For every “movement” where a group of people band together and try to improve their lives, there will always be a handful of nay-sayers trying to discredit the cause. The financial independence FIRE movement has a bunch of these haters. And while some concerns about early retirement might be legitimate, the most common objections I usually hear are myths (or personal limiting beliefs).

“Haters gonna hate. Potatoes gonna potate!”

It’s my opinion that “hate” really just comes from a lack of understanding. So my hope in this post is to explain a bit more about each of these common FIRE movement myths and expand on the reasons why I believe they’re mostly untrue.

Myth #1: The FIRE movement is only for young folks.

I can see why people think this. From the outside, it appears that FIRE walkers are a bunch of kids in their 20s and 30s. But, the deeper you dig and more entrenched you become with the community, the more you connect with people in their 40s, 50s, 60s and older. We’re all prioritizing financial independence by learning, sharing, and helping each other — no matter our ages.

One of the reasons I think this myth exists is because younger folks have a louder voice. Whether it’s new blogs, posts on social media or getting featured by news outlets, it’s usually the younger “success stories” that are published and shared the most.

Also, since time plays a big role in building wealth, some people believe financial independence can only be achieved by those who have decades of time up their sleeve. This simply isn’t true. While a young person might have a bigger time benefit, it’s not the only factor involved in building wealth.

We published a great article a few months back from Late Starter FIRE, written by an Aussie gal who discovered the FIRE movement when she was 47. Since then she’s encouraging more people in older age groups to join the community. Check out her Late Starter Interview Series with 25+ similar stories about people discovering FIRE movement “late” in life.

Myth #2: The whole point of FIRE is to stop working as early as possible.

“Early retirement” is just one single M&M within a massive bowl of delicious candies. (Excuse the weird reference, I’m staring at a pile of leftover Halloween treats on my desk!)

What I’m trying to say is that quitting your day job is only 1 of 100 benefits of getting your financial life in order. Retiring early might be the initial reason some folks are attracted to FIRE, but it’s not the main reason they’re sticking around.

In fact, most FIRE followers who are in a position to retire early are choosing not to! Somewhere along their journey they’ve found work or careers that they truly enjoy. They’ve found activities they are passionate about and work that adds value to their life.

Retirement is not the sole purpose. (In fact, it’s not really even a purpose at all).

To me, the FIRE movement is all about figuring out what the heck you want to do with the rest of your life. I want to slow that process down, not speed it up. Many other FIRE folks are jumping on the Coast FI train… Learning to identify work they want to do less of, and replacing that with stuff they want to do more of.

**You’ve probably already noticed a lot of people dropping the “RE” from the FIRE acronym… Shortening it to “FI” shows they care less about the “retire early” bit and more about the financial independence or financial freedom side.**

Myth #3: You probably need $5 to $10 million to retire comfortably

If you ask the average person on the street “How much money do you think you need to retire?” they’ll likely ballpark an extremely high dollar figure. It’s mostly based on feelings, not mathematical retirement planning. Actually, even some personal finance gurus ballpark that $5-6 million is the amount of investable assets everyone needs to retire comfortably. I think it’s crazy!

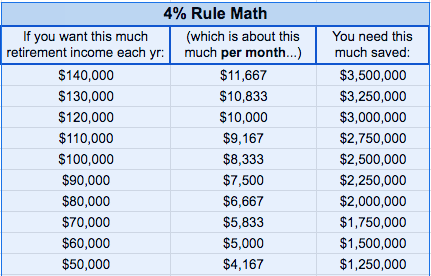

The most popular method the FIRE community uses to calculate how much one needs to retire (also known as your “FIRE number”) is the 4% rule. And since most of you already know what this is, I’ll save blabbing on explaining it in this post!

Anyway, what’s important is that the 4% rule uses your annual expenses to determine the size of your retirement nest egg… And since everyone’s annual expense is different, everyone’s retirement number is different. Check out the chart below with figures based on the 4% rule and desired retirement income…

Some people will need a bigger nest egg because they plan to spend a lot. Others need less because they can live on less. In my opinion, the average early retiree doesn’t need anywhere near $5 mil invested to retire.

What shits me to tears about this FIRE myth is that spreading a one-size-fits-all “magic number” for retirement can be harmful for people just starting their financial journey. Most people can’t fathom a $5 million retirement fund, and unreachable numbers can kill the motivation to start saving or investing in the first place. I’m not suggesting people should aim for low numbers; I’m suggesting that people learn the realistic numbers that suit their individual scenario.

Myth #4: You gotta have a mega high salary to become financially independent, or retire early.

Income is only part of the FIRE equation. Here are 3 main areas that make the most impact in building retirement savings (listed in order of importance):

- Reduce expenses. “A dollar saved is worth more than a dollar earned”

- Learn to invest intelligently. “It’s not how much you make, it’s how much you keep.”

- Grow your income. And be careful of lifestyle inflation :)

While a young person with a ridiculously high salary certainly has potential to build wealth quicker, or retire earlier, high income is not a necessity for FIRE. Just focusing on the first 2 points above is more than enough to drastically turn someone’s finances around.

Check out this awesome FIRE blogger, EducatorFI, who is living proof that low income earners can slash debt and build wealth quickly, by focusing on making smart financial decisions. Also, check out the interview series with 30+ other educators who share how they are improving their finances, while doing work that matters! (I have a soft spot for teachers – my wife is one!)

Also, remember growing income doesn’t always mean getting huge pay raises at work. Picking up a side hustle is a fun way to make a bit of extra money!

Myth #5: FIRE is for tight-asses who practice extreme frugality

I gotta laugh at this one. Personally, I have no issue with extreme frugality, but I can see why it rubs some people the wrong way.

There will always be enthusiasts who take money recommendations to the extreme.

For example, if you tell a group of people to “try lowering your expenses,” most people will cut out a few spending luxuries and be done. But, there will be a few creative thinkers within the group who will take the task as a personal challenge. They will try everything they can to reduce their expenses all the way to zero, even if it kills them. For them challenges like this are fun!

But these extremists make up a small number within the FIRE community. The majority of folks recognize that every rule about money is more like a guideline… They follow along until they experience diminishing returns, or when it impacts their happiness.

The FIRE movement definitely promotes reduced spending and a frugal lifestyle. But really most people only cut back on the things that don’t provide long term joy. Spending less on crap allows for more spending on things that provide value.

Myth #6: The FIRE movement is just a fad. People will lose interest when the stock market crashes.

Some people believe that when the next big stock market crash comes, the FIRE community will dissipate. Losing a butt-ton of money in a short period of time will test everyone’s faith, and shatter everything we’ve been working towards.

Well, this misconception was already proven wrong earlier this year. When the covid 19 pandemic hit and the stock market tanked, most investors lost over 30% of portfolio value within a couple weeks! But, everyone in the FIRE space stayed the course and stuck with the plans.

In fact, the FIRE movement actually gained a ton of traction and followers during the last market dip. It’s in dire situations like this pandemic where people actually wish they had learned more about FIRE earlier.

In my opinion, the FIRE movement will always exist. I can’t imagine a world where people don’t ever want to improve their financial lives and consistently work towards being happier and more free in life!

So, there you have it! What do you hear about FIRE or reasons people think it’s no good?

Happy Monday! Y’all have a kick-ass week!

Get blog posts automatically emailed to you!

Joel,

I am SO happy that you explained that the FIRE movement is not always about practicing extreme frugality. I’ve actually come across many people who believe that the FIRE movement is about crazy extremists who essentially live under a rock in an effort to save money – and I don’t know how many times I’ve had to correct this common misconception.

Well said.

Another point – I’m super glad that you illustrated that there is no “magic” number someone will need to retire. It’s so difficult to say how much you’ll need for retirement because it simply depends on your cost of living.

The Millennial Money Woman

A couple years back, my wife and I went to an all inclusive resort in Mexico. I told a friend about how I got a massive discount by quickly searching a few different websites to find this killer bundle deal… He then called me a “tight-ass” because I’m always looking for discounts.

Everyone’s got a different view of what being frugal means. My friend thought looking for discounts was being a tight-ass. I thought the complete opposite, because dropping $4k on a drinking holiday isn’t frugal at all. :)

Yes, this perception of frugality is so interesting to me lately.

My partner and I were laughing the other day about the date we chose. There is an (Australian) local charity called Share the dignity who request individuals fill a bag with sanitary/ hygiene products to be passed on to women in need. We chose to set a budget (what we would have otherwise spent out at dinner) and wander around the shops to find the best specials or bargains to fill this bag with.

When we told this story to some friends, we were having a giggle about our idea of fun, our bargain hunting was to the benefit of someone else, (they got an overflowing bag of products) but despite the fact that all intents and purposes was positive to this bargain hunting….. they were so uncomfortable just talking about the idea of budgeting or trying to save money.

Wow! If you didn’t get discounts, your bag of products would be half as full. Bargain shopping + charity is a win/win! It’s funny some people don’t see it that way. Thanks for sharing – and thanks for donating! Great date night!

Frugality has allowed me, as a woman, to be able to stay home and not work full-time for some of the 30+ years since we have been married. I know many women have to work or choose to work because they love it but I love staying home. I lost my temp job in March because of Covid and I am currently loving staying home. I have a little part-time job I do at home doing transcription but it is very low hours. I have helped out financially. I have usually made more per hour than my husband but I was able to work less hours in total, during the years that I did work. Several of the years I did work while my son was young, I was able to work from home and I also homeschooled him, so that worked out good. We are debt free and are able to travel and enjoy our lives but our needs are much, much less than many people. Essentially, I guess I am saying the FIRE movement allows you to do what you choose to do in life, no matter what type of decisions you make.

Thanks for sharing Chris. I think your story applies to Men also… FIRE has helped me take a few years off and stay home – which I absolutely love. :)

Great debunking of myths, Joel!

And yes, we can pursue FIRE even when we are older, with low incomes, with lots of kids or none, suffered setbacks such as divorce, addiction, crippling debt and so on – all demonstrated by late starters who generously shared their stories. Our FI numbers vary, depending on our circumstances and expenses. But we will all reach FI despite starting late. And Professor FIRE is adopting Coast FI so that’s not just for the youngsters either! :)

Thank you for the mention!

Thanks for continuing to encourage older peeps to get involved. Your interviews are very inspiring! Cheers LSF!

As an older person, I agree with the busting of several of those myths, especially the last one.

This year has not been the old hard hitter for me: 2012 was awful (go look at that dip *cries*) 2004 was also crazy… (notice the eight year trend? Not saying 1996 was also bad… But these things will happen, they may go in cycles. Just be mindful and keep your strategy going.

The nice thing about 401K and those investment portfolios where you are placing an amount in every month is when the market goes down or tanks, that same amount you are investing is getting more units of whatever you are getting, then as it increases, those more units do more work!

Good note on dollar cost averaging… Dips in the market are our friends (while building wealth)! Slow and steady wins the race :)

My boomer dad is mystified at how I could possibly have any kind of self-identity if I retire early and don’t have a job (…but then he was with the same gov’t agency from 1975 to 2011). My boss — a trusted colleague of thirteen years — gets confused when I occasionally decline projects that don’t interest me because I have the comfortable security of fat investment accounts, modest expenses, long tenure, and a wife who makes more than I do.

I really haven’t brought up the idea with folks, though. We had every advantage growing up, landed secure careers before the great recession, and bought a house in 2010 at the very bottom of the market. It would feel disingenuous to pretend we’re some kind of exemplary FIRE devotees when our present circumstances are >90% luck.

Thanks for acknowledging your privileged background. I fall into this boat, too. Luck plays a huge roll – and will continue to in the future, as long ats I keep trying my hardest!

You guys know that it was not luck. You guys did make the decision to save and invest. You could have easily spent all that money. Acknowledge that you made good decisions with your money that put you into this position to grab the opportunities that present themselves to you.

As a 51 yo, I commend you both on achieving what you did at your age. To have the flexibility to do what you do at your “young age” and the drive you have on your current projects, I salute you.

Keep up the good work!

Thanks for your encouraging words! You’re right – hard work and sacrifice is needed, no matter one’s advantages.

Congrats on your soon to be retirement! Have a great week!

Nice article. What is so nice about FIRE, you don’t give a rat’s ass about cutting expenses all the time.

This weekend, we had to replace the trunk lift struts on our Subaru Outback. I looked online and called Subaru for prices. For two lift struts, the price was $60 at Subaru. Online, I could have gotten them for $50, but had to wait two days. I drove three miles to pick them up at Subaru and within the hour installed them and the trunk opens nicely.

In my mind, I saved $200 by not having the dealership do the work and I didn’t waste time looking for coupons for 10% off. Granted 10 years ago, I would have been looking for an hour for a coupon for 10% and not felt good about paying $60 or would have waited a week to get the lift struts shipped for $50. Ha ha.

I am 51 and retiring in three years, life is good for RE. Time is money. Lesson of the day for me.

It definitely gets easier and easier as you build more wealth to spend money in order to save time. Great story on the trunk fix. Back in the day I would have probably just used a long wooden stick to hold the trunk open haha!

we got a late start too and didn’t open a brokerage account until i was 37 or 38 in 2006. it took 15 years of good investing to get to the prize. we did all that without deprivation of any kind. i don’t know if i’m in the FIRE community as i’ve never been much of a joiner, but i do write in the personal finance space.

even though i’m 52 and kind of been there and done a lot of that i’ve enjoyed writing the malevolent missy series to demonstrate how a younger person might start their successful investment journey. it’s good to take some of the mystery and black box thinking out of finance.

Freddy, you’ve inspired way more people than you think. And you’re definitely part of the community :) Your comments and contributions are very valuable, and needed! In case nobody else tells you this… THANK YOU for all your encouragement and support for the young guys. Your Missy series is great btw!!

Really nicely done with this summary here. Useful for busting myths but also nice reminders of key takeaways to keep focusing on for those of us familiar with FIRE. Oh and Late Starter and Educator FI are two of my fave FI bloggers :)

Interview series like theirs always brings new perspectives that are inspiring and REAL. Great to hear you like them too!

I think people who criticize FIRE don’t have the fortitude to do it themselves. Or they think it’s some new creation that people have just discovered in the age of blogs/podcasts.

But FIRE is what many 50-somethings have been forced to do for decades. They have nothing saved (except maybe some home equity) and then they have to rush and save their entire retirement nest egg in 10-15 years before retirement. The FIRE crowd just took that idea and applied it DECADES earlier!

That’s a great way of explaining it! Building up your finances needs to be done at some point in life… May as well learn how to knock it out as early as possible and enjoy the journey. Cheers Josh!

Love the myth busting! Thanks for mentioning me, and I’m glad I learned that your wife is a teacher. How did I miss that?! I love the push back on the one size fits all, particularly related to myths #2 and 3. People will do different things and have different needs!

Cheers Ed! Keep up the good work :)

I am one of those late starters. When I first became aware of FIRE, my goal was just to make sure I would be able to retire at my normal retirement age if I wanted to.

I learned how to calculate how much I would need in retirement and was flabbergasted to find out that I would probably have to work until age 75 (or maybe 4 years after I’m dead), just to accumulate enough savings to retire on.

I used everything I learned from FIRE to reach my goal. I practiced frugality and learned about investment allocation, I stretched the limits of my comfort zone in order to increase my income. I ended up reaching my goal ahead of time and was able to retire early to take care of my elderly mother. I had enough to carry me through for more than two years until Social Security benefits kicked in.

That’s an awesome and inspiring story. You are living proof that it’s never too late to learn, implement good practices, and reap the benefits. Thank you for sharing!!!

Great article and reminder for those that are motivated to get to FI. Like Freddy above I started a little later(28) and definitely was not frugal but was mindful of my spending and savings rate. I love to read the finance blogs because it helps keep me motivated.

The one thing that I think might help more people embrace increased savings would be to emphasize the benefits of having significant savings to weather storms like 2020. The retirement portfolio is almost the cherry on top for me I think the main reason to save is to have savings, period. I can’t imagine as a father of two having to deal with the stress of bills, job security and uncertain times if I was broke.

When the market dove earlier this year, I saw a bunch of FIRE peeps talk about how good their position was because they had emergency funds and all types of contingencies… It was good to see, but, if I’m being honest, a lot of it came off as bragging – which might have made those in less fortunate positions to misunderstand FIRE even more.

I totally agree that emphasizing the benefits of weathering storms would help more people understand better and want to save! The trick is doing it in a humble and encouraging way. :)

Glad you are motivated by money blogs! Me too! Cheers!

“What shits me to tears” is your writing. I don’t typically comment on internet articles, but if you’re going to spend the time writing for a public audience it would be nice if you were to spend some effort making your writing presentable.

Sorry bout that Joe – some of my Aussie slang leaks out here and there when I write. I don’t mean to offend anyone!

Joel, don’t mind Joe. I enjoy your writing and so so many others. Joe is obviously a sad individual and doesn’t realize this site is all about uplifting people and positivity. I like that you write as if you’re talking to a friend versus an audience of people you don’t know. Keep it up!

Thanks for the encouragement KJ! I try and learn from all feedback, both good and bad – that’s how I grow and get better. :)

Have a good one, friend! It’s a great day, to have a great day!

Josh +1

It is sad to see people undercut someone else’s FIRE success (or even attempt) just because they don’t think it is something that THEY can accomplish.

I also don’t understand why so many people get hung up on the RE part, it is OPTIONAL. There is NO requirement to retire once you are FI (I checked the pamphlet).

Bullying someone into NOT attempting FIRE because you don’t agree with retiring early is like ridiculing the gourmet dinner they’re making because you don’t like their choice of desert. I call this “FIRE suppression”.

Life is going to happen to you whether you plan for it or not. On your FIRE journey, something may come up that prevents you from retiring as early as you want to. But whatever it is, you will be in a FAR better position to handle it financially if you have been saving more for FIRE.

What you are saving up really isn’t money, stocks, or bonds. It is future choices and opportunities. I would 100% rather go through something that caused me to “fail” at FIRE than the same event when I hadn’t been saving at an accelerated rate.

If I lost my job right now, it would be an inconvenience. I’d either have to scale back my idea of retirement or find another job (at 50 years old). But I wouldn’t be THAT concerned. I could probably get a lower paying job, coast FI and still retire well before 65.

According to Fidelity, most of my co-workers (same age, income & area) would likely be financially cratered. The median retirement balance is about $65K which is much less than what we make in a year. Being out of work for a year with those starting conditions would zero-out if not make your net worth go negative.

Everyone should be encouraged to get into the FIRE movement. You can talk them out of retiring early AFTER they are financially independent. Don’t throw the baby out with the bathwater (I WILL call child services).

I love how passionate you are Gene. And “saving up for future choices and opportunities” is spot on. Cheers!

You make great points and I don’t really disagree with any of them. I just caution folks a bit about assuming the “4% Rule” will hold up forever. It isn’t like a law of nature or something. And if you want to SPEND $10K, realize that is after tax. Traditional IRA and 401K money is PRE-TAX.

Younger workers seem to think “tax-deferred” means “tax-free.” They put money into retirement plans without planning a withdrawal strategy.

I wouldn’t be surprised if future income taxes are much higher so this may become even worse.

Even now if your state tax is 6% and your Fed is 24% that’s 30% to the government.

I sometimes ask doctors how much they would need to support that level of spending ($10K/mo). They all underestimate the nest egg.

Even when I tell them to consider the tax. They might think they need $120 K or maybe $150K pretax. The actual number is more like $171K. ($120K / (1- tax))

That requires over $4M with a 4% withdrawal and over $5M with a 3% withdrawal.

Thanks for adding this! Yes, there’s a massive difference between tax “deferred” and tax “avoidance”. This is a classic mistake many people make, especially those planning to have high annual expenses later in life. If you haven’t paid taxes on large portions of your wealth, your FI number needs to be higher to account for that.

Good call including income tax in your projection, but I think you’re overestimating.

1) for the income level you state the marginal federal tax rate is 22%, not 24%.

2) Even the 22% is the MARGINAL rate. It does not apply to the entire income.

Plugging the numbers into the income tax calculator at smartasset.com for my state of Idaho that had roughly 7% tax, and remembering to add back the FICA taxes that you will not need to pay on your 401k withdrawal, it looks like they would need a $146,000 income to support $120,000 of spending.

Your main point still stands though. 25x 146,000 equals 3.65 million dollars, which is a lot of money. Supporting $10k/mo takes a big nest egg… Cut that spending in half and the target is much more reasonable!

Cheers!

In defence of RE

Great article Joel! I agree with all points, but would like to add some thoughts on #2.

It seems that every financial independence blog I have read feels the need to distance themselves from the “Retire Early” side of the FIRE coin. I would like to challenge that.

The whole point of the FI side of the FIRE coin for me is to Retire Early from mandatory work, and I’m not ashamed to say it.

I don’t want to sit around sipping pina coladas on a beach 100% of the time after I retire (although I certainly wouldn’t turn down a pina colada if one were offered… :) ). I have a long list of things I want to accomplish in my life that will not fit into a 50 hour a week + family lifestyle. Many of The things I long to do involve volunteering or finding ways to give back and help others.

I believe that most people are good people. Just about everyone will take a break after finishing their working career, but once they get bored with the break and don’t need anything else for themselves the next natural question to ask is “How do I give back and improve the world?”

The RE side of the FIRE coin opens up the time and space to consider that question. The more people that consider that question the better off we will all be.

So if somebody asks me if Financial Independence is all about Retiring Early, my answer will be “hell yeah!… At least for me!”

That’s an awesome way to explain it. Thank you! Work truly is optional when you hit FI. And people definitely need time away from everything to start figuring out what makes them most happy. Love your attitude about giving back and helping others – that’s the most satisfying job of all. :)

I love this! I’ve come across so many of these misconceptions on Twitter & in blog posts, it’s refreshing to read this and dispel those myths. FI really should be for everyone, regardless of age or retirement goals. Thanks for sharing!

Thanks for reading :) Glad you’re thinking the same!

So true about the “$5 to $10 million to retire comfortably” myth! It’s all about figuring out what’s a comfortable lifestyle to you as an individual. There’s no magic number – everyone can discover their unique path.

PS – I liked the honest “What shits me to tears” phrase. Keep up the personality!

-Jordan, FIRE Your Own Way

Thanks Jordan :) Have a great weekend my friend!