Well this was a much less exciting month!

And I’ll take it every time, haha…. (SlowAndSteadyIsSexy.com!)

Good to see all those reds turning back to greens though after last month’s blood bath, and now if we can only find an extra $50,000 laying around we’ll be fully caught up ;)

But that’s the way the game goes right? Can’t be UPS all the time, so if you can’t stand the heat gotta get yourself out the kitchen!

And then find a different room to hang out in instead, like perhaps the bathroom or the garage ;)

Not everyone loves or believes in the stock market, but fortunately there are plenty of other avenues that’ll still get you to the Freedom Finish Line all the same… Just keep experimenting and narrowing it down until you find the one that fits, and then POUR ON THAT GAS!!!

******

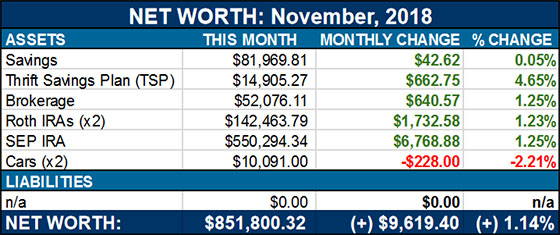

Here’s Net Worth Report #130: $851,800.32

[NOTE: These reports are shared to better start discussions around money and to showcase a *real life* snapshot of someone’s finances. Mine ;) Some months we’re up, and others we’re down, but it all gets displayed in hopes it helps you along your own journey and gives you a little more perspective on stuff. Thank you to all those who have been around from the beginning over 10 years ago!]

******

CASH SAVINGS (+$42.62): BOOM! Who wants to go clubbing???? That’ll get you at least a couple Long Island Iced Teas and some late-night pizza ;) (TRUE STORY: I once dropped $20 for a drink in a swanky New York club, and then had to wait a few days until payday as it was the last I had. #Priorities)

THRIFT SAVINGS PLAN (TSP) (+$662.75): Now we’re talking! The wife’s automatic deposits are back to kicking again, and all is good in the government world. One of the only things these days, it seems!

BROKERAGE (+$640.57): A nice little bump here too, and all better than it was sitting in a savings account for however long it did until I finally owned up and moved it ;) It’s nice to finally have an investment account I can tap if I ever wanted to too, without having to worry about early-withdrawal penalties!

ROTH IRAs (+$1,732.58): Back on the up and up again – even though we haven’t funded it for a matter of months (we wait until the end of the year to do it so I don’t F it up again).

SEP IRA (+$6,768.88): Similar territory here too! At the whims of the market until we do a little maxing out action at the beginning of every year… Though these days you don’t even see the deposits hit since it fluctuates so wildly every month! But we keep diligently filling it up!

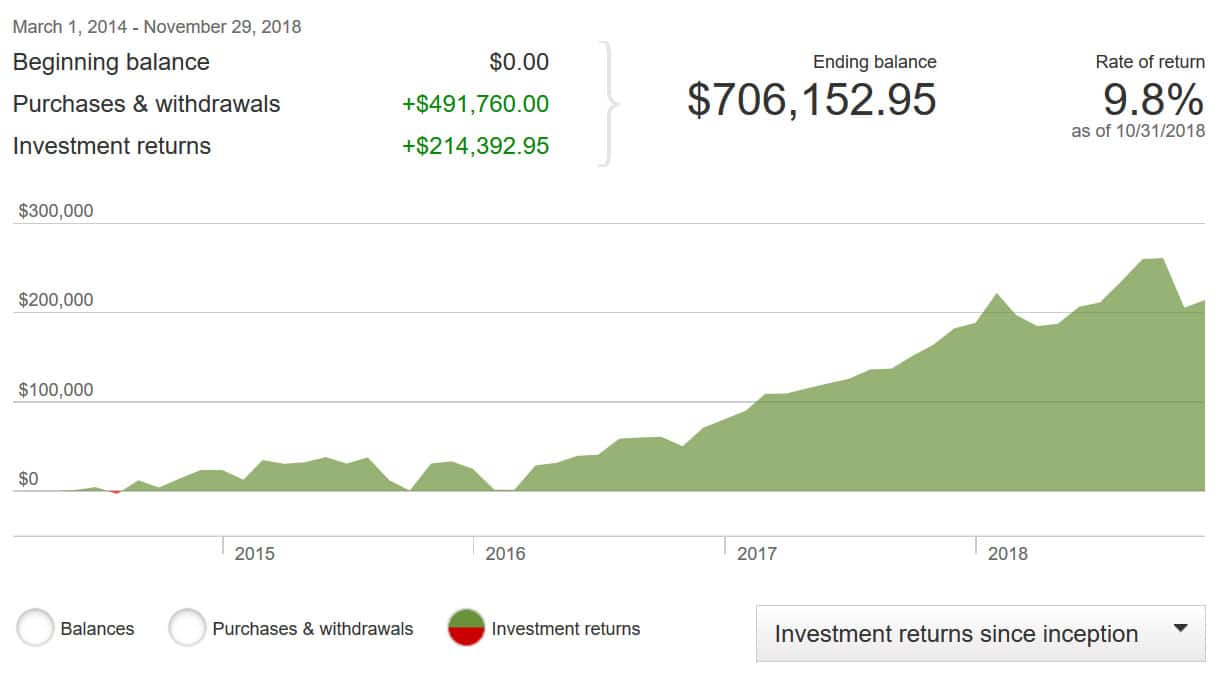

Here’s how it’s performed since we switched to Vanguard indexing a few years ago. You’ll see a number of dips in there, but the jumps are even greater!

CAR VALUES (-$228.00): Finally, the cars… that will always go down, unless you’ve figured out a way to reverse the odometer (legally!). Here are the values of both our paid off cars via KBB:

- Lexus RX350: $7,791.00

- Toyota Corolla: $2,300.00

Total change in net worth this month: (+) $9,619.40

Another month down on the books! If you’re itching to see all 129 reports prior to this one, feast your eyes here: My Net Worth Over The Past 10 Years

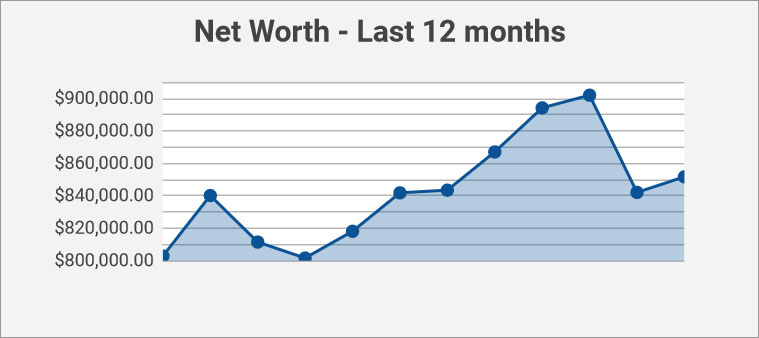

And then here’s how the last 12 months have gone to put things in more perspective:

Lastly, our kids’ net worths…

Baby Dime got baptized over the month, and for the first time in his – and our! – life, we got a check to go into his college savings account instead of a toy!! It was a Thanksgiving miracle!! ;)

[Socks or food, it’s all the same…]

And back to the grind we go! How’d you guys do this month? Any Thanksgiving miracles with your wealth?

Some quick tools can be found below if you’re new to this stuff, but however you play it, just make sure you’re indeed PLAYING IT!! Can’t win the game of life by sitting on the sidelines, so come out and get dirty with us!

Your friend in filth,

![]()

PS: If you’re just getting started in your journey, here are a few good resources to help track your money. Doesn’t matter which route you go, just that it ends up sticking!

- The "Budget/Net Worth" spreadsheet - the colorful Excel template I personally use.

- The "Money Snapshot" spreadsheet - a simple Excel template I created for my former $$$ clients

If you're not a spreadsheet guy like me and prefer something more automated (which is fine, whatever gets you to take action!), you can try your hand with a free Empower account instead (formerly Personal Capital)

Empower is a cool tool that connects with your bank & investment accounts to give you an automated way to track your net worth. You'll get a crystal clear picture of how your spending and investments affect your financial goals (early retirement?), and it's super easy to use.

It only takes a couple minutes to set up and you can grab your free account here. They also do a lot of other cool stuff as well which my early retired friend Justin covers in our full review of Empower - check it out here: Why I Use Empower Almost Every Single Day.

Get blog posts automatically emailed to you!

Time to replace that turkey in your logo with Mr. Grinch! Ha!!

Always love your report outs. I’m too chicken to share my deets like this. I’m guessing you keep any blog earning separate from the net worth calcs?

Oh yeah – gotta swap in my Xmas logo, thx!

Blog earnings – they all go into these reports :) I consider them my “paychecks” so you’ll always find them here. The only thing that’s not included is the value of my blog as an *asset*, just cuz it’s somewhat unpredictable and I’d rather count it as a nice “extra” on the day I ever cash out ;) So if you ever see a huge influx come in during one of these reports, you’ll know what happened! Haha…

Did you ever have any hesitation about sharing your financial details?

I did in the beginning, but after the first few months it wore off :) Plus – it helps being more anonymous online which is why I share it so openly (as well as other things).

I’m too chicken to share the details too! Other than we are minimal millionaires. Do you think you will ever change your mind?

I love reading these every month, and it’s amazing to look back at the progress through time. It’s also crazy to see how the Lexus value has halved since you bought it! Doesn’t seem like that long ago, either. Not judging, just observing how quickly that happens with cars. It’s no wonder so many people struggle to get ahead…

Wow – I’ve never noticed that! I do grade it super conservatively when running these reports, but even so I’ve only owned it for 2-3 years!

So close to $1M! Next year sounds like it will be the year!

Curious if you could tell me the reason you went with a SEP IRA instead of a i401k? Did the pros and cons list (with a post to come out soon about SEP vs i401k) and the i401k won out in my analysis. Wondering what I am missing before I go off and create it for this/next years side hustle earnings.

You’re probably not missing anything :) It’s been 9 years since I last looked into it and at the time the SEP made the most sense for me per my Accountant, but I’ve honestly not looked into it much since. I’m such a bad $$$ blogger, haha…

J, you’re probably right in that when you opened your SEP it was the best way to go. Today though, SEP has no advantages over i401k. You have to make more (using SEP) to contribute the same amount. Only reason to use SEP is if you have employees. i401k is only good for person + spouse companies. That being said you can get around this by 1099ing everyone who does work for you.

Thanks for the insight!

I’m loving the look of all that green!

Looking good! Great job with the kids’ college savings. They’ll thank you later.

Our November wasn’t too bad. It was better than October, for sure. Our net worth is up just a little this year. I supposed that’s better than being in the red.

For Olivia above, I’m using i401k. I think the overhead cost is a little bit more. The advantage with the i401k is that you can save much more. Oh, maybe J rolled over his old plan into a SEP IRA. I don’t think you can do that with the i401k, not sure…

I did actually roll over my old 401k into my SEP! Though I think I did that later after I was already going strong with it…

I have heard other routes let you save much more than a SEP for sure, but since I can’t really save more than I already am currently it hasn’t been that much of an issue for us :)

I set out at the beginning of the year hoping to get to half a million. Now it’s looking like it’ll be closer to $475,000. Fortunately, in the big months where the market was down, I was putting in enough to stay even. So, I’ve been treading water waiting for things to turn around.

Here’s to both of us hitting our milestones before it crashes for the longer term :)

That is going to be a sad day! But it will come back, right?

As long as you’re patient enough :)

Slow and steady IS sexy!

I prefer “slow n’ steady gettin’ dividend heavy”, but slow is still sexy.

Congrats on the great progress!

-Mike

Haha… that works too :)

Nice rebound! After a tough October it’s great seeing all that green again :)

My parents will always get me some kind of birthday gift every year but I’ve recently requested that instead of a gift they just put the value of whatever they were going to spend instead into a savings account for any future kids I may have! Hopefully they oblige and that way they have a good head start!

Oh I can do you one better than your $20 drink story. When we were young parents, I’m talking two baby girls (well okay they were 20 months apart) by the time we were 23 and 24, we used to routinely spend our last $20 before payday on breakfast out on the weekend! I cannot tell you how many times we did that. We were ridiculous! Of course the fact my parents had allowed us to live in the dumpy little house I grew up in helped us to have a false sense of security. We both worked and I went back to work full-time when daughter #2 was a year old. We were $4000 away from having over an acre of a beautiful land paid for in full and my husband had our house plans drawn, when on my 29th birthday when the girls were in kindergarten and first grade (December 22) I found out I was unexpectedly pregnant again! So we sold the property and bought a 4 bedroom ranch style house. Daughter #3 was born 2 weeks after we moved in. The house I grew up in was on it’s last legs. My mom had a house built on the adjoining lot and donated the house we had lived in for 7 years rent free (enabling us to buy that property) to the local fire department for a training exercise! Good times, good times…..

Slow and steady is equally sexy! Your kid is adorable.

Thanks, D$!

Gotta love these green months.

We ended up 0.92% in November.

The biggest news we had this last month was getting rid of a car payment! So we’re car payment free for the first time in 8 years!

That’s gotta feel good!

Nice! You’re almost there, J Money Millionaire! I love the transparency of posting these, but like Cubert, I’m a little nervous to share this type of info.

All good, brother! What’s important is that you’re tracking it in general – not that you share it with the world ;)