Morning!

Wanna ask your advice in a moment, but let me hit you with a quick status of where we are in our home purchasing journey so far as I know you’re on the edge of your seats over there ;)

- The Mrs. has abolished the back up idea of renting so we’re now 100% on for owning!

- Which I *think* I’m okay with now, but still a bit nervous of course since it’s all happening so fast…

- Although I will say that we got close with *two* homes so far, which gives me hope that the “right one” is out there just around the corner!

- And we still have roughly 2 months to lock one in heading into peak season here, so I think we should still be okay and not have to worry about settling just yet (I just wish we knew ahead of time *which* houses will be coming on the market so we can make the best call!)

- On the flip side, it also seems like we’ve entered a *seller’s market* now with houses flying off the shelves within 48 hours, which means when we DO find the one that fits our family we have to go all out and fight for it which hopefully doesn’t mean throwing more money at it (which I refuse to do, so the Mrs. better have a better back up plan!! :))

- And lastly, we’ve expanded our target communities now from one area to two areas we love, so hopefully that should make the options better as well, although the first one is still the nearest and dearest to my heart since a good friend and her kids live there…

So that’s where we’re at for now… And I gotta say, it’s a far cry from just a month ago of me FREAKING THE HELL OUT! Haha… It’s amazing how fast you can adapt to stuff when it comes up in life!

So keep on sending over positive vibes please!! I’m hopeful our house is out there!!

And in the meantime, it’s been head down in the *financial* aspect over here which should be no surprise to anyone that it’s been the most fun part of the process ;)

After getting pre-approved through two different places so far (USAA and a mortgage broker recommended by our realtor), it looks like we’re hovering in the $650k-$800k range of what we can “afford” based on their assessments, which of course has nothing to do with what we can REALLY afford, but at least looks good on paper ;)

Our true budget is actually closer to $350k, and might even go down to $330k depending on which area we end up in, and I’m feeling pretty good about that since it means our mortgage will be in the mid $200’s after we plop down 20%.

Which leads us to today’s question of whether it’s smart to go for a 15 year mortgage and save THOUSANDS on interest as well as a quicker pay off, or keep it nice and safe with a 30 year and much lower payments in case money’s tight some months/years?

I’ve hinted in previous articles that I was set on the 15 year since we can fortunately afford it and it’ll only push me to paying off the mortgage faster, however surprisingly I’ve gotten a few comments from people I respect on how the 30 year is a much better option to go. Despite the savings!

Here’s one of them I’ll single out, just because it comes from a financial journalist and author who you’d expect to say the opposite ;) Per, Kathy Kristof:

I promise to stop popping off after this… BUT… Buy a house that you can afford with a 15–year mortgage, but get the 30-year mortgage. Why? You can pay it off in 15 years, if you want. But, if something goes wrong — you lose a job; have a big financial crisis that needs to be addressed, etc. — the 30 year mortgage gives you the flexibility to drop down to the cheaper payment, without jeopardizing your house.

People get enamored with the idea of saving all this money with the 15–year loan. But the interest rate on this loan is only slightly cheaper than the interest rate on the 30-year loan. And for that slight differential, you buy yourself a TON of flexibility. Again, there’s no penalty for paying off a 30-year loan in 15 (or 10 for the matter), but you don’t have to….

Enamored – hah! That’s me! :) But I’ll agree on her points of flexibility here, as that’s exactly the loan we had ourselves the first time around and it was nice to be able to make extra payments whenever we wanted but weren’t forced to. Not that we knew what we were doing back then anyways, haha… We literally bought a house with no money down and financed 100% of it (!!!)

But I do wonder if now, with over 10 years of wealth building and *learning* under our belts, we could better withstand the volatility of life over the years? And if so, wouldn’t it be best to maximize the savings?

Kathy’s right that the 15 year rates are only “slightly cheaper” than 30’s, but a fraction of a percentage point – or in our case when I first got quoted – almost .75% of a point! – can still make a helluva difference over the long term!

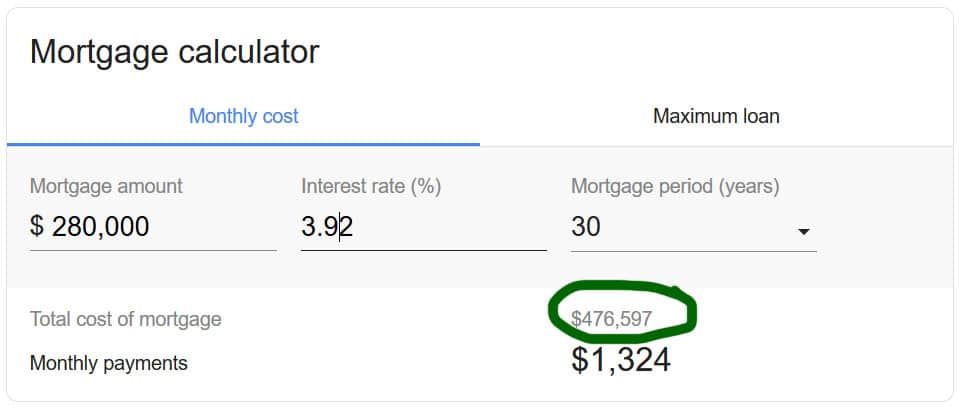

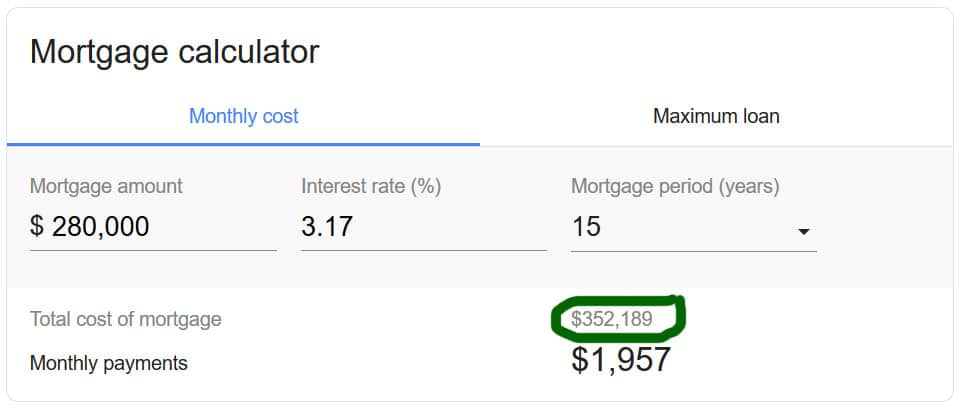

Check out this quick comparison off google’s mortgage calculator I just did to put it in better perspective… I’m using $280,000 as the mortgage since we’re putting down 20%, and I left the default interest rate alone since it looks about right anyways w/ our credit scores:

30 year mortgage @ 3.92%

(A total of $476,597 – crazy!!!))

******

15 year mortgage @ 3.17%

(0.75% less than the default rate)

As you can see, that’s not exactly “slightly cheaper!” Haha… We’re talking a difference of paying a total of $476,597 with a 30 year or a total of $352,189 with a 15! That’s $124,408 less!!

And sure, you can still pay more off every month and knock down that interest/time substantially, but you’re still coming up short even with paying *the same amount* every single month like w/ a 15:

30 year mortgage @ 3.92%

(paying an extra $633/mo)

(via mortgagecalculator.org)

Now this route gets you a LOT closer, saving you an additional $98,576.49 and almost 14 years off the original 30 year!, however you’re still about $26,000 short compared to sticking with the original 15.

And of course, this assumes that you’re indeed contributing that $633/every month too and not being tempted or forced to divert! Which is a lot easier to say than do ;)

And that’s really the heart of this Big Question at the end of the day…

Is the savings of $26,000 – $124,000 a better bet than the flexibility of lower payments stretched across a longer period of time? Or is it better to play it safe, knowing quite well that life doesn’t always work out as we all plan?

With a 15 we’ll be spending a little more than we are now in rent ($2,300) when you add up the insurance and taxes and everything else (those calculations weren’t accounted for in the above examples), but I feel like we have enough assets to fall back on nowadays than we did back then if in fact life really did get so dire? And worst case God forbid one of us dies, our $350,000 insurance policy should be more than enough to cover the remaining loan!

I’m obviously leaning that way, but I’ll admit Kathy and gang have got me second guessing, haha…

But that’s again why I need your help today!! To help me put things in better perspective, especially if I’m missing something?? Because I really can’t get over those insane savings!! :)

So tell me – have you ever tried a 15 year mortgage before? Or any other shorter terms? How did it end up working for you?? On the flip side, how are your 30 year mortgages going for everyone rockin’ those?

I might not always agree with everyone’s opinion, but I read and appreciate EVERY LAST ONE and like to think it makes me a better overall person! Haha..

So let me have it!! Tell me what you’d do if you were in my position? I need more outside advice!

Thank youuuuuu…

UPDATE: Here’s what we ended up deciding :)

*******

Fun fact: Our house budget now with an almost $900,000 net worth is the exact same as it was over 10 years ago with approximately $30,000 net worth! Hah!

Get blog posts automatically emailed to you!

On my last bachelorette pad (i.e. I was single so paid the mortgage alone) I took a 25 year mortgage (locked in for 5 years to get a low interest rate) and my monthly payments were pretty reasonable. Then I made sure I took advantage of the 10% overpayment allowance each year. I also took out critical health insurance which would have paid my mortgage had I been too ill to work. Thankfully I’ve never needed it! Now we are two (and a bit older and with better salaries) we have taken a shorter mortgage, again for 5 years locked in with very low interest rates, and when it’s time to renew hope to pay off an extra chunk with savings.

TLDR: get a medium length mortgage so you can sleep at night and overpay if and when you can!

Good luck!

I always forget there are more in-between terms, haha…

I’ll make a note to check out 20 years and see what the differences are there.

I wouldn’t make up your mind until you’ve picked your house and actually are getting financed because the rates may end up being way closer than .75% apart. We were quoted something similar when we were pre-approved but then, when we went to actually finance our home, the 30 year rate and 15 year rate ended up only being .15% apart. For our $208k loan at 4% instead of 3.85%, it made more sense to opt for payment flexibility. Plus we are making better than a 4% return on our invested money in the SEP IRA and Roth IRAs. So we overpay a little ($1250 a month instead of $990) but as long as our investments are solid, we’re not rushing too much on paying off this house. That said, we paid off our first house (now our rental property) in 6 years and loved that feeling…so we’ll see but we’re already 6.5 years into this new mortgage.

Oh wow – didn’t realize they could fluctuate so close like that over weeks?? Will def. keep in mind!

Congratulations on getting close to your home purchase! I’m glad you guys aren’t listening to the mortgage brokers (although I can’t say I’m surprised lol). They would have all your money tied up in house payments if they could. They approved us for the same amount (probably based on our incomes because we were $400k in debt when we bought), and we knew there was no way we could afford a payment that large.

I don’t think you guys can go wrong with a 15 or 30 because you can afford either and don’t have other debts. We went with a 30, but we plan to pay it off in a little over 5. Having the lower payment has enabled us to make significant progress on paying off our student loans. Once those are gone, we’ll work on the mortgage. The quicker you pay it off, the more negligible the difference in interest rates.

Excellent plan :) In a handful of years you’re going to be completely debt-free – that’s going to be amazing!!

Why not pay cash for the house now, and take out a home equity loan in the future if (and only if) you experience the kind of catastrophe that requires quick access to money? That way you’re only paying interest if the absolute worst thing happens. I had a 30 year mortgage that was paid off in 15. But then, when the mortgage started, there wasn’t the financial backing available to qualify for a 15-year option. Still, it felt good to watch the interest paid go down every month.

I don’t have that much cash :)

I agree with Nora. Why not pay cash if you have the funds? With no mortgage you will have that $2500 a month to throw back in investments quickly. I know that the market offers better “returns” but there is nothing better than the feeling of no mortgage! We actually put 45 percent down on our house we built and did a 30 year (had a 15 before) but we are thinking to bump down in price range and pay cash with the equity in our house in the next year. We did get a 30 with the plan to throw a chunk at it every year, but you must be disciplined enough to actually do that. We can afford our home but I would love to have no mortgage!

Also, you have more negotiation power coming to the table making a offer on a home because you don’t need financing ;) Just a thought! Excited for you guys!

That would be nice if we had it!! We’re going to need as much negotiation power as we can get it’s looking, haha… At least we don’t have another house to worry about selling!

We had a bi-weekly 20 year mortgage PLUS made extra monthly payments. It would have been paid off in 14 years but we were forced to sell the house since hubby’s knee injuries prevented him from climbing the stairs anymore. Still, when we sold, we walked away with a very healthy down payment for our current house. This home is pricier in a much better town/neighborhood so we took a 30 year mortgage & make extra principal payments each month plus we pay bi-weekly. Consider a bi-weekly mortgage & pay extra principal payments. The term is whatever you’re most comfortable with. There are calculators that will do the math for you & show you how much you’ll save with a bi-weekly mortgage plus making extra principal payments. This option will greatly reduce the interest you pay no matter what the term of the loan is.

Forgot about that option too! Didn’t realize there were *actually* loans set up bi-weekly like that, but I know you can pay them that way to help lower interest for sure…

Im sure you’ve already got a solid idea of what way you’re leaning, but, look over at Financial Samurai’s site as he discusses ARM’s and how he leveraged them, his insights on mortgages etc. are very informative.

When we finally get to our destination, we will be looking at a max of 15 years because, RETIREMENT… When I get ready to call it quits I don’t want any debt. 10yr or 15yr fixed rate (which raises my pmt quite a lot) definitely fits the bill. But if we decide to cut it short and retire early then an ARM 5/1, 7/1, 10/1 may be better.

Depending on rates at that moment I may go with a 7/1, then I can play the game to see if I can do better or lock in a longer mortgage. Maybe Ill just pay if off. And depending on location, location, location, we could just sell it, buy an rv and drive into the sunset….

Course don’t forget, no more than 25% of your monthly net income should go towards a home.

Good point on the arm stuff – I’ve kinda had my blinders on focused on the 15 or 30 but when it gets closer to “GO” time I’ll review the options before we sign :)

(And i agree – i don’t want debts either on the books when it’s retirement time!)

We got the 30 year in 2013, but it will be paid off this year. That’s SIX years. Even better than a 15. The 30 gives you flexibility in case of emergency. You will only use that flexibility in case of an emergency. You, and everyone who reads your blog are too damn smart to be a SUCKA and abuse that flexibilty and end up riding out a 30 or even 15.

Is that a challenge, sir?? ;)

First thing to do is buy a house you can afford and NOT one your mortgage company says you are qualified for loan wise.

When we bought our first couple houses we did 30 year mortgages. We also paid extra principal every month.

When we bought our most recent home we planned to be in it a while and took out a 15 year mortgage and continued to pay extra principal.

Go with what you and your family are most comfortable with. That might be a 15 year or a 30 year. Only you can decide what is best.

You could get a 15 year mortgage now, and if shit happens and you need the extra monthly income, you can refinance. Refinancing usually gives you a month off of payments as well!

Oh, d’oh – yup, forgot about refinancing too.. Although doesn’t it cost some money?! It’s been a while since I had to think about that haha…

I am not currently a homeowner so take my input with a grain of salt but for my next purchase I really, really want to go for a 15 year mortgage. I don’t want to stretch myself, though, so I’d want the payment to be one that has some comfortable wiggle room.

That would be a pretty killer move if you could pull it off on your first go at it!! I definitely couldn’t then haha… (not to scare you off or anything :))

Well this technically would be my second go at it (first one didn’t go so well) so I’ve learned a thing or two from my past mistakes. However, to your point it would be a great feat if I can pull it off. I’m sure I can but it may take a little longer. :)

I will be rooting for you the entire way – whatever that’s worth! :)

For me it was kind of an apples-to-oranges comparison. We took out a 30-year 4.375% loan in 2010 because it seemed like the thing to do and we didn’t want to lock up our meager monthly income in additional payments. Five years later we refinanced to a 15-year 2.625% because our incomes were higher and we’d just discovered this ‘FIRE’ thing, so we wanted to be out from under the debt that much faster. We spent more in interest those first five years than we will over the entire course of the 15-year loan ($36,904 vs $35,748). Running those numbers convinced me… and it’ll be dope to own free and clear when I’m 50.

Alternately, if you’ve got room in the budget, maybe try a 30-year but making larger payments in the first few years (e.g. $800-$900 instead of $633). It’ll front-load the payback and carve down principal faster during the time that you’re paying the most interest — kinda like spreading additional down payment out a little bit.

Good idea w/ the bigger upfront payments – hadn’t thought about that one before, thx :)

I use the direct deposit benefit at my company to make a recurring weekly payment against my mortgage. Since it’s automated, I don’t have to think about it & really don’t miss the money. I figure by doing this, I will be able to shave off 2.5 – 3 years on my mortgage.

**I did start out with a 15-yr mortgage but refinanced last summer when changing from a bank to a credit union and ended up with an affordable 7-yr mortgage.

I just learned about 7 year mortgages!! haha.. had no idea they went that low??? Can you literally choose *any* amount of years you want?!

I 100% agree with Kathy’s argument for a 30-year mortgage and would add one item to it. If you take the 30-year, paying the minimum for the first 15 years and investing the difference between the monthly payment on the two loans, where would you be in 15 years? Obviously, there are risks if you are going to invest the money, but investing $622 per month for 15 years is almost $112k in investments, think about the compounding return on that money!

The other idea I hear a lot that many people don’t consider when making these decisions because its hard to put a number to, is do you plan to stay in the house forever? If you plan to stay there forever, yes, it likely makes sense to pay down the mortgage as quick as possible. But if you think you are likely to move before the mortgage is paid off or shortly after paying off a 15-year mortgage, then there is less benefit to paying it off quickly.

I agree. I did this math when I was looking at buying, and although in the end I went with a more expensive, turn-key-ready place, with a 30-year mortgage, which means paying a bit more than the cheaper place I was originally considering (but less work over time to make it liveable), once all other higher-interest debt is paid off, the plan is to use the mortgage as a low-interest loan and invest the monthly difference that I would have paid on the 15-year mortgage. This is also providing a cushion for me as I get accustomed to insurance, property taxes, and other expenses that go with the mortgage payment that I didn’t have to consider on a rental.

We don’t have market guarantees, but I’m interested in both home equity and a variety of investments. If we assume that we will have an average 7% annual return on investment, or even 6%, then you would have hundreds of thousands extra, far outweighing your $98k gain that you calculated above. This means discipline every month for a very long time, but in my estimation, it is well worth it. Even if you miss months, or, like me, won’t start this method till a few years in, you would still end up with 2-3 times the dough in the bank compared to your calculated savings.

I hear y’all loud and clear! :)

Hadn’t thought about the “investing the difference” option until today which is def. a possibility, although I always find paying off debt much more exciting and gratifying haha… Maybe since it’s so instant? And SUCKS??

As for the timing – it probably won’t be our “forever” house, but it’ll def. be our 10-15 years or so house, so long as we find a good one in time!! We’re ready to settle down for the long haul finally :)

Please read the Mr. Money Mustache Forums where you will be educated on why you should NOT pay off your mortgage (or pay down, or take shorter terms, etc.)

Those forums are a bit too hardcore for me, haha….

It really comes down to your specific situation and what other goals you have for your money. If you think you can swing a 15-year without sweating it (you also have to think about how much maintenance costs will be and save for those repairs, in addition to taxes, utility bills, etc).

Personally, this is my 3rd kick at the can with a mortgage. Previously I went with longer terms but I rarely put extra money down (that was before your blog of course). But this time i went with 15 and a much smaller house and smaller mortgage and it is working out for me. But I won’t lie, it’s been tough to try also balance paying off my mortgage with funding my other money goals. But again, my situation is different from yours.

See what kind of house you end up with, what all the various costs of homeownership will likely be with that specific house, know your other money goals, and chat with the Mrs. and the answer will come to you.

15 year mortgage ONLY. You are already being smart and frugal by buying yourself a lower payment by only spending half of what you can “afford”. If you hit a rough patch and lose a job or something else equally dramatic, that’s why you have emergency savings. If you don’t have enough emergency savings to carry you through an emergency, then you shouldn’t be buying a house.

I have zero experience with house loans so just try to be the smartass here :)

If you really have no restrictions on extra payments (I know that we in Europe do) then I would go for the 30 years because of the safety reasons. If you could afford you can still go for the savings. I don’t know your budget but in theory, I would go for the 30 year one with aggressive repayment. You added the difference to extra payments but what if you go further? While you are in great financial condition round up the payment and throw $2500 into repayments. That calc shows me that in that case the total cost would be $349,126.23 and repayment time would drop to 11 Yrs 7 Mts. I would go for that until you can afford and shift down the gear if sh*t hits the fan. On the other hand what if you would do a calculation, not on the savings but the opportunity cost? Go for the 30 year one, pay the $1324 per month then invest the difference automatically. Maybe I am wrong but a quick calculation tells me that $633 per month compounding for 30 years with only 3% interest rate would become more in value than the $350k and the interest earned will be more than the $124k saved… but maybe I am missing something. :)

I am also curious about the answers to prepare for future situations :)

Yes to the rounding up whichever route we go!! I used to do that with our first mortgage and it definitely helped over the years (plus always easier to remember and feels good having a *round* number, haha…)

Didn’t know there are limits in Europe? I wonder why? So banks make more?

Banks are businesses after all and if you pay your loans earlier they lose some planned profits. Because of this if you want to pay more in a month (you cannot pay as much as you want on an ad hoc way) or kill the mortgage at once you will face some costs (1-2% of the prepaid amount). The rules change from bank to bank, some give you additional payment opportunities only after five years, some give unlimited some only one or two occasions per year or per the whole mortgage period, some limit the amount (like you can only pay additional two months per year). It seems they use these as marketing tools for promotions and incentives for example for VIP clients. I think this is really weird as I get that the bank loses on future interest payments but they will get back the money after all so they can redeploy it and start earning again.

I think I just vomited a little in my mouth.

Jay, here’s my best advice (free and worth every penny). :D I’d take the 30-year mortgage in your position. Your income fluctuates, which makes life less certain, and you have three kids, which makes life less certain. Sure, you can afford the payments on either mortgage, but consider property taxes and home insurance, which are also part of your mortgage bill. The lower your overall bill, the better the chance that if lean times come, you’ll be able to meet that payment without tapping into savings. If good times come, you can make extra principal payments and pay off sooner–just make sure your mortgage allows extra principal payments. Also, I would get an umbrella policy for a million dollars–your approximate net worth. For two or three hundred dollars a year, you get the peace of mind that if something happens on your property or with your car and someone sues you, that policy stands between the courts and your actual hard-earned money to hopefully absorb whatever damages are awarded. I am excited for you and especially for Mrs. J$, who wanted this in the first place!

We have an umbrella policy for a million dollars! WOO! I feel smart now, thanks!!! :)

I’ve Got 99 Problems but a *Million Dollar Umbrella Insurance Policy* Ain’t One.

(and I hear ya on the uncertainty of kids/income… you’re not wrong on that)

I have more experience with “God forbid” type occasions on life than I’d like, so I think I’d tend towards the 30 year for that reason. Three kids are three extra variables, and man, can they be expensive! God forbid you have any kid expenses that are of the God forbid category, but I’d so much rather you be able to go from biweekly payments back down to monthly and cash flow whatever comes up than need to go through the time, emotional energy, and cost of a refi if the proverbial ish hits the fan. My two overly cautious, perhaps, cents.

Haha I hear ya!

I ma currently on a 15 year mortgage, and on a whim (I decided my credit could take the hit of a hard credit check) I checked on REFI. and the poor mortgage broker said there was nothing he could do for me.

With a 15 year mortgage, and mortgage cost the same as rent (the first year or so), Can you afford an extra 1000 a month due to sudden maintenance issues? Are you comfortable getting a loan to fix your major housing issue for the pieces of the repair insurance won’t cover?

Mortgage payments will fluctuate yearly based on changes in appraised home value, homestead exemption laws, and of course, cost of insurance. Make sure any taxes that have been quoted on the house you want to buy will be the same should you own it.

Overall, I am quite happy with the 15 year mortgages I have negotiated and I think it makes more sense; just be sure you allow for the “landlord fees” too.

I agree with almost everything in the quote from Kathy except the difference is not so little. If interest rates were the same then I’d default to the longest term. However paying a higher interest rate just for “in case of disaster” is the same as buying a warranty on your iPhone and a very expensive way to do it.

Haha… true that.

I have a 30 as the wife’s business was making pennies at the time we bought our second home and we absolutely needed the flexibility. Fast forward 3 years and the wife is killing the online business game so we are stacking cash and putting more towards the principal.

I don’t think you will go wrong either way. You have the reserves to cushion a financial blow. Even the worst case scenario where you can’t put food on the table, you could (not suggested unless this scenario came true) pull with a penalty from the retirement accounts. Again, not advised. I have a feeling you would mitigate that situation months before required.

I think you should go with the 15, but completely understand going with the flexibility of the 30.

End of the day, just accept the reasoning for whichever decision you make and don’t man-I-should-have-done-the-opposite. Be at peace with the decision knowing the reason you went that way.

D

I have a feeling what will end up bringing me the most peace is asking the wife to make the call in the end :) Something I really haven’t discussed fully yet with her, outside of the generalities which has her on board w/ the 15 so far…

I’ve gone back and forth on this issue before J. Honestly, it’s probably best to go with the 30 year and have the option of paying more towards the principal if you have the extra cash. Unless you’re really set and sold on the 15-year mortgage, I think it’s better to keep your options open. Things come up and you don’t know what will happen in the future. On the other hand, I’ve known some to go with the 15 year and pay it off successfully. Though, they got lucky and did not have any life changing and/or financial catastrophes during the time they had the mortgage. Just my thoughts. Hope that helps! :)

It all helps!! And just so fascinating for me to see since the 30 year def. seems to be winning out here despite the costs!! Which just goes to prove time and time again that this stuff is way more than just numbers alone!

Go with the 30 and pay it off as quickly as you are comfortable and able. You have no idea what the future holds for jobs, kids, health, etc. so think of this as a type of insurance policy giving you flexibility. Done this three times so far and never took more than 7-years to pay off a house.

Oh damn, haha… I want to be like you when I grow up!!

Amortization is such a scam. Most of your interest is paid off in the first 1/3rd of the loan… Unless you buy and never move you never actually build any equity in real estate. If your goal is to pay it off ASAP, why not just get a 5/1 ARM and save even more on interest? Of course, that puts you on a 5 year timeline to either refinance or get it paid off, could be good, could be bad…

Would 5/1’s be a lot more cheaper interest-wise? I honestly haven’t even looked at it yet but plan to now as others have brought up… (though not sure i’m confident enough to pull THAT ONE off! lol…)

Cheaper by at least a half of a point for 5 years. It gets quickly worse though if you don’t refinance.

My only advice would be to try to envision yourself many years later there and get a house that accomodates that. If you have 3 boys(and counting) what may seem large to you now won’t in 8 years. Our previous house wouldnt accomodate our family of 4 now that our girls are 12/13 I’m pretty sure, and boy do they change over the years!!!

Hello J,

Appreciate this post & the responses read thus far, especially the following:

NORA: ‘… pay cash….’

– The only caution I would say with this one comes from personal experience. Although, based on the things I have read from you I doubt you would allow yourselves to do something as unwise as what my husband and I did.

– After paying cash for our small home many years ago we used the equity there to get much needed funds. Unfortunately, we never replaced that money.

MK: ‘…direct deposit at work to make a recurring weekly payment against the mortgage’ ‘… ended up with an affordable 7-year mortgage.’

– Any mortgage less than 10 years in my eyes is best.

– I appreciate MK’s comments, because I had never heard of weekly payments before. If one must have a mortgage, and the funds are available, this makes a lot of sense to me.

KATIE: ‘… investing the difference between the monthly payment on the two loans’

– You seem to have the discipline & finances to do this. So, to me this sounds like a good idea.

DEBBIE: Regardless of your ultimate financing decision Debbie’s comments are definitely worth keeping in mind. Whether it be like Debbie’s husband’s knee injuries, which prevented him from climbing stairs & caused them to have to sell their home, or something else, I think you and your wife are financially savvy individuals & will make the best decision for you.

– I think Debbie’s comments & subsequently the style of the house (ranch vs upstairs, layout, etc.) is just as important as how to finance the home (or not, you might choose to pay cash, if the money is available).

Wishing you and your wife equanimity in your decision making on the financing, style & function of your next home.

Peace & love,

Karlene

Thank you Karlene!!!

And love that you taught me a new word there too – equanimity – awesome! :)

You are welcome J. :)

Looking forward to reading about what you both finally decide.

I will definitely be doing that!

With a 30, you can always prepay and make it a 15. If you need breathing room one month, you can’t make a 15 year a 30. Default to safety but prepay……

I’d get the 30 year mortgage. It’s simpler and more flexible. You can pay it off early if you want.

Also, the mortgage rate is super low right now. You might as well take advantage of it.

I don’t think the difference really is $125,000. If you pay extra on the 30 year mortgage, the saving would be much less than that. Can you do the math?

See comparison #3 up there :)

Since you have a bunch of savings already, and don’t plan on deploying that cash in other real estate or cash-heavy investments, 15-year sounds like an easy win to save 1,500+ a month avg over the next 15 years (as compared with paying off a 30-year early).

Like you said – since you’ve tracked spending, know yourself and your money habits, it seems like the added flexibility of the 30-year wouldn’t be needed. It’s the safer choice for sure, but you’re paying for that safety.

My wife and I just bought our first home and we went with a 30 year mortgage. I don’t make very much and she is paid on commissions 2 times a year. So we can easily afford the house but on months where she doesn’t get paid all we can do is pay bills with my salary (no investing or discretionary spending). So we had to go with the 30 to get cheaper monthly payments but pay big lump sums off her commissions in those months.

Yup, totally… 15’s are only good for those with stable incomes/savings/wealth already built up! We went with a 30 too our first time around and it was a Godsend (especially since we didn’t know what the hell we were doing!)

Agree with Katie on investing.

This should not be a discussion at all. This should be clear as day.

The longer the mortgage the better. Invest what is left.

With a 15 year horizon and a diversified portfolio, hard to see you end up in the red.

“This should not be a discussion at all. This should be clear as day.”

do you see how many comments are being passed around here??? haha…

I would say you’re probably making the right choice. You’re used to paying roughly that amount for housing and have enough FU money built up that you shouldn’t need the flexibility.

I also have a 15-year, with the idea that it would be paid off right around the time I hit FI, but one thing I’ve thought about is the opportunity costs. At such low interest rates (mine are sub-4 as well), assuming a safe long-term return assumption of 7%, would my money be gaining more if I had a 30 year and was investing the difference instead?

But for me psychology comes into play – it’s my only debt and I want it gone as soon as possible, so I pay more than the mortgage payment. I want to be mortgage/rent free in FI, or renting out the house to cover the rent in another country I move to. I go back and forth on this daily lol.

One thing that gave me a little pause. I’d see if you can revisit the renting back up plan in the short term at least. The housing market is ridiculous right now, total sellers market. I’ve heard this is starting to ease in some area, but in my own houses are selling within 24 hours of listing, with bidding wars between 6-12 people, according to my realtor sources. When I looked in my neighborhood I looked at more than a dozen houses – now there isn’t even that many houses for sale – last count there were two in my whole neighborhood without accepted offers. It might make sense to keep renting as an option so you’re not forced by time constraints to buy a house – it’s just too big a decision to be pressured into. My two cents anyway.

I KNOW!!

It’s getting crazy out there!!! Bad timing for sure :(

Can anecdotally confirm the sellers’ market. A house across the corner from me went up for sale last week at >2x what they paid in 2010, there were at least three pre-inspections even before they open-housed it Saturday and Sunday to MOBS of people, and they expected to sit down with their agent yesterday at noon to pull out the top four or five offers to play against each other. We’re all gonna miss some fantastic neighbors… but man, are they getting PAID.

*closes my eyes and downs a beer…*

I am so risk averse, I’d go with the 30 no matter what, so long as there was no pre-payment penalty. But that’s me.

What I really reacted to in your post was the interest rate. I financed my home in December and had a nearly perfect credit score (hovering anywhere from 800 to 850 depending) and still, the rate I was quoted was 4.875%. I didn’t realize that the amount of the loan mattered so much. If I had gone over 500k (as you probably know, NOT hard in the DC area), it would have bumped up to 5.1 something percent. The other thing that was really surprising was that I got a higher interest rate with 20% down than I did with 10% or less down…because PMI. I ended up buying a point or half or something to lower the rate.

I didn’t really shop around–I did one of those online quotes where everyone and their brother ends up contacting you. They didn’t seem to differ much if at all from the one I got from one of my agent’s recommended brokers, and I loved her and everything went super smoothly, which doesn’t always happen with the financing.

Oh wow – I didn’t realize the % could be more with putting down 20% either??! Or by choosing more expensive houses for that matter, although I suppose that makes more sense…

Congrats on the new house though!! I bet you got a better deal snagging it in December too :)

You’ve enjoyed being debt-free for a while now. So why take the longer loan and potentially be in debt much longer? Yes, you can pay off a 30 year like a 15 year mortgage, but you can also pay off a 15 year even much shorter (I’m paying mine off in 4 years!). I get the feeling you really like being debt free…like I do. If that’s correct, just make a stab at it and take the 15-year mortgage and then go ahead and pay it off in 5 years. The reality is that you are more likely to maintain financial stability in the next 5 years without anything tragic that will stop you from paying it off. Compared to if you get the 30 year mortgage and keep it for longer than 15 years: there is a higher likelihood of hitting a rough patch over that long period of time. Just keep it simple and clean and avoid the analysis by paralysis: go for the 15 year mortgage. All the best

I’d like to think I could pull 4 years off but sources tell me that won’t be happening haha… But I applaud you for being able to do it!!

I say go with a 15 if it’s not too much of a stretch. We originally had a 30, then refinanced to a 15 after 5 years. If we’d just started with a 15, we’d well and truly have the house paid off by the time our 10 and 13 year olds head off the college. As it is, it will be paid off by the time the 10 year old (nearly 11) starts. I waffle back and forth between paying it off faster, but the interest rate is only 2.85%, so instead I just put extra in a 529. But, once it’s paid off, I can just funnel that money instead to college expenses, so having it paid off the earlier to better when I think about that. I guess it also depends on your ‘will power’ to pay extra on a mortgage vs using that money for other things. I tend to be very ‘carpe diem’ about travel and experiences, so a lot of our money goes there instead. ;) Good luck!

2.85% – wow, that is good!

I know! Amazing. Feels almost like free money. Nearly impossible to convince myself to pay any extra on it at that rate.

Hey bro, I figured I would add my two cents. I am in my third house. Each time, I took out a 30-year mortgage. When the rates dropped in 2011, I refinanced to a 15-year mortgage. At the time, I wanted to minimize the interest paid and keep more of that money in my pocket. The loan was at least 0.5% cheaper with the 15 than with the 30. I also wanted to pay off the house as soon as possible. Through the years I have gone back and forth on this decision. I thought if I had the extra money then I could have invested and taken advantage of the previous bull market. The truth is that I would have spent the money elsewhere and I would have nearly 25 more years to pay on my house instead of the less than 10 I have now. One must be extremely diligent to take on a 30-year loan and pay it off in 15 or less. It is far easier to say you are going to do it than it is to do it. Do not worry about gains you could potentially make in the stock market. No one knows what the market will do in the future. We could have a recession that lasts the next decade to counterbalance the meteoric rise we had during the past decade. The 15-year mortgage is not much more than the 30-year in terms of monthly payment, but the benefits are worth so much more. You can still pay extra on a 15-year loan if that’s what you want to do. You will save on interest and pay the debt in half the time or less. Therefore, since you can do it without any extra effort, I recommend the 15-year mortgage. Best wishes to you and yours and happy house hunting!

Thank you sir!! I’m still leaning that way, although the 30 year proponents are starting to get in my head more haha…

Stay the course, my friend. You are going to pay it off in under 15, so you might as well take advantage of the lower interest rate. Taking the 30 is just putting more money in someone else’s pocket.

That’s what I keep telling myself but MAN people are comign up with some good reasoning!!! :)

I bought my house in 2008 on a 30. I refinanced to another 30 and saved about 1% in 2010. I was 45 at the time, so if I wasn’t able to make additional payments, I would have been paying until I was 75! In 2017 I refinanced to a 15 at 3.25%. If I make no additional payments, I will pay off the house the month before I turn 67. I am currently paying off other debt with much higher interest rates. I anticipate paying off this debt in a little over 2 years, then will focus on paying down the mortgage.

We all have our own situations, and the 15 year mortgage I have now is working for me. The payments are about $250-300 more than what they were before I re-financed from the 30 year.

If I were in your situation, I would absolutely go for the 15 year. I think you can afford to pay extra and probably pay it off in 10 years or less while still making your usual retirement investments.

Before I became self-employed, my hubby and I paid down a huge chunk on the mortgage and refinanced it to a 30-year. Why? We wanted our monthly bills to be as small as possible, because we knew it would take time to ramp up my income. We always pay extra on the principal every month, but it varies based on our current situation. Some months we pay $50 extra, and other months it’s $1,000 extra. Having that flexibility gives us peace of mind. And even if that costs us a little extra in interest, I think it’s worth it.

Everyone has a strong opinion on this and mine surely doesn’t matter as much as yours or your wife’s, but we had the same discussions and ended up with a solid compromise. I wanted 15, wife wanted 30 for “just in case.” We ended up with what I consider a win for both sides. My salary is high enough and savings high enough we were never going to run in to problems if work suddenly ended, but wanted to make sure we still invested heavily. Safety is number one for my wife and investing is number one for me. We went with 30 just in case for my wife’s sanity which is more important than paying off a house early since the marriage is more important than 2×4’s and drywall. Then I took the first principle payment and doubled it the first year but then the second year tripled it because an extra $300 in savings wasn’t going to do much since everything else was maxed out. So instead of the basic $1,000 payment for 30 years, it was $1333 the first year and $1667 onward. We had it on auto-pay so I couldn’t decide month to month to cheat. House paid off in less than 10 years (luckily ran in to 10 awesome years at work and with the market) and all retirement accounts fully funded as well. We all win! No one right answer for everyone otherwise we’d all be doing it.

Okay – I’m totally copying and saving this one one to present to her if needed, haha… That’s a really clever idea (and compromise!!)

13 years ago, we bought our first house for $82,500 (recently flipped 3bd/1ba/double garage, nice yard–this is rural midwest living!), put 10% down and took out a 30 YEAR MORTGAGE because we literally didn’t know there was another option. Sold 5 years later.

8 years ago, moved to a more expensive town and bought a $157,000 house (5bd/2ba/double garage/huge yard) with a 15-year mortgage (those payments jumped pretty high compared to our last house!)

1 year ago, now with 3 kids, moved to a larger $275,000 house (5bd/3ba/tripple garage) that we plan to stay in forever with a 15-year mortgage. The interest rates varies about .75% but the biggest thing for me was that i wanted it paid off by the time our youngest leaves the house and I wasn’t sure we had the discipline to “Pay as if it were a 30” as our kids got older and more expensive. With no mortgage at age 50,

Mathematically it could make sense to take the 30 but instead of paying off early with extra payments, investing the difference and writing off the mortgage interest if you itemize. Paying it off early is more of an emotional decision.

My advice: What will you be most thankful you did 15 years from now?

My question for you: WHERE DO YOU LIVE??? I want to move there!! :)

Like you, we are a single income family with 3 young sons. We asked ourselves the same question when we bought our house. We could comfortably afford the monthly payment on a 15-year mortgage (even on our single income), but wondered if we should take the 30-year mortgage and pay it down like a 15 just to give ourselves flexibility in a financial emergency.

We signed the 15-year for the following reasons:

(1) We have enough in emergency funds, other savings and brokerage accounts that we could dip into during an unexpected financial emergency/crisis, whereby the financial flexibility argument was not a big concern for us. If we somehow sustained an extended financial emergency and drew down all those backup funds, we could send the non-working parent back to work temporarily until we were back on our feet.

(2) We wanted to force ourselves to pay off the mortgage in 15 years (or less), such that it was paid off right around the time our oldest child went off to college. Since we are currently not saving enough in 529 plans to cover the full cost of our kids’ college, we wanted to divert the mortgage payment to fund the shortfall. Assuming, of course, that the kiddos deserve to get their college paid for….I have no problem keeping that extra cash flow to myself if they insist on majoring in underwater basket weaving!

(3) We knew ourselves well enough that if we took out the 30-year and intended to pay it off in 15 years, that we wouldn’t necessarily have the discipline or willpower to execute on that plan. It would just be too easy for us to get distracted with house improvements (wouldn’t it be great to replace those ugly countertops?!?!? If we’re going to tear out the countertops, might as well replace the cabinets while we’re at it! Oh it’s almost summer, let’s build a deck out back…and buy a new grill or fancy lawn furniture to go with it!). Home ownership is a slippery slope…signing the 15-year was essentially our way of protecting us from ourselves.

Best of luck in your decision, J! Can’t go wrong either way!

Thank you!!!

I hope all my reasoning makes as much sense as yours when we finally come to a decision!! :)

(Which I’ll be sure to blog about of course, so we’ll see one way or the other, lol…)

J. Money – been a follower of your blog for a couple of months now and LOVE IT!!! KEEP IT COMING.

I want to echo what Single Income Life said about paying off my home before my 4 kids go to college! We have lived in our house for 12 years now. Started off with a 30 year mortgage and then we eventually re-financed down to 15 years. Our interest rate dropped from 7 % down to 3 %. So, you can always start off with a 30 year loan and then drop down to 15. I have not saved enough for college for the kids so hope to use some of that mortgage money to offset education expenses.

One big thing i want to highlight though is the new Trump tax plan. I used to itemize deductions, but this past year that stopped since the new tax plan upped the standard deduction a ton. I know a lot of people were planning on deducting their mortgage interest only to find out they no longer can as it is preferable to take the standard deduction.

The beauty of the 15 year long (i am 7 years into it) is the interest is so much less. Right now, my principal payment is $ 750 and interest only $ 200 a month. I also add extra principal each month so I’m paying about $ 1,000 against the principal each month! Whereas, I know friends that have $ 2,000 a month mortgage payment with $ 1,600 of it as interest. So, they are giving away $ 19,200 to the bank each year, and I am only paying the bank $ 2,400 a year for the privilege of a mortgage. So, having a 15 year loan helps lower expenses.

My rational is I’m already maxing out my 401(K), HSA, emergency savings etc. and I want to pay as little interest as possible each month. The 15 year loan allows for this. I also recast the loan a few years ago and lowered the payment amount even more so I could sock away extra at the principal each month. This strategy will allow for us to pay off our house in 6 years around the time when my first kid is off to college.

Last, I live down the interstate from you in the Richmond, VA area. Maybe if you move farther away from D.C. you can get a cheaper house. I know my friends in D.C. area have told me our house in Richmond ($ 275,000) would cost $ 700,000 in D.C. It is crazy to see the price difference! Just my 2 cents. Love the blog!

I saw that from your RVA reference – love y’alls branding down there haha…

I’ll actually be heading south of DC to avoid all those nasty costs (and way of living – it’s so chaotic up here!!), so thankfully our housing will be closer to yours than theirs…

Great point about the tax stuff btw – I’m not the best at following it since I relay a bit too heavily on my accountant, however this reminds me to actually ask her opinion on it too! So thanks!! And for taking the time to pop in and share too – really means a lot :)

Hey J. Love the site. I was in this same situation 6 months ago and we had a local credit union that did a 15/15 ARM. The rate is lower than the 30 year fixed but slightly higher than the 15 year fixed. Rate is fixed for 15 years and then it can change up or down a max of 2%. I would have never considered an ARM before this but it made perfect sense to get the best of both worlds with very little risk. Not saying this is a better option but it’s another possibility and it fit our plan of paying off the mortgage in 15 years but having an emergency option.

Another idea I did not know about! haha… I believe my options are now up to 88 of them to consider after today’s post :) But it’s all helping!!

Amazing how house hunting can be fun and frustrating all at the same time, huh?! Great question and I can’t wait to read all the responses later. Thought I would share my experiences and advice I received. Years ago (probably around 8 years or so) I refinanced my previous house. I freaked out because the lender said refinance at the 30 year rate – but I had already worked on paying down some principle and didn’t want to go backwards. She said to refinance using the 30 year rate but write it up for 21 year mortgage. I actually ended up with lower monthly payments, knocked years off the original term of the mortgage and would have paid less interest than if I refinanced at the 20 year rate. Not sure if this is an option but might be worth asking your lender and then doing some number crunching! I’ve taken a different approach with my current house. I did sign up for a 30 year mortgage. My rate is lower than what they are now so makes no sense to refinance. A good friend of mine gave me this advice – stick with the 30 year but throw extra money at it to knock it down (you could even play with mortgage payoff calculators online to see how much extra you need to throw at it to still pay it off in 15). By keeping with the 30 year mortgage, you are locked into the lower mortgage monthly payment – that way if something in life was to happen you won’t be locked Into a higher mortgage payment if money got tight. I didn’t start making my extra monthly payments until about year after my mortgage started so (if all goes to plan) I will be paying off my mortgage somewhere beteen 15 and 16 years instead of 30.

Very nice!! Congrats!!!

What I want to know is how are you getting a 3% interest rate? I have near perfect credit and a very low DTI ratio and am getting 4%….? Show me your waaaayyyzz

I have no idea – it’s just what the lenders told me! :) Though maybe since it’s in pre-approval vs total approval maybe that makes a difference?? I’m sure I’ll find out soon enough and will report back, haha…

It sounds like mortgages are set up differently in the UK, the key factors on what rate we pay were LTV (loan to value) and how long a deal you buy into. When we first got our mortgage it was a 60% LTV, fixed rate for 5 years and a 28 year term. The husband already had a house so we wanted to make sure we could make both payments if needed. We sold that old house after about 6 months on the market. Around 2 years jnto the term we realised we should and could be overpaying.

At the end of 5 years we opted for a 2 year fixed rate, unfortunately the house value had decreased so we were again about 60% LTV but took a 20 year term.

We are currently in our 3rd deal; a 15 year term with a 5 year fixed rate and more overpayments. Each year we are able to pay 10% off the capital without penalty. Sadly our overpayments are no where near that point yet!

In 4 years time, when the current deal ends, the plan is to take a 10 year term but no fixed rate and no Early Repayment Charge and pay it off soon as possible, hopefully under 5 years. This will take our initial 28year mortgage to under 17 years without putting us under too much pressure at any time. If kids come along or life throws up surprises we have plenty of safety net.

TL,DR? Get a longer term and pay it off quickly!

Haha – thanks for that last line as I was starting to get a bit confused :) Def. different over there!

Disclaimer: I’m so risk non-adverse that I don’t ever see the point of paying off very low-interest debt, when that money could be invested in the market.

So for mortgages, 30 years it is anytime rates are this low.

– More flexibility

– Bigger interest tax deductions

– Extremely high chance the market does better than 4%

– You’re a FI person, so you’ll actually invest the extra savings properly, and not waste it

The main thing that doesn’t make this good general advice is that the majority of people are terrible with money. Most people say they will invest the money, but life gets in the way… If you can take behavioral economics out of the equation, then this is actually still a very low risk proposition.

Good points Sparks. With the change to the standard tax deduction for married filing joint (it’s been doubled this year), it’s almost impossible to use an interest tax deduction since you’d need to itemize everything to include it. But, I’m also not an accountant so I don’t know all the ins and outs.

That’s true, I firmly believe the market will do better than 4% over the next 30 years, if it doesn’t, then we’re all in trouble :)

Agreed with all of these, but it’s also SUPER FREEING having no debts too if you’re an emotional human being like I am!! :)

Two-ish years ago we went through a “worst” case scenario – job loss, single income family and still had a mortgage.

Here’s our history.

We took out a 30 year and paid PMI on our first house, until a year later we were able to refinance to a 15 year, eliminate PMI and because we were able to eliminate PMI and lower the interest rate, our payment on a 15 vs. a 30 wasn’t much different. Eventually we refinanced again to a 10 year.

Then we sold our first house, bought our second house and did a 15 year. We were debating between a 10 and 15 year loan, but decided to compromise by paying extra on the 15 year and putting a little extra aside in case of emergency.

When we experienced job loss it was tough, but we had savings to get us past the rough patch. We then aggressively paid our mortgage off (2ish years).

The only thing we wish we would’ve done different is to be more aggressive with paying the mortgage off sooner.

Good luck to you!

More aggressive than 2 years???! That’s incredible!! Haha….

More aggressive paying our mortgage off from the beginning – from the first mortgage we took out on our first home.

There are a whole lot of comments on here (and I didn’t read them all) so please forgive me if my comment is repetitive. I think it’s wise to run the numbers and then see how much you will save by choosing a 15. Then you have to run that savings by your risk tolerance (and your wife’s of course) and the odds that you wouldn’t be able to pay. Is your wife likely to lose her job, be laid off, etc?

You may also feel more comfortable with a shorter term if you have access to cash. This would be in places like savings, your brokerage account, and contributions to your Roth IRA. You would have to sell investments in some of those accounts, but you could get access to money if you desperately needed it.

Have you ever run a calculation to see how long you could survive off of your cash, Roth contributions and brokerage account? Sometimes it helps to realize you have enough for “x” number of months. If bad times occur you’ll feel confident that you have a little time to get back on your feet.

Totally!

I haven’t ran the numbers in a long time but it does sound fun so i’m adding it to my list for later :) If only I could do it with my SEP too where the majority of our $$$ is!

Hey J,

Congrats on getting closer to a house! It’s a good question you bring up and has lots of different opinions…

If it’s your house and you see yourself staying there for more than 5 years, then go with the 15 year :) It is only like 40% higher monthly payments and you obviously save over 100k in interest. It’s worth the lower interest rate.

I mean, could you really sleep knowing you could have gotten a lower interest rate with a 15 year? :P

If, however, you’re investing in long-term buy and hold rentals, then you want to leverage them out over the long-term if cash flow is your number one priority. That’s what we’re doing. Rentals on a 30 year. When we buy our “dream house” that we’ll live in for a while, then I’ll do a 15 year or just pay in cash.

Good luck!

Let me get through this first house and then we can visit rentals, haha…

16.5 years ago we started out with a 30y mortgage. At the time this made sense to us as we were just starting out and that’s what we could afford. We absolutely expected to increase our earnings, but made decisions assuming our wages would remain steady or dip rather than rise.

Several years later we earned roughly twice what we did then, plus had investments. Interest rates were down, so we refinanced at a much lower rate. Since we could get an even better rate at 15y and could more than afford it, we took the 2.875% and ran with it.

It has worked out very well. We could have still gotten a great rate at 30y for flexibility and just paid double, but I am self aware enough to doubt that would have happened consistently. As it is, I regularly pay an extra $50/mo to principal. We’ll have it paid off before our eldest graduates high school.

Yayyy!!! Congratulations!!

We faced the same dilemma a number of years ago and ended up going with a 10 year mortgage and I think it was the best thing we did. While everyone else was using their house as an ATM we paid off our mortgage. The interest rate is even lower than a 15 year mortgage and it sounds like you are living within your means and have enough cushion to ride out any downturns.

Totally going to find out and run those numbers just to see ;) I fully expect to pay off our mortgage under 15 anyways, but not sure I’m that confident locking in a 10!

I’ve had both the 15 and 30. I’d go with 15. 26,000 is still a big savings. Let an emergency fund keep the pressure off. When you’re in your late 40s early 50s you’ll really appreciate having no mortgage. It gives you so much freedom and it’s awesome owning your home.

Oh man, the idea of a 30 year mortgage is crazy to me.

I don’t know what my life will look like in 3 years, let alone 30. All my friends had 30 year mortgages and all of them have sold their houses in less than 10. And now have NEW 30 year mortgages.

I bought a 8/1 ARM figuring that I couldn’t plan for eight years in the future and I’d save enough to pay it off by then.

I’m only six years in and could pay the mortgage off three times over.

I vote plan for the next ten years. Do what’s cheapest over the next ten years. Because likely life will be different then and you’ll have to reconsider no matter what.

I was all for your 30 year option until you mentioned that insane saving on interest!

In that case I would go with the 15 years and keep a good emergency fund of 6 months so even if things are tight you’ve got 6 months to figure it out. And of course always be ahead on your mortgage payment so you have an even bugger buffer! I went in at 30 years as I bought my house I was 24 and as far as I knew – everyone did it – haha but we still got an amazing rate and we are on target to pay it off in 10 years total anyway *fingers crossed* so didn’t really matter anyway :D

Good luck on the house search, how exciting! Keen for updates!

10 years is awesome!! Well done!

I’m saying this as a) someone who has not actually purchased a home herself and b) a spreadsheet geek. But I know I’m singing to the choir on part b.

When I do eventually buy a place, assuming I can’t just pay cash for it, I’ll probably get a 30 year mortgage. But each month, I’ll consult my handy dandy amortization spreadsheet and pay that month’s payment + the next month’s principal. If I’m feeling especially flush, I’ll pay the next two months worth of principal. In the early years, because the principal is so low compared to the interest, it’s not actually that much more money, but each time you pay an additional month’s principal, you’ve cut one full month off the back end of the loan. The amount I pay each month would then increase gradually over time, as the principal payments are a bigger and bigger proportion of the total, but presumably my income would be going up as well.

Of course, I’m also a happy renter in DC, so this isn’t on the immediate horizon, but I have a grand time playing with amortization spreadsheets and calculating it out to see the effects.

This plan is EMINENTLY doable – it’s exactly what I’ve been doing for the last 9 years and I LOVE seeing the overall loan term move UP the spreadsheet every month :D

Yes to all of this!!!

But more especially to the “happy renter” line, haha… I’m definitely going to miss it! ;)

Go for the 15 year. The extra you are paying is equity to yourself. Take out a Heloc for emergencies. Especially true if you are not itemizing.

Dave Ramsey says research shows 92% of people with a 30 year mortgage never make extra payments! That was my thinking about my first mortgage too and I never managed to pay extra on it either!! Statistics don’t lie. Stick with the 15 year mortgage and eat PB and J a few times a month:)

I eat PB&js a few times a *week*! For pleasure!! ;)

Make sure to bounce those rates and closing costs back and forth between the lenders. Just recently purchased a few rentals and got about .5 percent lower and less in closing.

Oh nice!! Excellent idea.

If you’re looking in Northern Virginia, home values are very high and have been increasing annually. That will add $$ or $$$ to your mortgage rate to cover additional taxes.each year your home goes up in value. I’m in Lorton, just south of Springfield mixing bowl. Reach out if you have any questions. Good luck in your search!

Thanks man!! I hear you on the rising values!! Wishing the next crash would have already happened by now, but can’t always time your life around these things :(

Not sure you mentioned how long you plan to stay in the house. Even if people think it is their forever home; the average folks stay 7 years in a house because your taste and life circumstances may change. Get a 7/1. If you decide to stay longer you can always get a longer term later.

We def. plan on being there at least 7 years – possibly even 15! – but you’re right that we need to check out some of these other options as well… Totally forgot about ARMS until seeing everyone’s comments, thx.

I bought my house in 2010 and went with the 30 year mortgage because it was my first time being a homeowner, I was paying the mortgage by my self and wanted the safety net that came with having my *required* mortgage payment be only $768/month. This was technically slightly less than what I had been paying in rent ($825) – but doesn’t take into account HOA and property taxes – but at least I was in the ball park.

All along though, my plan had been to make much larger payments – I’ve actually ended up on track to pay off my mortgage in 10 years. So yeah, I paid some extra interest than if I’d had the 15 year mortgage and made the same payments – but the security of having that low required payment, gave me a lot of peace of mind over the last 10 years, and i feel it was totally worth it.

Thanks spiffi – that definitely seems to be the overall consensus from people here.

I’m glad it’s been working out so well or you :)

Either way you go, you can’t go wrong.

We have done the 15 year as well as a 30 year mortgage. And as she suggested, we DID have job loss and were thankful that the lower payment on the 30 year was still affordable, despite less income. For you, though, that may not be a worry…

Anywho, bank loans are just another name for “legal loan sharking.”

HAH! Good thing though or else no one would ever own homes these days :)

I’m right there with you on the house hunting (in the same region and price point none-the-less!) and I personally will be going with the 30 year. As most have mentioned there is just the safety of the flexibility that if something were to come up, you know you have that “cushion” every month, but can always pay extra towards the principal.

I bought my current home almost 10 years ago and got a 30 year loan (that was because I couldn’t afford the payments on the 15 at the time!) and by paying just a little bit extra towards the mortgage each month I’ve already shaved about 5 years off my loan. But on those months that the budget was tight, i was able to reign in my payment for that month and put the money where is was more needed.

But, I have to say, I am a single person trying to buy with a single income, so that definitely makes a difference in my reasoning to pick the “safe” choice in this scenario. If I lose my job, or become ill, then I’ve got nothing but my EF to use to pay the bills, whereas you have two incomes so the blow wouldn’t be as hard.

You will always second guess your decision, at least I do, because there are positives and negatives for both choices. But once you make that decision don’t focus on the what-ifs. You”ll have made the decision based on the best information you had at the time. (and, you can always refinance to a loan with different terms if you absolutely felt the need to!)

Good luck with the house hunting! It’s a scary place out there for buyers in the DMV right now! :)

YES INDEED!!! Haha….

The market is so hot all of a sudden!! I hope you’re able to find your next Great One too pretty smoothly! :)

I’m praying a house comes up around Easter when no one’s looking and will be easier to snatch up :) I used to be a realtor wayyyyy back in the day, and the two – and only two – houses I ever helped people buy were both around holidays haha… No one to compete with!

And you’re right on the safety part with being solo… Good call.

Go with a 15 year. The interest in the first 5 years of a 30 year makes me want to vomit. Starting with a 15 year makes it easier to get down to paying it off in 10. Maybe angle to be mortgage free by the time your oldest goes to high school / college?

Totally planning on having it paid off by then! Don’t want that hanging around in early retirement! ;)

I didn’t read all the above comments, but part of my college funding plan for my two kiddos is to have the mortgage paid off by the time #2 starts college, hopefully sooner. My husband graduated debt-free, and that is my goal for my two kids. I don’t want them burdened by graduating with what essentially amounts to a mortgage payment.

I like it :)

I would check with your accountant. With the current federal income tax changes, rent vs. buy is a much simpler equation. With the $24,000 standard deduction for a married couple, and the $2000 tax credit per dependent minor child under age seventeen (not totally refundable), many people will find no tax benefit to home ownership whatsoever, in which case either paying cash outright or having total housing related costs (including everything) lower than or equal to rent would make a lot of sense.

I have never purchased a home, so I have a lot of ignorance here, but I’m curious…if you went with the 15-year loan, but then changed your mind to gain more flexibility, is it possible to convert to a 30-year?

Yup!

But you’d have to refinance and go through the process all over again, as well as probably pony up some money too… (and that’s *if* your house is still worth what it needs to be to refi)

Get the 15!! My advice to you.

Or, go with a 30 year and pay as much as you can on it each month, 1 1/2 payments or double payments as long as you can. Then, if the need should arise, you can pay your lower mortgage payment if times get tough.

We started out with a 30-year mortgage, paid extra most months, then refinanced a few years later to a 15-year mortgage. 2017 we paid off the mortgage after only 18 years. The feeling of freedom and security we have now is awesome. A few months ago, we paid off the last of our debt, a car. (yes, we did things a little backward) We are now DEBT FREE!!!)

YAYY!!! Congrats!!! That is huge!

Hi J Money,

Of course, there are pros and cons to both!

If you go for 15 years, you would be in the mindset of paying it off as early as possible. Meaning that it would be priority no# 1. Owning your own house would be such a relief, knowing that no matter what happens to your investments (or your job), you always have a roof over your head. If you have it set at 30 years, the loan may suddenly drop to priority no#2 or no#3.

Another possible consideration with the longer mortgage is that you will have 30 years to pay off the extra $125K. Assuming you invest the extra $633 per month (the difference between 30 and 15-year mortgage repayments) for the next 30 years, you will earn $800K (based on 7.2% p.a.). If you minus the initial $125k extra cost, thats a total gain of $675K. Through this method, you would have invested enough to have paid for the $280K outright in 18 years.

As a few others have said, there are options if you want to repay a 30-year loan faster, or on the other hand, if you need to refinance a 15-year loan.

Keep us updated!

Matt

I like that idea of the mental priority of it being #1 – hadn’t thought about that before :)

Five years ago I would have said go with the 15yr but financial flexibility is worth a lot. We started out with a 15yr then had a kid, we still made it work but obviously our expenses went up. Then we were about to have a second kid and refi to a 30yr. We could have made the 15yr work but it would be extremely tight until the kids got out of daycare. While I know I’m paying more in interest, financial stability and flexibility gives me a lot of peace of mind. Our interest went up .5% when we went to the 30yr.

I will $hit a brick if I have two more kids, but yes – I hear ya, haha…

Definitely a 15 year mortgage. I did a 15 year, was laid off in year 13. We used my severance and vacation payout to pay off the mortgage and retire mortgage free. Fear of being laid off is what a 6 month emergency fund is for. If you have a good career you’ll find another job. Worst case if you have to sell the house you’ll have more equity.

Oh wow – i’m glad you got enough to pay it off in the end!!! That’s a helluva parting gift! :)

Don’t let the interest rate difference be an issue between the 15 and 30, as you can prepay points on either loan to wash any difference for minimal upfront. Go for 30, you will have it paid off in 10-12 years.

I think there’s only so much you can buy though, right?

Hi again J,

For me I think it would depend mostly on the % that is offered. I am in the proccess of moving house and have accepted 2.04% for 5 years fixed, so was happy to take that on a 21 year (random number I know) mortgage. With your situation between 3.17% and 3.94%, 15-20 years wins every time! Each to their own but I think if I took the 30 saying I would overpay, this leaves a lot to our complicated brains to come up with excuses for not doing it. That maybe returns in the market are more appealing.

I was debating with the Mortgage Advisor over different companys to shave off every 0.1% I could. Kind words of wisdom for everyone, but the cheapest deal on the list paid a lot less off the mortgage and would cost me more in the long run, though cheaper for those 5 years.

Loved this as it is very relevant to my life right now.

Cheers.

Oh good!

Great timing indeed – I hope it goes smoothly for you!

Thanks for chiming in! :)

I would like to give Kathy a big (hopefully welcome) virtual hug.

100% the way I’d go.

There are not just 2 points in time or numbers to look at. Is there any reason you think the next 15 years will have a market return that’s way below average?

Even Jan ’00 – Dec ’14 had a 15 year CAGR of 4.2% and it was the worst decade of my life.

Jan ’96 – Dec ’10 (with the same crap decade) returned 6.76% CAGR.

If you take the difference in payment and save it, you are almost guaranteed (Ok, not 100%, maybe just 97.38%) to have more in the savings than the mortgage balance at year 15. I wrote an article “Retired with mortgage” that shared my own decision on this issue. I have 8 years left on the mortgage now, but far more in my 401(k) than the mortgage balance was at year 15. And most of the 401(k) was saved at 28%-33% tax rate vs coming out at 22%-24% now.

If inflation come back, you will pay the mortgage with cheaper dollars. Wouldn’t it be great to owe $250K at sub – 4% while ‘getting’ 5-6% in the bank? But. If we have another bad recession, you might refi even lower.

Congrats on this next chapter of your life, Jay!

Thanks Joe!

Shaping up to be an interesting adventure already, haha…

And at least getting some new blog fodder off it! ;)

We’ll see about the mortgage stuff though… I’m still not convinced either way, so it might just be a matter of what my wife is more comfortable doing in the end… still need to have “the talk” with her – hah.

FWIW – I pulled S&P data for the last 65 years, and calculated the cumulative returns for each possible 15 year period. The CAGR for 24 of the 50 period was over 10%, the next 6 best period were 8-10%. There were only 5 periods that were under 5%, with the lowest 2 returning 4.2%.

If a casino offered you these odds, 50% chance of ‘jackpot’ (the middle scenario shows a mortgage balance of $180K at year 15, but ‘savings’ of $285K) a 40% chance of a nice return, and just a 10% chance of breakeven to being down a tiny bit (due to order of returns, the 5.4% CAGR for the 15 year period failed in 2011, with a 20K shortfall, but with patience, 2012/2013 put the strategy spectacularly in the black by over $60K.

Note – I used your 2 mortgage rates for 15 and 30 year loans at the $280K you stated. I ignored tax savings on interest, because that would add a layer of complexity I really didn’t need to prove a point, although if you took the deduction, 22% (?) would really make even that worst case scenario positive. I can send the spreadsheet over, just need to fill in how I did some of the math.

I trust you! Haha… You’ve been on this Earth longer than I :)