. It’ll show up in a 1099 mailed to you and the IRS. I got one a couple years ago just from a $100 bonus from my bank when I opened a new account. That said, you’re probably not paying more than 25%, so you’re still looking at a net of about $3,400.

Okay, I need to learn to read because you already answered the APR question. Nevermind on that.

@Money Beagle – The card itself had a $15K line, and, as we spend about $6K/mo, we drew down savings by less than $20K to do this. If the deal were still available, Doing it with 6-9 months worth of regular spend would still have been reasonable.

@Eddie – This was not a ‘signup’ deal, it was a cash rebate on spending, no different from the 2% cash back card I’ve used for 10 years. I am not expecting a 1099.

@Veronica – That’s how I looked at it. A bit of effort, stopping to buy cards multiple times on way home, and then tracking their use, but a large reward.

@Perry, I’m at the end of the cards now. Had I known this, I’d have done it 10 fold. Maybe next time.

@Abigail – saw your update, a new account bonus is taxable, I agree. Rebates are your own money back, so not likely to be a taxable item. Note, I never say never. Just like I looked at account on line to see the $1000 in cards counted as a purchase, I’ll still keep an open mind that the bank will issue the 1099. I don’t see it on 2% rebates or 5% rebates, so I’m 90%+ sure I won’t see it here.

I think this sounds awesome!

That’s amazing Joe! You’re one clever dude. Not a bad return on your investment!

Go big or don’t go at all, eh? I’ve heard of people doing this on a much smaller scale with credit cards that give you a larger cash back rate at grocery stores, but I can’t say I’ve seen/heard of someone going this big with it!

Hahahaha! OMG! GENIUS!

I never thought of this. I get really annoyed at some places when I can’t use my cash-back card to pay for a purchase. Maybe this will let me skirt around that?

10% is amazing though, I think my card only offered 5% back for the first 6 months and that’s probably expired now.

Ok I just checked and I get 3% cash-back for the first $600 spent on gas & groceries. I don’t have a car and I only spend about $200/mo on groceries BUT those Visa gift cards are perfect and I find most local grocery stores have gift cards for my favourite restaurants and clothing stores.

So doing this. Starting right now.

@Holly – Thanks! It was a fun deal.

@20’s – The real investment was my time, happy with the return

@First Million – My only regret is not going even higher!

@Bridget – You had me at “Genius.” Ha! Thank-you – As long as the cards you buy are for planned purchases, you’re good to go. Good luck, let J$ know how much you make using this idea.

Am I the only one that thinks this is unethical?

Yes, I understand that credit card companies are out to get all of us, but offering 10% on grocery purchases and then purchasing gift cards at the grocery store, while going with the letter of the deal is against the spirit of it. I suspect that had the bank found out you did this the rewards would likely have been invalidated.

Erik, I was up late last night, and had a chance to sleep on this. I have only one response – The world would be a far better place if every last person had your sense of ethics. I appreciate your thoughts.

Bravo, Joe! I just wish I would have thought of this idea first.

Joe, it’s a brilliant idea, and I’d do this in a flash, but you really need to be careful about your taxes. Getting – or not getting – a 1099 has absolutely NOTHING to do with whether this is taxable income or not. (I’m a CPA, but don’t take my word for it; check on your own.) It’s income: it’s taxable, period. Yes, there are some items of income that are specifically non-taxable, but rebates are not one of them. Too bad the deal was taken down, but congrats for thinking of it!

You are incorrect. This is a rebate and as such is not taxable. The courts have ruled on such matters previously against the IRS.

Oh, and something to add: to those of you who think this is too much trouble: you get to choose that for yourself but for crying out loud – this is free money! Doing one more spreadsheet is no big deal!

@g – from the Usenet group misc.taxes.moderated there was a long discussion of what’s taxable and what isn’t. They made a distinction between ‘bonus’ as in “open an account and get $500” which would be taxable, and “X% back” which is a rebate.

There are some reputable people there with decent credentials who were in agreement that rebates are not taxed.

I’m asking you – Do you think the 2% cash back deal I’ve been getting for 10 years should have been taxed all along? I’m not 100% on this, as I said above, if they 1099’d me, I’d be surprised but not shocked.

I understand the way drug dealers launder money is by purchasing these kinds of cards. That’s probably why they asked for your ID. Whaddaya bet they reported you to the local or federal authorities?

Being the paranoid type, I’d be uncomfortable about that. Wouldn’t be worth four grand to me. Privacy: priceless.

@Funny – At first, I took offense to being asked for ID. After all, the rules from Mastercard itself prohibit this. Then I spoke to the regional manager at CVS and he explained that the stores were finding a high scam rate on these purchases, and they were seeing stolen cards used to buy them. Cash transactions over $10,000 are reported by banks. I doubt local drug stores have the time or inclination to report a customer buying these $2000 at a time.

Privacy? If you use any card at any store they can track your purchase. There was a news story that Target profiled an under 18 yr old’s purchases, decided she was pregnant, and sent her the appropriate baby coupons. Target knew before she told her parents. Now, that’s creepy.

Man, these discussions are great! Morality? Taxes? ID checking? It’s crazy how one idea can have so many different side affects :) Super fascinated by all this stuff… thanks for always putting in your two cents when they come up, Joe!

The deal is still on: “Earn 5% cash back on gas, grocery and drug store purchases and 1% cash back on all other purchases for the first 90 days after account opening.”

For a lesser margin (5% at chase/ discover during their rotating categories and 6% amex blue) the deal is always available.

But spending out from a giftcard is a pain. Can’t be used to pay mortgage, property taxes or tuition payments (50% of my monthly expense). Nor can you pay your credit card bills.

That leaves me with just groceries & utilities. Now I need to scrap all the auto-payments and remember to pay all bills each month on time. Not worth the 10% savings. It’s quite a lot more effort than just “a stop at the drug store on my way home every 2 or 3 days…”.

@booyaa – I’m still following the conversation here. I see that for your spending, there might not be enough regular expenses to make this worth the effort. I just looked to see where we stand and there’s $10K in cards left at about the 10 month mark, so we’ve used $4000 per month on average.

I’ll add one point I missed in the article. Some charges withhold or freeze an amount higher than the bill, hotels and restaurants, for instance. So a dinner bill of $200 might freeze $300 on the card until the charge gets fully processed. No argument from me, this meant tracking and a quick check on line to verify the lower amount plus tip was withdrawn. After a month of that, I stopped using them at restaurants. All in all, if this exact deal came up again, I’d jump all over it and see how far I could push it.

(And then you better write up another post for us to see how much better you did! ;))

Your accounting is incorrect. You only made $4550-1800 with the deal. You have to discount how much cash back you’d have had if you just with your normal business. Since you say you spend $6000 a month, and the offer lasted for 3 months, that means you’d have had $1800 cash back.

@blabla – I see what you mean. The 10% reward was only for gas/grocery/drug store. So had I simply used the card as usual, only 1/3 or so would have gotten the full 10% rebate.

What you miss is that my normal card gives 2% back on all purchases, so between the 1% fee and 2% regular card, my real gain was 7%. I’ll concede that. Either way, it was a once-in-a-lifetime deal. (until the next one comes along)

I got the same offer and did the same thing, Only got a double bonus with Stop and Shop giving 2 times points for gas rewards. So besides earning $4500 in cash back (3964.50 net profit minus the $5.95 per card for 90 cards). I have paid under $20 all summer to fill up the car from July to Sept. taking off $2.20 a gallon for each fill up. This card is golden if you get an offer. As for cash flow i have a home equity line of credit and used Bluebird card to unload the gift card money for no fee at Walmart

Nice! Way to work the game :)

For those interested in this type of thing, it’s called manufactured spending and there are a lot of resources out there for those interested.

From what I understand, the tax ramifications do not matter in this instance because essentially you have $50K in gift cards and $15K in debt with $4,550 in cash back rebates, none of which are income because you don’t have to pay taxes on money you already paid taxes on. If you do the math then you are left with your initial savings of $35K and a profit of $4550, but that is only if you paid off the $15K credit card debt in full without having to pay any interest. If you don’t pay off that debt in full before the 90 days interest free period is up and only pay minimal payments after that until it is paid off you will have made no profit as the interest will eat the $4550 and then some over the life of the loan. And from what you said, you did not pay it off in full, therefore you made nothing but a pile of debt and turned all of your liquid savings into gift cards that expire over time if you don’t use them. Sorry, but that doesn’t sound to smart to me.

Adam – The credit card was paid off before the 90 days. I had the money available to do so. The $50,000 was less than a year’s spending. We used them up after about 8 months.

This deal is long behind me. There was no interest to eat up any of my profit, it was all paid before the card charged its regular rate. You’re welcome to view it as a pile of debt, but as I always had the cash to pay it off, I view it more like turning $50K I would spend in the next 8 months, and turn it into $54,500. There was never any risk of expiring before we used them.

To be clear, in effect, I exchanged $50,500 in cash for $55,000 in Visa gift card. It ‘cost’ me 25 visits to CVS, at 10 minutes each, 4 hours of time. A bit of a pain to use $500 cards. But as the balances dropped below $20 or so, I just dumped them against my cable bill. An easy bill which let me make multiple small payments on line. Some stores (Trader Joe’s for one) easily just ran the card to zero and told me the amount I still owed them. So maybe a few hours of extra pain to use these. In the end, $4500 is nothing to sneeze at. 30% of 55+ Americans don’t even have $10,000 saved for retirement. Smart is seeing an opportunity, assessing the pros and cons, and jumping on it. Stupid is not going for a full $100K.

I believe you misunderstand the timing, the risk, and the concept of money for nothing. Excuse me, while I queue up some classic Dire Straights.