Was thinking about the way I spend my money, and noticed how drastically I treat it depending on *how* exactly I come across it ;)

For example:

Money I get as gifts: Time to spend away!! And almost always towards *wants* vs needs and those things I’d never go out and buy for myself but deep down really want, haha… So basically – the best types of gifts anyone could give me :)

Money I get in winnings: Same as above, only not including the *costs* of attaining those winnings if any were incurred (like, say, money for lottery tickets or tickets for raffles/giveaways, etc).

Money I earn at the “job”: 100% for living and goals/dreams/retirement/etc :) Quite the difference from the above!! Haha… But why is that since it’s all still THE EXACT SAME MONEY at the end of the day??

Money I earn from “hustles”: Usually treated 80% like “job” money and 20% like “gift” money. Only I’ve recently realized that if I don’t SPEND that 20% “gift” money within a certain time period, my guilt starts creeping in real good and it eventually morphs into “job” money.

Trying to pinpoint the EXACT amount of time until that occurs, but so far I know it definitely happens after *one week* because I tried setting aside a good chunk from that old domain I sold last month, and by the time I was literally in front of the object I had earmarked it for I couldn’t bring myself to pull the trigger! Even though I really wanted it! However I’m pretty sure if I had gotten around to it within 24-48 hours of the money hitting my account I would have been all over it.

Interesting thing to figure out about yourself for sure, haha… And which could also be used as a trick against you if you ever wanted! ;)

Money I inherit: Similar to “job” money, only straight to the goals/dreams/retirement section and not allotted for “living” expenses at all… I once read somewhere that out of all the money you receive, you should treat inheritances with the upmost respect since it honors your loved one who set it aside for you. And blowing through it would be one of the most disrespectful things you could do since they poured hours of their lives into *earning that money* which is now gone and literally sitting there in your hands.

Of course blowing through money is probably not any of our M.O.s anyways since we’re all here reading a finance blog right now, haha, but it’s never left my brain and now I make sure to spend *extra* attention and care to this money as if it’s the holy grail of it all. Even though again, money is still money at the end of the day!

What other types of money am I missing?

Hmm….

Money you get back in refunds/loans from people: 100% applied the same as “job” money. Right back into the pipeline and not treated at all as “free” money since it was all your money to begin with!

Money you get back in taxes (of course that was coming, haha…): Almost always towards maxing out retirement accounts. And if not retirement accounts, some other major priority that increases overall net worth.

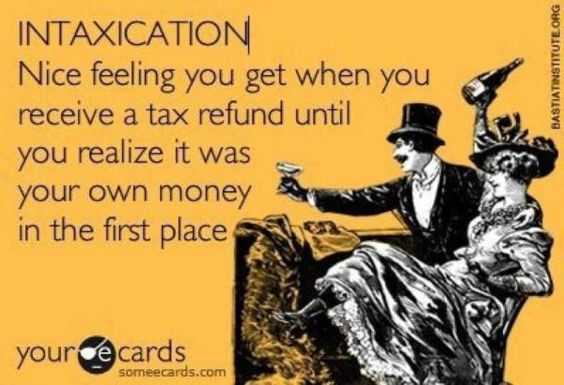

Actually found this on the ‘nets the other day while looking for money jokes and thought it was pretty hilarious (and accurate – though of course you know my feelings on tax refunds! :))

Money you get from investments/dividends/etc: Straight back into the investment!! So those pennies keep compounding and making more penny babies!!!

Money you find on the street (which happens a lot to me actually – people just be throwing their money away!): Treated the same as “gift” money – towards anything my heart desires, which is usually coffee since I mainly only find pennies or dimes :)

(I did find a bag of cash once though in the middle of the parking lot which freaked me out!! I quickly put it in my pockets and drove off since there was literally no one – or car – around for at least 50 feet, but it didn’t stop me from envisioning some drug dealer chasing me or Candid Cameras stopping me down the road to interrogate me, haha… Fortunately I lived to tell the tale ;))

Okay, that’s probably enough examples for now, haha…

Point is – I seem to treat my money differently depending on how I get it, and pretty much any “expert” will tell you that’s the *opposite* of what you should be doing ;)

But hey – that’s just the way I’m wired! So sue me!

And honestly, it’s kinda refreshing to have some flexibility around this stuff since I tend to be so rigid with the “real” money I bring in (i.e. job money or investment money). Still, pros and cons to this stuff but it helps knowing at least how you operate in case you want to change it and/or enhance anything.

Anyways, thought I’d throw this out there and see where it goes…

If anyone wants to include me in their wills, you now know you don’t have to worry about me being a good steward of your hard earned money ;) Just sayin’…

![]()

UPDATE: I’ve since been told this idea of treating money differently is called “mental accounting” and is very common! Here’s a post I just wrote up on it, along with two other interesting iterations of it: More forms of mental accounting: the “endowment effect” and “nudge theory”

Get blog posts automatically emailed to you!

You missed money you get from a life insurance policy. I received $20,000 almost 6 years after someone passed away. I was in shock. It took the life insurance company that long to find me since I moved out of state My almost 14 year old car was on its’ last leg so I used most of it to pay cash for a new car. I put bday $$ & gift $$ into savings but love spending gift cards on “wants”. Any $$ I find on the street goes into a jar saved for vacation (comes in handy for tolls). Any gains on invested $$ remains there for compounded interest. Tax refunds go into savings or IRA’s for the following year. Job $$ goes towards regular bills with $150 automatically used to pay down mortgage principal every paycheck. Also have job $$ automatically withdrawn each month towards Roth IRA’s. Thanx for the fun read!

Well that was a cool $20k surprise!!

Good reminder about *gift cards* too – I also spend those much freely than my “normal” money :)

When my grandmother died a few years back I received enough to live on for a few months; I used it for that, living frugally, while dumping 100% of my paycheck into a 401k. That got me ahead enough to realize I could max out my 401k in October or November, then save enough the last couple months of the year to live on in January while applying all of that month’s paychecks toward maxing it out even sooner. Right now, for instance, my 401k is already half funded for 2019.

It was a good lesson. Grandma would’ve approved.

Now that I’m in that groove, any other ‘found’ money will go right into an after-tax brokerage account to help cover living expenses between pulling the ripcord and age 59.5… unless it’s somehow a particularly large sum, in which case we’re adding a second bathroom to this bungalow of ours.

Grandma would be very happy, indeed :)

Being that you didn’t cross to the other side of town, across the tracks to say, there’s:

Bribe money: good honest days extortion. Probably need to spend it at the bar but you’ll feel guilty because you should pay rent

Hush money: not quite as good as bribe but they get the meaning when you’ve got a shovel in one hand … This could be filed under side hustle. Should really save it for a rainy day –>

Action money: did you get your cut? Did you win big? Its money you could’ve saved but because its your winnings/cut then why not have a little fun.

Tax evasion: Ha! now we’re getting somewhere. Its your money. Should probably invest it in multiple shell corps or false fronts that way it can grow…

Last but not least

Money on the streets: everyone’s gotta hustle. Little gambling here, little protection there… this is your daily spending money.

Fuhget about it…

Haha okay – you win today, my friend :) Put my boring post to shame!!

I treat all money the same. I never quite understood doing it any other way.

A dollar is a dollar

Guess that’s why we all have different net worths :)

Me too. The money just goes to the bank. Especially now that we rarely get cash anymore.

In the old days, when I got cash, it’s way easier to treat it differently and splurge. Now, you have to deposit everything first.

I am with the above folks – I tend to put it anything extra toward my goals. The sooner to FIRE, the better!

The funny thing is one of my very best friends is the polar opposite of me. Whenever I’ve talked about getting a raise or some extra money she’s always like “oh, you could spend it on xyz!” Nope, in the stash those little employees go!”

They really are better employees than we are sometimes, huh? :)

…as I type this at work lol

I think I treat all money the same too if I let them all go to the bank and not doing anything about them for a week. If I decide to put 100% of certain money towards retirement accounts, I have to do it right away when I receive the money.

That’s where *automating* helps too :) Which unfort. you can only do with income you already know is coming in advance, haha…

By comparison, I’m so boring but I consider it “elegantly simple”. XD

I treat all money from all sources rigidly right now. With one minor exception last year – I had an unexpected tiny windfall and I spent a portion of it on clothing that I had been putting off for a year. Everything we want normally has to be cashflowed or it waits until we can cash flow it. All other money not already earmarked goes into savings and from there into investments. I tell them FLY MY PRETTIES! FLY! MAKE MORE MONEY!

Hahahaha… your monies have such wonderful parents :)

I used to treat it it all differently – pre-personal finance awareness, my paycheck went toward living expenses, while all bonuses, tax returns and salary bumps were YOLO money.

So many spontaneous vacations and shopping sprees went down in those days :P

Nowadays, I treat it all the same – it gets budgeted toward goals first, then fun!

Probably smarter, even if it’s not always *as* fun ;)

Haha–I’ve noticed the same thing. If I don’t spend those little windfalls within a week or so, they just get rolled into something boring…which is good, because they help me reach my financial goals that much sooner but sometimes I’m mad because those are also my little treats. I pick up extra cash here and there doing research studies. I carried a $50 check around for a month recently while I tried to decide how I wanted to treat myself–pedicure? nice lunch out? Finally deposited it and put it toward a debt I’m trying to knock out for good. While that check was burning a hole in my purse I also ended up with $20 cash from a different study. Trying to figure out what treat I wanted and I realized all I wanted was sleep. As in, I legit would pay $20–or more–to get more sleep. I’m a single mom with teenagers and little kids and I NEVER get enough sleep. I offered my oldest the $20 if she made sure that everyone did their chores, packed their lunches, gave the youngest ones a bath and got them off to bed, and turned in the teenagers’ phones by 10pm. I took a bubble bath and fell asleep by 8pm. Probably my most favorite way that I have ever spent $20… and you can bet your sweet booties that I will do it again.

YES!!!! Hahahahhaa…

BEST IDEA EVER!!!!

Totally going to have to share that somewhere :)

I treat any windfall (including tax returns) differently than most other funds. 10% of it goes to something fun, 90% goes to mundane stuff like the mortgage or retirement.

I treat the rent I get from my guest house as mortgage payment money only. It goes directly to BofA to help me get rid of this pesky house payment.

Pretty much anything else just gets treated like my job money. I guess I’m just kind of boring like that.

Boring with a higher net worth ;)

No, all money is the same to me. It’s money, something that is good to have as well as essential for sustenance and freedom in our world. I don’t like it better when it is earned. Come to think of it, while I don’t respect money/value any less regardless of its way of getting to me, I think I like it more when it *isn’t* earned. Just thinking about interest/dividends and the like. I know we call it “earned”, but it seems more like a passive entitlement!

Totally, haha… money making money as you continue to live your life! ain’t nothing bad about that…

I’m totally the same way! Sometimes my gift money ends up going to living expenses if I wait too long with it in my wallet, but otherwise, I definitely tend to align my spending much as you do! My only exception is with my side hustles—I generally put the majority of those back into a business account since my side hustles are stuff I like to do for fun anyway (photography, blogging), so I’ll reinvest a lot of the money right back into it :)

I WISH I was getting a big tax refund this year so I could get the intaxication! We were actually due to get around $8500 back this year but then ended up converting my husband’s old 401k to a Roth and took the tax hit last year instead. I did my blog post today all about it, actually! But if we would have gotten it, it totally would have gone toward those “big picture” things, just because it’s nice to see such sizable progress in one fell swoop!

At least you got that tax hit out of the way! And better when you break even like that than having to pony it up which feels much worse :)

The one I’m guilty of is money from credit card churning . It becomes the vacation money bucket. It’s a psychological thing obviously since money is money.

And something tells me you are not alone in that ;)

Haha this is good!

I *definitely* treat money differently based on where it comes from.

Pretty much every dollar I get follows your rules – dividends/money from investments goes right back into them, job money goes to responsible things like retirement, bills, etc.

Gift money – gift cards usually as I don’t know anyone who just gives me cash (red envelopes are not in my heritage, sadly) – those are spent on fun things/experiences.

The one category that I have, that I didn’t see in your list, is cash back earned on my credit cards – I use that money 2x a year – once in the summer for my birthday gift to myself and once in Nov/Dec for my Christmas gift to myself :)

Good one – forgot about those!

I think I just have them auto. deposited back into my savings over here… Which is quite different than the other *extra* money I received, I wonder why?

What did you use to sell your domain name? I currently own Nikegolfshoes.com which I randomly bought because I thought it would be worth something some day. Well it officially is I think and don’t know what to do.

Also what websites do you use to figure out a selling price for your website?

Fun! I totally bet you could sell it well, so long as it’s okay to have “Nike” in the domain like that (not sure what the rules are of branded names…).

For this domain I was just directly reached out to by a buyer who wanted it, but I know there’s sites like Flippa.com and others that specifically focus on domains and websites… In fact, most hosting companies where you buy the domains from usually offer some sort of auction listings too – so I’d probably look into that first.

As for the pricing, I’m not sure how that’s done domain-wise (I just did my best to get something that *excited me!*), however with full websites at least in our $$$ world here they tend to go for 2x-3x yearly profit. Sometimes more depending on the strength of the site, how old it is, how it’s monetized, branding, potential, etc etc.

I bet you could dig up a lot of tips/info with a quick Google search :)

I absolutely love the idea of handling inheritances with extra care. Thanks for sharing that. It resonates with me!

Yeah, I’m pretty similar to you in how I handle money differently depending on how I obtained it. Except this Christmas I used my gift $ to finish maxing out my IRA. It felt way better than a new sweater :)

Haha I agree completely :)

And so glad that inheritance part resonated with you!! I wish I could remember where I first heard it as it’s always stuck with me since.

I have this uncanny ability to stuff whatever I earn, regardless of how I earn it back into something that will benefit me in the long run, whether it be my TFSA, my mortgages, RRSPs. I’ve even been told I suck the enjoyment out of things sometimes when me and my buddies grab a win at the casino and they want to go out but all I want to do is hoard the cash and call it a night haha.

Oh well, I’ll thank myself for it in my 50’s!

Haha… I suppose there could be worse problems! :)

After years of being a 100% committed YNABer I really do see now that a dollar is a dollar is a dollar. The only money I treat differently now is that $1K I have at the end of the year from using the Money Saving Chart. And even then, I buy a treat up to £1K then the rest gets pumped back into the money pool.

YNAB really is pretty awesome :)