When I mentioned a few months back that my wife and I haven’t had health insurance for the past couple years, some of you thought I had lost my marbles. Thank you to everyone who emailed me their thoughts and were concerned about my family’s well-being.

Some good news — starting October 1, I am now eligible for employer sponsored health insurance. As a new employee, I don’t even have to wait for open enrollment.

But, it’s not all roses … health insurance is expensive!

Is health insurance worth the cost?

Hard question, because everyone values health insurance differently.

Some people with chronic health issues absolutely depend on insurance to cover medical expenses. Others haven’t visited a doctor in decades and see little value in insurance. Some people enroll in health insurance only because they get a hefty discount (or get it free) from their employer. And sadly, many people out there simply can’t afford health insurance.

It’s a crazy landscape. Everyone’s health situation is different. Everyone’s risk tolerance and attitude toward insurance is different.

Let’s take a look at my new health insurance options and run some medical issues and cost scenarios. You might see how hard and crappy it is for young and healthy couples to make a decision on health insurance. I’ll also share some of my experiences paying for health care out of pocket the past few years.

My New Health Insurance Benefits — Plan Options

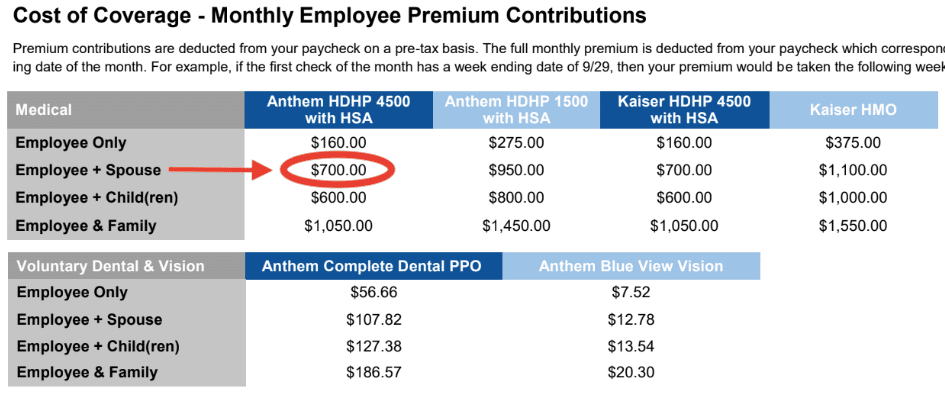

As a California resident, I get to choose between Kaiser or Anthem insurance. Both providers offer only 2 plans each through my employer. Here are the monthly costs …

The Anthem HDHP 4500 plan is recommended to me and my wife based on our health profile. It’s also the cheapest monthly cost to cover us both. Circled in red, this is $700 per month, or $8,400 per year. Ouch.

HDHP stands for High Deductible Health Plan. The reason the deductible is “high” is because this $700 monthly premium is considered “low”. 😥

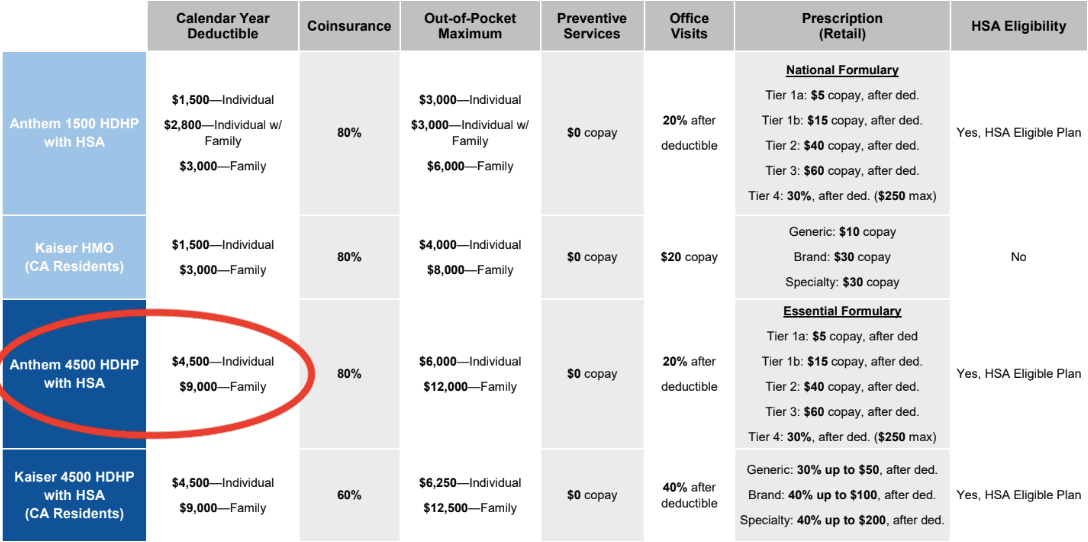

Now let’s take a look at the deductible and what health coverage these plans include…

Looks like this Anthem plan has a $4,500 deductible. The deductible is the amount paid out of pocket by the policyholder before an insurance provider will pay ANY expenses.

So on top of the $8,400 annual plan cost, I am responsible for paying the first $4,500 (Or $9,000 for me AND my wife) in care costs before I see any financial benefit from this insurance plan. Actually, that’s not completely true … This plan will throw me a few free preventive care visits or “check-ups” each year. Apart from that, it’s $12,900 in total before the insurance company chips in a single cent.

So Is Health Insurance Worth the Cost?

Well, everyone defines “worth it” differently. Let’s just look simply at the financial calculations for a moment …

For me to realize any financial value from this health insurance policy, I would need to spend $12,900 in care in a single year (either me OR my wife). Or, $17,400 if we both wanted to see value from the plan.

Will I need more than ~$13k in medical service in the next 12 months? I have no clue! (and I certainly hope not!). It depends on what goes wrong throughout the year. Let’s run 3 different health care scenarios for the upcoming year and compare my out of pocket costs of having insurance vs not having insurance.

*Quick note: In the great state of California, they issue a fine for people without a health insurance policy for 2020. This fine is a maximum of $750 per person, so I’ll be including $1,500 in annual fees in calculations for the non-insurance examples.

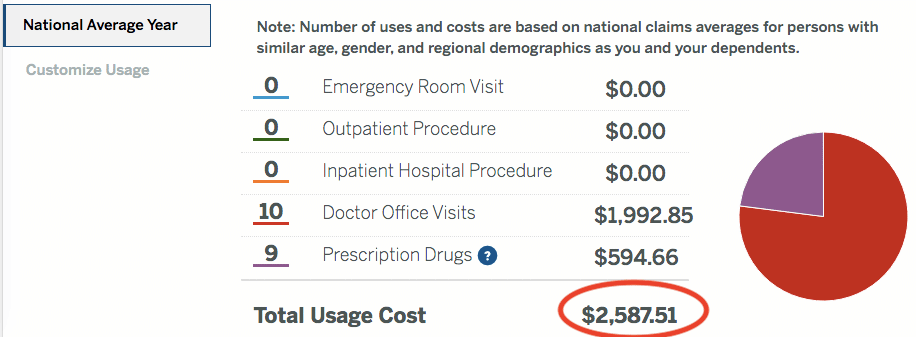

Scenario #1: A “National Average Year” (Not Much Health Care Needed)

According to the calculator on my benefits website, the national average for a married couple like me and my wife would come to 10 x doctors visits, 9 prescriptions, 0 emergency room visits and 0 surgeries.

The total cost would be $2,588 in medical costs for the year.

Now because this is less than the $4,500 plan deductible, I would be responsible for paying this cost out of pocket whether I had insurance or not.

Annual Cost with insurance: $10,988 ($8,400 annual premium + $2,588 in care)

Annual Cost NO insurance: $4,088 ($2,588 in care + $1,500 no-insurance fines)

In an average low-health-issue year like this, my wife and I would be better off without family coverage, even if we took on a $1,500 fine. This is how we have gotten by the past couple of years, which I’ll explain more below.

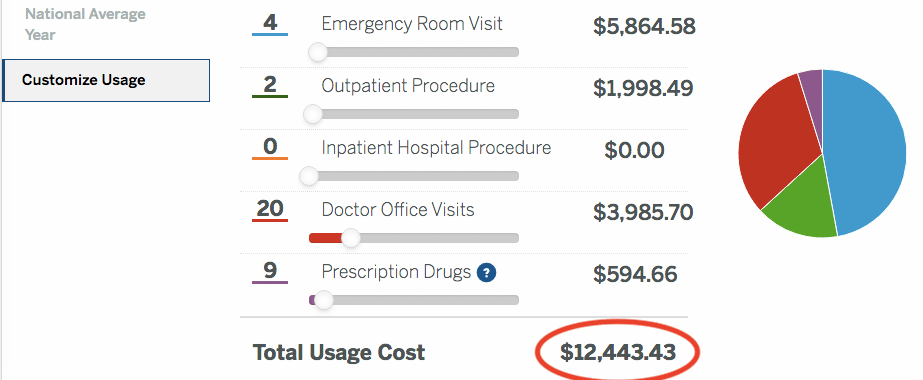

Scenario #2: An “Unusually High Year” (Getting Sick and Hurt A LOT)

In this scenario, I added 4 x trips to the emergency room, 2 same-day surgeries, and doubled the amount of doctor visits to 20.

Even though a year like this has low probability, it could happen. Disaster strikes at any time and health problems affect everyone.

Annual Cost with insurance: $14,400 ($8,400 annual premium + $4,500 deductible, + $1500 in additional 20% of co-pay. $6k is the plan max out-of pocket)**

Annual Cost NO insurance: $13,943 ($12,443 in care + $1,500 no insurance fines)

Hmmm … I didn’t expect this outcome. Looks like having no insurance still works out financially better in this scenario.

**This calc is based on either myself OR my wife having all the health issues. If we split these doctor and emergency room visits between us, we’d have to cover our family deductible ($9k), so the cost would actually be just over to $18,000 total.

OK, now let’s add a horrible in-patient surgery to the mix …

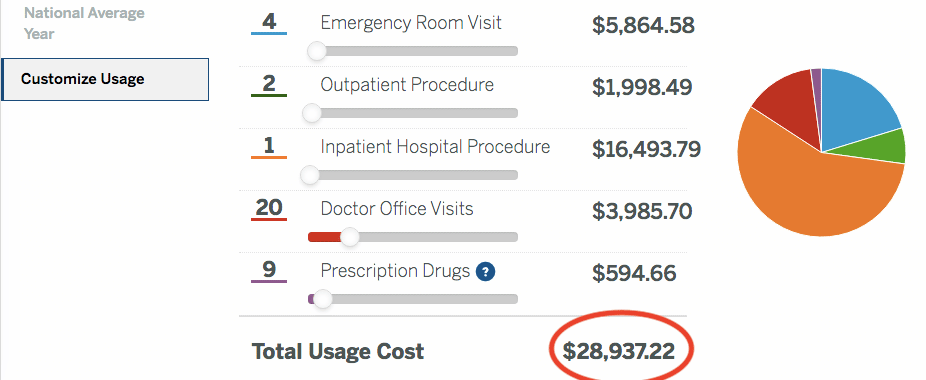

Scenario #3: “Horrible Year” (Major Surgery Needed)

Here I’ve added an in-patient surgery or major event staying overnight at the hospital. This is on top of the unusually high year scenario we just reviewed…

I wouldn’t wish this scenario on anyone. But unfortunately, it happens every year to people around the world. Insurance not only provides financial coverage, but also peace of mind in traumatic times.

Annual Cost with insurance: $20,400 ($8,400 annual premium + $12,000 out of pocket family max)

Annual Cost NO insurance: $30,437 ($28,937 in care + $1,500 no insurance fines)

For a horrible year like this, insurance would save us an additional $10,000 medical bill. It would still be an expensive year out of pocket ($20k) but we could rest well knowing that this is the worst it would get financially. Insurance pays off financially when extensive care is needed.

Covered California Options

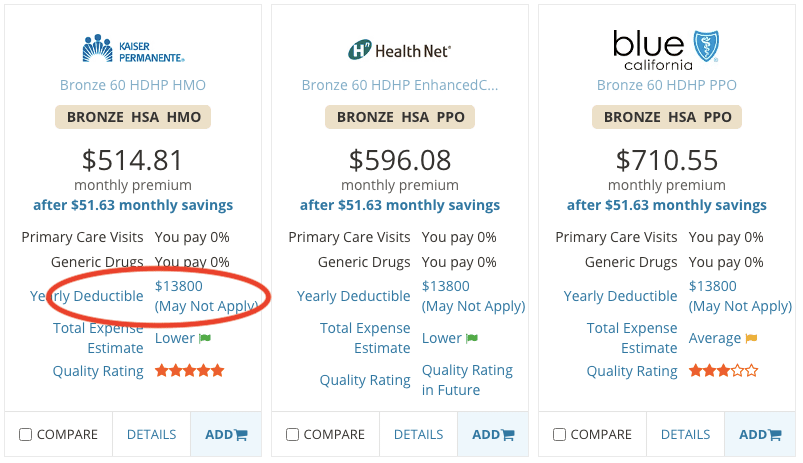

Another option I have is to decline medical coverage through my employer and look for a cheaper health plan elsewhere. Covered California is a program under the Patient Protection and Affordable Care Act. It provides tax credits to offset private health insurance costs depending on your income level. My household size (2) is eligible for some credits, as long as our income is under ~$100k.

Using their quote tool and an example income of $70k per year, here are the HDHP options available for my family coverage …

Although two of these plans have a lower monthly health insurance premium than my new work options, the deductible is much higher… $6,900 per person, or $13,800 for our family max. Saving a few thousand in one area seems to just cost us more in the other.

Surviving Without a Health Insurance Plan

Health care is a sensitive subject. So before going on I want to acknowledge how lucky and blessed my wife and I are to have not had any major health or financial problems the past few years. It’s unfair that some people are born healthy, while others have continuous medical problems. Our decision to be uninsured was one based on our personal risk tolerance and financial situation, not because we think we are immune to health issues. Our chances of unexpected health disasters are the same as everyone else our age/sex/race etc.

When I quit my corporate job in March 2018, I got a letter shortly afterwards explaining my options for COBRA (Consolidated Omnibus Budget Reconciliation Act). This was basically an option to continue paying for coverage at my old employer’s insurance rates for up to 18 months. The problem was, this rate was $1,600 per month and had more coverage than what we needed! I never realized how much my employer covered while I was working there — something I will pay attention to next time for sure!

My wife and I declined the expensive COBRA option and planned to look at cheaper alternatives, and possibly short term health insurance to cover us for a few months in case we started work again. After searching around a little bit, it became a lower and lower priority. Weeks turned into months, and we realized we could probably stay without insurance for another year. Paying out of pocket was just easier and proved to be cheaper.

Out of Pocket Costs

Since mid-2018, we’ve paid a total of $1,190 for medical services and care. (We’ll also pay an additional $2,890 total in fines for having no health insurance in 2018 and 2020). So about $4k total so far.

Believe it or not, the $1,190 in care included a 1-day out-patient surgery for my wife, about 10 clinic and doctor visits, and a few physical therapy sessions. While traveling in Africa I got pretty sick with a fever, but thankfully recovered naturally by staying in bed for 2 days. My wife and I also both got bad bronchitis while traveling in Australia — but thanks to the awesome clinics down there we recovered with antibiotics that cost less than $20, and a lot of rest. We’ve been extremely lucky.

Local clinics and student medical facilities were pretty easy to find in Los Angeles. We didn’t qualify for Medicaid … Even though we were unemployed most of 2018-19, our income exceeded the Medicaid limit (Max of ~$22k for household of 2). But, since our income was still considered “low”, we qualified for other financial discounts and programs. I didn’t know these even existed. This is how we got my wife’s surgery so cheap. Our local clinic referred us to a hospital that had crazy cheap financial plans and offered discounts to lower income households and people without insurance.

I was a little skeptical at first about the level of care at small clinics but quickly found that the services were on par, or better, than regular physician offices I’ve been to in the past.

Healthcare Blue Book is an awesome website that shows typical and “fair” medical costs for all types of procedures, lab tests, and medicines. Check it out if you find yourself wanting to estimate your out of pocket costs, or want information to negotiate a ridiculous medical bill.

Health Care and Retiring Early: What Should We Budget for the Future?

Our lack of insurance can’t go on forever. As my wife and I get older, our health risks increase, and insurance will become more and more valuable. Having no insurance was always a temporary decision. Same with dental insurance, and vision insurance (and maybe pet insurance for Cooper!)

What will the costs be in the future? What do I put in my future budget and how do I calculate my FIRE number to cover my future needs?

Health care is my biggest unknown. As a placeholder, I put in $10,000 per year for health care just so I could have a line item in the budget. Now I’m thinking this number is horribly low. Even if we do get cheap or subsidized care during retirement via Medicare or Medicaid, there’s still a lot of costs involved and potential disasters.

I haven’t figured it all out yet. I’m no expert. My wife and I will be working for at least the next 5 years, so we have time to make changes and adjust the budget as needed. Our FIRE number is a work in progress.

Important Considerations I Didn’t Cover Fully in This Post

- HDHP plans allow you to contribute to an HSA account (Health Savings Account). HSAs are probably the most tax efficient investment vehicle, available only to those with HDHP plans. So if I utilized an HSA, my overall “costs” for insurance could be lower.

- If I went with my employer-sponsored health insurance, the premium would come out of my paycheck on a pre-tax basis. So in my comparisons above, the annual premium would be slightly lower because it’s not counted in my taxable income. Actual savings depend on your tax rate, and ours will be probably pretty small in 2020.

- No matter if you have insurance or not, a large emergency fund is necessary to cover out of pocket costs and deductibles. I’m calling this out because even if you have insurance, you can still have huge medical bills just meeting the deductible.

- Care costs included in my examples were all estimates provided by my benefits website. In reality, prices are different from doctor to doctor, provider to provider, and sometimes “cash” prices are cheaper or more expensive vs. pre negotiated insurance rates. Many costs are even negotiable. Healthcare Blue Book is a wicked resource for specific cost estimates!

TLDR & Summary

- Woohoo, I qualify for health insurance through my work!

- But it’s still expensive … family coverage will cost $8,400 per year, with a $4,500 deductible each. Boooo.

- Medical insurance might not be worth the cost if you are young, healthy, or have low income.

- Wife and I survived on no insurance for a few years for ~$4k. We are lucky.

- Health care is tough to figure out for early retirees. More to come one this!!!

Get blog posts automatically emailed to you!

The UNaffordable Care Act tripled our premiums in 7 years & the deductible went from $2500 to $7500 per person.. Last year our out of pocket medical expenses were $28,000 WITH insurance thanx to high premiums & high deductibles ($7500 per person) for knee surgery (him) & skin cancer out patient removal (me). When the premium hit $2000 per month last Oct we were forced to drop it. as the premium/deductible/co pays continue to climb every year. Our solution: we retire 10/13 to Panama. $250 per month medical insurance for both of us with 80/20 co insurance & $500 deductible. Last year’s USA insurance was 30/70 co insurance!! Dr visits in Panama are $2 in a public hospital or in office $12-$15 without insurance (my dr charges $165 office visit here)!. Specialists $20-$40 depending on if you go to a hospital or private office. No dr referral to get blood work.. Just go directly to the lab. Pay $40 & get same day results. Bye bye crazy USA medical costs! As you get older, it will only increase. Our prior insurance had a $150 co pay to see a specialist & $1000 to walk into the ER. Glad to put all this behind us next month.

Hey Debbie. I have a friend that lives in Los Angeles and drives across the boarder down to Mexico for dental work. Cheap, quick, and he makes a fun vacation out of it. It’s cool to see people think outside of the box to get cheaper and more convenient healthcare outside of the US. But it’s also not an option for a lot of people who can’t retire yet or can’t uproot their family to move. Congrats on your retirement and good luck with the move! I’ve never been to Panama but I hear it’s awesome!

Healthcare costs and health insurance costs are ridiculous. I have been fortunate to have better (less expensive on a premium basis than yours) plans through my employers.. I don’t think my risk tolerance could handle not having it. I don’t have any serious chronic issues, thankfully, at least yet (in my 40s). I take a few prescriptions and do preventative visits. That being said, it’s knowing that if heaven forbid, I was diagnosed with a major illness or had a major accident, the costs could wipe out my savings. I once slipped on grass and broke my leg while traveling for work (so it ended up being covered by workman’s comp in this case) but the costs were astronomical. I don’t remember the exact number but something on the order of $100k without insurance. My friend was in a very bad car accident with her sister 2 years ago. I don’t know the cost but it required major rehabilitation and stay in a facility in addition to hospital stays and surgeries. Her sister was worse, and had inadequate insurance which limited her care options and cost more. To add to that, she had to stop working. So, what enough is to have in savings to make it ok to not have insurance? Not sure! All that being said, I always take the high deductible plans and contribute a lot to the HSA to reduce my taxable income.

Thanks for sharing Christine – It makes a huge difference having great employer plans. This is something I probably took for granted in the past and didn’t pay attention to at my old employers. I’m glad you know your risk tolerance, it makes it an easy decision and protects your wealth. The HSA is very attractive so I’m glad you are taking advantage of that too!

You think a surgery will cost $30k total but you need to factor in that the doctors will charge $$$ for poking their heads in the room. Each bandage and scan, and medication has its own separate charge. Suddenly you’re stuck with an outrageous $500,000 bill that neither you, nor the hospital, nor insurance wants to pay…

Yep, it’s crazy how fast things can add up unexpectedly. These figures were estimated from my benefits website but I am very aware that things increase drastically in some cases!

Wouldn’t it make sense to separate insurance for you and your wife? You are only $160/month through your employer, which means she’s $540. Seems like it would be worth running the numbers on the marketplace for just her and going that route.

Also, given your youth and health and record of low medical needs, your odds of needing to meet one deductible, no less TWO, are pretty darn low. What about just having enough to cover one deductible in full in an account earmarked for that?

Hey Katie – yes there is that option. I could do the $160 plan for myself, then enroll my wife in Covered California for $370/m with Kaiser on a Bronze plan. It’s still a pretty horrible deductible for her plan, but at least it’s $170/m cheaper if we never use it.

Medical insurance costs and no proper maternity leave makes the US a really bizzare country.

I think we’re making some good progress on increasing maternity leave and companies sound a lot more flexible there. (at least that what I hear from the places that my friends work at). The US certainly has a bunch of pros and cons and yes it’s very bizarre!

The situation you didn’t consider was something like cancer, where you are looking at months if not years of expensive treatment and total bills in the six figure range. Is it likely to happen? No–but the purpose of insurance should be to protect you from the unlikely,not to serve as a bill-paying mechanism for the likely.

Thanks! I agree that insurance can’t be looked at using a ROI mentality for financials only. It’s to protect against the big disasters like what you mentioned. Thinking about cancer scares the shit out of me.

Yup, $13,000 is pennies in the world of healthcare. My mom was on Medicaid when she got cancer and they still came for her house after she passed to cover the six figure bill, which did not include hospice, etc. Heck, a healthy unplanned pregnancy will now put you into five figures!

My husband and I are young(ish) and very healthy, but I’ve seen enough situations amongst our peers that I couldn’t comprehend going without insurance. One lump, one unexplained headache, one stranger making a poor choice and you could instantaneously be facing bankruptcy.

Thanks for sharing GJ, and I’m so sorry to hear about your Mum! What scares me most is that even with Medicaid insurance she got stuck with a massive bill. I’ve heard horror stories like this where insurance refuses to pay for whatever reason. Scary stuff! I’m so sorry!

When my wife was getting surgery last year, I had 12 hours to kill waiting in the hospital… So I went down to the finance services area and read all their brochures and stuff. For an unplanned, uninsured, pregnancy my wife and I would be out of pocket about $5k. I was shocked at how cheap this hospital was for having a baby! This covered 9 monthly visits, the delivery and 2 days in hospital, and some after delivery visits too. I wish I kept the brochure, I could share it. I’m not saying this is an ideal and perfect plan – I just wanted to know how much $ we’d be up for if we accidentally got pregnant. It *might be* cheaper than most people think. Then again, it might not.

Sounds like the brochure covered a vaginal birth that results in a healthy baby and mama. ;)

It’s the premies, c-sections (US stats are terrible), maternal complications and NICU stays that are $$$ and almost entirely out of your control.

Yep – I hear ya. Brochures usually show lowest prices and best case scenarios. Cheers!

I hate to be somewhat blunt about this, but it might eventually be worth looking at other employers in the long term. Between the 401k and the medical it sounds like the benefits at this company are terrible. I’ve actually never seen “benefits” this bad anywhere that I have ever worked. My premiums are around $30 every two weeks for a HDP at my current employer, lower at previous employer, and a tiny bit higher at the employer before that. I know different states and different employers cover things at different levels, but still.

Hey J – that certainly crossed my mind. In fact this is why Barista FIRE exists. Because companies like Starbucks will let you work part time and offer wicked medical insurance plans. So glad to hear you’ve got a great plan currently!

I’m passionate about this topic. I’m single with no kids. I haven’t had health/dental insurance for over 12 years. I pay cash for all medical expenses.

Most people think sickness is inevitable, but that’s simply untrue. I eat a strict organic diet and know how to keep my immune system operating at its highest capacity. I spend ALL my money on high quality food and supplements.

Insurance doesn’t actually cover good health care. Let me explain. When I got into nursing, I was fortunate to be introduced to functional medicine at the same time I went into allopathic, conventional care. In functional medicine, I saw people get healed of advanced cancer (no chemo, radiation), autism, diabetes, autoimmune issues, etc. On the other hand, I saw people get sicker and sicker with allopathic, conventional medicine. Most doctors just throw pills at you and are CLUELESS about nutrition/diet. I had to leave nursing after 13 yrs because it was too depressing.

A lot of stuff in functional medicine isn’t covered by insurance. There is a top holistic hospital named Sanoviv. They are light years ahead of anyone in treating advanced cancer. People that have been told (with cancer) “there is no more hope for you, plan your funeral” have gone to Sanoviv and reversed everything. Their cancer program is SEVERAL thousands out of pocket. Is it worth it? Of course.

I know a lot of stupid people say “What about accidents?” I don’t think like that. That’s not a right way of thinking.

Even when I start to have children, I will use a midwife. A hospital is one of the most dangerous places to have a baby. Again, to have a midwife/doula is out off pocket.

This is an interesting perspective, especially from a nurse :). Nutrition/diet have a lot to do with staying healthy and my wife and I try our best for that. But it can’t save us from the horrible stuff, which still can happen.

I didn’t know about that place in Sanoviv. But I hear a bunch of stories where people leave the US to get different opinions, better care, and/or cheaper costs for healthcare! Thanks for sharing, Angie!

“I don’t think [about accidents]. That’s not a right way of thinking.”

So you advocate against homeowners, renters, business, auto, life, disability and any form of health insurance?

Yes, based on the math. The product they are selling is at to high of a margin. How do we know that. Have you driven by state farm and or look at a insurance agents car. They are making too much money on the product they are selling

“Most people think sickness is inevitable, but that’s simply untrue. I eat a strict organic diet and know how to keep my immune system operating at its highest capacity. I spend ALL my money on high quality food and supplements.”

Lol you are so cute. Better hope that tip-top immune system doesn’t turn on you and start attacking your body like mine did. None of us get out alive.

This is why I hate the US health care insurance. You pay a premium, deductible, copay and you may still have to pay some more out of pocket. Health insurance companies should never be publicly traded because they would only care about making their shareholders happy (translation: screwing their customers).

Having lived in other countries with national health insurance, I’d prefer something. They’re already deducting premiums out of my paycheck, why not just change it into a healthcare tax based on your income?

I know people have their own opinion about insurance. There should be hybrid system like a national healthcare insurance so that everyone has coverage up to a certain amount. People who wants additional coverage can purchase it through private insurance, like how Medicare works now.

Yep, it’s frustrating to see rising costs and shrinking value over time. It’s also sad that I am one of those people profiting from the system (as a shareholder/investor in HC companies). Definitely a complex problem to solve!

Here’s a real quick solution to this problem. Since you are a mobile worker (make content, from anywhere with an internet connection), you should move to a Northern Country. Canada, Norway, Sweden, etc.

Because this is just another reminder that this system is broken. F’ing broken. Like let it die, grow a another system from literally nothing and it would be better than this. Because that system would figure out that the costs shared across the system are better having it concentrated on a few individuals with ridiculous markups.

I had to have a scan a few years ago (twisted an ankle real real bad and thought it was actually broken, one of the worst of my life from a guy who does it randomly, not even on purpose once ever 6 months), and the hospital visit plus scan cost me nothing out of pocket, probably less than 0.1% in my taxes that i already pay, and even if it wasn’t covered by my Provincial Plan (hint) it was going to be about $56

Hey Steve! My wife and I talk about moving to Australia sometimes (I was born there, so kind of makes some sense). But, we also kinda think running away from our country problems over here, might just be running TO an equal amount of different problems over there. If the solution was that easy, we’d already be doing it :)

My lung collapsed at the age of 22 while walking down the hall at work. In a private hospital for 7 days after emergency room surgery. Cost for me was a low ball/very generous $2500 deductible at the time, but I was working for the federal government, would have cost me $35,000 minimu otherwise,

Wow I’m so sorry to hear you went through all that. Insurance for the win!

Healthshare’s are pretty cheap… Since you are paying OOP anyway you should be able to float the 90 day reimbursement times. I did it when I was self employed, Healthcare costs dropped from 1500 a month in premiums +13100 deductible, to 450 a month with a 1500 deductible (family plan). Was actually pretty decent all things considered.

Wow what a killer saving! Thanks for the recommendation!

Premiums can get expensive. But you have got a LOT to lose.

I direct your attention to an article on this site. (coincidentally written by yours truly):

https://budgetsaresexy.com/why-work-so-hard-to-build-a-fortune-and-not-protect-it/

Insurance is the only thing that prevented a serious accident from becoming a financial buzz-kill for me.

Thanks Gene. I needed to read this. I’ve had 2 motorbike crashes in my life – both in Australia where the care and ambulance was free – (I also wasn’t at fault). Nothing as bad as yours though! Wow. $180k saved – plus wages is no chump change. I’m so glad you had the extra coverage!

I do like insurance, in general. I have policies for renters, landlord/property for all my rentals, umbrella liability and auto with the highest limits available. What kills me is the premium for health. It’s more than all my other 8 policies combined. Maybe I need to read more stories like yours… Just that knee xray photo makes me cringe!

What an interesting way to look at this! Love your comparison. I’m the Doc who worked with J on this article previously:

https://budgetsaresexy.com/direct-primary-care-dpc-a-health-insurance-option-worth-looking-into/

And a local Direct Primary Care practice would save you hundreds if not thousands in scenario #1 (and the other scenarios as well), and might help make up for the pain of that monthly cost for HDHP. DPC is better for doctors and patients alike, and is the only reason I’m able to be such a happily practicing physician! Less expensive + better care means a lot to me. Locations from around the country are included here:

https://mapper.dpcfrontier.com/

Thanks Dr Rachel! This is great info I love seeing all the alternative types of care. I see there’s a place close to me – looks like mostly preventative stuff included – what about the horrible scenarios where specialists are needed? I’m guessing I just get referred from there?

Thank you!

I think you’d be surprised by how much a good family doc can manage – we’ve gotten a bad rap lately, with insurance companies mandating how many patients we have to see in a day in order to get paid. Most family docs don’t have the time to use all the skills they were trained to have. With an hour to see a patient, I have plenty of time for a full joint exam, to discuss exercises and stretches to help, to apply a cast – to go through a thorough history and maybe avoid a specialist at all.

Bit late getting to this, but scenario 3 is not the bad year. My bad year was mysterious breathing trouble with 3 ER visits, 6 CT scans, 3 MRIs, 11 specialists of different flavours, 2 ultrasounds, a VQ radiation scan, 3 full pulmonary function tests, a bronchoscopy, a lung biopsy with a common complication resulting in a week in ICU and another week in hospital. That’s well into 6 figures and all of that was just to diagnose what the problem was.

My sole wage earner dad’s bad year was back pain resulting in an 8 month in-hospital stay in an isolation ward for leukemia bone marrow transplant at a cost of well over a million dollars in 1991 dollars.

You are not insuring for the day to day stuff which is definitely cheaper to pay out of pocket. You are insuring for the catastrophes so you can 1) get treated instead of dying or becoming disabled and 2) not go bankrupt.

Thanks Caro! These stories scare the shit out of me. I’m really sorry you and your Dad had to go through those tough years!! A good update – I have do have health insurance now! :) Thanks for reading :)