Time for ye ol’ net worth updating again!

And just like last month, it was a pretty juicy one for us this time around too – only much more fun than making IRA mistakes and playing the bitcoin game ;)

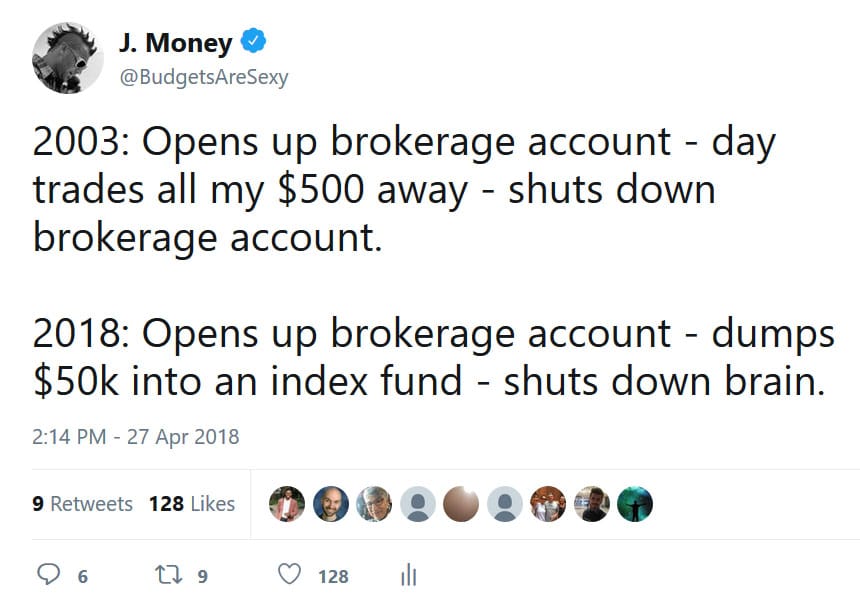

For the first time in 15 years, we finally have a traditional brokerage account again! WOO!! And what a difference all those years have made with our mindset:

(Of course I had to tweet it in real-time as blogging is too slow these days ;) So be sure you’re following me to get up-to-the-minute news and nonsense! –> @BudgetsAreSexy)

So yeah – dropped $50k right into it last week, and you can probably guess where it all went ;) I’ll give you a clue – it rhymes with Wanguard, and it got invested into Mindex funds, haha…

So why now? Three reasons:

- We finally had enough of staring at all our extra cash reserves, and it was beginning to feel unproductive

- We couldn’t use it to max out our Roth IRAs this year because of our higher incomes

- It was finally time to DIVERSIFY our tax advantaged accounts more, because it’s probably not a good idea to have 100% of your investments locked away in them… at least if you truly want to “retire early” one day :) (Though of course, you still have Conversion Ladders and other strategies you can utilize – which I refer to Mad Fientist on, who’s a master at this: How to Access Retirement Funds Early)

And of course because I’m obsessed with index funds, we poured it all into VTSAX which required zero ounces of thought – as designed.

I’ll probably use this account to tweak holdings over time and maybe diversify our index funds as well (you know, with bonds, international, etc), but for now we got it going, so I’m calling it a win in the “more well-rounded” department. Which only took us 15 years to get comfortable with again ;)

(And to be honest, I’m still a bit nervous about it, which is strange since we have over 10x this amount in our retirement accounts which are invested in the EXACT SAME FUND??, but I’m chalking it up to just being new and different for us, so hopefully it all subsides… We can always cash it back out whenever we want/need it, right? With much less hubbub?)

At any rate, that’s the major news over here this month! No baby yet, but should be any day/hour/minute now! It’s gotta come out some time, right??

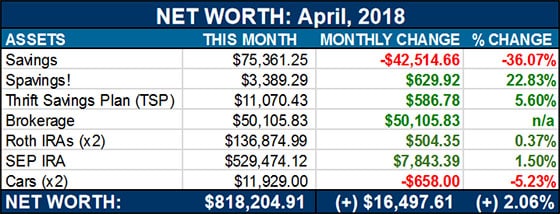

Here’s How April’s Money Broke Down:

[These reports are shared every month to keep things transparent, and to start great conversations around money in our lives. Sometimes we’re up, and sometimes we’re down, but whatever the case, we disclose it all and hopes it helps with your journey too. Welcome to net worth update #124!]

CASH SAVINGS (-$42,514.66): A big drop as we move out a chunk of cash into the new brokerage account just mentioned, as well as another clump into my SEP IRA to max it out for the year. Which thankfully we *were* able to do unlike our Roth IRAs because we earned “too much” last year – womp womp… We also got a decent amount back during tax filing too, which is why we only went down $40,000 here instead of $60,000.

SPAVINGS FUND! (+$629.92): Another great increase this month! This time due to cash back rewards with our USAA credit card, cancellation of our HBO subscription which now nets us $15.00/month (though very tempted to go back with the premiere of West World again!!), some reimbursements checks, and a bunch of other smaller cash findings we quickly stashed before it all went out the door again… Because as the saying goes, “if it’s not saved, it’s spent!” And if that’s not a saying yet, well, we’re making it one today! Spread it far and wide, people!!

(More info on the “Spavings” idea here)

THRIFT SAVINGS PLAN (TSP) (+$586.78): Up and up it goes, the more my wife works! And the beauty of 9-5s is that it should continue to do so even while NOT working and on maternity leave, due to using up vacation and sick days and what not. Benefits us self-employed schmucks lose out on ;) So yay for employers! They’re not always so horrible!

*NEW* BROKERAGE! (+$50,105.83): Best fake increase right there, haha…. Though we have already earned $105 since dumping our money in – much more than the $0.05 we would have leaving it in the savings account :) Of course, we still have a healthy chunk there for emergencies and other future opportunities, but it’s always a balancing act with this stuff, and you do your best to align everything with your goals and comfort levels… Not every last dollar needs to be optimized, but you do want it to be a *conscious* choice that best fits your lifestyle!

ROTH IRAs (+$504.35): Another nice uptick here as well! With obviously no deposits on our end as we were so rudely denied from investing in these for the tax year ;)

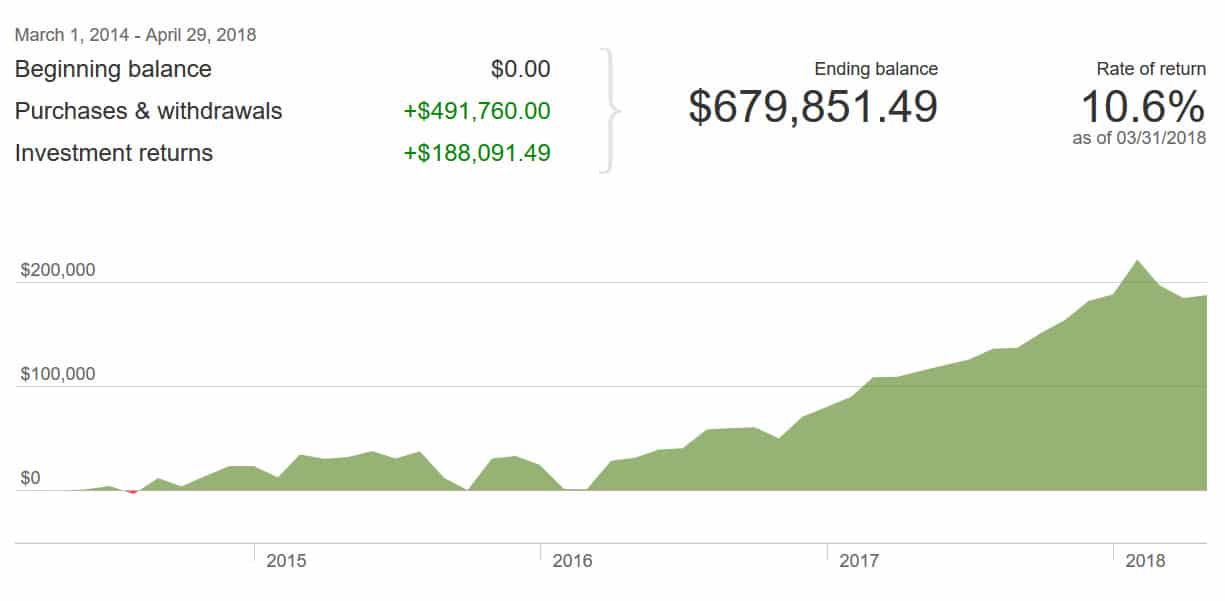

SEP IRA (+$7,843.39): A bit better here as we maxed out our account for the year, but we’ll see what the market has in store for us with all these ups and downs going on… Here’s a snapshot of how our Vanguard accounts have progressed since switching over to them close to four years ago:

(Just like with our new brokerage account, all money here is invested in VTSAX as well – Vanguard’s “Total Stock Market Index Fund” – Admiral Shares version (fewer fees, but you need at least $10,000 invested to move into, vs their “Investor Shares” account (VTSMX) which only requires $3,000))

CAR VALUES (-$658.00): Nothing too crazy going on here, other than we lowered our “condition” a bit for each car just to stay more conservative… OH! And we decided to wait on our minivan too until my wife’s car dies out! Turns out we can (barely) squeeze three car seats into my SUV, so for now we’re going that route until absolutely necessary :) The thought of car shopping with a newborn is just not exciting at ALL right now, haha… Or apparently the 9 months leading up to now either!

Here’s the value of our two cars per KBB.com:

- Lexus RX350: $9,111.00

- Toyota Corolla: $2,818.00

Total change in net worth this month: +$16,497.61!

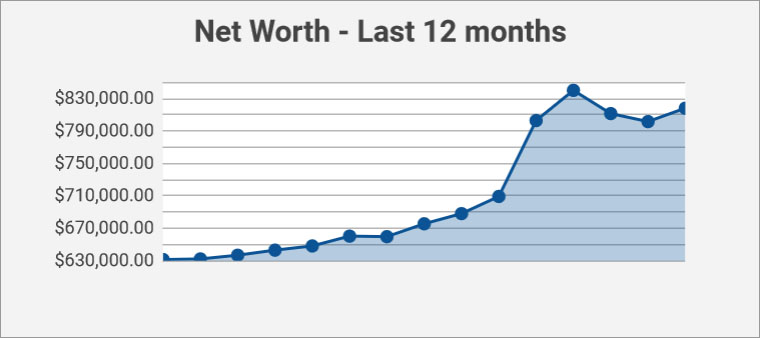

And here’s how the past 12 months have gone to put things in even more perspective:

Some stalls over the past few months, but as to be expected when a bulk of your money is tied in the markets… At least we’re able to scoop up funds cheaper these days! And fortunately when we opened up that new account I believe the market had crashed by 500 pts that day… Which I’m sure subliminally got me to finally act ;)

Oh, and here’s how our kids’ net worths are going as well… Which they have no idea about yet, and which we’re keeping a secret until they’re old enough to log on and read these reports (which will be super weird, haha…)

And that’s April! How did you guys do?? Anyone cross the million dollar mark? Or multi-million?

In “life” news which we now like to add here, it’s been pretty low key…

- Waiting for baby to arrive

- Waiting for baby to arrive

- Playing with my coin collection as I wait for the baby to arrive

- Playing with my other babies while I wait for the baby to arrive

- Sleeping as much as I can while waiting for the baby to arrive :)

It really is unnerving not knowing when – or *where* – it’ll finally make its appearance, haha… I swear every day I wake up it’s going to be The Day!

But I guess he/she’s not done cooking yet… And yes – I’m purposely keeping the sex a secret from you because it’s the only one I’ve got left!! You get everything else from me!!

Hope everything in your life and finances is going well :) MAY your blessings be as bountiful as your incomes this month!

Your (im)patiently waiting friend,

![]()

PS: If you’re just getting started in your journey, here are a few good resources to help track your money. Doesn’t matter which route you go, just that it ends up sticking!

- The "Budget/Net Worth" spreadsheet - the colorful Excel template I personally use.

- The "Money Snapshot" spreadsheet - a simple Excel template I created for my former $$$ clients

If you're not a spreadsheet guy like me and prefer something more automated (which is fine, whatever gets you to take action!), you can try your hand with a free Empower account instead (formerly Personal Capital)

Empower is a cool tool that connects with your bank & investment accounts to give you an automated way to track your net worth. You'll get a crystal clear picture of how your spending and investments affect your financial goals (early retirement?), and it's super easy to use.

It only takes a couple minutes to set up and you can grab your free account here. They also do a lot of other cool stuff as well which my early retired friend Justin covers in our full review of Empower - check it out here: Why I Use Empower Almost Every Single Day.

Get blog posts automatically emailed to you!

Congratulations! We got a big jump in net worth this month due to Mr. ThreeYear’s annual stock “gift” from his company. It’s not really a gift; it’s part of his compensation, but you know, we’ll take it regardless! I think it’s great that you opened a taxable account. We started doing the same this year as well. Funny, our brokerage also rhymes with Wanguard. :)

Hope the baby comes soon! Those waiting days at the end are so hard!!

Heyyy Wanguard twin! :)

Can’t you just do a backdoor Roth IRA to get around the income limits?

https://www.rothira.com/what-is-a-backdoor-roth-ira

We could, yup! At least I think we could – never really had a need to research it before now, haha… But it still wouldn’t help diversify our accounts much, so wanted to bite the bullet on that one first before getting into more exotic things :)

PLEASE do not do a back door Roth without talking to an expert. We did one based on advice from a well-respected podcaster. When it came time to do our taxes, the benefit was not what we thought it was since we have additional money in IRAs and that factored in. So, we tried to undo it and thought we had until we got a letter from the IRS. It is all sorted out now after hours of paperwork and a trip to the accountant but whenever I hear in a podcast or read in a blog to “just do a back door Roth” I want to scream. You know the disclosures that say “Don’t take advice from me, I don’t know you?” This is why.

Scary!! Thanks for jumping in here to remind us!

Agree with Ark….this is a simple and easy way to keep a Roth at higher income levels. If you are worried about any tax liability, just make your initial IRA contribution to a cash account and then rollover. *I am not a tax expert or lawyer :)

Wait I thought the gender of the baby was revealed in passing in an older post?! @_@ Did I read it wrong? Soooo it’s not a girl?!

The Toyota Corolla is such a contrasting frugal car in comparison to your $$ monies, I love it.

Haha yeah – my beat-up hooptie looked great there too until I upgraded to the Lex :) I miss my old girl!

https://budgetsaresexy.com/franken-caddy-car-keeps-making-money/

(and nope – never stated sex! I did say I was secretly hoping for a girl though to help even out the testosterone, but we’ll have to wait and see what comes out :))

I’m back up about 13k this month after a bit of a nosedive in March. I expect the waxing and waning to happen all year

Very nice move J. !

I also dumped 6K into a total world fund (VT ETF for me) this month. Feels good to shut brain down :)

Oh yeah :) It’s hard enough to *earn* the money to be invested away – then to figure out *the best* place to put it every time is just taxing! Haha…

All in Vanguard Total World for me also. I was VTSAX in the beginning but I decided to diversify instead of just go all U.S.

Can’t argue with that strategy either :)

Technically backdoor Roth’s are still allowable… if you realllly wanted to max that out as well

Congrats on making the brokerage move! For some reason, it can be hard emotionally to move money into the markets. Glad you got past it to make your money work for you. I also love your investment choice. Can’t beat that expense ratio, well at least you can’t beat it by much.

Thanks! I think the hardest part will be dealing with the taxes every year with our auto-dividend reinvestments/etc… I know it’s all par for the course, but so annoying having to deal with taxes on this stuff vs never with retirement accounts! (Or at least not until you start pulling out the money later :))

VTSAX in a brokerage account is super tax efficient. 90% or more of the dividends are qualified.

We’ve had most of our investments with Vanguard for several years now. It’s nice to have IRAs, individual 401k, 529, and brokerage accounts all at the same place. It’s easy to manage and low fees are always nice.

Good luck with the baby!

Agreed! I would love to move our 529s over too, but then couldn’t get our state’s tax benefits, womp womp…

Great post. I like the move to have some funds in a brokerage account. Best part of this post “playing with my coin collection while waiting for the baby to arrive”.

It’s seen a resurgence since having more time to myself :)

Congrats on the net worth increase! You two are getting so close to the million dollar milestone.

Enjoy the last few days before the baby comes. I’m due late Aug and trying to do fun things before an infant takes up most of my time hehe.

You’re gonna have so much fun (and LOVE) in your household!! I’m excited for you!

How come your not still maxing the Roth’s via the backdoor option?

1) Because I haven’t taken the time to research it yet

2) I still want/need to diversify into non-retirement accounts

:)

I’ve got a friend who regularly squeezes three carseats into his crew cab pickup truck, and he doesn’t complain about it. Maybe waiting on the minivan won’t be too terrible. (Although we just bought one a few weeks ago and I’ve still never been happier about a vehicle purchase- 2008 Honda Odyssey with manual doors, so they can’t break).

Hah! Yeah, I kinda hope manual makes a comeback too for similar reasons :) Especially for windows! Those seem to break the most with electric..

I still don’t understand the allure of converting 401k to Roth. Maybe its something for the retire early crowd specifically and only during low income years.

Incidentally, it seems Zillow finally stopped low balling my house value and my net worth actually increased to the $390Ks from the $360Ks. It seemed like for so long no matter what I did every month was $360K on personal capital.

Congrats on the net worth increase! Always a good day to find out that your working in the right direction.

Good luck on the baby coming sooner that later….I am sure the wife is looking forward to it :)

The kids’ net worth looks great. I’m looking forward to see the 3rd one catches up. :D

Great month. Our net worth went down a bit in April due to all the checks we sent to the IRS. At least, taxes are over with…

Helll yeahhhh – can’t stand dealing with taxes, which is strange since we’re number nerds?

You prob won’t have to wait long to see the 3rd’s net worth increase though – gonna speed its 529 up so it’s more fair :)

I’m confused by your comment that you are going to speed up the 529 contribution because as I see it, you have the same “18” years to grow and if you bump up Dime’s immediately, they get an extra 5 years of growth compared to Penny’s 529. How is this fair? I’m really interested in what your logic is here in case I want to change my logic.

ACK!!! Editing both our comments right now so no one else sees I just slipped up on the sex there ;)

Regarding 529 stuff – you’re also right! Everyone still gets the same amount of investing periods, I guess I was just thinking of it more in that I need to make sure *I contribute* as much to this one’s account as I did its siblings’ since for both of them I invested big chunks early on… I’ll probably put in $5,000 or so up front, and then set up the automatic $50 contributions to take over from there (so not 100% caught up, but enough of a head start like I did for the other two babes)

Possibly he was saying more fair as an homage to funnel cakes, cotton candy and hastily built rides?

Scene: J puts money into his new child’s 529, throws papers in the air (for no apparent reason), runs around his house 4 times and yells FAIR SEASON IS UPON US!!!!

Haha… Yes. Let’s go with that instead.

We love Wanguard around our house too! Nicely done.

Good luck with baby dime, hope everything goes smooth!

Love it! My wife and I also recently opened a brokerage account. I had a similar hesitation and was keeping way too much money in cash.

Learning about the Ray Dalio All-Weather Portfolio approach is what got me over my fear of short-term losses in a stock index fund. It’s 55% bonds, which is perfect for us. I’m happy to trade some upside for a large reduction in risk.

Oh wow – super conservative! Way to know yourself well and not just go “all in” like many of us do here in the FIRE community :)

(AND I STILL NEED TO GIVEAWAY THAT PHONE – ACK!! I’m so sorry!!!)

Yep! The ups and downs of the stock market are not for us. Some of this money will get used in the next 3-5 years. So it’s not traditional long-term investing, but at the same time keeping it in cash wasn’t the right decision either.

you can still max out your roth regardless of income level.. make sure to do a back door roth.. it is actually pretty quick and easy.. I do it every year..

Happy May, J!

April was a bit of a roller coaster for us – tons going on, and lots of money going in and out, but we managed to maintain stasis in the end.

I’m also still trying to get my mind wrapped around the Backdoor IRA and if that makes any sense for us. My brain just doesn’t want to have anything to do with the topic! :)

Haha… same :)

Yes! I finally have a brokerage account after many years of aggressive mortgage pre-payments and it is a great feeling. My husband and I will probably open up a joint one in the next few months too, which is also exciting :)

Investing in stocks in retirement accounts (i.e. knowing I had already committed to not needing the money for decades) really helped me to get past my fear of the stock market. Now, I can just plop money into the stock market and not worry about it!

Very true :) And does that mean you’re now DONE with mortgages and it’s all paid off?? If so, CONGRATS!

No, not quite! We just stopped being as aggressive with it – wanted some more balance with liquidity and it got less scary as it got smaller (SO close to five figures now!!). We refinanced down to a 10 year term recently and plan to pay it off in five years by making double payments.

Well that’s sexy too :)

Glad to see you having a brokerage account. For the longer i thought there was something wrong with me reading these blogs because I have one. I do mostly VTSAX and BTSLX I believe is what the bonds are called because they both have a 0.05% er. I read JL Collins stock series and he believes you get enough large cap, small cap, emerging and international within VTSAX that it isn’t worth the higher er for those index funds. Or, at least that’s what I was picking up from him.

You should give Hulu tv a look. We cut the cord and I think HBO through them is a dollar or two cheaper.

Oh nice, thanks! And def. smart that your accounts are more diversified too! I’m just a little slow on the uptake here :)

Not a millionaire (yet!) but inching towards 6 figures! Maybe next month if the market cooperates :)

Love the money move, index and chill.. is that a phrase? It should be :)

LET’S MAKE IT HAPPEN!!

Interesting! I added some money into the brokerage account too. Was thinking to invest in some high dividend individual stocks (~5%) and to create a passive income stream; instead I decided to live a little to play the market. A totally different approach than you.

Good move, indeed, you have the intermediate term covered!!

Hey, very cool for you too! Nothing wrong with experimenting a little :)

It’s funny. A couple of months ago I told you that I moved a chunk of my Emergency fund from a nill savings account to VTMFX. A modest fund with actually decent long term returns after taxes compared to pure Stock. In any case, I too was more nervous about moving that than I ever worried about the much larger sum percolating in my 401k. I think it’s a psychological thing that we’re letting go of our life jacket. But we’re really not letting go of it. It’s now just in a glass case that we’ll have to “Break In Case of Emergency”. Sure we may cut our finger if we break the glass (pay taxes), but if the ship is truly going down will we really care? Plus it also keeps us from doing the savings/checking account shuffle. And in the past two months, the couple hundred dollars in interest equals about 20 years of nill savings account interest. Wishing you fair winds and calm seas my friend.

Very very good points, sir!! I’m feeling better already! :)

Hope the baby appears soon – must be so frustrating just waiting and waiting and waiting. And a healthy net worth increases all round as well.

It’s a quasi-milestone for me – I hit $1m in net-worth, but I think I need £1m to be a real millionaire!

A MILLIONAIRE IS A MILLIONAIRE! Haha… Congrats!! :)

Wow, that 12 month tracking graph is awesome! You’re killing it! Can’t wait to hear about the new little one. :)

That’s a big jump for one month! Congrats and keep going! You’re almost there! We’ve seen a steady increase in net worth over months but no huge jumps like that. We’re paying off our car this month though so thats an extra $450 each month!

That image of Personal Capital is super old! It looks a lot better than that. I’m trying it out now versus Mint to see which one I like. Mint I’ve used for a very long time, PC just half a year.

Way to kill that loan!! Where are you going to redirect all that money now?

Congrats on number 3! Brings back memories

We have 3. Back in 11/2014 when the first was just 2yo my twins were born. We waited on buying the minivan till they were born. The barely used odyssey popped up at a great price when they were 1 month old. They were exclusively breast fed at that time so the whole crew went to the dealership bc I couldn’t let the hubs do the negotiating alone. We were there 6 hours & the twins were breast fed twice in an empty office

Bottom line: the minivan is awesome for 3 kids!!!

Oh wow, haha… I give all y’all twin moms mad respect – that’s a full-time never ending gig right there! I bet they’re so cute and grown up now!