We all know it’s smart to have money saved up for emergencies, but what exactly constitutes an “emergency” these days? And do you ever feel bad when pulling from it even when emergencies DO come up?

(I do!! Which makes no sense at all since it’s literally what they’re set up for!!)

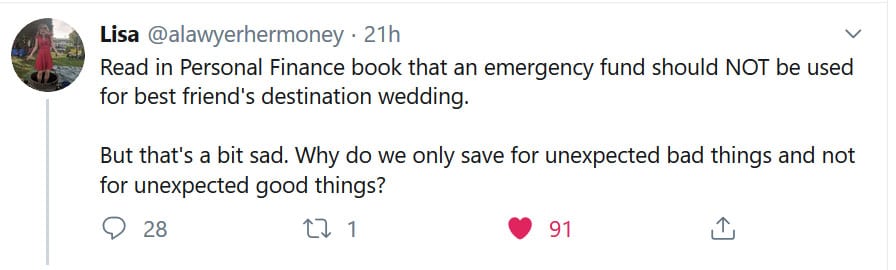

Been thinking about this a lot since my girl Lisa dropped a bomb on Twitter:

Interesting, right?!

My first reaction was: “Nope! That’s a “want” and not a “need” – don’t even THINK about tapping it, missy!!” But the more I pondered it the more I became uncertain of my answer…

Maybe it is fine to tap if the money’s there and it’s super important to you? Wouldn’t it be better than going into debt or liquidating other funds? And who’s making up all these “rules” we have to follow with this stuff anyways?! There’s no money police!!

After a while I forgot about this and went about my day, but a little later it crept back in and I hopped into the comments to see what others were saying.

Here were some of the highlights:

- “I think a separate fund is best for that. The emergency fund is usually branded as the medical or job loss fund.” – @LittleDollar

- “I would recommend NOT using an emergency fund for a wedding but trying to “cash- flow” it. Doesn’t mean you shouldn’t go to the wedding you just have to pull the money from someplace else” – @adimesaved

- “The wedding most likely wouldn’t be a surprise so therefore not an emergency, if it is a surprise than does says friend expect everyone to drop everything to jet off for her suprise destination wedding?” – @Charlotte_Musha

- “I think it’s your money, and nobody should tell you how to spend it. What is the point of a wealthy retirement if you only start living life then? I say you create a plan and figure out how to make it to this memorable event!” – @MetanoiaTraject

- “I recommend folks write a list of what expenses they consider an emergency when starting their emergency fund. So when something happens you don’t have to question if the expense counts. However, I also recommend folks have a vacation fund too. So you can do trips on the fly.”

– @purpose_money - “Debt free already?? Using the fully funded 3-6 months emergency fund? If so, why not. If in debt and using that emergency fund…no way.” – @moneysavvydaddy

- “Oh! I wrote about this. I have an Urgency Fund for “YOLO-Emergencies” like this: https://www.frugalityandfreedom.com/urgency-fund/” – @FrugalityFreedm“

- “The problem I have with my emergency fund is I don’t want to use it for “normal” emergencies. It’s gotten to the point where it has to be “a hurricane destroys my house at the same time as I lose my job and car” type of emergency for me to touch it. (I have a problem!)” – @Jovermyer1

- You can have as many savings accounts as you wish these days! I suggest naming them fun things like #FinancialFreedom fund, Escape to Bali fund, #SkiBumSavings #Sabbatical so the transactions represent your goal, as opposed to deprivation – @TwightFinancial

- And then my favorite response by @skostarasRV:

Haha…

But perhaps @NinjaBudgeter came up with the best solution of all:

Let’s start calling it an ‘unexpected fund’.

This draws a much clearer distinction on when you can tap it and when you can’t, all the while covering both the *positive* and *negative* items that pop into our lives as they do. Of course, you’d also need to top it off even MORE in this case since it would now be covering two large areas (with one being much more tempting to activate, let’s be honest!), but an interesting solution to the quandary indeed.

Personally, we go back and forth with having an E Fund or just mixing it all together into one main pot as we’re currently doing, but I think over time you get better at learning how you operate and what barriers need to be in place (or not) in order to maintain that healthy balance. Stacking up cash to never touch again isn’t that helpful, just like liquidating it down to zero constantly isn’t either. It always takes some fine tuning until we learn what’s best for us!

At any rate, more food for thought this week…

How do you guys currently manage your E Funds? Are they off limits to anything but hurricanes and heart attacks, or do you allow yourself to pull from it during emergency *wants* too?

Of course, step #1 is simply *having* an emergency fund set up to begin with, so if you’re still working towards that just keep on stacking and worry about all these “problems” later ;) Once you’ve got it filled up the main battle has already been won!!

![]()

Get blog posts automatically emailed to you!

I haven’t ever touched our emergency fund. We have enough cushion in the monthly budget that if things come up we can cash flow and just not save for whatever goals we have that month. We have the emergency fund so if something catastrophic happens or job loss.

You’re doing well for yourself!

Once money goes in savings, I hate to tap it for anything, but I do keep a fairly large cushion in my checking account that I am flexible with. I used part of that cushion recently for a stress-related spending bender. I asked myself if I could afford to spend out of stress and decided that I could, and that it was better than some things I could turn to in stressful times. (My actual thought was “It’s not heroin,” though I’d be hard pressed to know where to find heroin even if I was crazy enough to want it.) So now I have some great clothes, shoes, and bags, no pesky drug habit, and yes, a lower bank balance. It was fun and totally worth it as a one-time deal.

HAH!!! I like the way you think!

I use my emergency fund every day.

It buys me peace of mind without having to make any withdrawals. :)

I consider my Roth IRA contributions as my emergency fund, and it would have to be a certified emergency I couldn’t cover with cash-flow. I haven’t had to tap it yet and I shattered my tibia in 2016.

You’ll need less emergency fund if you have good insurance. Might be a blog post about that somewhere here. . . .

https://budgetsaresexy.com/why-work-so-hard-to-build-a-fortune-and-not-protect-it/

:)

Haha, forgot about that post of yours! Excited to share your recent Big News here too on the blog – get ready to be famous again!

Emergency fund / savings for a rainy day. The last time I was unemployed it lasted longer than previous times, so it was very helpful. I’m usually saving up for a Roth contribution 1x a year…so I could tap into that and fund it later in the year if I had to.

I -do- have a ‘travel’ savings account. We had been doing a extended family trip every other year, and then mom and I did an amazing trip in 2018. I wasn’t expecting her to call in Feb this year with another trip offer, but I had the $, & vacation time, so I could say YES!

As for destination weddings….

I have cousins in Florida who got married in Florida. My dad did cover the hotel room for my sister and i, but I paid for my flight, etc. Even then the wedding guests had a block of rooms at the hotel, so I’m sure there was a discount too. It was not extravagant so we weren’t expected to do lavish add ons. The night before party was walking distance (no cab fare) to a dueling piano bar, so maybe a few drinks and split appetizers?

Last fall a friend got married in Western Massachusetts, and I think everyone else drove, but the flight wasn’t that much. I rented a car and got to enjoy the foliage driving over. The wedding couple rented out this gorgeous old house, so my room was paid for, and breakfasts were covered, and the wedding dinner. It was an amazing setting, and a small wedding, I was actually the only friend in attendance. I feel it was an honor to be invited, and it was totally worth it to go.

I’ve been to over 20 weddings (I stopped counting). For some people you can tell, you being there is something they will remember and they really appreciate. For others it can feel like you were a number to fill a required minimum or an obligated ‘& guest’, or just to add to the head count, so they can tell people they had 200, 300 guests at their wedding. Take some time to consider that when deciding. Hopefully a very close friend has a sense of your finances and knows what they are asking of you, when inviting you to a destination wedding.

I definitely suggest / agree with either separate savings funds, or knowing your minimum emergency fund number and that the ‘rest’ is other events savings.

Especially because while on the 2016 family trip, my work got disappointing results, and a few months later had layoffs (that I survived), and while on this year’s trip the announcement was made that our company was having a portion bought / sold off. ( I was part of the group tha was made a new offer and still have a job.) Neither was known or expected when I left, so from experience I can say keep the trip money and the ‘oh no I don’t have a job money’ separate.

Then consider having a ‘slightly larger but expected bill’ savings account. If you have a car you will need new tires every so often (mileage or seem to randomly get a nail in one ). I pay my car insurance every 6 months, I know I will spend more at Christmas time than the other times of the year. If you end up with ‘extra’ in that account, maybe you treat yourself to something you have been waiting for, or maybe it goes to Vanguard.

Dueling piano bar!!! So cool!!

I have multiple funds: Emergency, House (always repairs), Car (teen drivers so who knows what may come up), Vacation and Spending. I had to create that last one as a reminder that money can be used and not only saved. Spouse is definitely more of a spender so having a dedicated spending account keeps him out of the other buckets. But I still hate taking from it!

Awesome idea w/ that Spending Fund :) Probably helps at least a little better spending from it than others, right?

My true emergency fund is strictly for a job loss or a major medical expense. I have separate savings accounts for auto and home, which are supposed to be for my next new vehicle or for planned home upgrades, but also serve as my emergency funds for auto and home repairs. We also have a vacation fund, so in the example, traveling for a wedding would need to come from that.

Smart with the Auto and Home ones – something many people forget to account for and really aren’t “surprises!”

I have dipped into my emergency fund twice. One time was when I bought my house and the money I had saved for a down was in an investment account that was going down at that time. I chanced it and made my self cash poor (at least in view) to pay the down payment. It all worked out and now I just took the money out of the investment account and it should mostly pay for me to have a new garage built! The other time I took some money from it to put on my roth IRA.

Since I have different categories of saving, I have been thinking of decreasing the amount of money I need to keep in saving strictly for emergencies.

The key in both instances here is that you used the money for wealth-building opportunities ;) Hard to fault that even if the $hit did hit the fan.

We tend to create separate savings accounts related to our savings goals and recurring large expenses. Using your terms, some are sexy and other’s not-so-sexy. We currently have separate savings accounts for Vacation, Christmas, New (read: Used) Car, Home Maintenance, Annual Taxes (didn’t escrow these with loan payment to get a better interest rate), and Emergency. Occasionally, we’ll borrow from one savings category to fund an expense related to another, excluding the E-Fund. We contribute monthly to each savings account, except the E-Fund, which gets evaluated once a year (typically after tax refund/profit-sharing bonus) in the springtime. A few years ago, we noticed we hadn’t touched our e-fund (which is typically a good thing), but it was obvious the account was under-funded given our circumstances had changed (i.e. higher income replacement, childcare, general inflation, etc.) since we set our original e-fund amount. This is why we evaluate annually now. Going into 2020 we’d like to create a couple more savings accounts (or rename current one’s) related to specific goals that we can achieve as a family, possibly even make a game out of it by creating a game board to visually track our progress together.

ooooh that would be fun!!! Promise to email me if you end up going w/ the board game route?? And shoot me pictures of it please?? Super fun idea!! (and also very smart on the *yearly* assessments like that as life can change pretty wildly over the years!)

I’ve only had to dip into my E fund for bad things recently but I wouldn’t hesitate to dip into it for a destination wedding depending on what % of the E fund was actually being used. If it could be replenished in the next month or two… who cares? :)

The replenishment factor def. comes into play :)

We have a savings account (high yield MMA) that we put our savings into and call this our “emergency account/fund”.

The only time we tap this “emergency fund” is to bridge the gap between monthly income and bonuses. My monthly income fluctuates depending on bonuses. So, sometimes we plan ahead and book a vacation or buy a large item. I know we can afford this in our yearly budget, but I withdraw from savings and then put the money back in savings when I get a bonus in 1 month or 2. My bonuses are “guaranteed”, and just get paid out 4 times a year.

My wife and I have determined our “savings account/emergency fund” is only for a true emergency when/if it occurs.

Interesting gig you have over there! Are you allowed to share with us what it is? :)

I work for a large, private engineering firm. We get paid in standard salaries, but also get bonuses.

Our bonuses are divvied up into 4 payments throughout the year. So, recently my wife and I wanted to buy a new shed for $ 3,000. We had the money in my bonus, but had to withdraw from savings to float the purchase. Then with my bonus we paid it back into savings.

That is what we do! Works for us :-)

I’ll have to come down there and say hi one day :) Was just in Richmond to see Hamilton!! Which was incredible!!

One other thing to add. Around this time (December) every year my wife and I look at our income projections and expenses.

Then we budget out our next year and determine what we need (new heat pump soon) vs. what we want. We then plan that if something tragic happens (job loss) we immediately go into emergency mode and don’t purchase large items we planned for.

We kind of lay out the whole year and time our purchases. We feel it is really important to say that “vacation” is something we want, but not needed and can be scrapped in case of emergency.

In 2015 we had the insane opportunity to attend a celebrity destination wedding out west. The couple had attended our own wedding in 2011 (before the bride made it big) and we really wanted to return the favor. Fortunately, all we had to cover was airfare and car rental. TOTALLY worth it.

Some close family friends got married ten years ago in Minnesota, far enough that driving was out of the question. We were pretty dang broke back then and couldn’t make it. I still regret that.

Since she makes more than I do, it works out that my wife tends to our cash savings. Current contents would keep the lights on and mortgage paid and us eating on the cheap for a year. We’re pulling $8k from it in a couple weeks for a bathroom reno, so that’d knock a few months off the “emergency fund” aspect, but it’s also unlikely that we’d both lose our jobs at the same time… and we should have it back to normal by March or April. We’re exceptionally fortunate.

That’s a sizeable e fund!!

BUT NOW WE HAVE TO KNOW WHO THE CELEBRITY IS!!!! Haha…

Tell me it’s a reality star of some nature??! :) DM me!

We have a $10k emergency fund and have tapped into it only to pay cash for a used vehicle (a few thousand) when we needed to replace one earlier than expected and didn’t quite have enough saved in the “vehicle replacement fund”. The reasons I was okay with it:

1) Due to other sinking funds our checking account has a large balance and even though everything is earmarked in categories, it could cover a true emergency for a few months. So, we could have technically borrowed from other sinking funds but it was cleaner record-keeping-wise to borrow it all from 1 emergency fund., Much easier to see what needed to be “paid back”

2) There was a clear plan to replenish the account within a few months.

3) It made much more sense to me to “borrow from ourselves” for the balance we didn’t have in the vehicle fund than to pay a bank interest to borrow it. I did think of it as opportunity-loss, though so told myself I was paying 1.9% interest on that money (what it would have been earning in the money-market account we took it from)

4) We have no other debt besides a mortgage.

One thing I don’t understand is when people have high-interest debt like credit cards but then refuse to use an emergency fund to pay off either the card or to fund a new emergency. Why would you put it on a card when you have cash sitting there? People say they are “Saving it for an emergency” but why wouldn’t you use it for the PRESENT emergency and only risk the POSSIBILITY of having to put a future emergency on credit instead of FOR SURE having to pay high interest on this one and having cash waiting around for a future may-never-happen emergency? Always puzzled by that one.

Emotions can do a funny thing to us humans :) And sometimes seeing a cash reserve makes you *feel* more stable even though you have scary debt on the side – at least that’s my take on it. Similar to how I’ve taken out car loans before instead of paying all cash because it feels better to have the cash and the debt vs no cash and no debt. I think we’ve blogged about that before actually?

Yup – here we go! Check out all the opinions on it :)

https://budgetsaresexy.com/would-you-rather-cash-vs-debt/

I actually think psychologically it is sometimes smarter to collect savings. (This opinion from a country where most credit cards never have such sky-high rates though – thanks bank regulations!) We experienced this first hand in our first years of marriage when we were both trying to get this money thing. I tried to pay our joint credit each month, but for a year it never went down. Then I started putting the same amount to a DIFFERENT bank in a savings account and only paying the minimum for credit. Mysteriously, the credit did not increase on that card, but soon we had enough to pay it off full. The same logic has helped my husband later – for years he resisted adding more to joint savings as he “needed to pay down his credit first” which stayed for years in the same place. When we finally started with small sums, he quickly realized it was pretty easy and voluntarily increased the savings amount.

I wish it were not such hard work to train husband, but I’m quite pleased by the outcome ;) He was of course pretty good to start with, and it’s nice to see how now he is also finally getting this money thing :D

Us men are a little slow sometimes ;)

Personally I am uncomfortable with job loss and emergencies being bundled, so I have two funds. One is a drawdown fund and the other is for unexpected expenses. The drawdown fund is peace of mind and future cashflow so I know exactly how much runway is in front of me. This is half cash in an ally savings account and half shares of relatively easy to liquidate etfs GOVT and VYM set on a DRIP through Ally Invest. The drawdown fund is my insurance against income loss. All of my income lands in this drawdown fund presently and flows out at a steady rate leaving a lot more than six months of cashflow behind. Any new or unexpected income I receive has a tendency to pool here as well completely unnoticed.

Downstream money pools in a savings account that automatically pays my “unplanned expenses” credit card which is anything outside of my regular monthly costs be that a vet visit for my dog, taxes, or an unexpected car purchase if necessary. This savings account refills faster than it is used so the surplus is assumed to be for recreational use. Within reason a destination wedding is exactly the kind of thing my ’emergency fund’ is set up for.

Thanks for sharing! Seems like you’ve got a good system down there (as well as great cash flow!)

I feel the E fund guilt!

My mom recently broke her hip, so my husband and I have been taking care of her in our home, getting her home ready to move back into, taking her to doctors appointments, etc. As a result, I’ve taken time off my job and he’s limited hours at our small business (his job). So we had a couple thousand dollars’ gap this month from where we’d normally be.

We COULD have taken more money out of the business to cover the shortfall, but in that case we wouldn’t be able to contribute as much to our retirement savings at the year end. That’s really important to us, both as a goal and as a tax savings strategy.

So instead, we took the difference out of the E fund.

Even though we KNOW we’ll be able to replace it pretty quickly, it still stings! I think because the situation is an emergency, but we could have made the money work other ways (but less advantageously in the long run).

I think it all comes down to how stacked your E fund is, how easily you can replenish it, and how often these fun “emergencies” come up. If you’re “needing” to go to a wedding or take a trip or buy the shoes (etc.) every couple months, it’s definitely time to rethink how you’re using the E fund!

As a side note…I wish all online banks would make it easy to sub-divide savings accounts! Looking at you, Discover.

Yes to that last line!!

SUCH a desired thing from people these days (at least us savers!) that it blows my mind too how not everyone is doing it… I remember when ING Direct came on the scene years ago and they were RACKING UP the customers by highlighting this feature! I’m not sure why they went out of business/merged or whatever happened, but I’m willing to bet it wasn’t from that :)

Ally is adding a buckets feature to their savings account as well as automation between buckets and most magically it seems a sweep system seemingly offering the same features as betterment’s old smart saver. If that is true than I will make heavy use of automated cash sweeping once it rolls out.

https://www.ally.com/go/bank/savingstools/?CP=EML400001540

Very smart! Thanks for the heads up!

For me personally I can’t stand having individual accounts for every little thing – seems like tying up a lot of money that could be doing other things, such as earning more money! And I like simplicity. So I have one fund, in a cash account, that I can draw down when I need, for whatever emergency, house project or sometimes I’ve even used it a bit for vacation. I guess I think of it as a cushion fund.

Rules are really rules of thumb. They serve as a framework until you figure out what all this really means to you, and what works best for you. These money “rules” are basically a framework until we build our own ideals. For example, I don’t need budgeting – I just don’t naturally like to spend that much. I say I track spending, but I don’t really even do that. I just am really conscious of my spending in general.

I have swear-filled thoughts about destination weddings, as a side note, but I’ll stay Midwest nice and ‘ope on out of here.

So much of this resonates! Years back I used to have three or four savings accounts; then I realized all that did was add unnecessary complexity. Now I’ve almost ditched the idea entirely — I tackle HSA and retirement and brokerage accounts, my wife handles cash savings. If other ways work for other folks, great! We ain’t other folks.

99% of the time I’m sure I’d agree with your thoughts on destination weddings. The one we’ve attended was done right: guests’ lodging, meals, and activities were entirely paid by the couple (or her dad? I don’t know, not my business).

Wowww that’s an insanely generous wedding event right there!! Never heard of that before!

I think the key is knowing yourself. How painful was it to accumulate that emergency fund? How long will it take you to get it back up to your target amount? How impulsive are you? Once you start spending it is easy to lose control. Once you cross the line of “emergency only” everything starts looking like an opportunity to spend money. YOLO sounds great until you have lost your job and can’t make your rent. It’s fun spending that emergency money until some OTHER PERSON hits your car and you have to pony up car insurance deductible AND medical insurance deductible at the same time.

No one should be blasé about spending emergency money until they sit down and calculate the risk and the time it will take to replenish the funds. What happens if your return flight is delayed a week because of a tropical storm? Job loss? What if you have to be hospitalized for the world’s worst case of food poisoning? How much are your medical AND hospitalization deductibles? Don’t like the idea of savings for “bad” things? Don’t call it an emergency fund – call it your cushion because it cushions life’s bumps. Only you know how bumpy your life can be and only you know whether you can trust yourself to quickly replenish that cushion if you blow it on a want. And, yes, why is this wedding a surprise? Saving up for things you want, no matter how much you want them, is a skill and an excellent skill for an adult to develop.

(When you say, “But I really WANT it!” you sound like Rocket Raccoon saying, “Why can’t I take other people’s things if I want them more than they do?”

Jane

You would make a great financial planner if you ever chose to be one :)

We never designated an official emergency fund. But we always maintained a large working capital balance in accounts that we could get to in no more than a day or two. So we never had to buy anything on credit, including cars, and generally had enough on hand that we could pay off the mortgage by writing a check, even though we didn’t do that right away. Once you reach FI status then the concept kind of goes away I think because if you’ve got enough money to live the rest of your life without working then by definition you can handle unplanned expenses.

Amen to that…

Congrats on being in that position after all these years :) How long have you been FIRE’d for now? Would you have done anything different knowing what you do now?

Hmmm…my emergency fund isn’t available for destination weddings. But that’s just me. I am still growing my emergency fund, by the way, so I’m not one of those has-a-great-cushion-not-so-worried-about-it people. That’s what goals are for, right? I keep a separate account at my bank that used to be for my daughter and myself, in case she had an emergency. She’s now financially independent, but I keep on direct depositing a set amount from each paycheck so it grows a bit each month. I also got onto Digit years ago when you brought it up, JMoney, and that’s more of a lump-sum pay something off fund for me that I might possibly be convinced to spend from, in the case of an awesome opportunity I just couldn’t let pass me by.

I am still a paper and pencil budget writer, balance my checkbook against my budget every Friday, and I use cash in envelopes for my weekly expenses. It works for me. I also have long-term envelopes for things like car maintenance, and my p o box (mail delivery isn’t all that certain where I live). As long as I live by my rules in a way that makes sense to me, and I see myself making progress toward my goals, I am okay with my spending. It’s when I veer from my path that I find trouble. So, for now and through 2020, I will stick to my guns and do what works.

One day I may branch out into multiple accounts but that just doesn’t fit my plan right now. Kudos to those who are able to though! It makes sense to me, but is just too scary for me to take the plunge.

Way to rock it old school like that! I agree that if you’ve found something that works you gotta keep on rolling with it :) Cool you’re still using and enjoying Digit too! Game changer when it came onto the scene back then…

Overall, the emergency fund is off limits except for job loss, emergency home repairs we don’t have the money for, or potentially flying home in an emergency. We haven’t had to go into yet. However, I’ve been considering a planned dip into it for a while. We’re saving for a car before our kid is due in the spring, and we’re going to be a few thousand short of where we need to be on car savings, so I’ve been thinking we might dip in and pay it back (instead of taking a car payment for that small amount). Oddly enough, I just had to switch my Christmas travel plans due to a family member being ill, but I don’t think of it as an “emergency.” Perhaps because the cost is low enough (hundreds instead of thousands) that I can probably figure out how to finagle the expense some other way. I’ve certainly been thinking of your last post as I switched travel arrangements.

This is just me and please others feel free to post. I’m almost 40 and have owned several cars (most used). Cars are SUCH a money pit!!!

I highly encourage anyone to buy a used, high mileage car that is in decent condition. My Accord is 16 years old, 144,000 miles and going STRONG. I am hoping I can get another 5 years out of it.

I would agree with that :) Though with little kids I’d just make sure it was super safe and maybe a little less mileage as nothing’s worse than breaking down with babes with you! The only reason I finally had to get rid of my FrankenCaddy a few years back, RIP…

I’m 43 and have never had an emergency fund. I’m not saying this is a good thing…but nothing remotely bad happens to me ever.

I only have $2000/month in expenses. Without a home and no children, I have nothing to worry about!

Oh wow – that’s some lean expenses, well done! Do you have at least some savings/investments *somewhere* you could tap if your luck changes?

We’ve always had a pretty big cash cushion so when large expenses came up the wife would just take the money from the account as needed. This included things like property taxes (we don’t have an escrow fund, or a large vacation like our cruise to the Mediterranean, or an unexpectedly large tax bill). But, with that being said, she would always take the next 6 to 12 months to replenish it back to her comfort level. We have a division of labor in our marriage, she manages the day-to-day, household expenses and I manage the investment/retirement side. Been married for 39 years and it seems to have worked out pretty well. I finally retired this month (I’m 62) and now I need to convince her that it is OK to take money out of savings/investments. That is going to take some time. LOL

Yeah it is! Haha.., Probably the hardest thing to wrap your mind around after all those years of saving!!! It’s all we know up to that point! :)

Our e-fund is only one month’s salary – and just one person’s at that. The plan has been to invest anything that goes over it, but so far we haven’t gotten that high. Things we’ve tapped it for: a surprise renovation bill (it was renovation from a year ago, where one contractor forgot to send the invoice, and only apparently noticed as he was closing his books for the year), paying off my husband’s credit card (it was getting close, and the reason for credit was the year he built his business with no salary and I paid all our joint bills), and rounding up an investment amount to the same company. In each case we had money elsewhere but earmarked so chose to use this account. Only one of those cases was a “legit” use of e-fund but in each case we made a conscious choice.

We do keep other separate savings accounts. One is for long term investments, which I tapped last time when I had the chance to buy my employer’s stock, and which is now targeting investment apartment. We also have accounts that we don’t even include in our net worth, which are for “splurges” – accounts that we use for expenses that are too large to cash flow from one month’s salaries. Planned renovations, travel, Christmas expenses.

I’d like to justify a bit this low emergency fund. As I mentioned, we have most times anyway 2-3 times the e-fund amount in other savings accounts, so those could also be used as buffer. But also where I live, the 6 month emergency fund would sound excessive, as I live in a country where several emergencies are already covered through taxes. In the case of unemployment, there is a fixed period during which government pays 80% of your salary while you are looking for a job, so emergency fund would need to simply cover the few weeks before this payment would start running. We also have fully funded public health care so even in big emergencies, the cost would be nominal.

As to destination weddings: I have missed a friend’s wedding twice. Once because of a job change, the other time because I just had a baby. Ten years later, I still hope I could have made it work. Don’t miss out on these once-in-a-lifetime chances! (But I would normally use that “splurge” account if possible.:)

Woahhhh where do you live???! That jobless perk sounds incredible! And of course the health insurance too, but basically all countries are better at providing for their citizens than here :(

Sorry missed this question! Finland, but similar scenarios are elsewhere in Northern Europe and much of other parts of Europe too.

Of course, Finns are notorious complainers and tweakers, so we are always trying to optimize how much and for how long we should pay the benefit. Currently gov is talking about shortening it a bit, which might make sense (most people do find jobs quite fast and we don’t want leechers just taking a “vacation” on that money). Then again in low employment areas (the countryside) it might become too short…you can’t make it work for everyone at the same time!

Super fascinating to hear about, thank you :)

I’ve used it twice –

Once I used part of it to replace the catalytic converter that was stolen from my 15-year-old car (cost $3k, an unexpected expense that month.)

This past year I used it to help fund a loan to a good friend to help with a down-payment on an unanticipated opportunity to buy his first house. The chance to buy came up very suddenly so it was helpful to have some liquid assets handy. I built the fund back up in the subsequent couple of months.

What is wrong with people stealing parts like that???!

Super nice of you to hook up your friend :) Did you become an investor in the house, or just loaned him the money straight up?

Just loaned him the money straight up. Low interest rate, a simple notarized contract to keep us all friends.

Yeah, I’d rather they had come and asked me for the $200 that they would get from the recycling shop. Security versus petty (or grand) larceny is an arms race where I work in the Central Valley.

dang… sad to be in that position :(

We are living on our emergency fund right now. My husband is a computer consultant and sometimes he can have times between clients, waiting for projects to begin, or just trying to find next job. We have had three separate years where he wasn’t working for at least 3 months at a time. Going on four months right now.

Destination weddings are NOT an emergency. What happens if you go on this trip, then lose your job when you get home? What if your car breaks, or your furnace goes out, or you house burns down, or you get hurt or become ill…? One thing I have learned in my years on this earth is that you WILL have things go wrong in your life. Plan on it!

Here are some things that have gone wrong over the years:

Natural gas leak in pipe: emergency weekend plumber fix.

Sewer backed up in basement. Emergency rooter service on Thanksgiving.

Planned surgery for daughter followed by unplanned emergencies and hospitalizations.

Sudden dog illness.

Car accident.

Washing machine broken beyond repair (only 2 years old!)

Pool pump gushing water

Multiple months of unemployment.

Sudden illness of parent who needed care for a few weeks

Emergency furnace repairs

Emergency hot water heater replacement

Many car repairs over the years

Now, does that mean you can’t go? No. Just make a plan to pay for it other than your emergency fund. Work extra hours, have a garage sale, pick up a side hustle.

Ack!! And notice how most of those things are *house* related too which never gets considered when people do the “owning vs renting” comparisons :(

I’m glad the emergency fund has saved y’all over the years though :) Sending good vibes over that your husband finds a new gig soon! That would be a great Xmas present!

I have about $10k for my fully funded EFund, but I just recently tapped into it to purchase a $2k ebike…that was on sale for $1250. It was a little too good to pass up and I didn’t really see anything big coming in the next few months while I replenished the money…

That being said, I also had surgery that I saved up for over the course of the year beforehand so I could just pay it off without tapping my EFund. I’m sure I could’ve saved for the Ebike, but it always seemed so silly and like I had other things to put my money towards. BUT…that sale was just soooooo good…!

So now my EFund should really be called the too-good-to-pass-up-but-not-for-vacation fund I guess?

Haha.. Well don’t leave us hanging here – has it been FUN to ride so far??! :) Are you now taking it to and from work, thereby saving you money and helping you get fit at the same time?! Inquiring bloggers want to know! :)

I have a savings account that doubles as emergency fund and “large necessary expenses” fund. I’ve tapped it for furnace repairs (emergency), a new roof (non-emergency but important), replacing a creaky old staircase (non-emergency but a bottleneck in a renovation project), and a complete overhaul on my clarinet (definitely an emergency, and worth every penny).

It’s a minor hassle withdrawing funds as it’s in a Tax-Free Savings Account and I have to go down to my credit union and sign a form, but the money shows up in my checking account the next day.

A Tax-Free Savings Account? Can’t say I’ve heard of that one before! In another country I presume? (And fellow clarinetist here! Though I haven’t touched one since high school :))

A Tax-Free Savings Account is Canadian (I’m in Winnipeg). Normally we have to pay tax on any bank interest earned, but you can put up to $6000/year into a TFSA without incurring any tax. Better still if you can leave the money in there to compound, obviously, but life happens.

I’ve been playing clarinet for about 15 years now. After falling under the spell of a community concert band — essentially the adult version of a high school band — I got more serious about practice and bought a really nice instrument for myself. (That was the first time I used my TFSA to save up for something, and it was nice to pay cash rather than using a credit card or buying on an installment plan.)

Very cool!! Glad you found something you can enjoy so much! And really cool name, btw!

I graduated early, had a subletter sign the lease for the apartment, back out from the lease (still wondering if that is legal), had medical bills, car repair bills with shocks and struts replaced (not cheap) and I still did not touch my unexpected fund. If you are well prepared then emergencies are nothing.

Well done, my brother. A good place to be at!