Want to know how to save 2 million dollars and become financially independent? It really is possible. These people did it and they’ll tell you how it’s done.

[Welcome special guests Amanda and Travis today! The team behind Freedom With Bruno, one of my new favorite blogs on early retirement. I asked them to share their story with us, and here it is! I hope it motivates you!!]

Hi everyone! We’re a young couple in our early thirties and we just saved up $1,000,000, quit our jobs, and began our journey of financial independence.

We planned our first big adventure: driving from California to Costa Rica. We bought a used 2000 Toyota 4Runner and aptly named him Bruno. We fixed him up so that we could sleep in the back, then we hit the road to camp and travel our way through Central America!

Life is short! Waiting for the full social security retirement age of 67 just doesn’t leave much time for all the things we want to do in life.

[Cruising along a beautiful road near Oaxaca, Mexico]

The Taste of Freedom

It all started a few years ago when Travis got laid off from his job in Berkeley, California:

“Suddenly, instead of waking up early and going to work everyday, I could instead do whatever I wanted! Sure, I needed to hunt for a new job, but that task was only eating up 30 mins per day. I could now sleep in, work on personal projects, exercise, read books, hang out with my cat, enjoy some cannabis, listen to music and go for a wonderful bike ride around Oakland… life was great! I could have dinner ready for Amanda when she got home from work, and maybe even bake some chocolate chip cookies!”

Sadly, after a couple months it all came to an end: he got another job.

It was at this point that the financial numbers were furiously crunched. Exactly how much money would we need to stop working, presuming we moved somewhere with a low cost of living? The answer ended up being $1,000,000. Living on a 4% safe withdrawal rate would give us $40,000 per year to live on. If you don’t live in the most expensive cities, this amount can go a long way.

[Editor’s note: There’s some minor controversy in the comments about whether the 4% safe withdrawal rate is enough to retire off of at 30. Just wanted to add a friendly reminder that early retirement doesn’t mean you can never work again! If the market takes a downturn, you can always adjust your expenses accordingly and pick up part-time work.

When it comes to the numbers, the best thing to do is to figure out your own goals and risk tolerance, and make the assessment for yourself. If you’re not comfortable with running the numbers yourself, you can use automated tools to help you figure out how to hit your (early?) retirement goals.

Personal Capital has a fantastic retirement planning tool that will look at your actual investment portfolio and run Monte Carlo simulations to give you retirement projections and financial insights with a high degree of accuracy. It even let’s you project how big life decisions like paying for a child’s college or buying a home could affect your retirement planning.

Best of all, it’s 100% free! If you’re even thinking of retirement (and let’s be honest, why else are you here?) you can run your own retirement numbers here.]

How To Save A Million Dollars

We started reading Mr. Money Mustache‘s blog and were both hooked. We embraced the idea of mustachianism with our whole hearts. Expenses were slashed and we ramped up our savings. We moved our money to Vanguard and optimized our portfolio with recommendations from many FI blogs. Eating at our favorite restaurants was saved for special occasions only, and instead we focused on making routine healthy meals at home. We hung our clothes out on the line instead of using the dryer. We wore sweaters around the house instead of jacking up the thermostat. We used bikes to get around town whenever possible and tried to use public transportation for our commutes.

All of these little things added up and we were well on our way to saving for our goal!

[The colorful, vibrant town of Guanajuato, Mexico]

On Autopilot: Working Hard and Saving Money

We were both lucky to have grown up in a wealthy, democratic country and have stable, loving families. With this solid foundation, we each got university degrees and aggressively jumped into our careers making the big bucks. Amanda has a Chemical Engineering degree and Travis has an Information Systems degree.

Financial independence is achieved by two means: maximizing income and minimizing spending.

To maximize income, we hustled and advanced our careers. Applying for promotions, and working hard to receive raises and bonuses when available. Here is a table we put together for a post on Early Retirement with Zero Income Taxes, showing our income and taxes over the last seven years:

| Year | Income (AGI) | Federal Tax | CA State Tax | Total Tax Paid | Effective Tax Rate |

| 2008 | $177,863 | $26,290 | $11,445 | $37,735 | 21.22% |

| 2009 | $158,857 | $26,192 | $9,713 | $35,905 | 22.60% |

| 2010 | $146,863 | $23,407 | $8,574 | $31,981 | 21.78% |

| 2011 | $149,305 | $24,775 | $8,229 | $33,004 | 22.11% |

| 2012 | $207,581 | $38,892 | $13,507 | $52,399 | 25.24% |

| 2013 | $204,718 | $38,241 | $13,729 | $51,970 | 25.39% |

| 2014 | $234,992 | $43,428 | $16,368 | $59,796 | 25.45% |

| Total | $1,280,179 | $221,225 | $81,565 | $302,790 | 23.65% |

As previously mentioned, we also reduced our expenses as aggressively as we could. Here is our monthly spending in the last full year of us working:

Note that this shows our monthly expenses for everything except our two-story rental home in North Oakland, CA. We lived there for the last six years of working and this was an additional monthly cost of $2,200/mo. So our total cost of living for 2014, including our rented home, was $47,576. Moving forward, our budget is $40,000 or less, which is the main reason we’ve moved away from the very expensive San Francisco Bay Area.

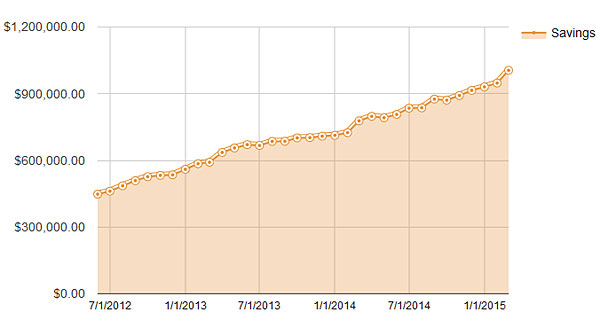

Once we optimized our lifestyle to maximize income and minimize spending, things were basically on auto-pilot. To keep track of our savings, in June 2012 we started checking our Mint.com balance monthly and updating a spreadsheet to track our progress. Our frugal actions, combined with a bull stock market during these years, meant we rapidly approached our goal of $1,000,000!

Here is the chart showing the growth of our portfolio over the last few years of aggressive saving and expense slashing:

Ongoing Travels

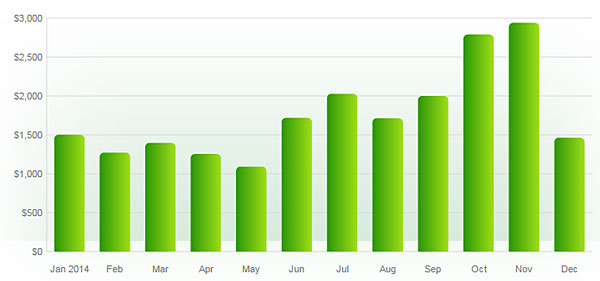

After quitting our jobs, we took 2.5 months to drive down to Costa Rica from California. We signed a five-month lease for a house next to the beach in Nosara, Costa Rica and have been enjoying our free time. Over the last six months we’ve taken some other short trips to Panama, Washington, D.C., and New York City. We’re now getting ready to head back up to the U.S. in a few weeks. We’re planning to be on the road for about 10 weeks with Bruno through Honduras, Belize and Mexico’s Yucatan Peninsula. We’ll certainly be documenting it all!

The good news is that so far during our traveling, we’ve done a decent job of adhering to our budget. Here are our monthly expenses so far:

| Month | Monthly Spend | Comments |

| April | $2,044.39 | Traveled through Mexico and Guatemala |

| May | $2,763.59 | Traveled El Salvador, Nicaragua, and Costa Rica |

| June | $4,215.56 | Costa Rica living with purchase of flights to D.C. |

| July | $2,684.01 | Costa Rica living |

| August | $2,800.96 | Traveled Costa Rica and Panama |

| September | $2,826.01 | Traveled Washington, D.C. and NYC |

| Monthly Avg | $2,889.09 |

This overall monthly average of $2,889 represents an annual spend of 3.6% of our portfolio. Our goal has always been to live on 3-4% of the portfolio, which at $960,000 translates to an annual budget of between $28,800-$38,400. This gives us a monthly budget of $2,400-$3,200.

So far so good!

If you’re interested in learning more about our finances or following our ongoing adventure, check out some of our other posts at Freedom With Bruno.

Thanks for reading! If you have any questions, just ask!

-Travis and Amanda

[Overlooking San Juan del Sur, Nicaragua]![]()

Get blog posts automatically emailed to you!

How inspiring! I love that they used a time of financial hardship (unemployment) as a time to re-evaluate their goals and then made concrete changes to reach their dreams. Well done Travis and Amanda, you have a new follower!

Awesome, thank you!!

Well, that’s awesome. I get inspired and bummed out a bit when I see this. I’m 30 now and we have 2 daughters. Our income is slowly creeping up towards where yours was when you started, but we’re not going to be able to save like you guys did when we’re paying 2k per month for daycare. But then, we couldn’t earn as much as we do without it. I like/hate my job, so I’m definitely getting out early. Just trying to figure out when that can be done. Right now target is 40 but that might change if we ever have another kid. Love the name Bruno though!

Daycare is such a killer. Hang in there!

I feel the same – inspired but challenged. Daycare for our two toddlers plus paying down student loans and some unfortunate medical debt is where a lot of our money goes, but I’ve just started using You Need A Budget and budgeting to zero and I can already see its going to help to really focus in on frugality in a whole new way. While I might not get to a million anytime soon, I might be able to payoff my debt sooner with this inspiration and some better budgeting! Let’s not accept the status quo life! Yeah!!

Thanks Chris! Before you know it, your daughters will be heading off to school instead of daycare. If you happen to have a son in the future, feel free to use the wonderful name of Bruno!

Yeah – kids def. change up the game for sure. They’ve been eating up my wallet for 3 years! :)

You know of any family that you can pay cheaper to watch the kids?

Or older, trustworthy woman in the neighborhood, that will watch them for less?

Take advantage of the kids in the family, especially on breaks, summer break. You should be able to cut back 25% of the expenses of daycare with that.

See if a student who takes night classes would be willing to nanny for you for a free place to live. Or for 700 a month. I used to do it as a student.

This all sounds really good, but I’d like to hear if the authors have any fears of a market crash or major market correction which would quickly kick them off the pace of adequate living expenses.

Good question! I would say we definitely expect a number of market crashes in the future, and when they happen we’ll simply tighten our belts and weather the storms until they pass. For example, we were recently thinking of traveling to Europe and when the market has faltered over the last couple months, we’ve postponed the idea (for now).

That sounds like an awesome experience to be able to have. And all of it is made possible by identifying the vision and making conscience movements towards it. It’s amazing what we are capable of accomplishing when we have a clear plan and a strong motivation to achieve it.

Great job Travis and Amanda!

Thank you very much! Mr. Largo – I like this name. It feels strong and a bit mysterious like Bruno.

That’s so fun! To people’s questions of what if it doesn’t work out–they’re 30 with highly lucrative skills–they could easily return to work if needed for a time. I’m sure they don’t want to and probably won’t need to, but a super fun sabbatical is better than spending those years in the cubical!

Thanks! It hasn’t happened yet, but if I needed to I could probably find work doing some remote part-time developer stuff from home. That being said, our skills will likely fade over time if we don’t make use of them. So I guess if a market apocalypse every happens, hopefully it happens soon!

If a market apocalypse happens there will be worse problems to deal with :) And you’ll be watching it unfold from a beautiful beach somewhere!

I love that the 4 Runner is named Bruno!! Inspirational story, thanks for sharing. Out of curiosity, did you use traditional savings vehicles like a 401(k), Roth IRA, etc? If you are drawing down already I’m guessing at least some of your savings must be outside of those.

Hi Dee! After we left our jobs, 401(k)’s were rolled into IRA’s. The bulk of our savings are in a taxable Vanguard account. For more info, all of our investments are outlined on this post:

http://freedomwithbruno.com/early-retirement-with-zero-income-taxes/

I love the charts and graphs, especially the one that breaks down all the travel. If you’re resourceful enough to make this happen, I imagine that you’re plenty resourceful to pick up new income streams if there’s ever a need. I truly enjoy reading about FIRE!

Hi Penny! Travis mentioned above that he would get some IT work on the side, if needed. I’d be excited to see what hobbies or activities I could get into that may pay out in the end. Always fun to brainstorm new ways to spend our time!

Great job, guys! Very inspiring! I will be right there with you asap!

That’s exciting, Holly! We’ll make some room in Bruno for you :)

Whoa, this is fascinating. I’m always so blown away reading about people who decided to change the trajectory of their lives in this way (while knowing that it would mean not eating out, not turning up the thermostat, etc. for years). It’s just something that never, ever would have occurred to me in my 20s. It sounds like your inspiration came largely from reading Mr. Money Mustache, which I think really speaks to the power of personal finance blogs and the personal finance community in helping people to become motivated to make real and lasting changes in their lives and priorities. I feel really fortunate to have stumbled upon this community earlier this year…and even though I’m definitely not going to be able to retire anytime soon, the impact of what I’ve read has definitely helped me to change both my priorities and my financial trajectory. Thanks for sharing your story here!

What a great comment, Sarah! We felt similarly fortunate when we found MMM several years ago. If his blog had not existed to introduce us to a completely different way of life, we would not have thought that FIRE is an attainable goal. This is one of the reasons we write & share! The crazy cold temperatures we kept in our house just shows how desperate we were to achieve and make it OUT!

Pete was the one who first got me interested on the path to FIRE back in college. I’ve had almost 2 years at my first job to put his advice to good use. It was basically the highlight of my year to be able to sit down with him at the Chautauqua to hear him say “Good Job” after looking over my financial info. Hopefully, I can do as well as you two in the long run! I look forward to reading more about your adventures!

You should count yourself incredibly lucky to have started your career with good habits and FIRE in mind! I have no doubts you’ll be able to achieve anything you want to :)

Great job saving so much while living in such an expensive area of the country! Can’t wait to follow your adventures.

Thanks Tre! Happy to have you along for the ride.

Just FYI, the 4% safe withdrawal rate studied by Bengen and then updated by Pfau et al is to cover a 30 year retirement – almost certainly not the case here. However, at a 3.5%-3.6% withdrawal rate, the risks of running out of money before heartbeats are slim and almost certainly within the risk profile.

This might be an interesting read as far as how to manage the money in retirement to improve the probability of not running out: https://www.kitces.com/blog/should-equity-exposure-decrease-in-retirement-or-is-a-rising-equity-glidepath-actually-better/

Thanks for this Jason, I’ll take a look at this! In our current travels, we’re targeting a spend of 3-4% annually, with our aggressive target being 3%.

Our portfolio is currently somewhere around $960,000, and our average monthly spending over the last 6 months has been $2,889 – which represents an annual spend of 3.6% of our portfolio. So far so good! Also, we’re thinking once we settle down somewhere and reduce our traveling expenses we can reduce our spending even further.

Wow! That was heck of an inspiring article.

Rich! Come on down! Costa Rica is ready for you, and the water is warm!

Will do! What is the best city to visit?

I would say anywhere along the coast in the NW. You can’t really go wrong!

Awesome job guys! I’ve been following your journey with Bruno for a little while now. But now you’re going to be in the limelight after this post and get some negative comments on your income and 4% SWR :) Just keep doing you!

Don’t be silly Fervent, there’s no such thing as negative comments on the internet! Also, if Fervent Finance says we can do it, then WE CAN DO IT!

Having haters it the definition of being successful :)

Could not agree more! Gotta love the haters.

Wow, this is truly amazing! What I love about it the most, is the fact that it is a proof that small wins are totally worth it. They just add up and make a huge difference. Definitely a great inspiring story to start a week with :)

Thank you Reelika! Over the years, every day I woke up early and forced myself out of bed for work was a small win!

Rock on, guys! You’ve found that saving substantial cash just isn’t all that tough to do as long as you want the end goal bad enough. You’re right, full time work sucks. Royally sucks. Luckily, finding a better way to spend your time isn’t tough – it can just take some time to accomplish.

Well done, and congrats.

lol, thanks Steve! Amanda was never too disgruntled about going to work, but for me it was mostly a bummer. For anyone reading this who actually enjoys their job: YOU ARE REALLY LUCKY!

For a minute I thought this article was about me. This morning I published a similar story with the headline “Zero to Millionaire in Ten Years”. :)

I’ve been following along on Amanda and Travis’s journey since nearly the beginning. Pretty awesome trajectory so far! It goes to show how you can save a ton in the bay area where the salaries are abnormally high. Stockpile your cash then get the heck out to somewhere with a much lower cost of living!

Thanks for all your support Justin!

Working in the frenzied Bay Area and escaping with money in our pockets feels a bit like breaking into a bank at night and successfully burglarizing it!

One of you will have to hit your 2nd million to differentiate yourselves ;)

I call dibs. Sorry Travis and Amanda.

Dude that’s not even fair, since your wife is still working! Plus since your portfolio is already more than 100k bigger than ours, you could at least send us 50k to level the playing field a bit, right?? :)

Nice little trick you pulled off there. It’s like quitting while you’re ahead in Vegas (except the house odds are in your favor if you know how to spend less than you make).

A perfect example of rockin’ it. Well done guys! Our path will take a bit longer (three kids and less than half your incomes combined)… but we’ll get there!

We are fully aware that not having any dependents helped get us there faster… Keep your eye on the prize and I have no doubt you’ll be joining us soon!

Can’t wait to dive in to some of the adventures and articles, I saw a little Nicaragua mention in here which could be where we potentially travel to and stay for periods of time as my wife is originally from there. Planning to visit again this summer. Thanks for the recap.

We’ll be heading back through Nicaragua on our way north shortly. If you or your wife have any recommendations, don’t hesitate to share!

Wow! Heck of a story!

Thanks Tiffany!

Simply amazing! What a great story to tell! Congratulations on your FI journey and enjoy your new life adventure.

ITs great they did it so early and are able to enjoy. I didn’t read anywhere if the rental was giving off some cash flow, which can help if the markets crash? Also they can go back to work if things don’t pan out or during big downturns. IT seems like even getting a job for a reduced salary like 75K will help them get back on track should the worse occur. Good luck.

Hi EL, we had a rental condo in Calgary, AB a few years ago but it was just barely covering the mortgage & expenses. We also weren’t around to take care of it, so we sold it (super small profit after the Canadian govmt took a bunch o’taxes). If/when we decide to settle somewhere, we’d be open to renting out our home for months at a time while we travel.

Very cool, they’re doing the same as Go Curry Cracker. :) Do you ever plan to venture outside of America?

Good question! There’s a family vacation planned to Jamaica next year, but Bruno is being left behind (shh we haven’t told him yet). Travis has still never been to Europe, so we’re playing with the idea of road tripping there or biking part of the EuroVelo route (http://www.eurovelo.com/en/eurovelos)… so many options!

Love love love this post! Definitely one of my favorites :)

We are aiming for financial independence by our early 30s and I cannot wait :)

Excellent, Michelle – we’ll see you on the flip side!

Your story is really is really inspiring, as I read more and more success stories the #1 thing I have realized is to cut down my own expenses which are sky rocketing these days, however all of them are mandatory at this stage but I am sure they are not recurring and will be down in about 6 months.

Yup, keeping your expenses as low as possible (doing whatever extreme things you can tolerate to get there!) leaves that much more for saving and compounding. There will always be hiccups with higher-spend months here and there. See if you can offset them with some extra-frugal months down the road :)

This is really cool, congrats to you guys! Although I don’t have any interest in long road trips or extended international travel, this is still a great example of doing what you want on your own terms. Like you, my family is trying to get ahead in a high COL area (orange county, CA). We have no interest in leaving, so it’s inspiring to see how another family was able to pare down their expenses and still come out ahead.

There’s always room for optimization towards leading a simpler, cheaper life – even in high COL areas! We loved living in Oakland, CA and had we been willing to work longer and amass more wealth, we might have been able to make it work long-term… but we were just itching to go! We’re optimistic we can find another (cheaper) town that will make us equally as happy. Enjoy your lives in the beautiful OC!

That’s freaking awesome. I can’t wait until I can quit my job and travel again.

Yes! Go Jason, Go!

Congrats to both of you for doing what you want at such a young age. I love that you are so young and you are making decision for where you want your future to be and what you want in your future. Responsibility of debt and material purchases (houses, cars, furniture, stuff etc.) are over rated….Enjoy!

Thank you Lisa!

Very inspiring, it’s great to see a couple that drew a line in the sand and made their dreams come true. Hard work always pays off.

Thanks Steve! We can draw lots of things in the sand here, living next to the beach!

I see people posting about the implications of a market crash affecting their portfolio, but I’m wondering if the rate of inflation over the next few decades has been taken into account?

Hi Judy! Good question. The 4% Safe Withdrawal Rate assumes a 7% return on investments, leaving 3% to be eaten by inflation. Here is a MMM article talking about it: http://www.mrmoneymustache.com/2012/05/29/how-much-do-i-need-for-retirement/

You guys are awesome! I wish I had the guts to do something like this.

Sylvia, you can accomplish anything you put your mind to! Want to become an astronaut and go to the moon?

Woohoo! Congratulations on achieving your financial goals and attaining the ultimate freedom. I love your approach to finances and as someone who was also GREATLY influenced by MMM (at a pretty young age), it’s awesome to hear where the desire to change courses originally came from. Can’t wait to keep up with your adventures! :)

Thanks Taylor! Happy to have another Mustachian enthusiast following along!

This is such an amazing story! Congrats on living your life now!

I’m working towards FI but it won’t happen anytime soon. I’ve got different goals tho so we’ll see where that leads me! Starting a family will definitely put a crunch onto my FI plans but hopefully I’ll get there.

Thank you, Christine. Best wishes for you achieving your own goals :) We’re also planning to start a family in the future – we’ll have to see how frugaly this can be done!

How do you make those kinds of salaries those? I know I’m in the non-profit field, but damn. Do you both work as tech programmers?

It also looks like your portfolio returned about half of your contributions in 2 years or equal to about $300k, what are you invested in? Those are some ridiculous returns even for a $600k-$1M portfolio, that’s between 15-25% per year. Not doubting you, but that’s incredibly lucky and impressive.

What kind of advice would you give to a couple who makes significantly less to still achieve something similar in a reasonable timeline and who also doesn’t start with such a big portfolio?

Do you still own the home in Oakland (and does rental income also included in your numbers – can you share details on how much it rents for and how much you bought it for?) or did you sell it and did that profit also contribute to your ability to retire early?

Hi Max, Travis worked as a system administrator and I had a job in engineering. We definitely didn’t have the high returns you mention. I think what you’re seeing is our contributions to the portfolio from our salaried jobs over the years (anything we weren’t spending was being socked away), in addition to portfolio growth due to market. We never owned the home in Oakland, we were renters for 6 years. No rental income in our portfolio (although this is a common strategy for retirees in general).

If you’re making as much income as you can fathom raking in, then paying down debt first, while spending as little as possible – many many tips out there to lower your expenses – and saving every penny you can into a low-fee Vanguard index fund. Easy-peasy. Email us if you want more details. We got all our bright ideas from Mr. Money Mustache and many other excellent blogs.

http://www.mrmoneymustache.com/2013/02/22/getting-rich-from-zero-to-hero-in-one-blog-post/

Awesome! I also live in the SF Bay Area and retired early and paid off our house. We made no where near as much and my husband will be working projected for another two years( still retiring early). We have always had to be frugal and much easier now without a mortgage payment- we live a simple life. Our biggest expense is that our 5 kids( 3 left at home) and food! So far they have gone through college debt free.

My question( and now after this article I am going to go back and read both of your blogs and find out what FIRE is) is first, which Vanguard you are invested in? Secondly, isn’t it all that wealth or assets just on paper since it is invested and it can go up and down? Is that million including your 401k? I am wary of the stock market as I lost a lot in my 401k at one point- it is like a casino and not a sure thing. Yet savings rates are dismal. I have tangible assets like my house which is 450k( was 675 at one point and also fell),275k in retirement savings( fixed percentage account not stocks),and 100k savings/cash so 775k in assets ( no debts at all). So do we have enough even to have retired early? Should I invest? Is there something safe out there to invest in?

Thank you amazing what squeezing can do or what you find when you start cleaning up and focusing. We do spend way too much. I needed this message though again now, feeling a bit detached from life only working and home with the family. Thanks. #cantwaittoretiresoon :) I actually don’t mind working but I do wish for more flexibility.

Hello Eva! Cycling through work-home-work-home can be mind-numbing. Hope you have a third option as an outlet of sorts: exercise, hobbies, a friend to listen to you vent, or reading blogs like these?! I wish flexibility for your future!

How are your taxes so low during the working years? Especially while living in CA?

Hi Albert, The table we showed is the effective tax rate we paid; different from the marginal tax bracket we were in.

Not that impressive when you have two people each making six figures and no kids. Your extreme budget is how many people live year in and year out even though they will be working full time for the rest of their lives

Lulu – I agree. Not that impressive. We were able to accomplish this much faster than many others making less income and with kids! I’m always amazed at those who make similar salaries to ours and still feel that they won’t be able to retire. Lifestyle inflation, I think.

This isn’t really inspiring. Inspiring would be if you had massive amounts of debt and started your career at an average income. Obviously if you make a lot of money and practice some basic budgeting you can save a lot in a short amount of time. Try starting out at 35000 with 40000 in debt living and working in a place where commuting without a car is not possible and living off $1500 or less each month including housing. In fact this article doesn’t even address student debt so it’s not applicable to most people. Really this post is just about how fortunate you have been in your lives. Not everyone is fortunate enough to have high paying jobs or even the opportunity to advance quickly, especially without relocating or leaving behind a significant other. And considering there there is only so much you can cut out of a budget this really isn’t feasible for the average graduate making an average salary.

Hi Amanda – we definitely didn’t have as many obstacles as some, which allowed us to get there quicker. It is still possible in the situation you describe, though. People are detailing their incredible debt-slashing stories all over the internet! Keep making smart choices and stay positive. If you really want it, you’ll get there!

This is really inspiring! We hope to do the same in a 10 years or so.

Thanks for sharing your story!

Thanks for reading our story, Mr. & Mrs. Dibidend!

This story is really awesome and inspiring! I’ve already started going through some of the other posts on your blog and am enjoying very much. Please keep sharing your adventures with your readers!

Thanks LeRainDrop! We’ve enjoyed seeing your new comments around our older blog posts!

I’m 28 and currently working an hourly job. I’ve been living this way for a while and recently woke up this year and decided I could live better. I’ve been reading books like Rich Dad, Poor Dad to open my mind to the possibilities. I don’t want to return to a 4 year schooling so I figured the only way to get higher pay without so many years of schooling is in the IT field…or coding, etc. This field is incredibly boring, I’m a very right brained artistic person but I feel this is the only way to make more. Do you guys think this is a smart idea? Sometimes we can’t see our lives from the outside in, so any input is helpful. Thanks!

You can give it a shot and see if your feelings change later, but the only ones I know who are super successful – either personally or business-wise – happen to love and believe in what they’re doing. You could probably make some $$ and do alright if you’re incredibly committed, but I’d keep looking around and see if anything more exciting to you pops. You usually need that to help get you through the first hard years of business/success!

Wow! Thanks for the share. As a 20-something this gives me some savings AND adventure ideas. Thanks you 2 (and Bruno!)

This isn’t applicable to very many people. The post title caught my eye, but once I read that you’ve never had to deal with a substantial amount of debt or any other financial setbacks, that automatically puts you twenty steps ahead of everyone else. In the end, all this post did was reiterate how wonderful it is to have a six digit income and never have to struggle to pay your bills, let alone save money. Lucky you. Unfortunately, your success story doesn’t apply to many of us college graduates with a large chunk of our measly income already claimed toward that education.

I agree, with this comment. My husband and I both have PhDs in our fields (still paying off student loans) and COMBINED income per year is 60k, I believe that is less than half of what you outline. What is outlined here is not that amazing. We have to cut all luxury from our life just to cover costs of our family (3 kids). I am not complaining, I love my life and my job so I don’t ever see myself quitting it, but the title of the blog is a bit misleading in that there aren’t really any ideas on how to save more if you actually are starting with a middle class income. Maybe if it had ideas on how to live on 20k a year it might be more applicable to middle class families. I guess that although my job pays considerably less, I do love going to work every day.

Yeah this post doesn’t really help anyone, most people don’t make over $100,000 a year to be able to save up $1mil that fast.

I’m trying to find a nice way to say this. You are the ones that pocked a field that apparently only nets you 30k after getting a PhD and at the same time had 3 kids. Seems like poor choices made this impossible for you.

I totally agree. You can make $30,000/yr at almost any entry level job without a college degree. I can’t imagine what field of study they are in where that is the most they can each gross with PhDs. I have an art degree and can make more than that.

May I ask what you do for healthcare? For many, that cost alone would blow a plan to retire early.

You mentioned living in a democratic country. Where did you live? America is a Constitutional Republic.

I drove with friends from Los Angeles to Panama taking about 6 months to complete. What an adventure. Fixed up a van to sleep in. Of course it was in 1967!

Too many comments to sift through so I apologize if this is a duplicate question… are kids in the future at all? If so would you still continue to live this way or settle for a while?

Cool for you guys but not really viable to many others. Most people don’t make over $100,000 a year.Of course it was easy for you guys to save up a million dollars that quick.

Guess none of us should try then :)

As soon as I saw they both grew up with wealthy families it all made sense. Some of us have to pay student loans.

Wow. It sucks that someone took out student loans in your name and you have to pay them back. Oh, or did you mean that you chose to borrow money and now have to pay it back? It is quite possible to go to college without student loans. Community college, work study, co-ops, etc. Granted, none of these are very glamorous and may involve going to a cheaper school, but it’s up to all of us to take responsibility for the choices we made. Maybe they came from wealthy families, but they also decided to major in well-paying fields (as opposed to something more “fun” or “interesting”) and cut their budget to the bone rather than living the type of lifestyle they could “afford” on their salaries.

It’s good living for healthy people though. I’ll be scared to run into health issues, costs of medicines etc.

I guess reality check will hit you whenever you decide to have kids and have to pay for those extra expenses, buying your own property to make worth living when you are old and at least have something of value, and losing the ability to continue getting professional experience in case you need to return to work to gain back some money because, $1 million won’t get you far. You guys are a young couple and 30 years from now you will be in your 60’s. That is still young now a days. A million $ would be worth nothing in 30 years from now and you would probably have spend it all by that time. Also, imagine what would happen if you guys are cough in some sort of an accident or get a weird condition that needs hospitalization? Do you have that budgeted? I bet this are things you have considered or at least thought about it with all your free time now.. I would like to know your comments about it.

Talk about motivation for a mid-week hump day! I celebrate that you pro-actively made choices about how to change your life to what YOU wanted it to be. You recognize the great start that your family and education gave you, but your actions and your choices led you to this great win.

Hats off to you for figuring it out way before I did!

Well that is just wonderful for this young couple.But this couple is not the the normal couple of today.Most young couples would be lucky to have 2 incomes at one time in a household.Majority of young couples don’t have a $100,000 yearly income no where near that,this couples yearly income was almost $200,000 average yearly income for a young couple if lucky maybe $45,000. Most are lucky to have one income coming in because the other spouse is at home with the kids because they didn’t wait to have children until they could afford children.

Sounds exciting! I am curious about insurance though. Do you have health insurance or are you covered by the universal healthcare system in Canada? Life insurance, car? Is all of this included in your spending? I agree with Norman. You may not need it now but when you’re 60 without work and your health begins to decline with age it will be difficult to find work if necessary. Living in the moment and enjoying life outside of a cubicle probably leads to a longer, healthier, happier life though. :)

Wish I could do something like this, but I’m in my 40’s and having to raise my 3 teenage boys on a single income. I can barely save a dime. I’m already a nurse and make as much money as I can, but the boys eat it all up. When they grow up however changes are coming because I can’t just keep working forever.

So cool! Inspired to see this happen so quickly. We are aiming for 40, so while we are relative slackers, we’re still doing okay. :)

I didn’t notice in the postings if you have health insurance. If not, getting sick can clean out your savings.

Love this! My question is, if you live at the low end of your budget (28,800) with the income you have saved (960,000), that would allow you to live at that rate for approximately 33 years. If you are 30 now, that only puts you in your mid 60’s. What’s the plan for after that? Also, what’s your strategy for health care?

Thanks for sharing!!

Yeah, very cool. Try to survive in Poland -$5000 a year, and you hardly cut the costs of your life…? Good luck…

I don’t know about u two, Life is about challenges, Roads to take and commitments, not being on vacation, always. Will see when u are almost 60, bored, no children to take pride off because u decided to go on vacation too early, maybe enjoyed too much ” cannabis” hopefuly you stay healthy and smart, Respect your desition, but absolutely don’t agree. I’ m almost 60 healthy with a wonderful family were money was not the priority, just the essential,, and live very well.

What makes you think money is the priority for them? They set themselves up to not have to worry about $$$ anymore :)

Ok J money, I have been were they’re are “vacationing”, in Central America on ” assignment”, beautiful , but extremely dangerous; Worries me about the cannabis thing, in that area. Is naive to think they’re not going unnoticed on a vehicle with foreign lic plates and of course, sharing their a complishments. Poverty and ignorance flourishes everywhere down there and also envy and violence. I wish them luck, for their car not to break in the wrong place, for them not have to be airlifted for proper medical care, for a ransom not to family, for…..

Amazing how a posting like this gets encouragement from complete strangers thinking their accomplishment is cool, lets see how they help when sh. hits the fan if they still post their problems, wake up people, it’s the journey, not the finish line.

Don’t get me wrong, what they accomplished is very good, but the accomplishment is not to get there, is how to stay there for the next 40-50 years. We are living longer than 60 years.

Diversify in other things in property to produce an income, but your money somewhere being handled by who, , depending on what? mmmmm, no thanks.

They seem to be doing well so far :) It’s not like you can’t change and adapt as time goes on either right? If you’re smart enough to amass that much money and create freedom for yourself, you’re smart enough to keep it going as the years change.

I am retired and have been for almost 2 years and I am 34 years old and have 4 kids so that makes travel more difficult but I am blessed to get to choose my life and even made it to where my husband doesn’t have to work . Being able to make choices based on things other than how your going to pay the bills is such a huge relief that I hope everyone gets chance to live more free .

Beautiful!! Love to hear it! Especially with 4 kids, wow… I’ll stop bitching about how it’s hard for me with only two, haha…

Yeah, all you have to do is earn a joint $177K without any student debt…hardly something that “just anyone” can do. Oh, wait, I guess Canadians don’t have student debt.

By the way, since neither of you has worked 10 years, neither of you will qualify for Social Security.

If the Obamacare law goes away (the dream of the GOP), and if either of you gets a pre-existing condition, how will you get medical insurance?

This is about the biggest BS story I have ever read.

Haha… why do you say that? Don’t believe it’s possible? Or don’t believe them?

Amazing story but that can not apply in Africa

What kind of account do you have your portfolio in? Is there any penalty for taking money out of it?