Happy 401(k) Day, everyone!

Yup, it’s a real day, and one of real importance too! Given that the bulk of American’s money is totally invested in their 401(k)s and respective counterparts. Trillions and trillions of it! (Don’t quote me on that one as I’m too lazy to research it right now, but I do know it’s a lot! ;))

So before we get to today’s goodness, make sure that the following two things are in place w/ yours:

A) That you’re getting 100% of your FREE MATCHING from your employer because it’s FREE MONEY!! Which is better than NO FREE MONEY, and especially when you don’t even notice the difference of it being deducted from your paycheck!

And B) That the money that’s sitting there is actually invested into something smart, and not ridiculous like cash or other “investments” that are sucking out your money in fees vs compounding it for you. Check out Blooom.com if you don’t even know where to start and they’ll literally log in for you and analyze/move your $$$ around where it makes better sense for you and your goals. They’re awesome, and you can find my mini-review of them here. [The link to Blooom is an affiliate link as we’re partners]

Now with that PSA out of the way, I’ve got a “Would You Rather” for you!

We haven’t done one of these in forever, and thought it would be fun to compare YOUR answers here with the ones we got when we interviewed over 200 financial bloggers for a new project over at Rockstar Finance we just launched (details in a bit).

Here’s the question below. Give it some good thinking, and then leave your answer below in the comments so we can all ogle at. It’s harder than it first seems!

“Would you rather….

Have all the knowledge from every financial book in the world

– OR –

Get $100,000 in cash money?”

Now remember, think on it for a bit before going with your gut answer! What could you do with all that knowledge?? What could you do with all that cash? Does going after one get you closer to getting the other one too? Are they both equally as important?

I initially chose “all the knowledge” myself, because of course you can then turn that knowledge into even more cash money over time, so long as you take action, but after sitting on it for a few I ended up changing my mind on it and here’s why:

If I had all the knowledge from the books I wouldn’t have a reason to read any more! Which is half the fun! And plus, $100k compounding right now means a handful more years closer to early retirement where I can then – wait for it – read more finance books! (BAM!)

Now of course, this is *current* me and not *old* me when I didn’t have 1/100th of the knowledge I do now on money, so our own journeys certainly play their part here.

Either way, mull it over for a bit as you read the next batch of words I type into the computer here, and then come back and leave your answers down below in the comments :)

Our New Rockstar Project: A Crowdsourced Report (and Directory!) of The Best and Worst Personal Finance Books as Rated by 200+ Bloggers!

Some of you may have already seen this if you’re a fellow blogger and/or follower of my sister site RockstarFinance.com (where we do a lot of curation and collaboration), but basically this week we finally launched a project I was DYING to get out and was super proud of in doing so :)

After letting the words from that killer book, Essentialism, seep in for a while, an idea finally clicked on how I could use my one unique “super power,” as they say, to really do something cool in the space. And not only cool, but also HELPFUL for our entire community!

And that was harnessing the collective minds of the financial blogging community to pump out insight on one targeted financial topic each and every month, to give us a SOLID resource from people who love and obsess about this stuff the most.

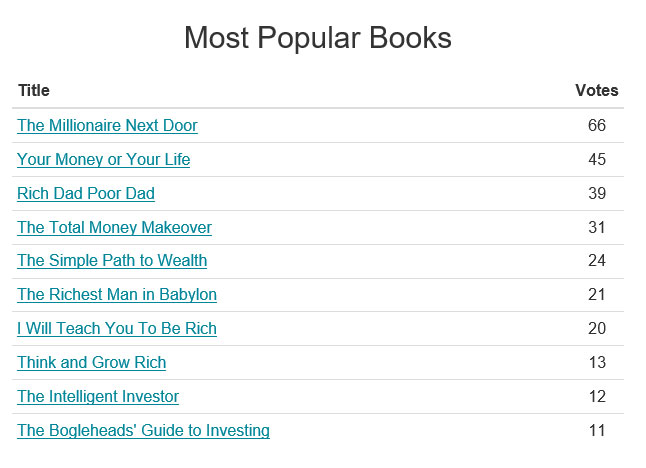

And we kick-started it with a report on the best, and most overrated, BOOKS on personal finance, as well a slew of other interesting nuggets such as that Would You Rather above as to not turn it into a snooze-fest ;) You can see a sneak peek of the report here before you click over:

But here’s the second cool thing that came out of it all – not only do we now have this nifty report to scan through, but it also gave us the ability to build out a new directory of BOOKS to compliment our Blogger directory too! So now EVERYONE can access this collective mind-meld of recommendations to better help them in their journey towards financial knowledge. Win-win all around!

So all that said, here are the two places you can now visit anytime you’re looking for a great new finance book to pick up (or ignore – hah!):

- Our new directory of the best finance books!

- Our in-depth report of all the polling data after interviewing over 200 bloggers

And again – that’s just month #1 :)

We’re already in the works of building out the next report and directory based on another focused category, and our goal here is to continue producing these 1-2 punches monthly until we either cross them all off, or more possibly bloggers get tired of answering all our questions, haha…

In either case, I’m thrilled with how our first run went, and I thank EACH AND EVERY ONE of you who participated and made this fun little idea a reality!

Getting this new project off the ground was just the burst I needed to feel energized again, so I thank you all mucho from the bottom of my heart and can’t wait to do more :)

Please enjoy your weekends out there, and we’ll see you back here on Monday for another riveting discussion on money, money, moneyyyyy!

XOXO,

![]()

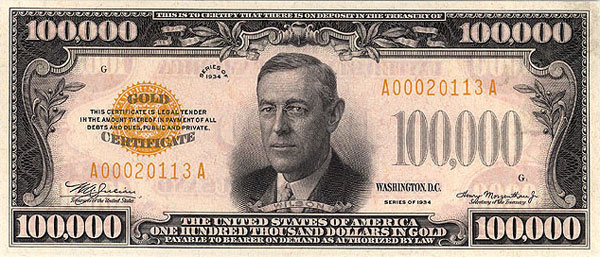

PS: Just like 401(k) Day, that $100,000 note above is also real! It’s a $100,000 gold certificate that was used for government inter-agency transactions back in the day and since retired, bearing the mug of one handsome Woodrow Wilson. It’s also very illegal to own in a personal collection (it was never meant for the public), so if you ever see one in real life it’s either fake or you’re hanging with the mafia :) You can visit one at the National Museum of American History though!

Get blog posts automatically emailed to you!

That’s a good would you rather. Where I’m at right now, I feel like either would be super helpful. But I think I’d rather have the knowledge. I don’t have the knowledge base that many other Financial bloggers do, and I think it would be more useful to us to have that than the money. The money would be so awesome, but I am going to say that knowledge.

Also, I’m really interested in checking out this book collection. We’re always looking for another good book!!

Good! There were a handful of books I’d never heard of that popped up on people’s favorites, so I think everyone will find at least one new book to check out :)

As always enjoy the historical bill topics. Any more info on other interagency denominations? I’m in the bloggers who were surveyed so I’ll let my answer re knowledge stand on it’s own.

And we thank you kindly for that!

Bills – oh yeah, there were a handful of other larger denominations that have since been discontinued:

$500 bills

$1,000 bills

$5,000 bills

$10,000 bills

$100,000 bills

Most stopped due to security reasons, as well as changes with how banks handle money (especially once computers and then later internet came around (everything’s digital now!)

You can see a lot of the cool pics on how they looked on the Wikipedia page: https://en.wikipedia.org/wiki/Large_denominations_of_United_States_currency

This one is easy J$ — I’d take the knowledge over the money. I’ve already read a good number of the books in your directory, but more knowledge is a good thing.

That, and $100k would only make a little bump in my net worth… nothing to get too excited about. If this was a sum of $1 million or $10 million I’d need to be a lot more careful in my consideration.

Interestingly enough, the books in your directory look nothing like the books on my list. ;)

We’d make an interesting date, then ;)

Ooohhh interesting tidbit on the bill. Happy 401K to you too — I felt a bit embarrassed when I answered “all the knowledge” instead of “take the $100K” when so many bloggers said $100K. I have similar reasons as Mr. Tako. I’m thinking I can make more than $100K in my lifetime with that knowledge.

You shouldn’t feel embarrassed at all!

51% of the bloggers picked All the knowledge compared to 49% of the Money!

http://rockstarfinance.com/best-finance-books-poll-results/

You are in the majority :)

The guy with the most knowledge on my team at work was just lured away to another company. He was kind enough to share the details of the offer. $165,000 annually. And he didn’t have anywhere near all the knowledge, but he had a lot! So, assuming this knowledge includes the world of IT and is in depth and multifaceted, and you are able to actually utilize it to solve problems, make plans… On could make that 100,000 back in short order!

Haha, no that is not included in this mystical poll :)

Only all knowledge from *finance books*, else no way anyone would choose the $100k! Would have to be at least $1,000,000 for that side to be continued I’d think.

Oh, that’s what the $$$ part meant, financial? Oh darn, I was thinking all knowledge from all books ever, like how to do surgery and repair all cars and never got lost and, well, everything.

Then the $100k. I don’t know everything, but I know enough by now, I’ll take the cash.

I originally opted for the books, but after reading your insight and being the frugal person I am, I can invest the $100k and borrow the books from the library or buy them used online.

If I didn’t handle the many effectively (aka buying a Corvette), I would opt for the books first.

Being the main $$ gal at work, I preach the “free money” mantra to all our employees – it can be an 80% return on your money!!! And I have The Millionaire Next Door but need to reread it since it’s been awhile.

I would take the $100k. Not too many years left to work (FIRE wasn’t a thing when I was *ahem* young) so I’d throw it in my retirement account & let it grow until I needed it.

Interesting insight with the stage of life there – I like it :)

Without the books I wouldn’t have the 100k I have now :) – so they have to get my vote

Happy 501k to you too! I loved your intro. Very funny!

I would choose $100k in a heartbeat! Reading is great, and books are valuable. But after being in school for 22 years, I’m just ready to get out there and get some practice. I can picture LOTS of things I can do with that $100k. :D

Oh yeah, gotta have the action or all that knowledge is worthless!

At this point, I’d rather have the cash, because I could pay off the student loans and credit card debt I accumulated when I wasn’t as knowledgeable about personal finance and invest/save the rest. I have a lot of resources at my disposal to learn more about finances, but the cash at hand could get me completely debt free, save me loads of interest (let’s be real, I can only pay off debt so fast on a librarian salary, though I love what I do), and free up more disposable income to save/invest. Being debt free would be a huge burden lifted from my shoulders.

Great points all around!

It’s not like you can’t still read a book if you choose the $100k :)

As a librarian you’ll appreciate this post a rare book buddy of mine put together:

Definitive List of the Top 10 Libraries In The Fictional Universe

I’d take the $100,000. I already have, and have read most of the books on the list. I have an MBA too. Our personal investment portfolio is north of $4,000,000. In one of our businesses (mortgage lending) we have earned more than 12% on a compound annual basis for over 25 years (in worst year ever we made 5.6% and that year we quit lending in April because of changes to the Income Tax Act). So I’d take the $100,000 and plonk it into our mortgage business.

As far as books go, it’s “The Millionaire Next Door” that I find most inspiring. It clarified my thinking (I’d made my first million by the time I discovered the book) and really allowed me to examine my many failures (nearly all of the crap that has been mentioned in your blog I have been guilty of) and what caused the reversal of my failures). R.I. P. Tom Stanley – your book was a real inspiration to me.

Amen, man… one of the most influential books on money there is.

I would take the money. I’m FIREd and I’ve already read many PF books.

I still read new books but as my latest post describes I always get books from the library. :

The answer to this question really depends on where you are in life and what your financial discipline is. If you obtained all the knowledge in the world, but you don’t have the discipline and motivation to use them, then those knowledge are wasted. It you get the $100,000 and you don’t invest it, instead you spend it all, then it’s also a waste of your free opportunity.

For me, I don’t need to make a choice, I will try to obtain both. I already got my $100,000. I am now using the knowledge that I obtained to multiply that money further. Just have to multiply it another eight times.

You know what they say, the first $100,000 is the hardest!

https://budgetsaresexy.com/the-first-100-thousand-is-the-hardest/

As others have written, without those books, I would have what I have today. Since I read most of them already, I will take the $100k.

Great job on the list and on-going projects!

Was just in the American History Museum a couple weeks ago and didn’t look for/see the bill. I will need to next time!!!

Oh man! We probably cross paths down there! I took the kids to the Air & Space and another one but didn’t have time for American History on that trip either…

The bill is within the National Numismatic Collection inside there where all the rare coins are too, *drool*..

I took the cash… I feel like I’d get overwhelmed with the knowledge, but I know enough right now to make wise choices with a $100K windfall!

Knowledge for sure but hopefully going beyond just financial concepts. 100k while a lot of money, won’t move the needle like it used to.

I would take the knowledge, hands down. I’ve read many financial books, but I couldn’t get through some of them. Some are too technical and some are too boring. Analyzing stock for example is still very difficult for me. If I can magically know how to do that better, then it’s worth much more than $100,000. That’s just one thing.

Reading a book doesn’t mean understanding the concept completely. I really need to go back and read some of these books again.

Good point on it all soaking in like that… I still love and choose Millionaire Next Door as my favorite book, but I couldn’t tell you all the interesting facts from it without picking it up again. I feel like as long as you can get the *essence* of them though you’re good. Except for stock technicals haha.. that’s a whole other ballgame, and one I’m fine without knowing :)

$100K because if you have read 3-5 PF books you pretty much have read them all anyway. The 3 I thought were good are Your Money or Your Life, Early Retirement Extreme, and Simple Path to Wealth.

Your Money or Your Life is the one that had the most impact on me. I think It was the truth of the message coupled with where I was at mentally and financially when I first read it.

I can see that… I think most people go with one of their first books read too as their favorites because it’s at the point you know the least so it has such a bigger impact on you.

I’d pick the knowledge for sure. Having all that info is probably worth millions. Think about all the time saved too, that alone may be worth $100K. Love the idea of polling personal finance bloggers! If you need another one, let me know.

I would say all the knowledge. The answer is based on how long it takes to make more thank $100k. I feel that with additional knowledge it would be possible to make more than $100k very quickly. However if I was to take the lump sum $100k inwould invest it the same way I do now and it would end up taking years to double. With additional knowledge I would end up doing even better.

I’d take the $100,000 since I’m close to retirement and that much money would reduce the time I need to work, giving me all the time I need to read some of those books on the list (and a mystery or two as well) that I haven’t had time to get to.

I remember going to Vegas years ago and Binions Casino had a million dollars in a cube of large denomination bills. I think they may have been thousand dollar notes but I’m not sure. I thought it was an awful lot of money back then but now it’s less than my goal for retirement. Just shows the impact of inflation over the years

Yeah!!! I remember that! Inflation or not though, a million dollars is still a million dollars :)

J$,

What an Interesting way to frame the question.

Are you implying that all the knowledge in the world is only worth $100,000 ;-)

Either way, I would say that investing in knowledge is more important than a lump sum of cash to me. Are you familiar with Charlie Munger, who says this:

““In my whole life, I have known no wise people (over a broad subject matter area) who didn’t read all the time — none, zero. You’d be amazed at how much Warren reads–and at how much I read. My children laugh at me. They think I’m a book with a couple of legs sticking out.””

“They think I’m a book with a couple of legs sticking out.”

HILARIOUS.

I’d choose the knowledge. But that may be because I’m out of debt and have a solid cushion. These days I read for fun, so having knowledge wouldn’t mean I had already read the newest chick lit book or sci fi.

The one downside reading for knowledge is that one would find it fairly haunting. I’ve read enough about the Khmer Rouge to know that a whole book on the topic would give me nightmares. Imagine having every book ever written on the Khmer Rouge in your head. And Congo atrocities. And the Boer War. And Nazi war experiments. And Japanese torture of pretty much all of Asia. Yikes. (Clearly I’m already haunted by the stuff I already know about).

Sorry to go all dark there. I’m worried about Irma so my thoughts are a bit negative. Feel free to delete my comment!

Ah, it was just finance knowledge, not all knowledge. My bad! I’d take the money.

Oh wow! Dark, yes, but that is an interesting thing to consider!! And not one that most would, haha… Kinda like if you could hear what other people were thinking too, especially about you. It would be fun for probably a day, and then just be way too much afterwards :)

I would take the money right now. I have enough knowledge to make some great choices with it. Pay off the smaller student loan and all CC debt. Fully fund EF and the rest would be a down payment on a tiny condo, because with one student loan paid off my DTI would be in a range that felt healthy to me. The condo size I want would allow for a mortgage that is less than my current rent. I could permanently reduce my expenses and go back to having a bathroom I shared with no one that I didn’t love.

I’ve been liking that answer from people – “I have enough knowledge right now” to be able to make decisions. Sometimes people think and learn *too much* before getting out there and making moves in the real world. So I’m glad you recognize you’re in a position to feel confident with taking action :)

I took the money. I’ve already read a lot, would continue to read more and would grow the money. I enjoy money but there are other things I’d rather have all the knowledge about.

$100K…It would help me towards my goals of being debt free…in fact, when I received a signing bonus from my new job (not quite 100k but a pretty good sum of money), I swiftly paid off my wife student loans that were sitting at 6% interest.

As for knowledge, for us reading your blog we will seek it. For the lottery winner who never cared about money, maybe knowledge would be a good place to start.

Your wife married a nice husband!!

Are we supposed to assume that all the knowledge that were written are true? False knowledge is more dangerous than not knowing at all. I’m changing my answer. Give me my $100,000. :)

HAH! That’s the gamble you have to be willing to take ;)

I would put it into Blue chip stock through a TFSA account. whyich I have done already as I am allready retired,

Hey J.money how are you today? This is a fantastic article and it was very interesting to think about what I would do. Personally I feel the knowledge I would gain from all the books would make me way more than $100,000. Everyday in my business I seek knowledge to better that business and this increase my income ten fold! Knowledge is power :) Have a great day!

I’d take the $100K! After all, isn’t investing and getting to FIRE supposed to be simple? “Shockingly Simple Math…” “Simple Path to Wealth…” I don’t know if you need *ALL* that knowledge, just index funds and time!

Love that you polled all the bloggers about the books! I haven’t read most of them, but I love Jim Collins, so his book gets my vote. I think most of us are already well on our way to FI here… MY question to bloggers about books is: Which book do you think would be best to give to an 18 year old to get them started on the right path? Which book would hold their attention the most at that age and stick with them?

I would go for Ramit’s I Will Teach You To Be Rich if they like to be entertained a bit while reading, or David Bach’s Automatic Millionaire if they just want to get in and learn and then start *taking action*. Although both books give specific tasks to get you going which is nice.

I’d take the $100,000. I know what that is and how it works, and can use it. I love reading and books, but they don’t give me ability and they can’t tell how to get the instinct(s) of *how things work*. I do have some of those, and applying them maximizes the value of that $100,000.

I’d take the $100,000 because I already have enough knowledge to not completely waste it. I would use it to pay off debt and invest. I can always read more books and redirect the money as I learn.

100% knowledge from books! It would be like being the finance equivalent of dude from the film/book Limitless!

While I do enjoy reading about financial issues there are also a million other topics which I’d like to read around as well. So it would be nice to just instantly knock off the finance category in one hit like that.

Also there are always new developments so you could still read finance blogs to keep up to date ;)

Good points all around :)

I would definitely take the knowledge. I am a nerd. I like knowledge more than money. And I could then turn my attention to other things to read, use the knowledge I have learned to earn more money, and pursue other interests as well.

The $100K so I could pay off my grad school loans, as well as the rest of my degree, and invest the rest.

Put me in the $100,000 camp.

All that knowledge sounds great but its kind of redundant at some point. You don’t need to know EVERYTHING to manage your finances half decently. You just have to know enough. In my opinion the average person could read 5-10 good personal finance books and be well on their way to a better financial life (assuming they put that knowledge into action, which is a whole other issue entirely).

“You don’t need to know EVERYTHING to manage your finances half decently. You just have to know enough.”

Excellently said.

The answer is simple for me – knowledge. The knowledge will multiply the $100k to any number I want