What up, what up!

Have an interesting one for you today – let me know if you’ve ever heard of such a thing :) (And you probably have, because apparently I’m the last financial blogger to write about them!)

The topic/company in the spotlight today is Self Lender who has a product called the “credit builder account.” It’s designed to help you build credit while simultaneously getting you to save money, and I’ll be honest and say I totally thought it was shady at first glance, haha… (as most “credit building” services are). But after sniffing around a bit and talking to some of my finance friends who are blogging about them and doing their own reviews of Self Lender, it actually looks like a pretty cool idea for those who need it.

So if you’re interested in a creative way to improve your credit, stick around and see what you think! If you have great credit or couldn’t care less about this topic today, check out this riveting piece on PODWOGS, MUPPIES and DINGLEDORS instead.

You can thank me later ;)

Self Lender Review: So What is Self Lender & This Credit Builder Account?

Well, Self Lender itself is a site that offers personalized credit score tracking, credit monitoring, and access to simple financial tools and resources all around helping you improve your credit, but the product they offer that’s getting all the attention is their “credit builder account.”

It was totally new to me as I’ve never heard of such a thing, but apparently it’s a type of account that’s been around for decades mostly offered by credit unions, only called names like “savings-secured installment loans” or “CD-secured installment loans.” Again none of which I was familiar with.

In a nutshell though, here’s what they are:

A CD (certificate of deposit) that you *pay into* every month until the term is up, all the while your good payment history is being recorded.

So unlike taking out a loan where you get the money up front and then you pay it back, you actually just *save* into it each month and then get it all in the end. While building up your (positive) history in the process.

Of course, if you’re not good at paying things off on time it’ll report your *bad* history too – in which case having the opposite effect, though at least you stashed some $$ in the process – but still a rather interesting avenue that I’m still trying to wrap my head around :)

Have you ever heard of this before? Building credit through saving instead of debt?

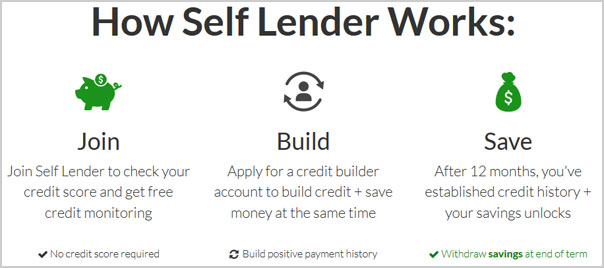

How it Works w/ Self Lender and The Numbers

Here’s the step-by-step process of setting up one of these accounts with Self Lender, along with the details so you can see exactly how it works in practice. As copied and pasted from their site:

- Our partner, Austin Capital Bank, lends $550, $1,100, or $2,200 that is held in a FDIC insured, certificate of deposit bank account (“CD account”) for 12 months. The CD earns 0.10% APY † while the loan has an interest rate of 10.57%. The total APR* is at most 14.77%.

- Pay $12 today (non-refundable administrative fee) to open the credit builder account.

- Choose the payment plan that corresponds to your loan, resulting in payments of $48.50, $97, or $194 per month for 12 months. Payment history is reported to the credit bureaus while the CD account earns interest.

- After completing the term with on-time payments, the loan is paid off, and the CD account unlocks (with the original amount you selected) plus interest**. Plus, you’ve demonstrated months of payment history to the credit bureaus!

So as you can see, it’s not free :) You pay $12 to open up the account, and then you also pay an interest rate of 10.57% up to a total APR of 14.77% max. Those number look scary (cuz they kinda are – though on the lower range of what’s “normal” for these types of accounts), and for a $1,100 loan pretty much means you end up paying about $75 at the end of the 12 months. And less if you choose the lower amount, or more if you choose the higher.

So the question to ask is,

Is it worth paying $75 to help improve your credit while also forcing you to bank $1,100? And if all you care about is the credit, should you just go for the lower amount and pay less instead?

(Btw, that ** up there in #4 basically says that the interest you’re going to earn is either $0.55 at the end of the year, $1.10 at the end of the year, or $2.20 at the end of the year – all depending on which CD amount you go for. So in other words, you’re not doing it for the interest ;))

So Who are These Accounts for?

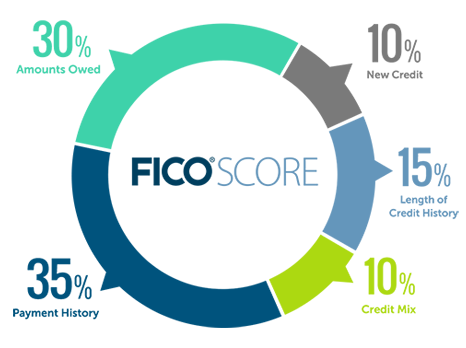

Anyone who has bad/damaged or *no* credit whatsoever. What this is selling here is a chance to improve your credit history through an alternative way than taking on more debt. The history isn’t all that matters, but it does factor into 35% of your overall score (the biggest chunk):

(Found at MyFico.com)

(Found at MyFico.com)

It can also be good for anyone trying to force themselves to *save more* too, however, there are plenty of other (free’er) ways of doing that, so I’d stick w/ the credit reasoning first and foremost ;)

Other things to note:

- You’ll need a bank account or debit card, valid email address, residential address, phone number, social security number (SSN) and be at least 18 years of age to set up the account

- There are no hard credit pulls when you open it

- You can pay off the loan any time you want, with no extra fees (though the point is to build up payment history, so if you pay it off early you lose the full benefits. However, you will still receive the loan deposit amount plus any accrued interest, but minus any amounts due when the CD matures.)

- If you miss any payments or are late, it WILL be reported! Thereby not helping you one lick, though you’ll still receive the money you paid into it minus any amounts due…

So… Is it worth picking up one of these credit builder accounts? If you’re credit is fine and you’re awesome at saving money, no. Just keep doing what you’re doing and you probably wasted 90 seconds reading all this :) (Though still not too late to learn about DINGLEDORS!)

If you’re looking for new options – AND – you have the money to apply towards it every month (and of course trust yourself that you will), then yes – it’s worth investigating more. Which you can do so easily here: SelfLender.com

So what do you think about this? Crazy? Awesome? Dumb? Anyone already trying it out – or have in the past – and it work out well?

Improving your credit takes time, but it IS do-able… Be sure to work on it whichever way you go!!

*****

PS: I wouldn’t be doing my job if I didn’t list the free ways you can improve your score too… Something I know not everyone knows about when first starting out:

- Keeping your debt-to-credit ratio low (i.e. no maxing out credit cards/accounts)

- Keeping your oldest accounts open (the length of credit history matters, as shown above)

- Paying down your debts vs shuffling them around!

- And by and large, just making sure your bills are being paid on time and you’re up to date on all your payments… At the end of the day lenders just want to know if you’re responsible or not when applying for credit, and there’s not one trick that will accomplish that.

[This article was sponsored by SelfLender.com and the links above are affiliate links. As with all products we feature here, always make sure to check them out further to determine if they’re a good fit for you or not. I do my best to pluck out the ones I think can be helpful, but I don’t know the ins and outs of your specific situation :)]

Get blog posts automatically emailed to you!

It seems just a little crazy to me since you’re paying for a loan you aren’t using. Why does the company need to charge such a high interest when there is no risk for them?

If I needed to build up my credit I’d go the free routes and open a credit card to demonstrate low usage and on time payments in full. Slowly but surely it’ll improve.

Interesting post, J$, thanks for sharing.

Keep in mind though that if you have bad – or no – credit at all, you’re not always able to open up credit cards or other accounts so easily :(

Wow, interesting service. I guess it makes sense, but like GS above, I’m wondering about that interest rate spread. Seems like they are making a lot of money!

On the other hand, if it really helps someone’s credit out enough that they can then buy a home, for example, then I guess it could be worth it.

Somehow, it reminds me of that old Pink Panther cartoon. The bit where he is vacuuming the living room and then start vacuuming up the vacuum and eventually sucks everything on the screen up into the vacuum including himself and the vacuum. Maybe it’s just me…

Hahahaha…. completely forgot about that cartoon!! Memories!

Would be a little more intriguing if they could get a CD rate to cover more of the interest charges – but I suppose on balances that small it wouldn’t be close to possible.

I see the benefits if you can’t get any other type of credit and are serious about rebuilding – I hope people that need to use a service like this aren’t rebuilding to start the cycle over.

It’s an interesting idea and it might help someone claw out of bad credit if they are determined to do so and can’t get a loan to establish credit otherwise. That being said it needs to be coupled with something. There was a cause to why they got into bad credit in the first place. Something has to address the root cause before going on the journey. Otherwise it will likely be just another late payment for the prime demographic.

Yup yup – ain’t no trick gonna solve all your problems!

Really interesting! I think my husband would have been all over this a while back. We had to build his great the old-fashioned way (and with a few fun tricks). I would hope that this company will eventually create a financial literacy component or even resource page. Fixing credit is important, understanding credit is even more so!

I didn’t pay attention to them much, but they’ve got a bunch of resources and tips/calculators on their site around credit.

This draws me back to the “Would you rather have $1M or an excellent credit score?” What is $1M Alex.

Seriously though, $14.77% APR seems steep…kind of like the percentage you would pay on a lousy loan for material goods…OK, so it’s saving instead of spending, but something just doesn’t feel right about paying $32 in interest + $12 to set up the account to save $550.

Does no one freak out about paying 15% interest anymore? Is the new anchor point 20% now, thanks to credit cards and subprime car loans? I guess I didn’t get the memo.

Haha yeah – to people like US living on $$ blogs it’s still SUPER high, but unfort to others – and esp those who would be helped the most by this – it’s comparing worse rates with not-as-worse rates. Esp when you start comparing to paydays and what not – shiver.

I’ve always had good credit, so I feel fortunate. The only reason I need check my credit report these days is just to make sure that there is no identity theft going on.

These would describe me best:

NOBUDNOC — “No Budget No Care” – LOL!

FREEDLER — “Freedom Lover”

WOBANOWA — “Won’t Buy Anything – Not Worth Advertising To”

Haha… that was one of my very favorite posts we’ve ever done on this site :) People came up with some good ones!

Well, it’s interesting. The same people who use this may have been the same people who were surveyed that they would take a higher credit score over a million dollars.

I know there are some people that believe we don’t need a credit score, but I think that is because those people either have never had bad credit or are financially able to buy whatever they want. For those who don’t fall into those categories, this option would seem ideal. Thankfully I am not one of those people! You would have to be desperate to take on those terms but desperation is what gets many people into a lot of financial trouble. This desperation is a way to get them out.

If the rate was lower, it would be a good idea. The rate seems pretty high, though, considering it won’t help the unbanked, the people who could use this service the most.

Maybe the local credit unions have better rates for a similar program? If someone had trouble establishing bank accounts due to previous problems and could use the program to establish the opportunity to set up a bank account, then it might be worth it.

From what I hear they’re within the same range of credit unions, and in some cases even lower, but def. good to check around once you know it’s worth considering :)

CDs can actually be really good for building credit. Sometimes you have to include an upfront deposit, which can be difficult for some people, but if you can swing it it’s worth it. I do like that you can accrue interest as well.

I would limit the affiliate link articles to maybe one every month or two that are very established. This one seems pretty pricey.

I usually go *months* without featuring any companies, but lately I’ve just come across a handful at the same time I thought was worth sharing so here we are :) I don’t do any strategy or anything with blogging so everything’s in real-time as I come across them.

Interesting idea! Still the best way to build credit is to: Pay as Agreed!. (On Time, every time) No tricks to building credit!

For folks who are really working to repair their credit, $75 in interest might not be a bad idea. I have renters who have scores in the 500’s from medical debt years ago, and then they never opened any sort of credit card or checking account out of fear. They pay me by money order every month. So there is a demographic that could benefit. I have worked with a few people who lived “all cash.” No checking, no savings, no credit cards. Not because it was cool, but just because they were poor and didn’t trust banks. It’s hard to get a home loan when to take that path.

:(

This might be good for people who just moved to the US. When I was looking for a tenant, there was a couple from Spain who immigrated to work for Nike. They have a great job, but no credit history. So many things depend on credit rating these days.

YES! Great candidate for this…

Yes, the interest is high, but that’s the catch right? If you don’t have a credit history or bad credit, then yes, you will be facing higher interest rates in most anything you do. I think this is a great idea- there are other ways to build credit, but no others that I know of reward you with a pile of cash at the end. Thanks for sharing- I appreciate that you provide information for different levels of financial competency and I don’t think you need to provide alternate entertainment for your readers who have it all together.

Thanks Jennifer :)

I should have read reviews like yours first…this bs dropped my Fico 12 points and also minus 9 with my 2 year projection!!!…I should sue these bastards!!!….gonna post everywhere to make sure buyers beware!!!

Damn, sorry to hear that man. I feel like there has to be other stuff going on for that to happen? Have you reached out to them and inquired (and also paid everything on time?)

I wouldn’t lead with the “sue these bastards” part though – probably won’t get them to want to help you ;)

PS: I left this comment in so others can see and decide for themselves if it’s worth researching or not, so thanks for stopping by!, but I had to delete all the others where you were saying the same thing and blowing up the thread here.. I think one comment gets your point across just fine.

I did this when I was in college. I asked my credit union if I could get a credit card to build my credit, and they told me no, but we have these things called “Credit Builder Loans”. So it was this minus the $0.55 from the CD. It ended up costing me about $40 for the $500 “loan”. The way I figured, I was paying $40 for 12 months of credit history. I don’t know if it helped, since I never checked my score before the loan, but I was able to get a credit card with a different bank after the loan was done.

Oh nice!! I’m sure it had some effect. Cool to hear stories of people doing this in real life – thx for sharing :)

Wow, this is a really interesting service. I’m glad to see something of this type available if it’s not dodgy!

Our credit reporting system works quite differently in Australia (you are assumed to have good credit until you prove otherwise by failing to pay back loans – it’s better to not borrow money you don’t need). But occasionally I come across friends who read a lot of US information – and in some cases, have actually taken out loans they don’t require in order to try and establish a credit rating – even though having a loan they don’t need can actually reduce their ability to borrow in Australia!

Thanks for the interesting read

Sarah

enrichmentality.com

“you are assumed to have good credit until you prove otherwise by failing to pay back loans”

WOW WOW WOW!! That is amazing!

I think this is a last ditch effort, I think someone would be better off using a secured low limit CC to build or help your credit. While you might need cash up front to secure it you can find ones that won’t charge a fee plus you will get your secured amount back at some point.

This is a really interesting concept that I have never heard about. It does seem awfully expensive to be paying essentially $75 to repair your credit score but if that’s your only option I guess it can make sense. Thanks for sharing!!!

This could be a nice service for some people, but the 10+% interest rate seems excessive.

Building credit the old fashioned way seems like a better route.

I must admit, I’ve never heard of these. It’s an interesting idea that sounds expensive. Having said that, it might be worth it for those who need major improvements in their scores.

I hadn’t heard of it either until now :) It’s pretty cool to learn about new things after 9 years of blogging!

My experience with a credit builder loan has been very positive.I have one through my credit union. I took the loan out earlier this year to bump my scores and put me in a better position for a better mortgage rate. My scores were ok, with a couple of credit cards that I use and pay off each month. But an installment loan would give me another type of credit because they’re factored differently in the scoring algorithms.

I did some research and found a few credit unions offer variations of “credit building loans”. Some work just like secured credit cards where you front the money and they loan back to you against that. Others work like you’ve written here. And that’s the kind I took out with my credit union.

I had to deposit $20 to join the credit union and open a checking and savings account. The loan is for $1000 and was placed into a CD. I set up a direct deposit to that checking account and they deduct the payment every month automatically.

My scores went up 15 points the first month the credit union started reporting the loan on my reports. So that was an immediate win. Also, my family is planning a big celebration next year for which my contribution will be around $1000. So I was already going to have to set up some sort of savings specifically for that. This way, by the time the money is due, I will have saved it painlessly (for me) and in the process, added a positive installment credit to my scores. I was going to have to save the money anyway, so the mechanics were no different for me.

Its worked out great and I close on my mortgage this week!

Love this!! Way to go!!! The real life stories left in comments are always my favorite – makes all this theory and money talk so much more REAL hearing how it affects others! Thank you so much for taking the time to share – and congrats on the house!

The most terrifying thing to me is the interest rate. I don’t even want to pay 1%, let alone 10 to 15%. I also believe the whole concept of credit is overblown in our society. It is not something that is really needed and it should be rarely used. Only in the last 50 or so years has it been used on a massive scale. Before that we paid cash for everything unless an extreme emergency came around. Now a days we use if for everything, hence why the world is now 150 trillion in debt. Moral of the story is, it seems like extreme measures for something you don’t even need.

I agree it’s overblown, but unfort if you have bad credit or even no credit it’ll still hurt you for the times you DO need it :( And mostly in the beginning stages of your life before you finally master it all (hopefully!).

Always make payments on time to build credit history. Doing this, it shows that you’re a good payer.

If you have any money saved you can do this yourself through a bank. When I thought I wanted to buy a new house, my credit score was zero but I had money in the bank. So, put some money in a savings account and borrowed from myself with a secured loan using the savings account as collateral. Costs were around $50 for an 18-month loan but it helped me get a credit score. When it was all said and done, I decided not to go in debt and I had paid myself a nice little chunk of change. This might be a handy tool for “tricking” yourself into saving.

Nice! Love the creativity!

My sister was screwed when she was kicked out of an apartment but they didn’t take her name off of one of the utility bills. She looked at her credit score a year later, never having heard anything about still being on the bill (I know it’s her fault but that’s not at issue here) and her credit score was at rock bottom. (and this has been 5 years ago so I assume all statutes of limitations have lapsed) Her credit is so bad she can’t even get approval to take out a credit card, so there’s no way for her to build it back up. I’m going to help her set one of these up, unless another reader has a better idea for her. Anybody?

Dang, that’s harsh – sorry to hear :( You guys are on the right track now researching and reading $$$ blogs though! This stuff takes a lot of time and patience, but it’s definitely worth the pay off so I hope you guys keep on going. (And hopefully she’s off the utility bill now!)