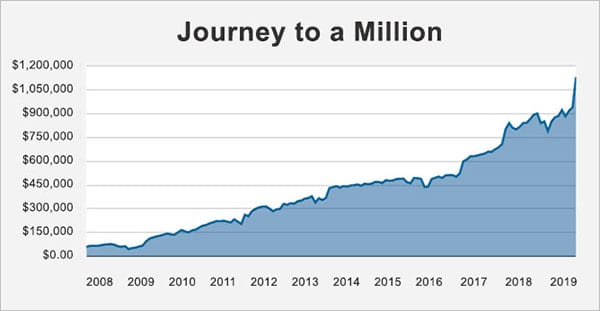

[UPDATE: We did it!! We hit $1,000,000!]

Here’s every single month of tracking my net worth, going back over 5 11 years to the very first one I did in February, 2008. Complete with links to all blog posts where I broke down the month in detail – daddy don’t play around! ;)

If you’re asking yourself why someone might do such a thing, here are three reasons for you:

- It holds myself accountable (numbers don’t lie!)

- It keeps myself motivated towards the dream of a Milly (click to see how I’ll reach it)

- It reminds myself that it’s all a journey. Which is important for someone with A.D.H.D.

I highly encourage you to do the same if you haven’t started already (if you’re a regular reader of this blog you better be! ;)) There are a billion ways to track it, but I prefer using a plain ol’ Excel spreadsheet that I manually update at the end of every month. This forces me to stop and soak things in before moving on to the next shiny thing.

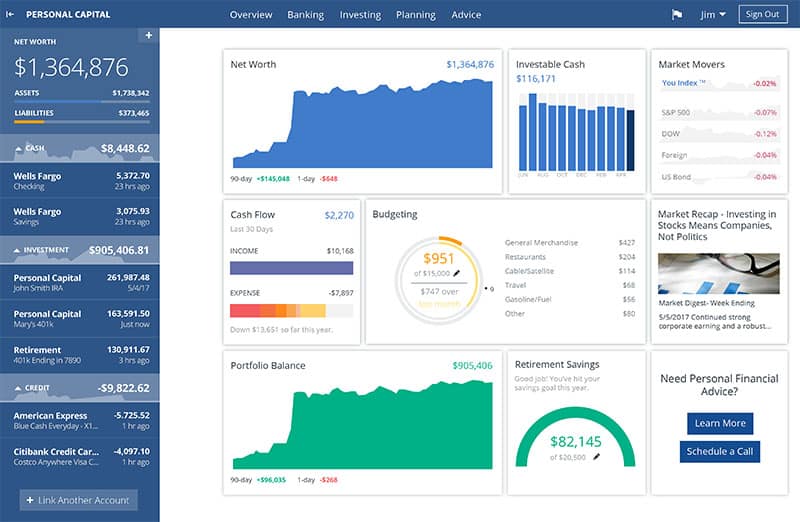

Here’s the exact template I use – complete with budget built in and all: J’s Financial Snapshot. If you’re not a spreadsheet guy and prefer something more automated (which is fine, whatever gets you to take action), you might wanna grab yourself a free Personal Capital account.

Personal Capital is fantastic tool that connects with your bank/investment accounts to give you an automated way to track your net worth. You’ll get a crystal clear picture of how your spending and investments affect your financial goals (early retirement?), and it’s super easy to use.

It only takes a few minutes to set up and after that everything is automated, so if you’re serious about tracking your net worth as you build your first million, you can grab your free account here. They also do a lot of other cool stuff as well which my early retired friend Justin covers in our full review of PC – check it out: Why I Use Personal Capital Almost Every Single Day.

(There’s also Mint.com too btw which is also free and automated, but its more focused on day-to-day budgeting rather than long-term net worth building)

How to Calculate Your Net Worth

There’s a ton of different ways to calculate your “net worth,” but technically speaking it’s:

All your Assets (savings, investments, property, etc) minus all your Liabilities (credit card debt, student loans, mortgages, etc) – that’s it.

Whatever number that equates to is your net worth. If you’re not sure what you should include and what you shouldn’t, just start tracking the parts that are important to you and you can tweak it over time. You can also check out this list of Blogger Net Worths I put together on my other site too, which will give you a good idea of how others calculate it (and even more juicier – what *their* net worths are ;)).

But again – this number is for YOU. Nobody cares as much about our money as you do, so always make that #1 priority. Include whatever makes the most sense to you!

Okay. Enough jabbering… Here is my complete list of all net worths I’ve tracked going back to February of ’08. The good, the bad, and even the most ugly months ;) But we “started from the bottom now we here!” – Drake.

2019 Net Worth:

- Aug: $1,131,601.03 (+$190,000 – WE DID IT!! We hit a million!)

- Jul: $940,412.06 (+$20,000)

- Jun: $919,538.34 (+$35,000 – Market rebound)

- May: $883,910.63 (-$40,000 – Markets crash…)

- Apr: $923,966.07 (+$37,000 – Markets continued climb)

- Mar: $886,776.74 (+$9,000)

- Feb: $877,998.20 (+$29,000 – Markets up)

- Jan: $848,665.47 (+$57,000 – Surprise Increase?!)

2018 Net Worth:

- Dec: $791,150.37 (-$61,000 – MARKET MELTDOWN)

- Nov: $851,800.32 (+$9,000)

- Oct: $842,180.92 (-$60,000 – MARKET SPIRAL!!!)

- Sep: $902,133.51 (+$8,000)

- Aug: $894,310.86 (+$27,000 – Markets up)

- July: $867,121.96 (+$23,000 – Markets up)

- Jun: $843,567.22 (+$2,000)

- May: $841,903.39 (+$24,000 – Markets up)

- Apr: $818,204.91 (+$16,000 – Tax refund)

- Mar: $801,707.30 (-$10,000)

- Feb: $811,570.54 (-$29,000 – Markets crash)

- Jan: $840,243.99 (+$37,000 – Markets up)

2017 Net Worth:

- Dec: $802,949.84 (+$93,000 – Sold a website)

- Nov: $709,372.08 (+$21,000 – Markets up)

- Oct: $688,210.30 (+$12,000)

- Sep: $675,681.17 (+$16,000)

- Aug: $659,786.34 (-$600)

- July: $660,442.69 (+$12,000)

- June: $648,316.94 (+$5,000)

- May: $643,155.75 (+$6,000)

- Apr: $636,893.40 (+$4,000)

- Mar: $632,301.91 (+$700)

- Feb: $631,547.73 (+ $20,000 – markets up)

- Jan: $610,770.25 (+ $10,000)

2016 Net Worth:

- Dec: $599,826.38 (+ $75,000 – new partnership)

- Nov: $524,910.47 (+$22,000 – markets up!)

- Oct: $502,883.49 (-$10,000 – market down)

- Sep: $512,820.73 (-$200)

- Aug: $513,016.99 (+$1,000)

- Jul: $511,782.60 (+$17,000 – market growth)

- Jun: $494,758.25 (-$9,000 – bought a car)

- May: $503,939.92 (+$8,000 – HALF-A-MILLIONAIRE STATUS!)

- Apr: $496,016.17 (+$8,000)

- Mar: $488,217.20 (+$48,000 – market rebound + taxes + gift)

- Feb: $440,023.40 (+$2,500)

- Jan: $437,562.07 (-$51,000 – sold house + market crash)

2015 Net Worth:

- Dec: $488,967.81 (-$4,000)

- Nov: $493,424.80 (-$2,000)

- Oct: $495,297.66 (+$34,000 – market come back!)

- Sep: $461,580.18 (-$7,000)

- Aug: $468,391.43 (-$23,000 – market crash!)

- July: $491,174.40 (+$1,000)

- June: $489,886.10 (+$2,000)

- May: $487,648.94 (+$8,000)

- Apr: $478,907.13 (+$1,000)

- Mar: $477,624.11 (-$3,000)

- Feb: $480,609.75 (+$17,000 – market up!!)

- Jan: $462,741.66 (-$7,000)

2014 Net Worth:

- Dec: $469,631.26 (-$500)

- Nov: $470,167.09 (+$10,000 – market up)

- Oct: $459,266.46 (+$3,000)

- Sep: $456,140.18 (-$3,000)

- Aug: $458,924.81 (+$13,000 – market went up)

- Jul: $445,934.49 (-$8,000)

- Jun: $454,218.23 (+$5,000)

- May $449,527.32 (+$2,000)

- April: $447,240.46 (+$7,000)

- March: $440,520.07 (-$3,000)

- Feb: $443,799.65 (+$10,000)

- Jan: $433,149.74 (-$10,000)

2013 Net Worth:

- Dec: $443,561.57 (+$6,000)

- Nov: $437,088.81 (+$6,000)

- Oct: $430,950.10 (+$62,000 – Sold some sites)

- Sep: $368,618.16 (+$12,000)

- Aug: $355,921.34 (-$11,000)

- July: $366,913.82 (+$27,000 – House value ↑)

- June: $339,921.97 (-$40,000 – Perfect Storm ↓)

- May: $379,397.06 (+$11,500)

- April: $367,855.72 (+$3,000)

- March: $364,600.94 (+$12,000)

- Feb: $351,979.18 (+$5,000)

- Jan: $346,969.28 (+$14,000 – Market uptick!)

2012 Net Worth:

- Dec: $332,608.93 (-$3,000)

- Nov: $335,866.43 (+$10,000)

- Oct: $325,990.16 (-$5,000)

- Sep: $331,530.72 (+$30,000 – Sold a site + Hustlin’)

- Aug: $300,032.81 (+$3,000)

- July: $296,797.00 (+$12,000!)

- June: $284,665.99 (-$16,000 – House value ↓, Loss of 2nd income)

- May: $301,195.59 (-$14,000 – Market swings)

- April: $315,258.43 (+$1,000)

- March: $314,246.43 (+$5,000)

- Feb: $309,002.70 (+$10,000!)

- Jan: $298,449.90 (+$13,000!)

2011 Net Worth:

- Dec: $285,368.44 (+$32,000 – More hustlin’)

- Nov: $253,545.67 (-$9,000)

- Oct: $262,425.97 (+$60,000 – Inheritance + mad hustlin’)

- Sep: $204,762.73 (-$15,000 – Market spiraling!)

- Aug: $219,283.45 (-$14,000 – Market crashin’)

- July: $233,453.70 (+$20,000 – Got long lost 401(k) back!)

- June: $214,025.67 (-$5,000)

- May: $219,609.14 (-$5,000)

- April: $224,724.81 (+$3,000)

- March: $221,941.10 (-$1,300)

- Feb: $223,270.25 (+$10,000!)

- Jan: $213,832.79 (+$5,000)

2010 Net Worth:

- Dec: $208,485.96 (+$10,000!)

- Nov: $198,019.06 (+$5,000)

- Oct: $193,025.18 (+$11,000!)

- Sep: $181,641.37 (+$13,000!)

- Aug: $167,997.16 (+$3,500)

- July: $164,387.81 (+$14,000 – Market roaring!)

- June: $150,815.98 (-$7,000)

- May: $157,729.89 (-$9,000)

- April: $166,261.93 (+$15,000 – Tax refunds + Market up)

- March: $151,355.70 (+$15,000 – Maxing out 401(k) early!)

- Feb: $136,496.68 (-$1,500)

- Jan: $138,033.98 (-$6,000)

2009 Net Worth:

- Dec: $143,817.65 (+$7,000)

- Nov: $137,838.30 (+$7,000)

- Oct: $130,706.36 (+$4,500)

- Sep: $126,207.64 (+$6,000)

- Aug: $119,810.05 (+$6,500)

- July: $113,210.89 (+$18,000 – Back to maxing out 401(k) aggressively)

- June: $95,149.11 (+$27,000 – Got old 401(k) money owed to me!)

- May: $68,061.80 (+$5,500)

- April: $62,535.77 (+$7,000)

- March: $55,609.58 (+$3,000)

- Feb: $52,331.20 (+$7,000 – Tax refund)

- Jan: $45,070.34 (-$13,000 – Major loss in house value + Merged money with Mrs.)

2008 Net Worth:

- Dec: $64,189.42 (+$3,500)

- Nov: $60,532.07 (-$3,000)

- Oct: $63,566.66 (-$10,000 – Major meltdown)

- Sep: $73,360.56 (-$4,000 – Market starting to tank)

- Aug: $77,460.40 (+$1,300)

- July: $76,093.30 (+$2,500)

- June: $73,547.62 (+$4,000 – Wedding over = savings!)

- May: $69,425.23 (+$3,000)

- April: $66,491.68 (-$1,000 – Wedding expenses)

- March: $67,059.63 (+$1,000)

- Feb: $66,153.27 (+$7,000 – Tax refund + 401(k) back pay)

- Jan: $58,769.65 (-$2,000 – 1st time posting my net worth online!)

How’s your journey coming along? You tracking YOUR money too, right?

Again, the point of this isn’t to brag or show off numbers, but to hold our selves accountable and to continue REACHING for our next higher goal. And the only way to do that is to know where you stand at all times! So please please PLEASE start tracking where all your money’s at. You don’t have to share it with the world like us crazy bloggers, but do keep it somewhere so you can access it (and update it!) with each passing month.

Good luck! :)

—–

PS: After spending some time soaking all this in, I realized a majority of the success here came from only focusing on one main thing: Retirement accounts. Yeah I hustled my ass off and got lucky here and there too, but the bulk of this success was maxing out both my Roth and my 401k/SEP every single year. You invest $20,000 a year and your wealth will explode too! Even if you never did anything else.

[UPDATE: Here’s a breakdown of the 7 main forces behind growing our net worth to over $900,000 to help put things in better perspective. Published in May, 2019]

PPS: Investing in retirement accounts works because tax deferment/tax reduction lets the power of compound interest work on a bigger chunk of your money. On the other hand though, a lot of institutional retirement plans are loaded with hidden fees. Even tiny fees have a massive impact, because you end up with the power of compound interest working against you. That means those fees can reduce your lifetime savings by hundreds of thousands of dollars.

Its pretty mind-boggling how tiny %s can compound into life changing amounts of money when you let it grow over the years. You can use this free fee analyzer tool to analyze your retirement accounts and figure out if you’re paying any hidden fees.![]()

![]()

*Links to Personal Capital above are affiliate links, meaning we’ll get compensated if you end up trying them out. Really great (and free) product though we think you’ll love.

Enjoying the site and it’s always nice to see progress like this, but to be fair you picked the best time to invest. Starting at the bottom in 2008 and having a five year bull market to assist your growth.

Having read lots of FI blogs starting around the same time, I’m interested to see how things work out when the next bear strikes.

True, but also at the same time my house value plummeted as well – helping to even it out ;) As did the first chunk of investments I had before the crash too before it made a come back.

But you’re right – it’s been a damn good time to invest. And when it crashes again (‘cuz of course it will) I’ll just continue picking up more funds (on the cheap!!) knowing it’s all about the end game years down the line. Which is the beauty of starting out early in life – plenty of time to let it grow!

You nailed it. Keep investing during a bear market. Stay the course and keep buying VTSAX on the cheap and at the same time adjust your asset allocation slowly into bonds as you get older.

That is one awesome looking chart :) We have been working on maxing out our IRA’s, and your right, if you stay focused on it, before long it’s amazing what you begin to accumulate. And yes, the awesome market has help for sure. I am interested to see what everyone’s net worth does during the next recession, whenever that might be. In the long term, the market goes up, so best to stay focused and invested!

You know it! Plenty of pros in a down market too, so as long as we stay on the mission we really can’t go wrong :)

THIS!

Love it.

YOU!

Love! :)

Love this I need to start tracking my money, I belong in the lazy bunch

Please do! Doesn’t matter what stage in life you are either – just merely tracking it will help you mentally get better over the years :)

So much transparency, great stuff! Love the look of that graph… J$ keeps on moving on up!!!

Thanks man! If I were a smarter man I’d start going down your route with real estate too :) You’re graph is going to look a lot sexier than mine as time goes on!

Love this! I wish I could track mine on my site, but the hubby says no ;-(

Tracking it personally now with mint- but I do think publicly posting is a great way to stay accountable and FOCUSED for all of us with ADHD.

Hah! Indeed.

As long as you’re tracking it though it’s good in my book :) Only crazies post their numbers online for the world to see (double hah!)

I just noticed our net worth numbers are within a thousand dollars of each other!!!

Sweet! Are you going to copy me all the way up to a million too? ;)

I’ve been using Mint.com for several years, and I love seeing how compounding and small changes in my lifestyle has made a huge difference in the bottom line. Just checked back to see my “net worth trend” and I was at -$150,000 in 2010, but on the plus side a whole $38k now, with student loans paid off and the car almost paid off! Can’t wait to drop that debt and only have my underwater mortgage left. Probably a year left until I get to scream and shout like you did with your no-longer-underwater-mortgage. It’s been a long 8 years already being underwater… maybe my next career is in pearl diving? :)

HAH! That’s a crazy ratio you got going on too. You’re averaging $50k in increase every year! Way to go!

I like the net worth tracker. I find that for me, seeing the ups and downs while my investments are still marching towards that goal of early retirement keeps it real and in the front of my head. I’d accumulated a lot of credit card debt and school loans and it wasn’t until I started tracking spending and assets with a simple spreadsheet, that I was able to rein it in. Now I’m ~5 yrs away from financial independence and getting to transition from dual income to dual stay at home parents. Tracking my spending and investments was key to getting on the path to FI.

Rock on! I love to hear that!! And I totally agree – the tracking part of stuff does wonders, no matter what stage of the game you’re in. I hope to reach your guys’ stage too in the near future – congrats :) And now of course I have to go check out your blog… while sipping coffee.

JMoney, looking good man, you have come along damn way since you started. It has just been recently that i started throwing all of my expenses together to see where i am sitting financially speaking. I dont know if turning 30 was what happened or getting married and soon to have a kid is the reason for doing it but i love it.

Do you find that by running this website and keeping track of your networth you are getting overwhelmed in it all? Seems to me like the more i write stuff down and think about it the less i can think about other things even when its time to goto sleep.

Anyways I’m going to keep tuning into your blog, i like reading the articles and looking at peoples net worth as well. I don’t do it for a competition but its nice to know that there are people out there that take this shit as serious as me.

Tossing around the idea of starting my own little financial blog but have never done anything like that before so i don’t really know if it for me or not. Don’t even know how i would get people to read it to start with.

Keep up the good work, I look forward to seeing you hit 1m$

I actually go into two phases with this stuff: 1) When i get things out of my head and online it helps to free up my mind :) but on the other hand, 2) I do get sucked in and end up thinking about money, net worth, life, career, etc a lot too since I now do this stuff full-time. It’s a hard balancing act for sure, but much better than not paying attention at all and just keeping my head in the sand :)

RE: Blogging – only one way to find out! If you’re passionate about it and enjoy interacting with others, give it a shot and see how you like it. I had no idea it would turn into what it did all these years later (I’m almost at 7 years of blogging now), where as I’ve quit 99% of all other hobbies I’ve tried in the pas too, haha… But you never know until you just do it and see what happens. There’s a lot more potential for opportunies out of a blog than most people (myself included) ever realized. Shoot us the url if you go for it and I’ll check it out :)

Signed up today, just waiting for everything to go through, apparently they don’t like the fact that my IP of where I am is over 8000km from my billing address.

Oh jeez, haha… well hopefully it works out in the end :)

I love this page, it’s just amazing to see the culmination of 6 years of hard work, saving and investing, in one ‘sexy’ little chart like that. I’ve always been a little less disciplined with tracking, but I’ve been slowly coming around to the idea of sharing this on my blog – setting some goals and being motivated to grow this thing! Was always reluctant to share this with the world, as I didn’t think anyone would care, but seems like some people find it interesting, and as you said, it’s more to keep you accountable anyway.

Think I’ll just share my stock portfolio though, as that’s the real focus for me – and don’t want to share everything with friends, co-workers and other acquaintances who might stumble across my site!

Hey man! Oddly enough I was literally just on your blog for the first time last night – I’m really enjoying it :) And I’d agree – stick with what you’re comfortable with especially if friends and people you know in the real world read your site. What’s the info is out there it’s hard to go back. And you can always divulge more later too if you change your mind…

Glad you like this page! It’s one of my favorites too. Amazing to see your entire financial life over the years in one spot. The benefit of being a financial blogger :)

Ha that is quite a coincidence! I’m thrilled you’ve made a trip to the Islands and are enjoying it :)

Definitely keen to get some tracking up and running soon on the site – especially as I’ve just gone and made my journey to financial independence a whole lot harder with the purchase of a new home! The extra motivation of putting my portfolio out there for others to see will hopefully help spur me along to great things :)

Oh boy. Yeah, that opens up a whole other can of worms in the personal finance world, haha… You might as well tell people you buy coffee every day! Hah! (But I’m with you – gotta do with what’s best for you and your family in any situation regardless of what others may think… But still keep an ear out in case they whisper words of wisdom that can help us in the future :))

Awesome site and I love the net worth pages! Will definitely be visiting the site often.

I’m glad, Michael – thanks for stopping by :)

Absolutely love the transparency. There is something about seeing real numbers that makes a personal finance blog seem authentic. I just recently got into the personal finance blogging world myself about 4 months ago. I knew from day one after reading your site and plenty of others that I wanted to be fully transparent to my readers.

How else are readers supposed to know if what you write about is actually working and worth there time? And the extra accountability and motivation that comes with posting your numbers out there on the web for everyone to see and scrutinize.

Its one thing to think about posting your numbers. I will admit that I hesitated this morning when I published my new financial stats page and the corresponding post announcing the new page and new detailed income/net worth report I would be publishing starting with January of 2015.

I am committed now. Looking forward to catching up to you. The wife and I have made a lot of progress over the past 3-years. At the end of 2012 our net worth was just $42,000 and at the end of 2014 it has climbed to $197,000. Should hit $200,000 in another month and then its on the march to $300,000.

I think we should be able to grow the net worth by about $60K to $100K this year without any market appreciation. We just initiated our 7-year plan in January to pay off the mortgage early. On top of this we will start maxing out an IRA for my wife (we already max out my 401K).

Thanks again for being an inspiration.

Cheers!

YES! Love to see this!! Being mortgage free would be incredible – on top of how fast your net worth grows and compounds over those 7 years. Good for you for jumping all on it, and then for sharing it with everyone online too. It really is amazing how much this helps people whether they tell you so or not.

Going now to check out your blog :) Congrats on getting it launched!

My graph isn’t the only sexy thing about me.

No, really, I’m an exotic dancer.

Hah – even better :)

i used to be of the mindset that was easily intimidated by large numbers, and would just wait and procrastinate. in fact i found your blog last year some time, downloaded the sexy budget template, and even used it for almost 2 months. then i stopped, and guess what, not much changed for me financially. i paid most stuff on time, side hustled here and there, was a water treader.

i got original at the end of december and went with pseudo new years resolutions. i found a net worth spreadsheet i liked, adapted to my needs and situation, and went crazy, filling it all out. my net worth, not-lol, is -10k. and i dont have a house yet.

but, in one month of not budgeting but consciously being aware of the fact that come feb 1st i’d be filling it out again, i went down to -6k. i have some massive side hustles going right now, made a niche site last month that showed a few dollars profit but is growing, am building out two other sites, and have been going crazy on amazon fba program. point is, i expect to be in the black in less than three months, which is ironic considering ive just begun really tracking.

i enjoy your blog, a lot, and i find many actionable steps here. its not only inspiring me to take control of my situation, it does so in less drastic means than mr money mustache for example, kind of bridging the gap between a consumer driven lifestyle and where i hope to go. ive always been a side hustler, but ive also always spent the earnings. now i am learning to apply them to true growth.

anyway, that is all. i don’t comment too much but i heard an old podcast from financial samurai on pat flynn’s podcast last night, and he said he tries to comment because he knows how much work people spend on their posts, and how good it feels to get comments. i need to engage in the community more to get all the benefits!!

keep up the good work, and thanks for the help.

Pat’s a smart guy, we love getting comments :) And we both respond to them too since we know YOU take time to share your thoughts with us as well! After all, we wouldn’t be doing what we do if no one read what we were writing.

Now as for your hustling and new mindset? BAD ASS man. Seriously. And I completely agree with tracking everything for a bit to really let things sink in. I don’t track every penny like I used to because I now know what the heck I’m doing compared to always *thinking* I knew what I was doing w/out looking at the cold facts. It really is amazing how much smoother your life gets too once you’ve solved the money puzzle… It doesn’t mean we never get into trouble again w/ $$$ (I’m always making dummy mistakes) but by and large it’s a lot easier to power through and keep growing that wealth when you’ve got the structure down.

So thanks again for stopping by and passing on your story. It all adds to a powerful financial discussion!

Man after a shortened february which we also vacationed in los angeles for 8 days (this was planned BEFORE i began my super tracking net worth turn-around) i still managed to up my net worth by 1100. just by making extra car payments (one of the two is almost done thank god), not charging stuff, and trading my keurig cups for a re-usable keurig cup i made a splash and a half.

oh, and side hustling of course. besides amazon fba ive now launched two affiliate sites since jan 1st, am currently working on two more, and a few other projects. all internet based for the most part, and all super exciting and foreign to me a few short months ago.

finally, for my last update, i heard a podcast you were on from jeff and mandy rose from a few years ago. i am really excited and grateful i am now entering this world. i hope you get used to me, i have a feeling im going to start turning up more and more.

Hah – no problem with that man, always nice to be surrounded by cool like-minded people :) Stop by anytime (and glad you liked the podcast! Those two are beasts!)

I’m digging the “Net worth over time” aspect of this page. I need to copy this for my own blog since right now the ambitious and curious reader has to track down my last 18 months of financial updates to see how my net worth changes each month.

Yeah, helpful to readers but even more so yourself. Pretty cool to have a nice tidy record of all your hustling over the years + pretty graph to look at :)

Anyone have any idea idea about counting a pension in your net worth? A friend financial planner said I could def count it. It’s worth about 1.32 million if I live until 80 (and to get the benefit I have to work for 22 more years for the system–which I plan to do). Thoughts? Suggestions? I need some help from all you sexy budgeters! Thank$$!

Well, the nice thing about net worths is that it’s totally up to you how you’d like to use/track them :) A pension to me seems more like an *income stream* than an asset – similar to Social Security and other “guaranteed” money later (hah!) – so I’m not sure I would include it personally, but if it makes sense to you to then by all means run with it. This is why I don’t include any paychecks or other streams too. That money can be used for savings and investments and debt payoffs which in turn go into the net worth calculations, but until that point it’s just income.

[A place where I *would* include it in, however, is in retirement planning calculations. Since that’s all about income and expenses. If you check out our Financial Freedom article I posted last week, you can find a spreadsheet there from one of my friends who included an area for pensions and the like. This will help gauge how much you need to live down the road – or at least a good estimate since we’ll never really know for sure until we’re there :)]

I get it, we’re calculating net worth right now. 401, 403, those have cash value w a penalty where the pension isn’t worth anything until I actually retire. I’ll check out the spreadsheet. Thx, J

J$, was just browsing through my Canada Revenue website and found a link to a bunch of my tax assessments, made me think back to your post in January 2014 about your LWR. Would you be interested in throwing that in to some future net worth updates? I think its a really good number to let you know how you have done lifetime, rather then just recently. I got a BIG surprise on mine and not a good one, i am sure that yours must have gone up since you calculated it last.

Interesting…. Not a bad idea at all actually. I’ll make a note for the next one and see I can do that for you :)

Here’s the post btw for anyone else reading this right now – it’s the “Lifetime Wealth Ratio” I made up that compares your total lifetime earnings vs what you’ve saved/invested over the years.

https://budgetsaresexy.com/2014/11/total-lifetime-earnings-wealth-ratio/

Iam new to the whole world of saving/ investing…financial illiterate making up for all the time I have spent living under the rock!:( am so glad to have come across this site…I can understand what is being discussed…love the laid back style of information output…andd…am inspired( never thought would say that about a finance site!)….thank you for being you! :)

HAH! Well welcome to our world of awesomeness here :) It gets better as your money starts getting better too! (Which is my job to help with)

J. Money!!!

I have been following your blogs/articles for a little while now and started tracking my net worth at the beginning of the year. I just logged by Q1 results and wanted to share with you.

Net worth @ 1/1/15 = $51,464.61

Net worth @ 4/1/15 = $60,707.87

That’s a whopping 18%! In just 3 months!! Ya dig?!?!??!

I’ve done this mostly by upping my 401k contributions, set up monthly payments to max out my Roth IRA and starting a brokerage account. Every dollar I used to spend (throw away) on random crap I now analyze how much it would be worth in 40 years.

I still have a ways to go. I spend WAY too much money eating/drinking out. I am getting married this October and will be merging accounts with the Mrs. pretty soon so that will present some road bumps.

Overall, I am very confident about my financial future and reading your blogs definitely helps. One thing I feel I need to point out to you though:

I see you put (almost) all our dough into a total stock market index fund. While that is a simplified method of investing and you certainly can’t beat those management fees I think you will lag the market for the next (possibly several) years. The market has been on a bull run for the past 6 years and while overall index funds do well when the market is going strong a more diversified portfolio can do wonders for you in terms of risk reduction and overall return.

This guide lays out 10 ETFs that construct a completely diversified, low cost portfolio:

http://seekingalpha.com/etf_hub/etf_investing_guide

I use a modified version of this portfolio for my rollover IRA. I am only 25 so I am light on bonds right now and will slowly start upping that % as I get older. I also use actively managed funds in my Roth for more diversity. Anyways, I just wanted to share my 2 cents. Thanks for everything and keep up the good work!

J Money!

I’m not gonna lie… I am a little bummed you haven’t replied to my last comment.

But no matter, I will keep replying month over month with updates until I get some acknowledgement ;)

Net Worth @ 5/1/2015 = $63,234.44

That’s up 22.87% since the beginning of the year!!! I am still pumped, but I know I could have saved more. I went to Vegas this month and definitely spent more than I should have.

This month is going to get tough as I am currently locking a mortgage and will need to come up with closing costs/ appraisal fees/ etc. On a more solid note, most of my stocks in the brokerage account killed it on earnings this quarter and that portfolio is up ~12% year to date.

Drop me an email when you are ready to talk about investments my friend!

Yo!

I’m so sorry dude – I don’t know how that first comment eluded me.

I love everything you said!! Even the parts you disagree with my overly simplified strategy :) You’re probably right, though everyone says something that makes sense to me (hah!), so I’ll adjust as time goes on, but for now baby steps… It took all my energy to move my funds over and get decently aligned here, so next will be tweaking it when I’m ready to dive in again. As you can tell, I hate the details :)

Back to your killer worth and saving/investing though – Absolutely BRILLIANT. It’s amazing how different you see things when you’re actually tracking the #’s right? Motivating as hell! Even when it goes down (which it will – cuz most of the $$ is/will be tied in the markets) it’ll still be great to *know* where you stand. And really you can only do so much within your control, which you’re now learning to rock.

Keep pushing along and pouring all that $$$ into the “system” baby. It’s totally cool to splurge and have fun too, so don’t get too hardcore! Don’t want it to all go to $hit if you burn out :)

Keep me posted brotha. And sorry again for such a lame delay.

Hey hey hey!

Until I get the time to sign up on your rockstar finance net worth blog I am going to use this comment string to keep track of things.

Net Worth @ 6/1 = 65,731.93

I am still chugging along sitting at 27.72% up since the beginning of the year!!

I had to extend the lock on my mortgage due to some issues with the estate I’m buying from.. so that will cost me a little extra $$ but will also give me more time to save up for it. I’ll be happy just as long as I can keep the 3.6% I locked into :)

Thanks again for the wise words and for calling out my comment last month. Keep on keeping on my friend!

– John

You too, my man. Life is good!

Yo J. Money!

I’m back again. Ready for a Q2 update?!?!?

Net Worth @ 7/1 = 67,093.93, that’s up just over 30% for the year!!!

Had to extend my lock (again..ugh) so that money is still sitting in cash reserves waiting to be used on the closing costs. I’m still happy I get to keep my 3.6% rate though and should close within about a week.

That market sell off on Monday certainly hit me hard but I resisted the urge to sell. I am thinking a market correction could happen sometime soon if this whole Greece situation doesn’t work out. If that is the case it would be good to have a little cash reserves on the side to invest on the dip…

Oh yeah – when the market is down it’s a damn good time to buy! Especially for those young folks like us who have time on our side…

Congrats on the increase my man. You’re blowing up! (And wish I could get an interest rate @ 3.6%, wow. Hell, I’d be happy at anything below 5%!)

Hi JM,

I visit your site a few times a month. I am old-school, so the transparency is very unnerving. But hey, I’m learning from you nonetheless. Congratulations on your progress!

On the topic of retirement, I just read Wess Moss’ book. He has an interesting perspective on how to get to a happy retirement and then what to do when you get there. I enjoyed it.

Lately, I seem to be doing more research on multiple streams of income. Kinda good to think of it before that day I get off the career treadmill.

Keep up the good work!

Thanks JC!

It’s probably unnerving because people don’t talk openly about this stuff in the real world (at least w/ transparent #’s), which is exactly why I do it here on the blog :) Gives us something hard and real to look at and allow for some good discussions!

If you like seeing other peoples’ numbers, try out my blogger net worth tracker on my other site that links to over 150 bloggers sharing their #’s – it’s pretty wild:

http://rockstarfinance.com/blogger-net-worths/

And the nice part about it is that everyone’s getting into all sorts of different income streams which they share on their blogs :) For some it’s dividend stocks, real estate, or passive income, and others it’s entrepreneurship or hustling on the side, etc.

Pretty cool community we’ve got here. Always ideas to explore :)

Hey J Money. That drake song is hilarious because it fits pretty much for most of us net worth bloggers. It was actually your blogger net worth link that finally converted me over to start tracking mine also. I really appreciate you making that page and keeping it updated.

You rock bro!!

Nice! Love to hear that! Welcome to the dark side! :)

Hi Jmoney, what do you think of this? I just read it on the Cheat Sheet website: “I have found that retirement is all about cash flow, not net worth, especially after the real estate crash. I have met people who have a net worth of $2 million, which looks great on paper, but when it comes to retirement income, they are just barely squeaking by on their Social Security and a small pension. It’s great that you are worth $2 million, but ultimately, it’s your cash flow that will determine your quality of life in retirement, not your net worth.”

Read more: http://www.cheatsheet.com/personal-finance/7-quotes-that-will-motivate-you-to-save-money-for-retirement.html/?a=viewall#ixzz3e4ZB9pt4

I think having both cash flow AND a nice net worth is ideal :)

But yeah – you can only “retire” when you have enough money coming in to cover your expenses. So if you have a house worth $10 Million that you’re living in but no paycheck, then you can’t survive so you can’t retire (though of course you can always sell the house and then voila!). On the other hand if you had $10 Million in stocks then of course you can start pulling from them – or better yet, live off the interest/dividends – and can do whatever you want now.

The point of tracking your net worth is really to get a good snapshot of your entire financial life. Assets, debts, everything. It doesn’t necessarily tell you that you can do one thing or another, like retire. Your expenses and income will tell you that part.

Here’s a spreadsheet I put together to help more with that actually:

https://budgetsaresexy.com/2015/02/early-retirement-fi-spreadsheet/

Also, it’s important to note that everyone calculates their net worths a bit differently too, depending on their goals and what they want to get out of that #. Some income cars and houses while others’ don’t, and some include all personal items (furniture, jewelry,etc) that others don’t. Just depends on what they’re trying to get out of their net worth, other than the more common “financial snapshot” idea which is why I personally track it.

Here’s a list of 150+ other bloggers’ net worths which you can check out and see how (and why) they’re doing it their way too:

http://rockstarfinance.com/blogger-net-worths/

Point is, cash flow and net worth are two different things. And in a perfect world you’d have a lot of both :)

JMoney,

Agree on the Net Worth thing. However, looking at your Net Worth tracker and then following along with the Retirement Calculator the above message references. There seems to be a disconnect.

It appears the majority of your net worth growth comes from Contributions. And a hearty congratulations on the discipline to move the needle as you have. On the retirement calculator you reference an anticipated 8% return on investment though, and the Vangaurd fund pays a divi of 1.84%. and It looks like you anticipate to scale back the contributions amount to $ 13,000 annually.

One thing I like to do is look at investable assets as a percentage of net worth. Yours looks fine. But when you consider that the majority of your net worth is tied to investments, you might need to have those investments work a bit more for you than the one Vanguard fund allows to meet your goals.

Perhaps I missed something and the Vangaurd index fund is tied to only a portion of your investments. Alternatively, the Roth and Brokerage accounts are where you seek greater returns. Is that the case? Did I miss something? By contrast. I have a 19.36% growth in my Investable accounts this year for a total 82K gain. I’ve funded those accounts with 20K so far this year. My point being that you are obviously great at managing to save and invest. At 400K plus in investable assets, if you are not proficient in this area, you may wish to seek an advisor to manage that 8% ROI. (Disclaimer: I am not an advisor)

For additional Reference in Jan 2011 My Net Worth was 291K Today it stands at 604K. Investible assets 192K and 502K over that same period of time. My contributions to investments are roughly between 20-25 per year including company match.

By the way, I’m a bit older, not without my shortcomings to getting to retirement as I was slow to recognize that throwing money in was not enough, as well as not throwing enough money in early as you have. I’m also a lurker, come back from time to time to check in. Have posted a couple of times previously. 4-5 yrs lurking, Have a spreadsheet that tracks back to 2007. Save at end of the year and refresh with a new one that continues to track summaries back to 2007. Looks forward too, including Social security calculations.

Nice man! You are doing a helluva job now that you’ve figured it all out :) Thx for stopping by and chiming in (and for reading for so long!).

To answer your overall question – I’m not an expert in this area and always learning and tweaking to get closer to my goals. In fact, investing is the part I suck the most at and which is why I went straight to Vanguard index funds – easy, simple, and powerful! And since everyone I look up to and admire in the Early Retirement field does the same, I knew it would be the strategy for me. As for the 8% you’re wondering about – that’s the growth of the funds themselves, not what I expect to get in passive income/dividends. That will be much smaller unfortunately.

I’m still learning as we go here, but for now I’m pretty content with how things are shaping up. I just need to get better at shaving expenses and banking even more as time goes on to hit ER sooner! :) But I’m trying to enjoy the ride (and my life – hah) in the process.

All the best, I realized that I left the growth factor a bit lacking in that message, but I also think you will find that in most investment senerios the compounding of the dividend/income is what drives portfolio performance rather than capital gains. We are in a wonderful period where everything is coming up roses. But if you look at other L-T periods the market can be rather stagnate for capital gains. Something to consider perhaps.

Just as an example (and anyone can cheery pick data to make a point as I admittedly have done here) The DJIA was at 11,497 in December of 1999, in Dec 2011 the DJIA stood at 12,217. Just a thought.

As for myself, I only wish I had it all figured out. And I’ll give you props for getting me started all those years ago as I took the basic structure of your Net Worth spreadsheet as a starting point. Attention to many of those details; evaluating my actions and results has been a big help, so thank you for that.

Regards,

E

Glad to hear it! That’s the key start of it all really – tracking your net worth to wrap your brain around things. Once you’re on a mission to grow it, all the other decisions in life can be handled better :)

J. Money,

Do you have a downloadable template file for tracking your net worth you can share with us? I am interested in starting to track mine and would love to see one of yours.

Thanks

Hey Parker,

Sure, the one I use is an adapted version of this one here (it’s a budget + net worth tracker all rolled into on – woo!): https://budgetsaresexy.com/budgets/j_budget_template.xls

And then here’s a much simplified looking spreadsheet here I use for my $$ coaching clients: https://budgetsaresexy.com/files/Money-Snapshot.xlsx

In a nutshell though, all you need to do is add up all your assets one one side (cash, savings, investments, 401k, etc) and then all liabilities on the other (c/c debt, loans, mortgages, etc). The difference is your net worth!

your graph is really sexy. what’d you use to make it?

Hah! Just good ol’ Microsoft Excel :) With a dash of gradiant action, haha…

Thank you for the inspiration! I love the way this looks so I’ve finally gotten around to making one of my own here: http://www.unchained55.com/net-worth-updates/

Thanks again! :D

Beautiful! Love the graphs you’re incorporating, and even more so that you just surpassed me :) More fuel for me to keep on going! Haha.. well done.

You are making great progress towards your goals, I have been tracking with the personal capital app as the numbers on the educational loans tend to fluctuate, I find it easier to track this way.

Love what you’re doing here, J. Money. I never thought about keeping a public tally of my net worth. But … if you have goals, then making them public is a great motivation to sticking with those goals. So I’ve made my 2016 goal public and laid out the families net worth here:

http://www.beardsandmoney.com/the-beginning-beard-and-net-worth-month-1/

We’re doing better than the average family our age, but that’s a low bar. It’s also ridiculously low considering my fairly decent salary and how much we’ve realized gets blown on ridiculousness. If we can follow our new plan, then we should see that bottom-line number spike.

We use Mint for tracking. Personally, I LOVE Personal Capital. Much better interface and I love the cash-flow tracking and lack of ad after ad. But, PC can’t connect with our main checking account right now. According to their support, their working on that, so when its all done, I’ll switch back to tracking with them.

Yeah dude! Loving your blog over there – Beards and Money – what’s better than that??? :) Been fun reading your comments around the blog and getting to know your story more. We totally need to grab bears one day – would be fun.

This is super interesting, thanks J Money!

Does anyone know of a broader list like this, where people voluntarily publish their net worth?

I am working on a project where we are building a model to predict net worth using home values and income, and need some good data points for my training set.

Thanks!

Nice!

And sure do :)

As luck would have it, I’ve been building out a list of ALL personal finance bloggers who publish their net worths online, and we’re now over 200 strong:

http://rockstarfinance.com/blogger-net-worths/

Hope it helps!

You have come along way in 8 years Mr Money! Well done! Who knows where you’ll be in another 8! I’m guessing very well off

Thanks man – we’re trying :)

Hi,

I keep track of my net worth similarly and have done since 2007. I have always updated long term assets like property when I get them revalued, usually once a year. I’ve recently started investing through a company structure though and have learnt that accounting principles state that I should not do this until such time an asset is sold and a gain is realised. Therefore my accounting software reports a different net worth to my personal excel sheet. Do you revalue your net worth as you go or do you wait until you have actually realised the gain? Should I be doing both methods? I know for accounting records I can’t revalue but I also won’t have an accurate net worth if I don’t right? If I hold a house for 40 years and it still shows the original value it will obviously be way off….

Thanks.

Nice work tracking it since ’07 – that’s awesome!

There’s really no right or wrong way to track your worth here (and I don’t have a clue as to “accounting principles”), but what’s important is picking the route that best makes sense to YOU. What are you trying to get out of it all? Do you like seeing an overall snapshot of your money like me? Are you using it to gauge early retirement or cash flow? Do you want everything to be liquid like some people do? Does pre-tax vs after-tax matter at all?

Lots of variables and methods to tracking :) But to answer your question – yes, I update my worth on a monthly basis and do my best to calculate harder things like real estate and other such holdings whenever it makes sense (I used to use my realtor to help determine that every handful of months vs Zillow or other less-than-accurate places).

There are some parts I leave out though like what my businesses/blogs are worth or even all my personal property (including my coin collection that’s semi-valuable), but if at any point I sell any of those it’ll then be reflected in my net worth which will (hopefully!) pump it up in that month. So everything does eventually get calculated, but just at different times.

Not sure if anything really helps, but know that either route you choose is perfectly fine :) Just adapt it as time goes on and your beliefs shift, and all will be well in the end. Great questions though.

Recently came across your blog. You’re doing a great job! I agree keeping track of my net worth keeps me accountable and encourages me to save even more! https://twentysomethinglawyer.wordpress.com/2016/05/24/my-first-million/

Thanks! Way to stay on track of yours as well :)

Funny timing…..we just bought a car in June too. Took at $11K hit for it though. Ouch.

I know the feeling! Good thing we won’t have to get a new one anytime soon :)

Thanks for sharing your journey! I too, am working on my findependence! Do you have life insurance and do you make that part of your networth?

Cool! It’s a great thing to be reaching for!

Yup – both my wife and I have life insurance: $350k each of Term Life. We don’t make it part of our net worth, but in the unlikely case it’s activated in the near future it’ll of course affect our overall wealth. I really hope it doesn’t though! :)

Do you also track your exposures to your net worth?

Everyone I read on personal finance blogs talks about their net worth, but doesn’t give credit to the insurance protection in place of their net worth. it is a critical component.

If your home burned down, the $500k would take a hit. Or if you get in a accident with high net worth individual you could have out the top exposure on your auto policy, therefore need an umbrella policy. Similar could occur on your umbrella policy if you were at fault hitting a hedge fund employee.

These are the things I think about when writing on my site.

For sure!

I don’t think it belongs in the Net Worth itself, but of course you want to protect yourself so you get to hold onto your $$$ more :) Wouldn’t be a bad idea actually to include it in your overall financial spreadsheet where other things go too? I’m making a note now to do so myself…. I like that idea!

And for those who are wondering, we do have all the major insurance going on to cover our lives (auto, house, life, and umbrella too). Sucks to spend the money on it, but hey – better to be alive and healthy and not have to touch! :)

Thanks for stopping by.

Thanks for your great post! I’m at the beginning of my investment journey and have just started tracking my net worth each month. How did you make that graph? It would be interesting to visualise it over the years.

Good ol’ fashion Excel!

I still rock some way old version of it (2010 or 2011 I think?) and does the trick just fine :)

Bro I liked your style of tracking so much that I’ve done the same for my website:

http://www.fromcentstoretirement.com/my-net-worth/

Thanks for the inspiration, I hope you don’t mind.

Good luck!

Rock on!

Love the breakdown pie chart on it too :)

Is this your family networth or your individual networth? I’m tracking mine separate from my husband but maybe that is a silly thing to do…

There’s no silly or right or wrong way to do it :) gotta do what makes the most sense for ya! All the bloggers I know sharing theirs track it all sorts of different ways:

http://directory.rockstarfinance.com/blogger-net-worth-tracker

To answer your question though, everything I track here is our *family’s* net worth. Outside of the first handful of years when I just tracked my own until we eventually combined accounts.

Hi , thank you for creating and maintaining this blog about your journey to financial freedom. What do you think about my situation? I am 32.5 years old with a fiance and no kids. My fiance is working full time. My credit card debt amounts to $275, retirement savings of $57,000 and stock portfolio worth $290,000. I earn $4200 a month from wages (after tax and retirement savings), and $1200 a month from dividends (after tax). My monthly expense is $1800. I started saving and investing 6.5 yrs ago.

I would say you are well on your way and would shake your hand :) Especially after only 6.5 years of working towards it – congrats! At that rate and expenses you’ll hit financial freedom in no time.

Hi J! I’ve been reading your blog and I have a massive thank you for your inspiration. I recently launched my own blog about personal finance, frugalism and minimalism to fight anxiety and I don’t think I would have dared a few months ago. Your insights about breaking the taboo around money has made me a very open person about it and I have you to thank for it!

So glad to hear it! I hope you really enjoy blogging – never know where it can lead! :)

I admire your progress. The thought occurred to me. How are you planning to retire early if the bulk of your assets are in retirement accounts that you can’t touch without penalty until you Are 59 1/2? I am older now and face the problem that the bulk of my assets are in such accounts.

Thanks for stopping by!

Two things – I probably won’t ever retire-retire early as I’ll continue working on stuff I love that’ll prob bring home money, and then secondly I plan on opening up a separate brokerage account at some point too to start investing in outside of the retirement accounts. Although, some of my friends on other FIRE blogs have figured out how to convert over IRAs and such where you can still pull money out without penalty if you do them the right away. Look into “roth conversion ladders”.

Here’s a great article (and blog) on tapping your retirement funds earlier w/out penalty: http://www.madfientist.com/how-to-access-retirement-funds-early/

Good luck! :)

For a Brazilian, what automatic tool is available to track net worth?

I don’t know about *automatic* ways, but luckily spreadsheets and pieces of paper work just fine around the world ;) Only takes a few mins to update it every month – don’t let the fancy tools stop ya!

Great progress and tracking. As you said, just keep stashing as much as you can in your Roth IRA and 401K. As time goes by, it is amazing to look back and see how those accounts grow.

Yup! Even if that’s all you ever do every year you’d be set!

I find that it is really awesome to see the growth from the early days to now – the grind is real!!

Looking forward to reflecting on my own journey as I’ve gone from negative to +40K net worth thanks to these markets and also my diligence in saving.

Keep doing your thing man!

Nice! It all takes time but if you don’t start it’ll never add up :) Tracking it gives you a nice boost over time too – highly recommend!

This is probably one of the longest and more complete net worth compilation that I’ve seen. Excellent work on maintaining this website and the follow-up. Like the transparency and the simplicity (easy to read).

Bookmarked to keep an eye from time to time.

Excellent work J. Money! Have an excellent journey into your first million! :)

Thank you sir! Glad you like! :)

Thank you for sharing your story. Going through and looking at your net worth, it helped me to notice the down months as much as the up ones. It doesn’t matter in the end, things always go up if you wait long enough.

Oh yeah… It’s never a straight line! And I’m willing to bet this year will show a lot of those downward drops too :) Just gotta keep that long-term perspective!

This is awesome J$.

I’ve been meaning to dip my foot into blogging and you gave the final push I needed. I wrote my first net worth update yesterday (https://www.windespair.com/net-worth-april-2018/)

It’s nice to see real numbers and how you’ve killed it over the past 10 years.

Thanks for the inspiration!

LOVE IT!!! Such a fun thing to take on, blogging. (And tracking your net worth for that matter :)) I hope you enjoy it and helps keep you and your money accountable!

OMG! Recent follower and wanted to share that I started doing this also about 10 years ago (2009) for family finances. I cannot wait for each month’s end to see the new numbers. Totally motivating and a great way to adjust as you go. Keep up the good work J$

Glad to hear, SA!!! Makes such a difference for your finances, right?? :)

Great Job J! If my math is correct, that’s a 93% increase in wealth in 10 years, not to mention nearly 7 figures, that’s amazing! I’m guessing it’s a testament to discipline, saving, earning, and delayed gratification. For all of us striving to get here, J shows us it can be done! Great work bro!

Thanks man :) Yup – all about patience and getting that foundation down really… Then it’s harnessing that great power of time to do the rest!

In your monthly updates, displayed are savings accounts, brokerage and ira accounts, do you factor your house value into your net worth? (My wife and I just surpassed the 500k net worth this year-house worth minus remaining loan included )

Half a millionaire! Congrats!

We used to include our house when we owned one, but now we happily rent so no longer applicable ;)

Hi ,

I am 26 years with a net worth of about -20,000 … I earn about 50k a year how possible is it to save .

Thanks

It’s very possible if you care enough to make it happen :) Keep searching around $$$ blogs and trying out new things until you find stuff that sticks! People have done it on far less than $50k/year!

Did you post your net worth statement yet? I can’t find it

Our latest one? Just dropped this morning:

https://budgetsaresexy.com/new-net-worth-record-791k-down-61k/

This is one amazing journey. Thanks for posting this.

Hope you’re tracking yours too! :)

This is great. You are getting close to a new milestone.

One of these days! :)

Hope yours is going well too!

And how much alone from blogging?

I’d say it’s a pretty decent part of it, but keep in mind it’s my day job so if it weren’t the blog bringing me a salary it would be a different job ;) Though I have sold a few of my online projects over the years that certainly contributes to it.

Here’s a recent breakdown I did that shows where a bulk of the money came from:

https://budgetsaresexy.com/how-we-grew-our-net-worth-to-over-900k/

Hey J Money,

I know this may be a difficult time, but would love to see this updated? My 401k has been decimated and I was on a similar trajectory as you (but smaller scale).

Also, what’s your feeling on going in on the market now? I missed out on 2008 bottoms, don’t want to do that again.

Yeah man, it’s wild out there right now! Def. not a millionaire anymore, lol, but just a matter of time until it climbs back up again so I’m not totally worried. More afraid of my family’s *health* than anything! The money’s not going to be worth much without that!

But to your questions – My strategy remains the same of keep throwing money in each month as available and riding it out for the long haul. And while our $$$ has dipped pretty substantially here, gotta keep my promise to the family of no longer disclosing the details here, though I’ll still share how we’re doing generally as I have been the past 6+ months since selling the site…

Keep staying strong over there! It’s all temporary!

Hope you made it back over a million J. Money! Awesome to see these recaps all in one place. Thanks for taking us behind the curtains, and best of luck moving forward!

Indeed! Wild times in both the market and life these days! Thanks for stopping by the blog :)

It is pretty cool to see this data being shared for over A decade now. Interested in how you track your net worth including real estate, collectible and other assets that aren’t held in accounts.

Congratulations on the $1M milestone! It’s pretty cool to see a precise net worth calculation (down to the penny!) going back for over a decade.

Do you track your monthly spending with the same attention to detail? My personal experience with using a budget / net worth tracker to track my spending is that it’s a lot of work to set up and maintain. Often, I simply want to be able to search my past purchases and see how much I’m spending, without setting a budget.

Ended up building a tool called Fion (fion.co) to search my past transactions, across all my cards, and actually see how I’m spending money. It’s more insightful than a basic “tracker” app when I want to look up a specific purchase and much easier than following a strict “zero-balance” budgeting methodology. Already making better spending decisions with it.

Cool, thanks for sharing. J$ uses personal Capital every day – I use Mint for budget tracking as well as manual spreadsheets to back-up all the raw data. So cool to see all the new tools out there today that are helping people get into the right habits. Cheers!

Love the transparency man! As a new blogger (personal finance for teachers), I’ve learned a lot from you on how to build an audience that trusts and believes in you. Thanks for all you do!

Thanks for sharing such beautiful information with us. I hope you will share more info about financial planning

Is there a system or a way to be able to easily account for balances that can’t be connected to Mint/Personal capital?

For example, I have some money in real estate syndications and some money in NFTs that can’t be connected/updated to my Mint account.

I guess the best way to do this is just to do a monthly accounting to see where you’re at with those unconnected accounts?

Hey Angie! Yeah I think just monthly manual tracking is the way to go for now. :)

This is an incredibly inspiring journey—congratulations on hitting the $1 million milestone! Tracking your net worth so diligently over the years is not just motivating; it’s a masterclass in persistence and focus.

One thing I appreciate is how you’ve emphasized the accountability and reflection aspects of tracking. That monthly pause to review your numbers is such an underrated practice. It’s a reminder to not just set goals but to continually engage with them.

Also, your point about fees in retirement accounts is golden. For anyone who hasn’t done this yet, running a fee analysis could be an eye-opener. The potential savings could easily redirect more money back into your net worth growth.

You know it!! Compounding works for debts/fees just as well as it does investments! Gotta always be harnessing it towards the right direction! :)