Whelp – another month, another financial temper tantrum! Haha…

Between the markets and our recent home buying expedition, our spreadsheets don’t know what to do with themselves ;)

Look at this thing:

A delta over $130,000 so far! Only to be off by $40,000 in the end! Although at least it’s off in the *positive* territory and not the opposite… for now ;)

Still – they can try all they want, but they’re not about to scare me off yet! ‘Tis only a blip on the path towards freedom, and I have a whole new mission to set my sights on now!

To pay off all this new $269,600 of death debt!!

That dang house ruined my 17 month reign of being debt-free – dag nabbit! Now it’s going to take me forever to get back there again, haha…

But I accept you, Challenge ;) Big risks for big rewards and all that, right??

A few juicy nuggets about this mortgage stuff before we get to the net worth break down…

- We took out a 30 year fixed loan after debating on whether a 15 was better or not for us (my gut really wanted the 15, but after a healthy discussion with the wife, and factoring in my tendency to change things up every 6-12 months, we opted for the more “responsible” route in order to give us maximum flexibility and peace of mind… Though we still very much plan on paying it off in 15 years, and probably even less.)

- It came out to $269,600 with an interest rate of 4.25% (not the best in recent months, but more respectable than our 6.75% back in 2007!)

- The mortgage servicer has already changed hands! (I.e. packaged it up and sold it to another mortgage servicer probably for a tidy profit, haha…)

- We haven’t gotten any statements or payment requests yet – that starts July 1st (which is actually nice, since we’re still paying rent until the end of June)

- And for the time being, we’ll be keeping the *value* of our house the same as our purchase price in our net worth reports since that’s literally the market value of it right now ;)

- Also – we’ll be keeping both the *house* and the *mortgage* in our reports since we like to have an overall snapshot of our finances, especially regarding such large items… So you’ll see the house listed in the asset section, while the mortgage is in the liability one – effectively accounting for our “equity”.

Here’s how the month of May broke down…

[This is part #136 of our Net Worth Series, where we share our real life #’s every month in hopes it motivates YOU to track yours as well – no matter how scary or awesome it gets ;) And hint: the more you pay attention, the more awesome it gets!!]

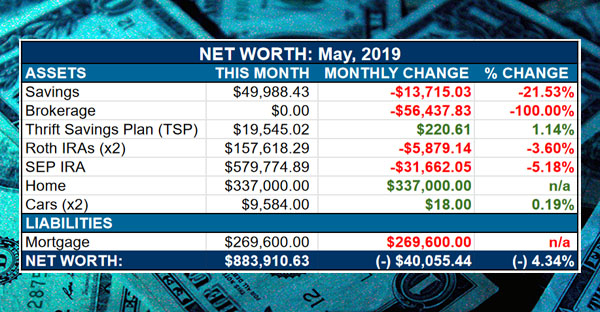

CASH SAVINGS: $49,988.43 (-$13,715.03) — A punch to the gut there as we give up some funds to help pay for closing! On top of liquidating our brokerage account as you’ll see below as well… Which at least is all going towards equity, but still not nearly as sexy as cash ;) But that’s how the game goes!

BROKERAGE: $0.00 (-$56,437.83) — Bye bye brokerage account – it was nice having you around for a little while, haha… But love that we started with a one-lump sum of $50,000 and got back an additional $6k! For doing absolutely nothing at all! Of course it could have gone the other way too with this market, but hey – we’ll quickly take the win and count our blessings :)

THRIFT SAVINGS PLAN (TSP): $19,545.02 (+$220.61) — A nice gleam of light amidst the sea of destruction! Haha… And only because the account’s too low still for the swings to overcome my wife’s bi-monthly contributions :) But again – you take all the wins you can get! And the dollar cost averaging doesn’t hurt either – for ANYONE who remains calm and collected throughout!

ROTH IRAs: $157,618.29 (-$5,879.14) — A fairly big chunk taken out here, but apparently my wife’s funds over at USAA are performing better than our Vanguard indexes during this current period which is interesting. That’s why you see the difference in % losses here – we still haven’t moved her IRA over, although for some reason we’re also not in a rush? I think it’s literally just because I keep forgetting haha… And it’s also a smaller portion of our funds so haven’t really prioritized it. Not that either of those are good excuses :)

SEP IRA: $579,774.89 (-$31,662.05) — Now this one’s the whammy! Ouch! You could pick up a brand new minivan for that! ;) Though of course none of it truly matters until you cash out, which we don’t have any plans on doing anytime soon…(although I *have* promised my wife that that van is coming her way, which I still need to make good on!)

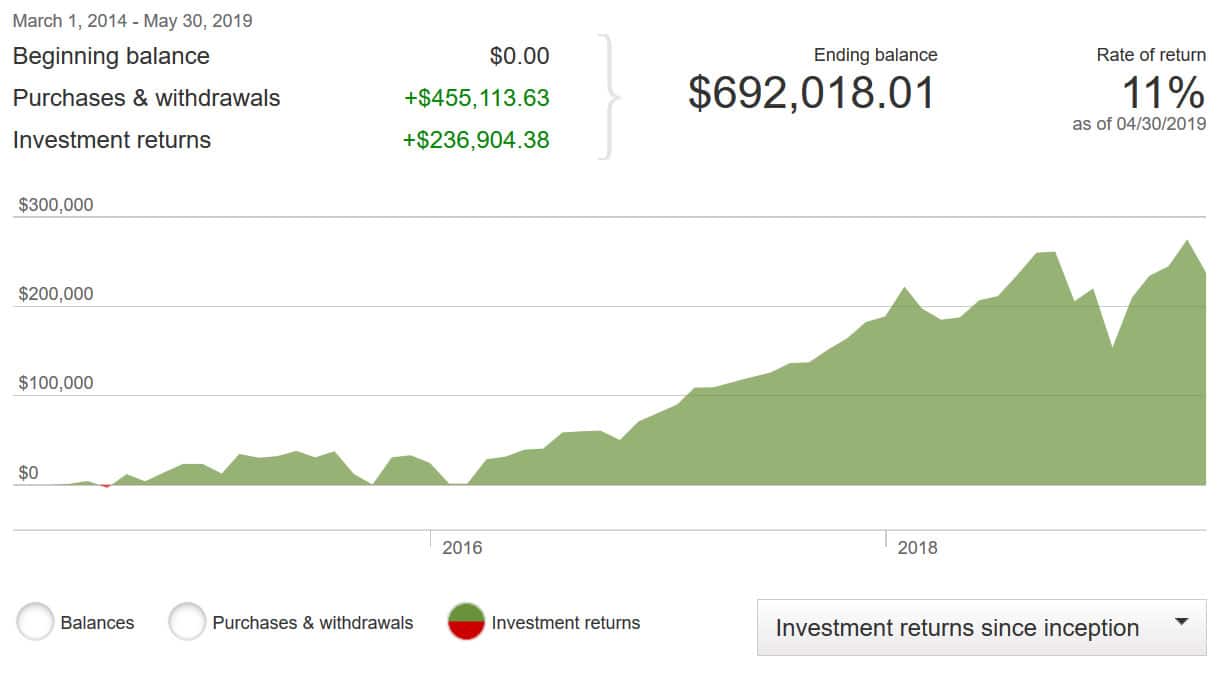

Here’s how our investments have fared over the years since moving over to Vanguard:… All the money here is in their VTSAX fund as I haven’t cheated on them and moved ’em to Fidelity ;)

HOME VALUE: $337,000.00 (+$337,000.00) — BOOM! Instant diversification! Haha… Though would have been much more fun if it didn’t come along with some debt ;) Still, we’re finally out of pure stocks as investments, and now have a little equity under our belt to help balance stuff out a little more…

Should be an interesting journey as we go along here as it’s been a number of years since we last tracked this stuff. And as I mentioned above, we’re going to leave the value here the same at least for a while (the end of the year?) and then re-asses from there… Last time around we hit up our realtor every 6 months which we found to be more accurate than Zillow, so we’ll probably do the same thing this time as well. Either way, it’s nice to know at least for *right now* what the house’s true market value is! I.e. whatever the amount someone is willing to pay for it! Which was apparently $337,000 for us! Haha…

CAR VALUES: $9,584.00 (+$18.00) — The second month in a row our cars have gone up, but I don’t challenge KBB’s algorithms! Haha… Toyota must be brewing something up over there! :)

The values of both our (paid off) cars:

- 2008 Lexus RX350: $7,018.00 (+$13.00)

- 2005 Toyota Corolla: $2,566.00 (+$5.00)

MORTGAGE: $269,600.00 (-$269,600.00) — And lastly, the DEBT, Womp womp womp… On the plus side, we’re already 20% paid off now! WOO! More than even our first house when all was said and done after 10 years! So we’re making progress, haha… Now to just get my mind right all the way… :)

Total change in net worth this month: (-) $40,055.44

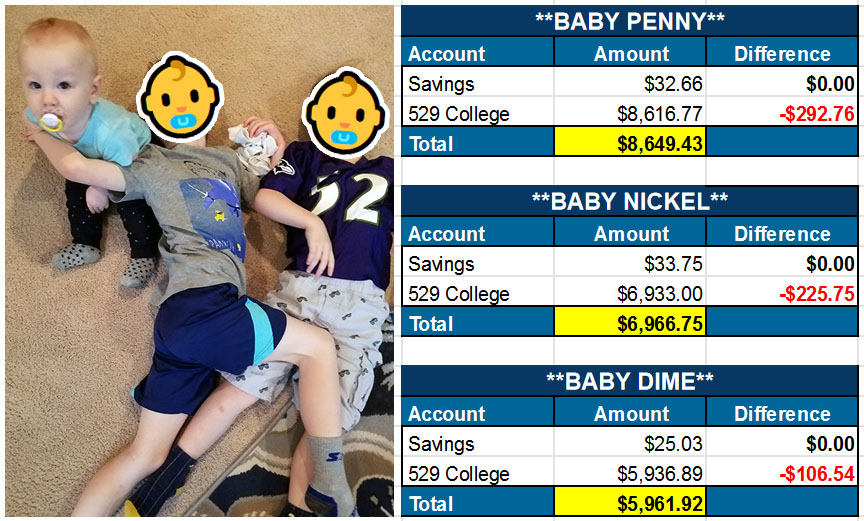

And as always, here’s a snapshot of how our kiddos are doing too…

I still can’t believe the markets treat babies like this ;) Is nothing sacred anymore?!

[Some babies aren’t babies anymore!]

How’d you guys do this month?

Anyone cross a milestone or become a millionaire for the first time?! Anyone become a millionaire and then quickly have your millionaire status revoked? ;)

Every time I get close we get a huge push backwards, so I’m not even thinking about it anymore, haha…

I feel like a million bucks anyways, and that’s all that really counts! ;)

See ya down in the comments,

![]()

PS: If you’re just getting started in your journey, here are a few good resources to help track your money. Doesn’t matter which route you go, just that it ends up sticking!

- The "Budget/Net Worth" spreadsheet - the colorful Excel template I personally use.

- The "Money Snapshot" spreadsheet - a simple Excel template I created for my former $$$ clients

If you're not a spreadsheet guy like me and prefer something more automated (which is fine, whatever gets you to take action!), you can try your hand with a free Empower account instead (formerly Personal Capital)

Empower is a cool tool that connects with your bank & investment accounts to give you an automated way to track your net worth. You'll get a crystal clear picture of how your spending and investments affect your financial goals (early retirement?), and it's super easy to use.

It only takes a couple minutes to set up and you can grab your free account here. They also do a lot of other cool stuff as well which my early retired friend Justin covers in our full review of Empower - check it out here: Why I Use Empower Almost Every Single Day.

Get blog posts automatically emailed to you!

Sorry to see such a big chunk of value being chopped off. But in the form of stocks, luckily it usually bounces back after a while!

Like you said, it matters when you cash out.

I didn’t cross any milestones, but I just had to point out that I made a Net Worth update and arrived at 880k as well!

https://www.thewealthyfinn.com/2019/05/how-we-grew-our-net-worth-to-900000-by.html

(I rounded the title )

We have a large mortgage as well, but I’ve just deducted the debt from the house value for simplicity. It’s the only debt we have.

Or would it be simpler if it was separate?

Oh wow – we are close, however if you came over here and converted your € to our dollars you’d win it with millionaire status ;)

Fun post to read though – love all the graphs you put in it!

Always a good read. Thanks J Money! Also one of your poppets doesn’t have a sticker covering their face. Just thought I’d let you know in case it got missed.

Oh, yeah – I’m okay with baby faces here but once they grow up and actually look like humans I convert them over to anonymous status :) But thanks for the note! And glad you’re enjoying these!

Google Photos groups my kids’ infant photos with their teen photos. I’m good with that, but if you want to remain anonymous, you should probably anonymize them now.

Freaky!! Thanks for the tip!!

I got up to $527,000 (+$2,000) before falling back down to $517,000 (-$8,000 since the end of last month, -$10,000 from my daily peak).

In good news, I paid off my house. After four years, I’m debt free again.

OH DAMN!!! Congratulations, G!! That’s huge!!

I’ve been tracking my net work for a year now. Even with the big hit in the market this month my net worth is up almost 18% in one year…

Power of tracking/paying attention right there – congrats :)

My wife has a jersey just like your kid’s — good taste. ;) Our mortgage is exactly half of yours at this point, with 11y left on a fifteen-year mortgage. I’m willing to bet you’ll beat us to the finish line, given your drive; our interest rate is nuts (in a good way) so we’re happy to make the standard payment each month and direct overage toward other things.

Like scraping and pressure washing and painting the porch. Which we spent all of the last two weekends doing, and we haven’t even gotten to the ‘painting’ part yet. Ahh, homeownership.

Oh jeez, haha… I spent about two hours trying to figure out the best way to mow our lawn this weekend! :) Should have seen me on that riding lawnmower though – i was zigging and zagging all over the place! Haha…

How much maintenance is required for the 2 vehicles as they are older? As my cars passed the 8 year mark, even with regular maintenance, it was just one thing after another, until I said enough is enough and sold my car.

Dang, sorry to hear :(

We haven’t had much back luck with our two here, or any of the ones before that really (knock on wood)… Just the typical oil changes and check-ups/new tires whenever needed… Although we did have to change the breaks a while back and that wasn’t cheap :) But for the most part we’ve had good luck and it seems most others do too in our community? That one post we did on 100,000+ mileage cars it seemed like everyone who reads this blog rocks old ones – and some up to 300,000 with hardly any problems! So who knows…. Maybe your next one will be a gem :)

My current car is awesome, cause I use the car share and I never have to worry about repairs and can choose the type of vehicle (hybrid, electric, van or SUV).

BOOM – there you go!!

Our portfolios took a dive thanks to the market – and thanks to a home improvement loan we took out to renovate the upstairs of our home… but it’s all good. We’ll pay off that home improvement loan pretty fast so I’m not too stressed about that.

Still, it’s always a bummer when you log-in on the first of the month and see that dip. :( Gotta remind myself we’re playing the long game, here.

Yep, totally..

And from those pics of your house you sent me the other day, the revisions you’re doing is looking damn fine, my dear!

You will have months like this. We sure have this month as well. Got spanked a bit with different expenses and that bit of a market decline. Keep grinding man!

-CJ

You too, sir!

All a part of the game!

I got a nice jump because it was a three-paycheck month, so by keeping my spending about the same I came out way ahead. I just missed the milestone of getting under $30k of debt (actually my long-term debt is under $30k, it’s just the credit card balance pushing me over), but while frustrating it’s kind of fun to just miss a milestone, because then there’s a chance to absolutely smash it the next month.

As far as mileage goes, I’m 1.5 miles from home, and there is nothing interesting 1.5 miles from home. Next month I should be in the park.

“it’s kind of fun to just miss a milestone, because then there’s a chance to absolutely smash it the next month.” – I always think that too!!! Haha… one extra month of excitement knowing you’re going to pass it the next one ;) Congrats!

Congratulations with the house. Getting a 30 year mortgage is a good plan.

Wow, all your money are tied up in the house and retirement account. That’s great for the future, but I guess no early retirement for you guys. :)

We were down about $30,000 or so in May. Let’s see how the market does in June.

We could probably figure out a way to early retire if we wanted to ;)

Those financial temper tantrums will end someday. Hopefully, we’ll see a big jump when that happens.

Congrats on the house purchase. Seems like a necessary move with all the Kid Moneys around.

I can’t believe you’ve been publishing these for more than 11 years now. That’s crazy!

Longest record of my life! Haha… can’t stop now :)

New net worth high of $948K for me. Up 6K from last month.

MAYBE $1250 of the increase was from investment gain.

The rest was from Zillow home value increase [2k], paying down mortgage[800], and pumping a third contribution into my 401k and HSA accounts this month [3 paychecks in one month – SCORE!].

I keep treading slowly upward. Still sticking with the “scared-y cat” portfolio: ~80% bond&short term index funds/~20% S&P 500 index funds. With this allocation, I’ve still been making acceptable increases in my NW almost every month. If nothing else, the volatility of my current allocation has been nicely muted compared to the market in general. I.E. I have been sleeping well at night. :)

While I know that low volatility isn’t the ultimate goal, I am only about 5-7 years from retirement and don’t want to lose all the recent gains I’ve made. Of course the sticky point is when to decide to change my allocation back to something more suitable for long term investing.

While I know that I am at risk of being accused of “heresy” for attempting to time the market, I will point out that in my head I’m not so much timing the market as I am value investing. I like looking at the “Buffet indicator” https://www.gurufocus.com/stock-market-valuations.php , but you can use Schiller too. Either measure shows the market is significantly over-valued. While that condition can and has gone on for extended periods, I think that there is much more down-side potential for losses compared for upward growth right now.

I would rather miss out on a little upward momentum, than incur a large loss this close to retirement. I can miss out on SOME market increase and still retire at my planned age of 53-55 ( I am now 48). But if the market truly TANKS, I would probably have to work several more years if I was heavily invested in equities. Given my retirement plans, my current allocation seems like the lesser risk for me.

Gene:

If it makes you feel any better, we are sitting 100% in cash. We keep an eye on the Buffett Indicator and Schiller PE Ratio, as well as some other signals. When nearly all our stocks are at their 52-week high, we can only believe that they cannot continue to go up. We may be wrong, but until we see some better buying opportunities we will hold our cash position.

Mr. SoS

You know, that DOES make me feel a little better to have some company. Thanks :)

I have also been taking solace in the 114+ Billion dollars Buffet is sitting on with Berkshire Hathaway.

If I happen to hear he is spending down that massive [77 MILE-high, if my math is correct] stack of Benjamins, I will begin to get more concerned.

Gene:

“Every decade or so, dark clouds will fill the economic skies, and they will briefly rain gold. When downpours of that sort occur, it’s imperative that we rush outdoors carrying washtubs, not teaspoons.” – Warren Buffett 2016 Berkshire Hathaway Annual Letter

We want to make sure we have the washtub available.

Mr. SoS

I hadn’t heard that quote before. I like it!

I second that!!

How do you do that from a practical perspective? The transaction costs for selling and then rebuying in a taxable account would have a material drag on returns. Also, research actually shows that time in the market is the most important factor for success. I agree w/ the keeping some dry powder in the case of a downturn, but trying to time the market with 100% of your portfolio is not a strategy supported by research.

J – thanks for being open about this. Congrats (or not?) on the home purchase. Am sure your wife appreciates. Curious. Why not include the value of your online assets? Perhaps this is too personal / not something you’d want to share – but isn’t that part of net worth? THx

I’ve thought about it before, but I kinda like it on the outside and just an “extra” since it fluctuates so much and who knows if I’d ever sell it all? If so that will make for a helluva addition that month, haha, and if not, well, then all remains the same :) I do include all the cash flow from it here though since it’s my “salary” so it’s not all excluded.

J$:

Congratulations on the house. Having the ability to put 20% down is huge. I still remember when we finally hit that 20% and stopped having to pay PMI. The funny thing was that our mortgage company sold our mortgage as soon as we reached that point. Now we have 40% paid off and we continue to chug along. We should have it paid off within the next 9 years.

Our net worth went up last month by just shy of 2.5%. This was primarily due to paying off the remaining $14,000 on our Home Equity Line of Credit (HELOC). Our next goal is to hit $1M in assets. We have $26K to go to get there. Dr. SoS’s business is doing better so we plan to set up a SEP IRA for her soon. That should definitely help.

Thanks for sharing your update.

Mr. SoS

Rock on!! I want an email (or blog post!) once you cross that magical number! :)

And now racing you to pay off that mortgage first, though something tells me you may win out on that front haha…

I will send an email. Hitting $1,000,000 in assets does seem like it may be blog post worthy.

You will really be hustling if you pay off your $269,600 at 4.25% before we pay off our $170,970.56 at 3.125%, but I am certainly up for a race. See you at the other end. I will be waiting for you with a towel. ;)

*** Goes to buy 100 Mega Millions Tickets ***

I’m a new follower, and it’s so cool to see how you have everything laid out. We were fairly responsible before (no debt except our house, which we hope to have paid off in 15 years from now, for a total of 19 years). Looks like our mortgages are similar (our was $272k at 3.875% in 2015). Thanks for posting, I’m excited to follow along!

Heyyyy nice to meet you, Mel!

So glad you’re enjoying this – thanks for taking the time to write! :)

going over now to check out your blog..

UPDATE: I love your topic!!!! Do you follow Bea Johnson from Zero Waste Home by chance??? She’s always talking about those R’s (except for the last one – Retire ;)). As a practicing minimalist myself I am alll about this stuff… and can’t wait to get back to composting too with our new home and land – I’ve already found a section or two that I’m pretty sure the former owners were using for theirs so that should speed stuff up! :) Thanks again for stopping by!

Thanks for checking it out! I didn’t follow Bea before, but I do now. I’m still a novice at this whole less-consumerism thing, though I’ve always leaned toward purging what I don’t need. I always appreciate a reference to some good information and sources, so thanks!

Composting is honestly so cool (and gross, honestly). I grew up with a compost bin, so I’m used to digging for worms. It just makes all sorts of sense to keep it out of a traditional landfill and use it for something productive, while reducing things like vehicle emissions for transporting the waste itself. I haven’t gone too deep into that on the blog because I need a lot more education on the topic, but I definitely think about it all the time! I hope to see some composting updates!

Sounds good!!! Looking forward to reading more updates from you as well :)

Hi J. Money. I’ve followed you for a while not but this is my first comment! I’m gearing up to buy a house in the next few years by starting to build my down payment of 20%. Since you’ve purchased a home recently, did you have any worries about the housing market going down in a few years given a few signs of a coming recession? Did you have worries that you’re buying at the height (or close to it) of the market before it’s predicted to fall a bit? I have this worry so I’m wondering how you overcame that.

Thanks!

YES TO ALL OF THOSE WORRIES! Haha…

And no – I haven’t gotten over any of it to be honest with you :) I DO think things are going to crash again and it’s not the best time to buy, but unfortunately in life you gotta do what you gotta do and sometimes that matches up well with the world and other times not.

So for us it was a *lifestyle* decision first (ie moving to the place we want to settle down for a while) and a financial one second. We could have prolonged it and hoped for better conditions, but in the end it wasn’t worth the trade off.

Happy June!

We took a hit this month too, Nicole & Maggie pointed out that the surprise drop was because of the tariffs (which I knew about and just forgot) so part of me feels a little pessimistic about the market coming back the way it should if the political shenanigans continues but I hope that that’s just unfounded pessimism. After all, the market has survived many decades of shenanigans …??

I keep reminding myself we’re in this for the long run. We can do this!

I hope what Toyota is brewing up is a fabulous electric minivan with great mileage for us ;)

ME TOO!!!! That’s next on our list to pick up – a new (to us) minivan! :) If you get it first you’ll have to tell me what you think and which ones SUCK so we can avoid! Haha… So far it’ll prob be between a Toyota Sienna and a Honda Odyssey.

I just recently closed on a refi from 5.5% to 3.875% on a 15 years..now it’s 3.2%!? Da fudge!!!

While I’m not anywhere near the million milestone, I am getting close to 700K in assets/475K in net worth!

Thanks for the inspiration, J. Money!

nicely played!!! I do already miss those lower rates with the 15 – good for you for pulling the trigger on it :)

I hit a couple milestones: TSP maxed out for 2019 and it was over $100K briefly.

Heyyyy that’s nice!!! And now you’ll have that wonderful feeling all over again the next time you cross $100k! Haha…

Our net worth has been stagnant around 745k for the past three months, despite contributions. For a day or two in May we were 3/4 millionaires.

How do you feel about the loss of the taxable account? I’ve been curious how necessary one is for FI. Recently our household income has decreased, so I was thinking about funneling money from the taxable to fuel future annual Roth contributions.

I can’t speak for J.Money, but from what I gather on all financial blogs, the general rule for FI is always pay off debt -> max out 401K -> max out ROTH IRA -> taxable brokerage account.

If you have a decrease in income, would definitely max out the ROTH as it’s tax free money. If you happen to have some money left after that, then go back to contribute to a taxable account.

I would agree with John!

At least that’s the order I do things myself :) Usually I don’t have much money to spare after doing those first two which is the only reason it took me a decade to even get the brokerage account started, haha… But if you check out MadFientist.com or GoCurryCracker.com or any of the more hardcore FIRE bloggers who are already living The Dream, they typically advise to get the free money/tax benefits too and then set up all kinds of conversion ladders which I have yet to still wrap my head around… :)

J. –

Knowing you, you’ll probably side hustle and dominate the hell out of that mortgage, no doubt in my mind.

I have ~20 years left on the mortgage at 4.375% and would LOVE to somehow refi. However, closing costs and the payback period are just not in my favor. AGH!

-Lanny

Still not a bad interest rate comparatively, though! I remember it being in the 6s and 7s years ago so to me anything under 5 looks sexy haha… But I hear ya, always awesome when you’re able to eek out more from it :) Hopefully something changes for y’all in the near future.

Good Luck with the new debt lol :)

Just adds one more fun line to the net worth report now right, gotta keep it interesting for the readership right. Seriously though, congrats on the house and the stage of the journey you are at right now.

Haha, thanks man… It def. does add a little spice to stuff indeed :)

Just to throw more fuel on the fire (see what I did there?) of freaking out about the house purchase, in theory, the market price of your house dropped the second you bought it, since the next available buyer isn’t willing to pay what you paid, and you are now on the selling side. Part of the theory on why companies seem to always be overpaying in mergers and acquisitions…

But don’t worry! The market price of a house you’re planning to keep living in is completely irrelevant as long as you can cover the carrying costs. ;)

True, indeed! Maybe I’ll just pretend I’m still renting, and then whenever anything breaks just pick up the phone and call my wife ;)

We got into the double comma club last month, but got kicked out this month by an angry market. Ah well, we’ll be back…

Have you met many new neighbors?

Nice!!! You’ll get to celebrate all over again then once you cross back over :)

We have met one of our neighbors and he seems super cool so far… also with kids too, so hopefully that means some good playmates for mine!

Good luck with the aggressive mortgage payoff — you can do it! I’ve set a rough goal of 10% of our purchase price per year. It took us 2 years to save a 20% down payment, so 10%/year. We’ve lived in this house for almost 3 years and are on track to hit 50% equity at the end of the summer. As the interest keeps going down, more and more is funneling into the principal. I’m so pumped! This is for sure stretching me a bit, but I go back and forth between mortgage payoff and non-mortgage savings goals (in case of baby fund, etc.). This jumping back and forth makes me feel like I’m making progress all around and I don’t get burnt out over-focusing on one goal.

Nice!! I 2nd that strategy too because the more you’re *excited* about something the more motivated you stay! Whether it’s house or savings or a combo of the two and anything else… As long as it moves the needle forward somehow you really can’t go wrong :)

Thinking hard on that 10%/year goal now too – I really like that challenge :)

I wanted to add a comment about “…we’ll be keeping the *value* of our house the same as our purchase price in our net worth reports since that’s literally the market value of it right now ;)”

I keep mine at the purchase price, minus 7% to cover commission and closing costs. I figure that is a better representation of what I’ll get out of it when I sell.

I’m currently on 15yr mortgage, and am now aggressively paying it down. The goal will be to pay it off in the next 2 years, for ~4 years total. My FI number is a bit fuzzy with my kids heading to college, but I want to be free of the mortgage to reduce sequence of return risk, and improve cash flow in case I do cut back working after the payoff.

I’m still investing in 401ks, but post-tax investment money is going to the mortgage for these two years. In that timeframe mortgage vs investing seems like a wash, since this isn’t the long term horizons that allow the market time smooth out ups/downs.

Hopefully your new servicer is good. I’ve had terrible ones in the past (including one with no website, and paper statements every month. Ugh). Mine just switched to Chase, which is much nicer than the last. A principal only payment is very straight forward on the website.

No website and paper??! That is pretty bad! Haha…

But none of it matters in 2 more years!! That’s a damn good goal to have before pulling the trigger on FI. Super inspiring :)

The ever elusive 1 million. Just when its within reach it falls back again. They say the first million is the hardest to reach and keep.