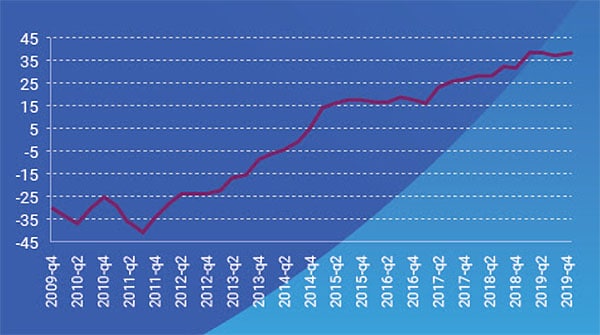

The AICPA just came out with their latest Personal Financial Satisfaction index (PFSi), and looks like it reached an all-time high of 40.2, suggesting that people are generally *happier* with their finances compared to the past 10 years of tracking.

Do you find the same is true for you?

I’ll hit you with my own set of indexing questions in a bit so you can gauge better, but first – more about this PFSi so it’ll make more sense:

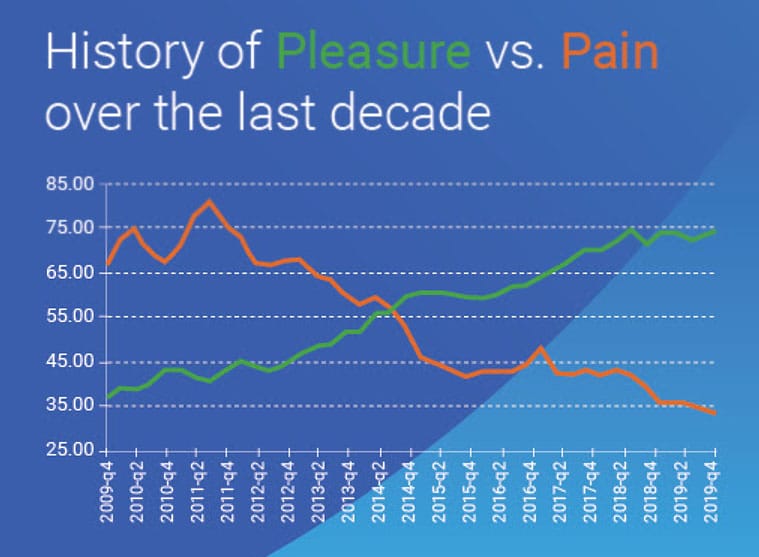

The PFSi is a quarterly economic gauge that measures the personal financial standing of a typical American. The index is calculated as the Personal Financial Pleasure Index (Pleasure Index) minus the Personal Financial Pain Index (Pain Index). These sub-indexes are each composed of four equally weighted proprietary and public economic factors which measure the growth of assets and opportunities in the case of the Pleasure Index, and the erosion of assets and opportunities in the case of the Pain Index. A positive reading of the PFSi indicates that the average American should be feeling more financial pleasure than pain and thus have an overall positive sense of financial satisfaction.

So basically, it uses data – not surveys – to figure out the probability of people feeling good or not about their money.

Which as a personal finance enthusiast I don’t necessarily put much stock in since WE’RE the ones in control here more or less regardless of what the world is doing, but it’s still interesting to see and play along with ;)

Here were some other findings comparing the past 10 years of the PFSi:

- Underemployment is at an all-time low (compared to an all-time HIGH exactly 10 years ago!)

- The PFS 750 Market index* remains the leading source of financial pleasure

- Pain from taxes is the only factor that did not improve over the past decade (shocking no one, haha…)

(*The PFS 750 Market index is an AICPA proprietary stock index comprised of the 750 largest companies trading on the US Market excluding ADRs, mutual funds and ETFs, adjusted for inflation and per capita.)

And then here are some pretty charts saying the same ;)

Pretty nerdy stuff!!

And we’ll keep the trend going here with my OWN version of the PFSi – or what I call, the PFSiONE (Personal Financial Satisfaction Index of Number One).

This will really determine how happy or not you are with your $$$ ;)

Jot down how you feel about the following 8 areas compared to 10 years ago, and use the ranking scale of 1-10 where 1 is BLEH and 10 is HOT MAMA!

Then share in the comments or just ponder alone!

- Investments: __

- Financial Outlook: __

- Home Equity: __

- Employment Status: __

- Personal Inflation: __

- Personal Taxes: __

- Debts Owed: __

- Career Potential: __

PFSiONE Total Score: __

70+ means you’re on FIRE, 60+ shows you’re a growing flame, 50+ means you’re starting to flicker (see where we’re going with this?), and then anything under 49 means you need to be re-lit 🔥

I’ll go first, then your turn:

- Investments: 10 (was at $171k back then, now over $700k)

- Financial Outlook: 10 (getting closer to financial independence!)

- Home Equity: 7 (higher than in 2009, but not by much)

- Employment Status: 9 (I’m still blogging here, but don’t have a renewed contract yet!)

- Personal (Lifestyle) Inflation: 3 (bigger home, bigger yard, more kids, more animals, more food, more everything! (Though personal spending has drastically been cut down thank goodness))

- Personal Taxes: 7 (paying more, but also earning more)

- Debts Owed: 8 (no car or credit card debt anymore, but still have a honkin’ mortgage)

- Career Potential: 7 (technically this should be a 10, but I worry I may be losing my “hustle” gene the more I enjoy life in the real world vs the online one! (*gasp!*))

PFSiONE Total Score: 61 – a growing flame! With only career and kids basically getting in the way of my perfect score, haha…

Good thing they’re so cute!

How about you? Feeling good compared to this time 10 years ago? Anything really surprise you going down the list?

The inflation part def. threw me for a loop, wow… I’m doing SO MUCH better in my head compared to the reality! Haha… Life is sneaky!

Get blog posts automatically emailed to you!

Investments: 8

Financial Outlook: 8

Home Equity: 9

Employment Status: 10

Personal Inflation: 9

Personal Taxes: 10

Debts Owed: 10

Career Potential: 10

74! Excellent! I am on fire! Funnily enough, the only time I took numbers off were when “comparing and despairing” with those bloody Joneses next door!

HAH!! They couldn’t stop you all the way from “burning up” though ;)

Congrats on all that financial happiness!

Investments: 8

Financial Outlook: 9

Home Equity: 9

Employment Status: 7

Personal Inflation: 10

Personal Taxes: 10

Debts Owed: 7 (Still have my mortgage)

Career Potential: 7

PFSiONE Total Score: 67

I feel good about my situation. I guess I am inflating my lifestyle because of another kid on the way, but that doesn’t make be feel bad. :)

They do inflate the *happiness* levels :)

This was fun!

• Investments: 10 – been a great ride

• Financial Outlook: 7 – what’s around the corner?…been a great ride too long?

• Home Equity: 10 – mortgage free

• Employment Status: 10 – RETIRED!

• Personal Inflation: 8 – Trying to keep it in check…

• Personal Taxes: 5 – never too low

• Debts Owed: 10 – Debt free

• Career Potential: 10 – Did I say RETIRED?

Happy with a score of 70!

You better have a 70!! Haha…

Good for you man. And I see you’re sharing the wisdom on a blog too! Going over now to check it out…

Investments: 10 (Net Worth up 187%)

Financial Outlook: 10 (Bucket Strategy, who cares what happens!)

Home Equity: 10 (paid off cabin in the woods)

Employment Status: 10 (FIRE’d in 2018!)

Personal Inflation: 10 (downsized for retirement!)

Personal Taxes: 9 (incomes down, but paying for those ROTH conversions)

Debts Owed: 10 (Nada, Zero, Zilch)

Career Potential: 10 (What’s a career? #ILoveRetirement)

PFSiONE Total Score: 79

Yep, I’m about as happy as can be. If I could only avoid those pesky taxes on my Before-Tax 401(k) rollovers to a ROTH! Great index!

I love that all early retirees are chiming in here, haha…

Cheaters! :)

Investments: 6 – I started too late to retire early but am on track to not have to be a Walmart greeter at age 80

Financial Outlook: 7- This could be my best income year ever, but I am also cognizant of the fact that half of the people over 50 will never get back to their peak income if they suffer an involuntary job loss

Home Equity: 10 – don’t own a home, which is exactly where I want to be right now. The long term plan is to buy a retirement home in cash.

Employment Status: 10 – the job is solid and stable

Personal Inflation: 10 – we downsized dramatically two years ago

Personal Taxes: 8 – I hate Trump, but his tax plan does mean I’m still deducting about what I did with a mortgage, without the mortgage.

Debts Owed:9 – owe about $4000 on a car that I could pay off tomorrow, but the loan is at 1.9% so why rush.

Career Potential: 5 – I’m old :)

65 – seems legit!

Super legit :)

Way to rock that downsizing!! I’m jealous!

Congrats to the commenters so far who seem to be doing so well! Here is a response for those of us on the younger side who are in the thick of it:

Investments: 3 (Defined-benefit pension and TFSA contributions)

Financial Outlook: 3

Home Equity: 0 (I rent)

Employment Status: 8 (Full-time permanent government position, moderately happy)

Personal Inflation: 9 (Living within my means)

Personal Taxes: 10 (Not sure how to rate this. Gladly pay my share of taxes)

Debts Owed: 3 (Low-interest student loans, $27k remaining. No other debt.)

Career Potential: 10 (Solid career trajectory and higher salary to come)

I feel like you need to add a 5 or so even for renting (we’re pro renters here!), and maybe even a 5 or 6 to debts owed too. $27k is a lot, but low interest and going towards something IMPORTANT is def better than nonsense out there…

But yes – very good to hear from people in the trenches more for sure :) thanks for sharing!

Investments: 10 – IRA is growing and Stock portfolio is generating 10K in dividends

Financial Outlook: 10 – Retired at the end of 2019, don’t foresee any issues

Home Equity: 9 – only have $43K left to pay off.

Employment Status: 10 – RETIRED! (I’m 62)

Personal (Lifestyle) Inflation: 5 – Not sure what we will be spending money on yet, but I really don’t see us blowing the budget or anything.

Taxes: 8 – Since the new tax law we’re finally getting refunds vs. paying $$$ (But I don’t mind paying my fair share)

Debts Owed: 8 – 1 car payment and 1 house payment

Career Potential: 1 – Since I’m retired, don’t see any new Careers around the corner, but that is what I want.

Haha… The only area where “1” is actually good ;) Congrats man!

Investments: 10 – have you SEEN the market over the last ten years holy cow

Financial Outlook: 10 – our jobs are secure, so if the bottom drops out we can just buy low

Home Equity: 10 – refi’d in 2015. We owe $128k on a place valued at almost 3x that

Employment Status: 5 – my job is a black hole of turn-off-my-brain-and-grind for 40h a week, but I’m probably paid more than I should be

Personal Inflation: 8 – we dedicated frivolous spending to 401(k) plans and regret nothing… but own a house and all associated nuisances

Personal Taxes: 8 – tax rates are at all-time lows; frankly at our income we should be paying more

Debts Owed: 9 – mortgage will be done in ten years!

Career Potential: 2 – I have lost all interest in working for a living. Thanks, FIRE. :P

PFSiONE Total Score: 62

…I’ll take it!

You just had to one up me…. again :)

Investments: __8 and still investing–positioned to do so until RMDs kick in

Financial Outlook: __10 about to “retire” from public ed and go to work elsewhere to doubledip

Home Equity: __6 or 7 1/3 of my home is equity based on current market value…my only debt

Employment Status: __10 AWESOME…retiring career educator with a 6 fig pension AND I’m about to do a second career

Personal Inflation: __6 or 7 some lifestyle inflation but I am getting it tamped back down

Personal Taxes: __5 still pay too much and will due to bad investment planning in my youth

Debts Owed: __7 only have the house which should be paid off in 4 years

Career Potential: __10 retiring from career one and don’t “have” to work but will start a great second gig

*Divorce is a killer but I’ve back where I was and the future is bright!

Score: 63 all this is subjective but I will take it and feel pretty good about it

Oooohhhhh what are you thinking for that 2nd career? Going after any old dreams of yours, or just trying something new?